Fill Finish Manufacturing Market Size

| Study Period | 2019 - 2030 |

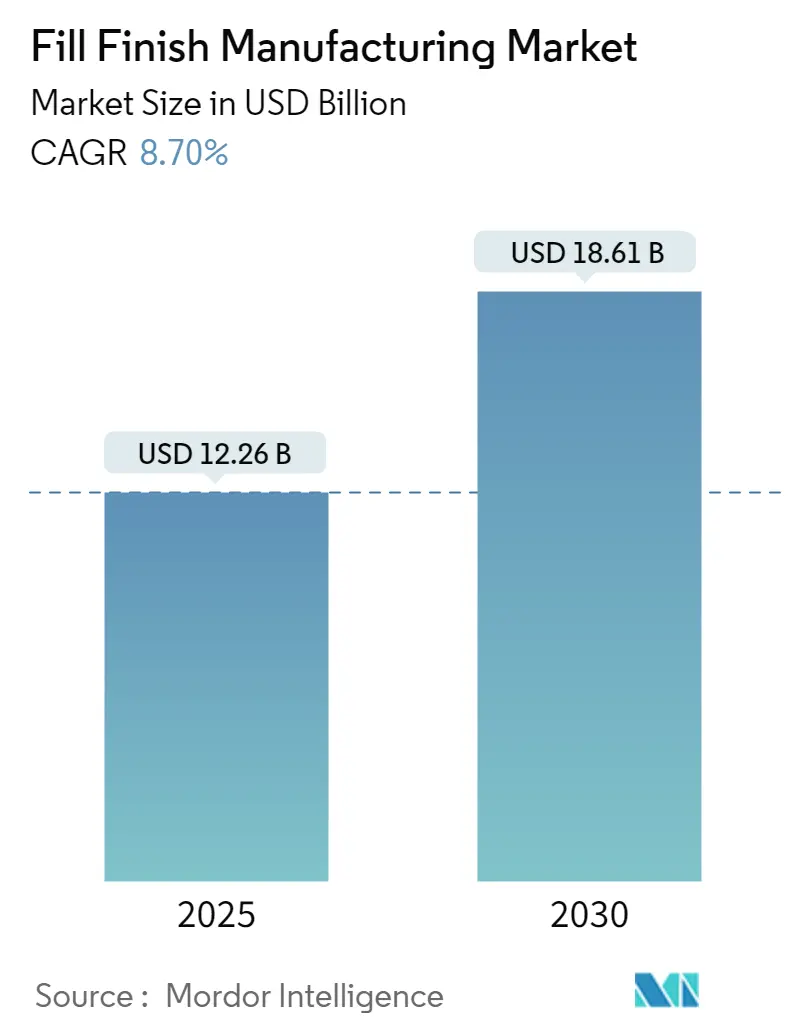

| Market Size (2025) | USD 12.26 Billion |

| Market Size (2030) | USD 18.61 Billion |

| CAGR (2025 - 2030) | 8.70 % |

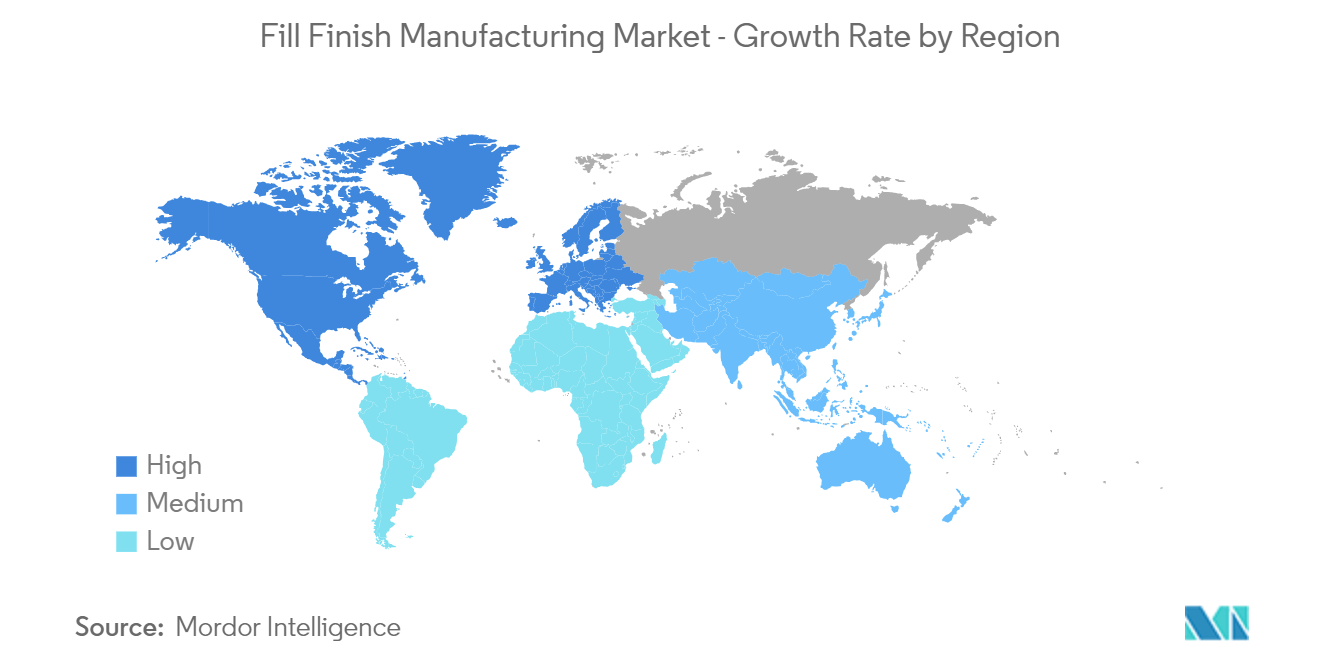

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

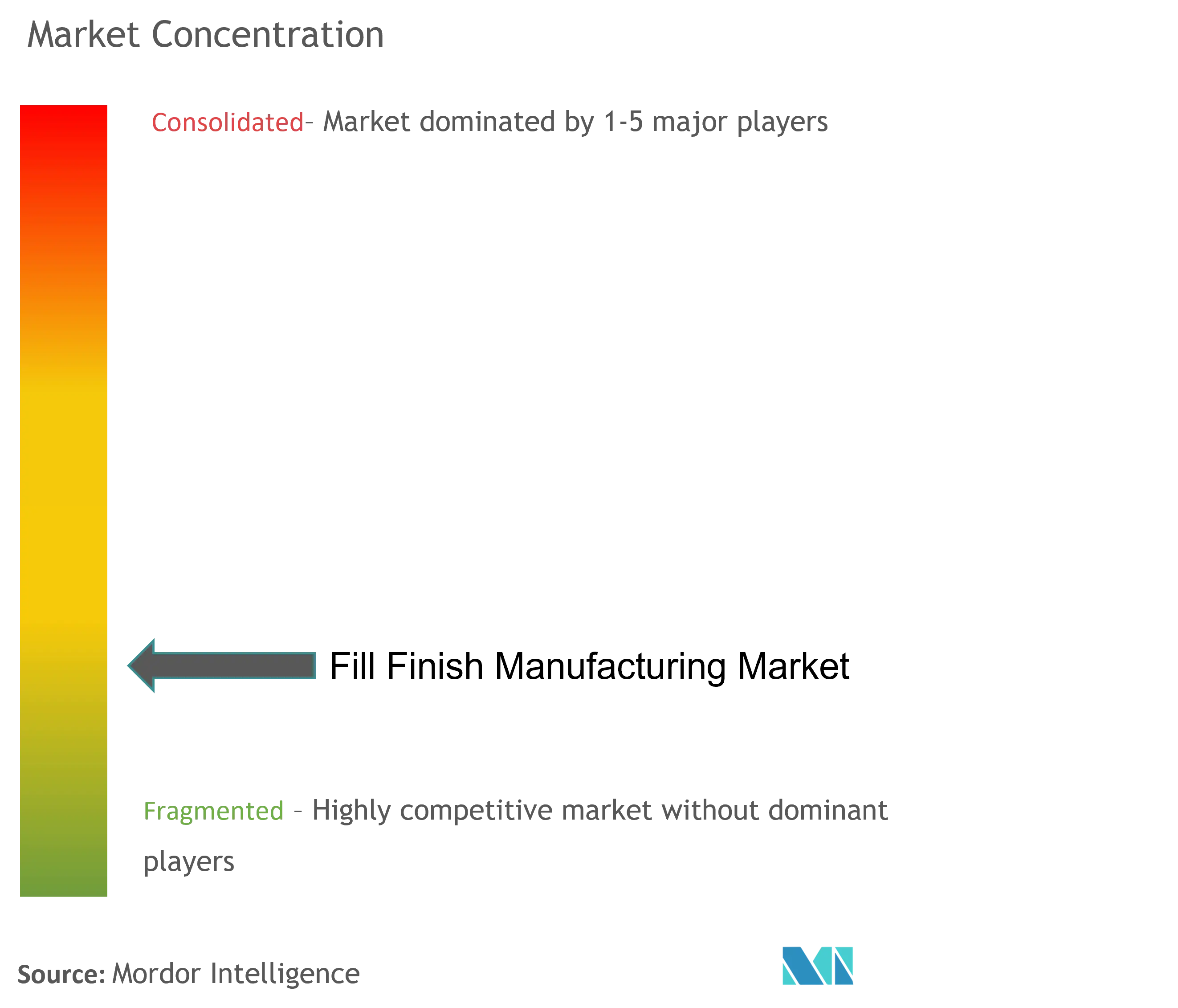

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Fill Finish Manufacturing Market Analysis

The Fill Finish Manufacturing Market size is estimated at USD 12.26 billion in 2025, and is expected to reach USD 18.61 billion by 2030, at a CAGR of 8.7% during the forecast period (2025-2030).

Fill finish manufacturing is crucial for the safe and sterile production of parenteral products free of microorganisms. The market is anticipating a digital, sustainable future with many more automated isolators and closed procedures such as personalized treatment, vital medications, and small batches becoming the new normal. The significant factors that drive the market include technological advancement in fill finish products, expansion of fill finish manufacturing facilities, and a rise in fill finish outsourcing.

The expansion of fill finish manufacturing facilities is significantly driving growth in the market. For instance, in March 2024, a contract manufacturer, SMC Ltd, expanded its capabilities by acquiring a comprehensive fill/finish facility in Charlotte, North Carolina. This strategic acquisition empowers SMC Ltd to provide its pharmaceutical clients with an expanded suite of services. Similarly, in February 2024, Simtra BioPharma Solutions committed over USD 250 million to enhance its sterile-fill finish manufacturing facility in Bloomington, Indiana. Hence, expanding these fill finish manufacturing facilities enhances the production capabilities, thereby boosting the market growth during the forecast period.

Also, innovations in fill finish technology, such as automated systems and advanced aseptic techniques, enhance production capabilities, improve efficiency, and reduce contamination risks. For instance, in January 2024, Stevanato Group SpA unveiled two new offerings to improve small-batch pharmaceutical manufacturing: the EZ-fill Kit and a non-GMP laboratory fill and finish service, both introduced at its Technology Excellence Centers (TEC). This allows customers to assess and identify the possible effects of the fill and finish process on their product performance in the container selection stage. Hence, these advancements likely boost the market growth during the forecast period.

However, stringent regulatory issues and high production costs are expected to hinder the market's growth during the forecast period.

Fill Finish Manufacturing Market Trends

The Vials Segment is Expected to Hold a Major Share in the Market During the Forecast Period

Vials are typically used to store medicines or laboratory samples. They have various capacities for filling the medicine and can be used as single-dose and multidose vials. The increasing investments of government and market players in fill finish manufacturing using vails are expected to impact the market significantly.

For instance, in February 2024, National Resilience Inc. (Resilience), a biomanufacturing firm with a strong technological focus, broadened its clinical and commercial drug product manufacturing capabilities throughout its network. Currently, the site boasts three high-speed fill lines for vials and others, with a fourth line set to be operational by 2025. Similarly, in January 2022, Recipharm collaborated with the Kingdom of Morocco to construct the largest fill and finish lines dedicated to producing vials in Africa. Hence, market players' new investments expand the facilities for the segment and likely propel the market to grow.

Also, the new company activities in the segment are expected to impact the market significantly. For instance, in November 2022, Berkshire Sterile Manufacturing (BSM) revealed its new, fully automated, 100% isolator-based filling line in a webinar. It can process up to 60,000 units of vials (RTU or bulk), and it has a lyophilization capacity of up to 35,000 10R vials per run. Thus, the new company activity in this segment increases the capacity of the fill finish facilities, which is expected to propel the market during the forecast period.

North America is Expected to Hold a Significant Share in the Market During the Forecast Period

North America is expected to hold a significant market share in the fill finish manufacturing market due to the large production capacities of several pharmaceutical and biopharmaceutical companies in this region. Also, the growing emphasis on superior biopharmaceutical products, the emergence of the biosimilar market, and the patent expiry of biologic products are fueling the growth of the overall regional market.

For instance, in March 2022, Curia, previously known as AMRI, forged a cooperative agreement with the Biomedical Advanced Research and Development Authority (BARDA) and the United States Army Contracting Command. The aim is to bolster the domestic production of injectable medicines. As part of this agreement, funding was allocated to introduce an isolated high-speed fill finish vial line equipped with biosafety level 2 (BSL-2) containment at Curia’s established facility in Albuquerque, New Mexico. This helps in domestic fill finish production of drugs, thereby boosting the market growth in the region.

Similarly, in April 2023, PCI Pharma Services (PCI) stated that three new state-of-the-art automated sterile-fill finish machines at its San Diego facility are fully operational. The innovative machinery from Cytiva can be used to fill various sterile medications into vials and syringes for small-to-mid-scale client needs. These new establishments and agreements among the major players help expand the fill finish facilities and are expected to impact the market significantly during the forecast period.

Fill Finish Manufacturing Industry Overview

The fill finish manufacturing market is fragmented and consists of several players. Companies are investing in advanced technologies such as automated fill finish systems, isolator technology, and single-use systems to improve efficiency, reduce contamination, and meet regulatory standards. Some of the major key players in the market are Becton, Dickinson and Company, Optima, West Pharmaceutical Services Inc., IMA SPA, and Groninger & Co. GmbH.

Fill Finish Manufacturing Market Leaders

-

Becton, Dickinson and Company

-

Optima

-

West Pharmaceutical Services, Inc

-

IMA S.P.A

-

Groninger & Co GmbH

*Disclaimer: Major Players sorted in no particular order

Fill Finish Manufacturing Market News

- February 2024: Novo Nordisk agreed to purchase three fill finish sites from Novo Holdings A/S (Novo Holdings). This transaction coincides with Novo Holdings' agreement to acquire Catalent Inc. (Catalent), a contract development and manufacturing organization based in Somerset, New Jersey (US).

- February 2024: Alcami Corporation, a contract development and manufacturing organization (CDMO), strategically expanded its sterile fill finish manufacturing capacity by adding a new sterile fill finish line equipped with an isolator and two lyophilizers at its established manufacturing campus in Charleston, SC.

Fill Finish Manufacturing Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Technological Advancement in Fill Finish Products

4.2.2 Rise in Fill Finish Outsourcing

4.3 Market Restraints

4.3.1 Stringent Regulatory Issues

4.3.2 High Production Costs

4.4 Porter's Five Force Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Consumables

5.1.1 Prefilled Syringes

5.1.2 Cartridges

5.1.3 Vials

5.1.4 Other Consumables

5.2 By End User

5.2.1 Contract Manufacturing Organizations

5.2.2 Pharmaceutical and Biotechnology Industries

5.2.3 Other End Users

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Becton, Dickinson and Company

6.1.2 Optima

6.1.3 West Pharmaceutical Services Inc.

6.1.4 IMA SPA

6.1.5 Groninger & Co. GmbH

6.1.6 Schott AG

6.1.7 Nipro Medical Corporation

6.1.8 Gerresheimer AG

6.1.9 Piramal Pharma Solutions

6.1.10 Syntegon Technology GmbH (Robert Bosch GmbH)

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Fill Finish Manufacturing Indsutry Segmentation

According to the scope of the report, fill finish manufacturing is the process of introducing a drug product into a container or delivery system and then packaging it under aseptic conditions. This is essential to ensure the safety and efficacy of the product. The fill finish manufacturing market is segmented into consumables, end users, and geography. By consumables, the market is segmented into prefilled syringes, cartridges, vials, and other consumables. By end user, the market is segmented into contract manufacturing organizations, pharmaceutical and biotechnology industries, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| By Consumables | |

| Prefilled Syringes | |

| Cartridges | |

| Vials | |

| Other Consumables |

| By End User | |

| Contract Manufacturing Organizations | |

| Pharmaceutical and Biotechnology Industries | |

| Other End Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Fill Finish Manufacturing Market Research Faqs

How big is the Fill Finish Manufacturing Market?

The Fill Finish Manufacturing Market size is expected to reach USD 12.26 billion in 2025 and grow at a CAGR of 8.70% to reach USD 18.61 billion by 2030.

What is the current Fill Finish Manufacturing Market size?

In 2025, the Fill Finish Manufacturing Market size is expected to reach USD 12.26 billion.

Who are the key players in Fill Finish Manufacturing Market?

Becton, Dickinson and Company, Optima, West Pharmaceutical Services, Inc, IMA S.P.A and Groninger & Co GmbH are the major companies operating in the Fill Finish Manufacturing Market.

Which is the fastest growing region in Fill Finish Manufacturing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fill Finish Manufacturing Market?

In 2025, the North America accounts for the largest market share in Fill Finish Manufacturing Market.

What years does this Fill Finish Manufacturing Market cover, and what was the market size in 2024?

In 2024, the Fill Finish Manufacturing Market size was estimated at USD 11.19 billion. The report covers the Fill Finish Manufacturing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fill Finish Manufacturing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Fill Finish Manufacturing Industry Report

The global fill finish manufacturing market is poised for significant growth, primarily driven by the rising demand for biologics and vaccines. Key factors fueling this growth include technological advancements such as automated and robotic fill-finish systems, which enhance operational efficiencies and reduce contamination risks, vital for biologics production. The shift toward biologics and biosimilars is escalating the need for advanced fill finish services, with consumables like pre-filled syringes and vials dominating due to their crucial role in maintaining sterility and dosage accuracy. The adoption of Contract Manufacturing Organizations (CMOs) is surging, attributed to their cost efficiencies and focus on core competencies. Geographically, North America and Europe lead due to advanced healthcare infrastructures and stringent regulatory frameworks, while Asia Pacific is the fastest-growing region, spurred by increases in healthcare spending and biopharmaceutical development. The market is also marked by strategic collaborations and technological integrations that improve the scalability and efficiency of fill finish processes, ensuring the efficacy and safety of final pharmaceutical products. For detailed market insights and forecasts, a comprehensive analysis is available from Mordor Intelligence™. Get a sample of this industry analysis as a free report PDF download.

Fill Finish Manufacturing Market Report Snapshots