Fiber Optic Cable Market Size

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 13.92 Billion |

| Market Size (2030) | USD 20.89 Billion |

| CAGR (2025 - 2030) | 8.46 % |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Fiber Optic Cable Market Analysis

The Fiber Optic Cable Market size is estimated at USD 13.92 billion in 2025, and is expected to reach USD 20.89 billion by 2030, at a CAGR of 8.46% during the forecast period (2025-2030).

The fiber optic industry is experiencing a transformative phase driven by the global push toward digital infrastructure modernization and enhanced connectivity requirements. The evolution of fifth-generation networks and fiber optic infrastructure has catalyzed digital transformation across industries, with fiber optic cables offering superior security, reliability, and bandwidth compared to traditional copper cables. The industry has witnessed significant technological advancement in terms of transmission capabilities and infrastructure development. According to the Fiber Broadband Association, US fiber-to-the-home (FTTH) witnessed remarkable growth of 13% in 2023, reaching 78 million homes, demonstrating the accelerating pace of fiber deployment.

Manufacturing capacity expansion and strategic investments have become paramount in meeting the escalating demand for fiber optic infrastructure. Major fiber optic cable manufacturers are actively expanding their production capabilities through new facility establishments and technological upgrades. A notable example is the October 2023 agreement between the Suez Canal Economic Zone and Hengtong, involving an $18 million investment to establish manufacturing capabilities for up to two million kilometers of fiber optic cables in the TEDA-Egypt zone. This expansion encompasses comprehensive solutions including optical communications engineering, wire production, and submarine fiber optic cable maintenance.

Technological innovation in fiber optic cables continues to advance, particularly in areas of transmission efficiency and installation methodology. The industry is witnessing the emergence of advanced cable designs, including micro cables with reduced outer diameters and enhanced fiber density, enabling more efficient installation and greater bandwidth capacity. The development of hollow core fiber technology represents another significant advancement, offering improved performance in terms of latency reduction and signal integrity. Canadian markets have demonstrated strong adoption of these technological advancements, with FTTH passings growing by 12% in 2023 to reach 12.1 million.

Regional development initiatives and government support programs have played a crucial role in expanding fiber infrastructure globally. The implementation of major funding programs, such as the Broadband Equity, Access, and Deployment (BEAD) Program in the United States, which provides $42.45 billion for high-speed internet access expansion, demonstrates the significant public sector commitment to fiber optic infrastructure development. These initiatives have catalyzed private sector investments, with major manufacturers establishing new production facilities to serve growing regional demands. According to GSMA projections, this infrastructure expansion will support the growth of 5G connections, expected to reach two billion by 2025, representing over one-fifth of global mobile connections.

Fiber Optic Cable Market Trends

Growing Penetration of Internet and High Data Traffic

The surge in demand for high network bandwidth is primarily driven by exponential growth in Internet Protocol (IP) data traffic. Major service providers have reported bandwidth doubling on their backbones every six to nine months, necessitating continuous infrastructure upgrades to handle the increasing data volume. According to Ericsson's report, the average monthly mobile data usage per smartphone is projected to reach 55 GB in 2028 in North America, driven by improved 5G network coverage and unlimited data plans. This substantial increase in data consumption is primarily attributed to video-based applications, virtual/augmented reality, and gaming applications.

The fiber optic cable market has become crucial in supporting cloud-based applications, audio-video immersive reality services, and video-on-demand (VOD) services, all of which require high-bandwidth, low-latency connections. The technology's ability to transmit information quickly across both long and short distances makes it ideal for supporting these demanding applications. According to ITU data, the estimated number of internet users worldwide reached 5.3 billion in 2022, representing a significant increase from the previous year and highlighting the growing need for robust fiber optic infrastructure to support this massive user base.

Increasing Adoption of 5G and FTTX

The deployment of fiber-integrated infrastructure has witnessed substantial growth, particularly in the telecommunications industry, driven by the rapid expansion of 5G networks and fiber-to-the-x (FTTX) architectures. These architectures, including FTTH, FTTP, FTTC, and FTTB, are becoming increasingly crucial for supporting the high-bandwidth requirements of 5G networks. According to the GSMA, 5G networks are expected to cover one-third of the world's population by 2025, with 5G connections projected to surpass 2 billion, constituting over one-fifth of mobile connections.

The telecommunications industry is actively investing in fiber optic infrastructure to support 5G deployment. For instance, in May 2022, Three Austria, Qualcomm Technologies Inc., and ZTE executed a 5G network demonstration in Europe using a standalone (SA) coverage layer. The integration of fiber optic networks with 5G technology is enabling enhanced mobile broadband services, ultra-reliable low-latency communications, and massive machine-type communications. This convergence is particularly evident in the growing adoption of fiber-to-the-home (FTTH) solutions, with many regions reporting significant increases in FTTH subscriptions and coverage.

Rising Number of Data Center Facilities

The exponential growth in data center facilities globally has become a significant driver for fiber connectivity deployment. According to Cloudscene data from 2022, the United States leads with 2,701 data centers, followed by Germany with 487 and the UK with 456, highlighting the massive scale of data center infrastructure requiring high-capacity fiber connectivity. These facilities rely heavily on fiber optic cables for managing all connections from the rack to the carrier separation point, enabling direct fiber connections to cloud service providers and eliminating the need for data to travel via public links.

The increasing adoption of cloud services and digital transformation initiatives has led to substantial investments in data center infrastructure. For instance, in November 2022, global asset manager Blackstone Group entered the data center business in Asia with a planned capacity of 600 MW across two large hyper-scale data centers in India. As data center speeds continue to increase, cable performance becomes critical for ensuring link quality. Fiber cabling has emerged as the only network infrastructure solution capable of supporting data rates of 50G and beyond, making it essential for equipment responsible for transporting and carrying signals in modern data centers.

Segment Analysis: By End-User Industry

Telecommunication Segment in Fiber Optic Cable Market

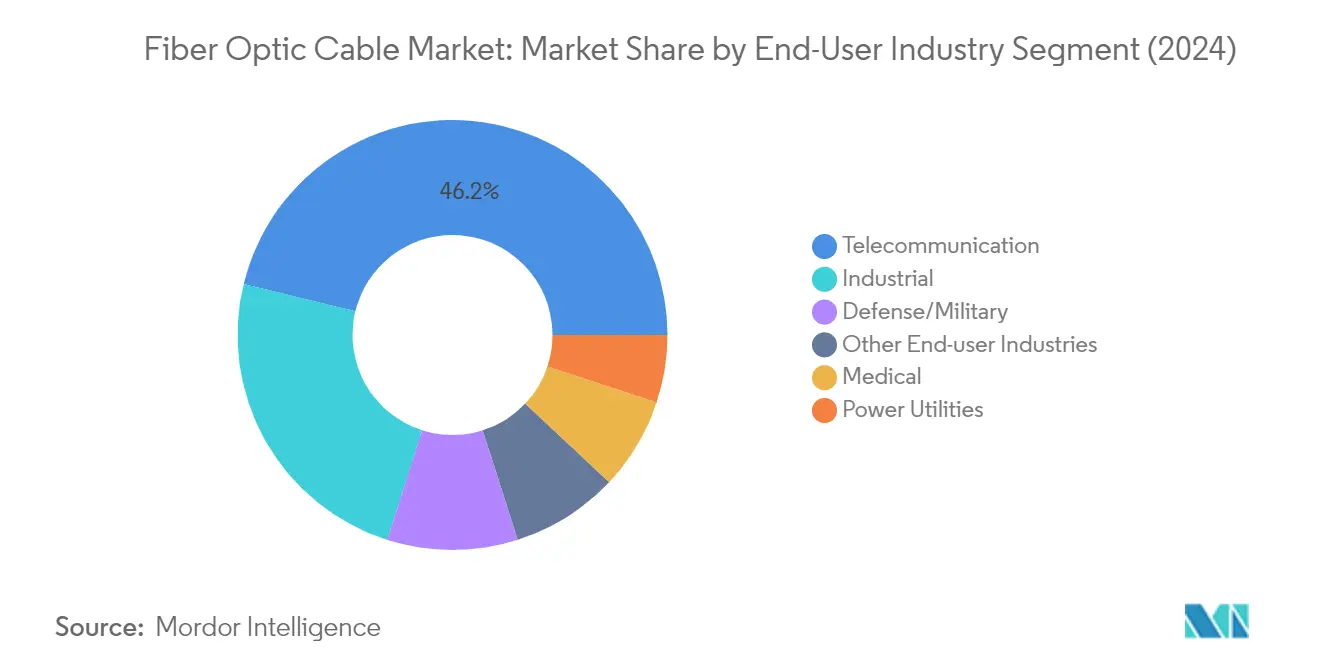

The telecommunications segment dominates the global fiber optic cable market, commanding approximately 46% market share in 2024, while also maintaining the highest growth trajectory with a projected growth rate of nearly 10% from 2024-2029. This segment's dominance is primarily driven by the explosive growth in data traffic, increasing demand for high-speed internet connectivity, and the ongoing global deployment of 5G networks. The segment's robust performance is further strengthened by major telecom operators' initiatives to expand their fiber infrastructure, particularly for supporting bandwidth-intensive applications like cloud computing, video streaming, and virtual reality. The increasing adoption of fiber-to-the-home (FTTH) services, coupled with the growing trend of digital transformation across industries, continues to fuel the demand for fiber optic cables in telecommunications applications.

Remaining Segments in End-User Industry

The industrial sector represents the second-largest segment in the fiber optic industry, driven by applications in manufacturing automation, process control, and industrial data communication. The defense/military segment utilizes fiber optic cables for secure communications, radar systems, and military aircraft applications, while the medical sector employs them for medical imaging, diagnostic equipment, and surgical procedures. The power utilities segment leverages fiber optic technology for grid monitoring and control systems. Each of these segments contributes uniquely to the market's growth, with applications ranging from high-speed data transmission in industrial settings to secure communications in military operations, and from precise medical imaging to smart grid management in power utilities. The demand for industrial fiber optic cable and fiber optic industrial cable is particularly notable in these sectors, enhancing optical transmission capabilities.

Fiber Optic Cable Market Geography Segment Analysis

Fiber Optic Cable Market in North America

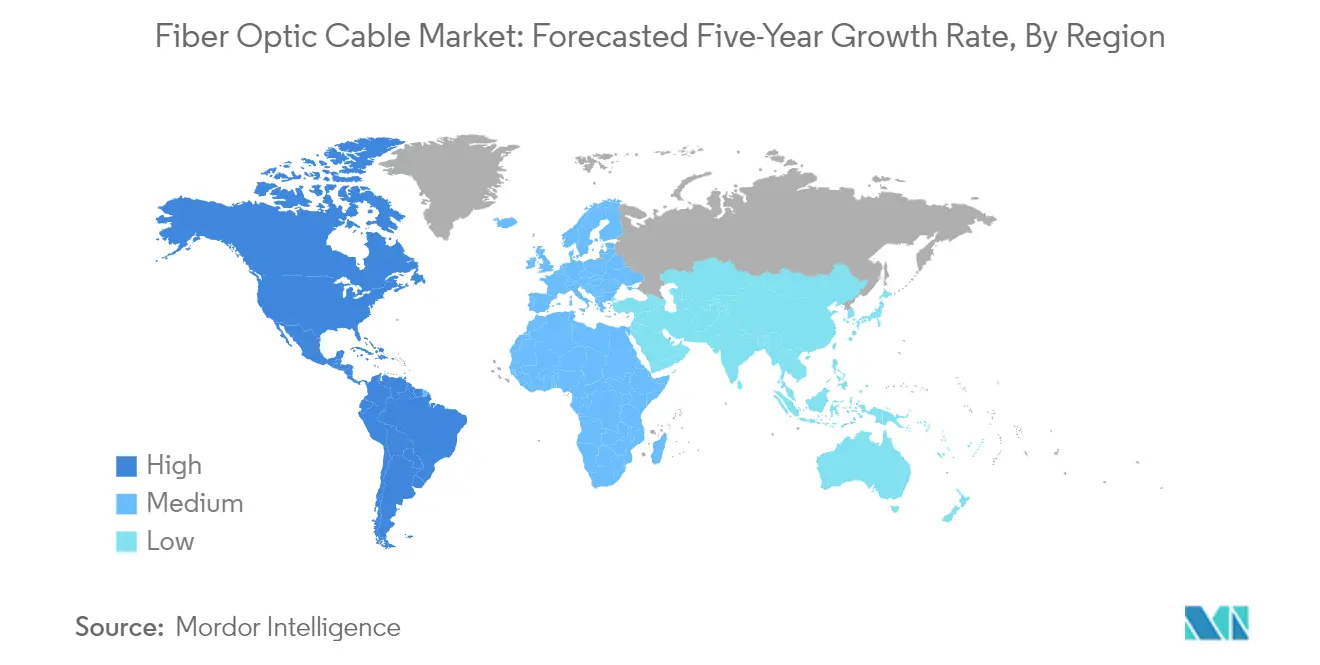

The North American fiber optic cable market commands approximately 16% of the global fiber optic market share in 2024, establishing itself as a crucial region in the global landscape. The region's dominance is primarily driven by extensive fiber-to-the-home (FTTH) deployments and aggressive 5G network rollouts across the United States and Canada. The market is characterized by significant government funding initiatives, including BEAD, RDOF, and ReConnect programs, which are actively supporting infrastructure development. The region's focus on digital transformation, coupled with the growing demand for high-speed internet connectivity in both urban and rural areas, continues to drive market growth. Major telecommunications providers are expanding their fiber networks to meet the increasing bandwidth requirements of data centers, cloud services, and emerging technologies. The emphasis on improving network resilience and reducing latency has led to substantial investments in fiber infrastructure. Additionally, the region's strong presence of leading market players and continuous technological innovations in fiber optic solutions further strengthens its market position.

Fiber Optic Cable Market in Europe

The European fiber optic cable market has demonstrated robust growth, recording approximately a 9% growth rate from 2019 to 2024, driven by aggressive fiber-to-the-premises (FTTP) deployments across major economies. The region's market dynamics are shaped by strong governmental support for digital infrastructure development and the increasing adoption of fiber broadband services. Countries like France, Spain, and Germany are leading the fiber optic revolution with ambitious national broadband plans and significant private sector investments. The market is witnessing a transformation from traditional copper-based networks to full-fiber infrastructure, particularly in urban areas. European telecom operators are actively collaborating with technology providers to enhance network capabilities and expand coverage. The region's commitment to digital transformation and smart city initiatives continues to drive demand for fiber optic solutions. The market is also benefiting from increasing investments in data center infrastructure and the growing adoption of cloud services, creating a robust ecosystem for fiber optic deployment.

Fiber Optic Cable Market in Asia-Pacific

The Asia-Pacific fiber optic cable market is poised for exceptional growth, with a projected growth rate of approximately 9% from 2024 to 2029. The region represents the largest market globally, driven by rapid digitalization and extensive telecommunications infrastructure development. The market is characterized by massive investments in 5G infrastructure, growing internet penetration, and increasing demand for high-speed connectivity solutions. Countries across the region are implementing ambitious digital transformation initiatives and smart city projects, creating substantial opportunities for fiber optic deployment. The presence of major manufacturing hubs and the growing adoption of Industry 4.0 technologies are further fueling market growth. The region's dynamic e-commerce sector and expanding digital economy are creating additional demand for robust fiber connectivity networks. Furthermore, government initiatives supporting digital infrastructure development and increasing investments in submarine cable projects are strengthening the region's position in the global market.

Fiber Optic Cable Market Overview

Top Companies in Fiber Optic Cable Market

The fiber optic cable industry features prominent players like Corning Inc., Sumitomo Electric Industries, Prysmian Group, Furukawa Electric, CommScope, Coherent Corporation, and Finolex Cables Limited, among others. These fiber optic manufacturing companies are heavily investing in research and development to drive product innovation, particularly focusing on enhanced bandwidth capabilities, reduced signal loss, and improved durability. Operational agility is demonstrated through strategic manufacturing facility locations and robust supply chain networks spanning multiple continents. Companies are increasingly pursuing vertical integration strategies to maintain better control over raw material supplies and quality standards. Market leaders are expanding their geographical presence through strategic partnerships, joint ventures, and acquisitions, particularly in emerging markets. The industry is witnessing significant investments in developing specialized products for specific applications like telecommunications, data centers, and industrial automation, while also focusing on sustainability initiatives and eco-friendly manufacturing processes.

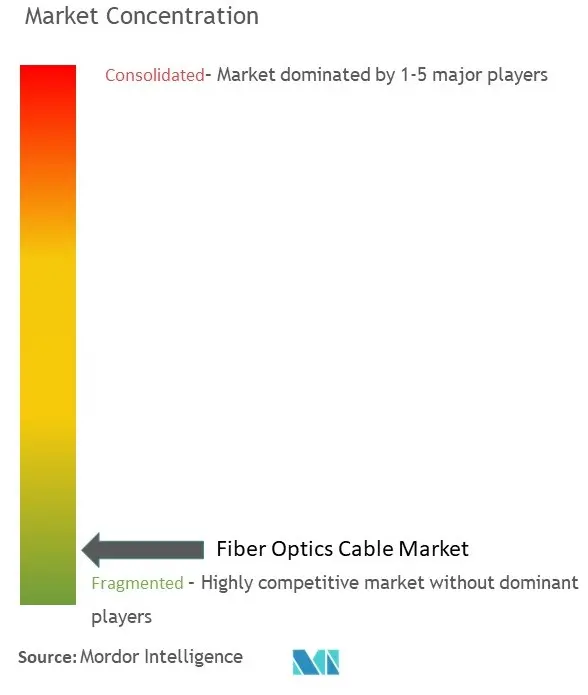

Consolidated Market with Strong Regional Players

The optical fibre market exhibits a mix of global conglomerates and specialized regional manufacturers, with the global players holding significant fiber optic market share through their extensive distribution networks and technological capabilities. Market consolidation is primarily driven by larger companies acquiring smaller, specialized manufacturers to expand their product portfolio and regional presence. The industry structure is characterized by high entry barriers due to substantial capital requirements, technical expertise needs, and established customer relationships, which favor incumbent players. Major companies are increasingly focusing on strategic collaborations with telecommunications providers and internet service providers to secure long-term contracts and maintain market position.

The competitive landscape is further shaped by regional players who maintain strong positions in their respective markets through local manufacturing capabilities and established customer relationships. Merger and acquisition activities are particularly concentrated in emerging markets, where global players seek to establish a manufacturing presence and tap into growing demand. The market also sees strategic partnerships between cable manufacturers and technology companies to develop innovative solutions for emerging applications like 5G networks and smart city infrastructure. Companies are increasingly investing in modernizing their production facilities and expanding capacity to meet growing demand while maintaining competitive pricing.

Innovation and Adaptability Drive Market Success

Success in the fiber optic cable market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements while maintaining cost competitiveness. Market leaders are focusing on developing specialized products for specific applications while maintaining flexibility in their manufacturing processes to accommodate changing customer demands. Companies are investing in research and development to improve product performance, reduce installation complexity, and enhance durability, which are becoming key differentiators in the market. The ability to provide comprehensive solutions, including installation support and after-sales service, is becoming increasingly important for maintaining market share.

For new entrants and smaller players, success lies in identifying and serving niche market segments while building strong relationships with key customers in specific industries or regions. Companies need to carefully navigate regulatory requirements across different markets while maintaining product quality and reliability standards. The market's future success factors include the ability to manage raw material costs effectively, maintain operational efficiency, and develop sustainable manufacturing practices. Players must also focus on building strong distribution networks and maintaining close relationships with end-users to understand and respond to evolving requirements while differentiating themselves through technical expertise and service quality.

Fiber Optic Cable Market Leaders

-

Corning Inc.

-

Sumitomo Electric Industries Ltd

-

Prysmian Group

-

Furukawa Electric

-

CommScope Holding Company Inc.

*Disclaimer: Major Players sorted in no particular order

Fiber Optic Cable Market News

- October 2023 - Sterlite Technologies Ltd (STL) announced that the company had developed a 160-micron optical fiber, among the world’s slimmest fiber for telecommunication. This innovation was conceptualized and developed indigenously at STL’s Centre of Excellence in Maharashtra. With this launch, the company has become the first to develop and patent this technology globally.

- September 2023 - Coherent Corp. announced that the company had launched the first pump laser module with 1200 mW of output power in a 10-pin butterfly package. Rapid advances in optical communications technologies are reaching the theoretical limits of fiber-optic capacity and driving the expansion of transmission windows into the extended C- and L-bands.

Fiber Optic Cable Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Consumers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of the Impact of and Recovery from COVID-19

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Penetration of Internet and High Data Traffic

5.1.2 Increasing Adoption of 5G and FTTX

5.1.3 Rising Number of Data Center Facilities

5.2 Market Challenges

5.2.1 High Cost of Installation and Associated Complexities

5.3 Analysis of Pricing and Pricing Trends

5.4 Technology Roadmap

6. MARKET SEGMENTATION

6.1 By End-user Industry

6.1.1 Telecommunication

6.1.2 Power Utilities

6.1.3 Defense/Military

6.1.4 Industrial

6.1.5 Medical

6.1.6 Other End-user Industries

6.2 By Geography

6.2.1 North America

6.2.2 Europe

6.2.3 Asia-Pacific

6.2.3.1 China

6.2.3.2 Japan

6.2.3.3 India

6.2.3.4 Malaysia

6.2.3.5 Indonesia

6.2.3.6 Thailand

6.2.3.7 Vietnam

6.2.3.8 Singapore

6.2.3.9 Philippines

6.2.3.10 Rest of Asia-Pacific

6.2.4 Latin America

6.2.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Corning Inc.

7.1.2 Sumitomo Electric Industries Ltd

7.1.3 Prysmian Group

7.1.4 Furukawa Electric

7.1.5 CommScope Holding Company Inc.

7.1.6 Coherent Corporation

7.1.7 Finolex Cables Limited

7.1.8 Proterial Cable America Inc. (Proterial Ltd)

7.1.9 Sterlite Technologies

7.1.10 Yangtze Optical Fiber and Cable Joint Stock Ltd Co.

8. INVESTMENT ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

Fiber Optic Cable Market Industry Segmentation

Fiber optic technology utilizes highly flexible, transparent fiber of extruded glass or plastic to transmit data. Fiber optic cables incorporate glass threads as thin as human hair, transmitting messages modulated into light waves. Although these cables are made of glass, they are highly durable and malleable.

The fiber optic cable market is segmented by end-user industry (telecommunication, power utilities, defense/military, industrial, medical, and other end-user industries) and by geography (North America, Europe, Asia-Pacific [China, Japan, India, Malaysia, Indonesia, Thailand, Vietnam, Singapore, Philippines, and the rest of Asia-Pacific], Latin America, Middle East and Africa). The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study also tracks the revenue accrued from the various types used in various end-use industries globally. In addition, the study provides the global fiber optic cable market trends and key vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem. The market sizes and forecasts are provided in terms of USD value for all the above segments.

| By End-user Industry | |

| Telecommunication | |

| Power Utilities | |

| Defense/Military | |

| Industrial | |

| Medical | |

| Other End-user Industries |

| By Geography | ||||||||||||

| North America | ||||||||||||

| Europe | ||||||||||||

| ||||||||||||

| Latin America | ||||||||||||

| Middle East and Africa |

Fiber Optic Cable Market Research FAQs

How big is the Fiber Optic Cable Market?

The Fiber Optic Cable Market size is expected to reach USD 13.92 billion in 2025 and grow at a CAGR of 8.46% to reach USD 20.89 billion by 2030.

What is the current Fiber Optic Cable Market size?

In 2025, the Fiber Optic Cable Market size is expected to reach USD 13.92 billion.

Who are the key players in Fiber Optic Cable Market?

Corning Inc., Sumitomo Electric Industries Ltd, Prysmian Group, Furukawa Electric and CommScope Holding Company Inc. are the major companies operating in the Fiber Optic Cable Market.

Which is the fastest growing region in Fiber Optic Cable Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fiber Optic Cable Market?

In 2025, the Asia Pacific accounts for the largest market share in Fiber Optic Cable Market.

What years does this Fiber Optic Cable Market cover, and what was the market size in 2024?

In 2024, the Fiber Optic Cable Market size was estimated at USD 12.74 billion. The report covers the Fiber Optic Cable Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fiber Optic Cable Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Fiber Optic Cable Market Research

Mordor Intelligence provides comprehensive fiber optic cable market analysis and industry research, delivering detailed insights into market trends, growth drivers, and competitive dynamics. Our industry reports cover the entire spectrum of the fiber optic cable industry, from structured cabling to submarine fiber cable applications, offering stakeholders a deep understanding of market segmentation, industry statistics, and future outlook. The report includes detailed market forecasts, analysis of fiber optic cable companies, and emerging technological trends in fiber communication and fiber connectivity, all available in an easy-to-read report PDF format.

Beyond market research, our consulting expertise extends to specialized services crucial for stakeholders in the fiber optic cable market. We provide technology scouting to identify innovations in optical transmission and fiber infrastructure, conduct detailed competition assessment of fiber optic cable manufacturers, and support new product launch strategies. Our team delivers value chain analysis focusing on fiber telecommunication applications, regulatory assessment for various markets, and project feasibility analysis for new fiber network deployments. We also assist in partner and supplier assessment, particularly valuable for companies exploring opportunities in underground fiber cable and aerial fiber cable segments, helping businesses make informed strategic decisions.