| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 3.35 Billion |

| Market Size (2030) | USD 4.10 Billion |

| CAGR (2025 - 2030) | 4.10 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Fertilizer Additives Market Analysis

The Fertilizer Additives Market size is estimated at USD 3.35 billion in 2025, and is expected to reach USD 4.10 billion by 2030, at a CAGR of 4.1% during the forecast period (2025-2030).

The fertilizer additive industry is experiencing significant transformation driven by evolving agricultural practices and environmental considerations. The rising costs of agricultural inputs have become a critical concern, with World Bank data indicating that fertilizer prices surged by approximately 30% since the beginning of 2022, compelling manufacturers to focus on developing more efficient and cost-effective fertilizer additive solutions. This price volatility has led to an increased emphasis on developing innovative formulations that can enhance fertilizer efficiency while minimizing environmental impact. The industry is witnessing a shift towards sustainable agriculture practices, with manufacturers increasingly investing in research and development of eco-friendly additives that can reduce nutrient runoff and improve soil health.

The market is characterized by growing technological advancements and innovation in product development. A notable example is ICL's launch of egX in 2022, a rapidly degradable biodegradable coating release technology for fertilizers in the European region, designed to maximize crop performance while reducing environmental impact by increasing nutrient use efficiency by up to 80%. This trend towards sustainable solutions is further exemplified by Soilgenic Technologies' introduction of Visio-N Supra in 2023, an enhanced urease inhibitor containing 40% N-(n-Butyl) thiophosphoric triamide (NBPT), which aims to reduce costs for farmers while increasing fertilizer efficiency.

The industry faces significant challenges related to nutrient efficiency and environmental impact. According to research by Hanfeng Evergreen Inc, China's agricultural sector, which consumes 30% of the world's fertilizer on just 7% of its land area, exemplifies the global challenge of inefficient fertilizer usage. This inefficiency has led to an increased focus on developing advanced fertilizer additive solutions that can improve nutrient absorption and reduce waste. The market is witnessing a growing emphasis on precision agriculture and smart farming techniques, with additives being developed to complement these advanced farming practices.

The economic landscape of the fertilizer additives market is experiencing notable shifts, particularly in key markets like India, where the wholesale price index of fertilizers and nitrogen compounds increased from 129.6 to 144.8 between 2022 and 2023, according to the Office of Economic Adviser. This price volatility has spurred innovation in cost-effective solutions and led to an increased focus on developing multi-functional additives that can provide multiple benefits in a single application. The industry is also witnessing a trend towards regional production and supply chain optimization to reduce dependence on imports and maintain price stability. The integration of soil additive technologies is also becoming pivotal in enhancing fertilizer enhancement strategies, ensuring sustainable agricultural growth.

Fertilizer Additives Market Trends

Rising Fertilizer Consumption

The increasing global population, coupled with decreasing arable land, has led to intensive farming practices that rely heavily on fertilizers to maintain crop productivity. According to the International Fertilizer Association (IFASTAT), the consumption of urea, which has the highest nitrogen content among solid fertilizers, increased from 51,141.0 thousand metric tons in 2017 to 52,258.9 thousand metric tons in 2019. This rising fertilizer consumption has created significant challenges, as approximately 20-30% of the total nitrogen applied through fertilizers is lost in humid regions through volatilization, denitrification, and leaching, with losses sometimes reaching up to 60% in extreme cases.

The extensive use of nitrogen-based fertilizers, particularly urea, which accounts for over 80% of total nitrogen fertilizer consumption in countries like India, has heightened the need for fertilizer additives. These additives play a crucial role in reducing nutrient losses while enhancing the efficiency of applied fertilizers. The high relative humidity tolerance of urea makes it suitable for hot and humid conditions, leading to its preference over alternatives like ammonium nitrate and calcium ammonium nitrate (CAN). However, this widespread usage also necessitates the incorporation of urease inhibitors and other additives to minimize potential volatilization losses and optimize nutrient utilization.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Strategic Activities by Major Players

Major companies in the fertilizer additives market are actively engaged in research and development, product launches, and strategic acquisitions to expand their market presence and meet evolving customer needs. For instance, West Central demonstrated this trend by launching Trivar, an innovative broadcast fertilizer additive powered by the Levesol chelating agent, designed to maximize phosphate fertilizer efficiency by increasing the availability of phosphorus and other key nutrients. This type of product innovation reflects the industry's commitment to developing solutions that address specific challenges in nutrient availability and uptake.

The industry has witnessed significant technological advancements, particularly in the development of specialized additives like ammonium thiosulphate as urease inhibitors. Companies are focusing on creating multi-functional additives that can address multiple challenges simultaneously, such as reducing nutrient losses while improving handling characteristics. These strategic initiatives by major players have resulted in the introduction of more sophisticated and effective products, with studies by agricultural research institutions validating their performance in various applications, such as the production of hard red spring wheat under reduced tillage management.

Enhanced Fertilizer Performance

Fertilizer additives have demonstrated significant capabilities in improving the overall performance and efficiency of fertilizers through multiple mechanisms. In the United States, which stands as the world's fourth-largest producer of nitrogen fertilizers, approximately 21% of nitrogen and phosphate fertilizer products are treated with inhibitors, polymers, or other controlled-release mechanisms to enhance their efficiency. These additives work by stabilizing nutrients in the soil, preventing losses through leaching or volatilization, and ensuring more consistent nutrient availability to plants throughout the growing season.

The performance enhancement provided by fertilizer additives extends beyond just nutrient retention, encompassing improvements in physical handling characteristics and application efficiency. Advanced formulations of additives help create slow-release fertilizers that break down gradually over time, ensuring a steady nutrient supply while minimizing losses. Additionally, surfactants and penetration enhancers improve the spreading and absorption of liquid fertilizers, allowing for better distribution of nutrients and more uniform coverage. These performance improvements have made fertilizer stabilizers an essential component in modern agricultural practices, particularly in regions where environmental conditions pose challenges to fertilizer efficiency.

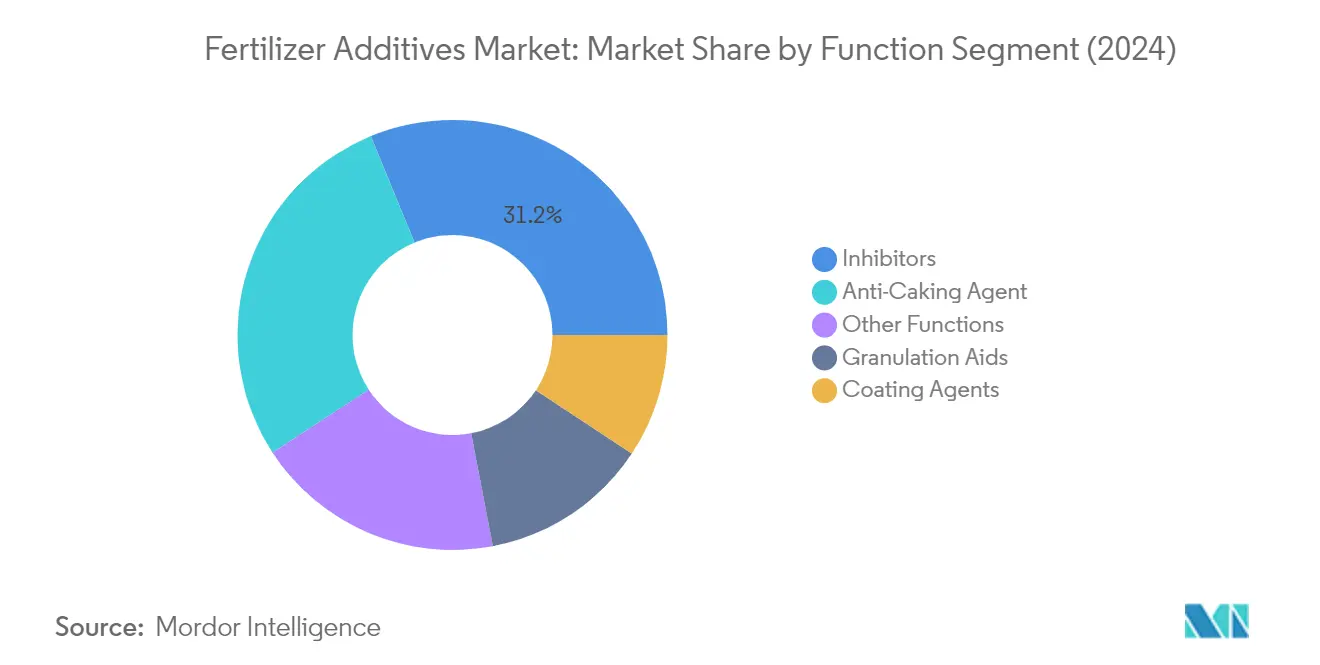

Segment Analysis: Function

Inhibitors Segment in Fertilizer Additives Market

The Inhibitors segment continues to dominate the global fertilizer additives market, commanding approximately 31% market share in 2024. This segment's prominence is primarily attributed to the widespread use of nitrogen fertilizers worldwide and the critical role nitrification inhibitors play in preventing nutrient losses through volatilization, denitrification, and leaching processes. The segment is also experiencing the fastest growth rate of around 4% for the forecast period 2024-2029, driven by increasing awareness about nitrogen use efficiency and environmental regulations regarding ammonia emissions. Inhibitors, particularly urease inhibitors and nitrification inhibitors, are becoming increasingly essential as they can reduce nitrogen losses by up to 70% while improving nutrient uptake efficiency in various agricultural applications. The segment's growth is further supported by technological advancements in inhibitor formulations and rising adoption in precision agriculture practices.

Remaining Segments in Function Segmentation

The fertilizer additives market encompasses several other significant functional segments, including Anti-Caking Agents, Granulation Aids, fertilizer coating agents, and Other Functions. Anti-caking agents represent the second-largest segment, playing a crucial role in preventing the formation of lumps in fertilizers during storage and transportation. Granulation aids are essential in improving the physical properties and handling characteristics of fertilizer granules, while fertilizer coating agents enhance the protection and controlled release properties of fertilizer products. The Other Functions segment includes various specialized additives such as dedusting agents, corrosion inhibitors, and hydrophobic agents, each serving specific purposes in fertilizer manufacturing and application processes. These segments collectively contribute to enhancing fertilizer efficiency, improving handling characteristics, and reducing environmental impact across different agricultural applications.

Segment Analysis: Form

Solid Segment in Fertilizer Additives Market

The solid segment continues to dominate the global fertilizer additives market, holding approximately 59% market share in 2024. This significant market position is attributed to several key advantages that solid fertilizer additives offer over their liquid counterparts. The dust-binding properties of solid additives make them particularly well-suited for incorporation with fertilizers during the manufacturing process. Additionally, solid fertilizer additives provide superior benefits in terms of storage efficiency, handling convenience, and cost-effectiveness. Their ability to enable better control of nutrient release makes them highly preferred among manufacturers and end-users alike. The segment is also experiencing the fastest growth trajectory, projected to grow at around 4% from 2024 to 2029, driven by increasing demand for enhanced efficiency fertilizers and the growing need for improved nutrient management in agriculture.

Liquid Segment in Fertilizer Additives Market

The liquid segment represents a vital component of the fertilizer additives market, offering unique advantages in terms of application uniformity and ease of use. Liquid fertilizer additives are particularly valued for their ability to provide uniform application and superior mixing capabilities with various fertilizer formulations. The segment's growth is supported by the expanding demand in the agriculture sector, coupled with the increasing adoption of precision farming techniques that require precise nutrient delivery systems. Liquid additives are especially preferred in regions with advanced agricultural practices and in situations where rapid nutrient availability is crucial. The segment's popularity is further enhanced by its compatibility with modern irrigation systems and the growing trend toward fertigation in commercial agriculture.

Fertilizer Additives Market Geography Segment Analysis

Fertilizer Additives Market in North America

The North American fertilizer additives market demonstrates a robust presence across the United States, Canada, and Mexico. The region's agricultural sector heavily relies on fertilizer additives to optimize nutrient uptake and improve crop yields. The United States leads the regional market due to its extensive agricultural activities and advanced farming practices. Canada follows with its focus on precision agriculture and implementation of innovative fertilizer additive technologies. Mexico's market is driven by the growing need to enhance soil fertility and increase agricultural productivity in challenging soil conditions.

Fertilizer Additives Market in the United States

The United States dominates the North American fertilizer additives market, holding approximately 75% of the regional market share in 2024. The country's leadership position is attributed to its significant agricultural sector and high adoption rate of advanced fertilizer additive technologies. American farmers increasingly recognize the importance of fertilizer additives in maximizing nutrient use efficiency and reducing environmental impact. The presence of major market players and their continuous product innovations further strengthens the market position. The country's extensive research and development activities in agricultural technologies, coupled with supportive government policies promoting sustainable farming practices, contribute to market growth.

Fertilizer Additives Market in Mexico

Mexico emerges as the fastest-growing market in North America, with a projected growth rate of approximately 3% during 2024-2029. The country's agricultural sector is undergoing significant transformation with increasing adoption of modern farming practices. Mexican farmers are becoming more aware of the benefits of fertilizer additives in improving crop yields and soil health. The government's initiatives to support agricultural modernization and sustainable farming practices are driving market growth. Rising focus on export-quality crop production and the need to optimize fertilizer efficiency in various soil conditions are key factors contributing to the market's rapid expansion.

Fertilizer Additives Market in Europe

The European fertilizer additives market showcases a diverse landscape across major countries including Russia, Spain, the United Kingdom, France, Germany, and Italy. The region's strong focus on sustainable agriculture and environmental regulations shapes the market dynamics. Each country contributes uniquely to the market, with varying agricultural needs and adoption rates of fertilizer additives. The presence of established manufacturers and ongoing research and development activities in agricultural technologies further strengthens the market. The European Union's stringent regulations on fertilizer use and environmental protection significantly influence market trends and product development.

Fertilizer Additives Market in Russia

Russia stands as the largest market for fertilizer additives in Europe, commanding approximately 14% of the regional market share in 2024. The country's vast agricultural land and significant fertilizer production capacity drive market growth. The Russian agricultural sector's increasing focus on improving crop yields through efficient nutrient management supports market expansion. The country's strong domestic fertilizer industry and growing emphasis on sustainable farming practices contribute to market leadership. The presence of major agricultural companies and ongoing modernization of farming practices further strengthen Russia's position in the European market.

Fertilizer Additives Market in Russia - Growth Analysis

Russia also leads the European market in terms of growth rate, with an expected growth rate of approximately 5% during 2024-2029. The country's agricultural sector is witnessing significant technological advancements and modernization efforts. The increasing adoption of precision farming techniques and the need for improved fertilizer efficiency drive market growth. Government support for agricultural development and increasing focus on export-quality crop production contribute to market expansion. The growing awareness about environmental protection and the need for sustainable farming practices further accelerate market growth.

Fertilizer Additives Market in Asia-Pacific

The Asia-Pacific fertilizer additives market encompasses major agricultural economies including China, Japan, India, and Australia. The region's diverse agricultural landscape and varying soil conditions create unique market opportunities. Each country's agricultural policies and modernization efforts significantly influence market dynamics. The increasing focus on food security and sustainable farming practices drives market growth across the region. The presence of both established and emerging players contributes to market development and innovation.

Fertilizer Additives Market in China

China dominates the Asia-Pacific fertilizer additives market, reflecting its position as a major agricultural producer. The country's extensive farming operations and significant fertilizer consumption drive market growth. The Chinese agricultural sector's increasing focus on efficiency and sustainability supports market expansion. The government's support for agricultural modernization and environmental protection influences market development. The presence of domestic manufacturers and ongoing research in agricultural technologies strengthens China's market position.

Fertilizer Additives Market in China - Growth Analysis

China leads the Asia-Pacific region in growth potential, demonstrating strong market expansion. The country's agricultural sector continues to adopt advanced farming technologies and practices. The increasing awareness about environmental protection and sustainable farming drives market growth. Government initiatives supporting agricultural modernization and efficiency improvement contribute to market expansion. The growing focus on food security and crop yield optimization further accelerates market development.

Fertilizer Additives Market in South America

The South American fertilizer additives market, primarily represented by Brazil and Argentina, shows significant potential for growth. Brazil emerges as both the largest and fastest-growing market in the region, driven by its extensive agricultural operations and increasing adoption of modern farming practices. Argentina contributes to regional market growth through its focus on improving agricultural productivity and sustainable farming practices. The region's agricultural sector's modernization efforts and increasing awareness about efficient nutrient management drive market development. Government initiatives supporting agricultural development and environmental protection further influence market dynamics.

Fertilizer Additives Market in Africa

The African fertilizer additives market, with South Africa as a key player, demonstrates growing potential in the global landscape. South Africa leads the regional market both in terms of size and growth rate, supported by its relatively advanced agricultural sector and increasing adoption of modern farming technologies. The region's focus on improving agricultural productivity and food security drives market growth. The increasing awareness about sustainable farming practices and the need for efficient nutrient management influence market development. Government initiatives supporting agricultural modernization and environmental protection contribute to market expansion across the continent.

Get Analysis on Important Geographic Markets

Download PDF

Fertilizer Additives Industry Overview

Top Companies in Fertilizer Additives Market

The fertilizer additive market is characterized by continuous innovation and strategic developments from major players like Corteva Agriscience, BASF SE, and Arkema. Companies are focusing on developing advanced formulations with enhanced nutrient efficiency and environmental sustainability features, particularly in nitrogen stabilizers and anti-caking agents. The industry has witnessed significant investment in research and development, leading to the introduction of next-generation products with improved granular technologies and specialized coating solutions. Market leaders are expanding their geographical presence through strategic acquisitions and partnerships, particularly in emerging agricultural markets. Manufacturing capacity expansion and the integration of digital technologies in product development and distribution channels have become key trends, as companies strive to meet the growing demand for specialized fertilizer additives across different agricultural segments.

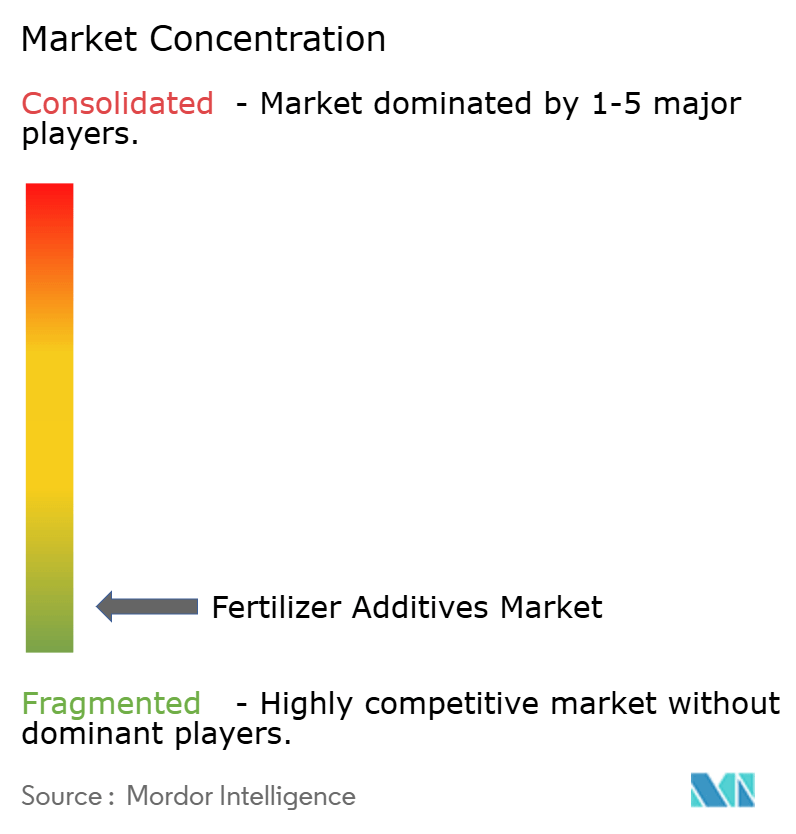

Fragmented Market with Consolidation Opportunities Ahead

The fertilizer additives market exhibits a fragmented structure with a mix of global chemical conglomerates and specialized agricultural input manufacturers. Major multinational companies leverage their extensive research capabilities and global distribution networks to maintain market leadership, while regional players focus on serving specific geographical markets with customized solutions. The industry is witnessing increasing consolidation through mergers and acquisitions, as larger companies seek to expand their product portfolios and strengthen their market presence in key agricultural regions.

The competitive dynamics are shaped by the strong presence of established chemical manufacturers who bring decades of expertise in product development and manufacturing processes. These companies maintain significant investments in manufacturing facilities and distribution infrastructure across multiple regions. The market has seen several strategic acquisitions aimed at expanding technological capabilities and geographic reach, particularly in high-growth markets. Regional players continue to maintain their relevance through specialized product offerings and strong local relationships with fertilizer manufacturers and agricultural communities.

Innovation and Sustainability Drive Future Growth

Success in the fertilizer additives market increasingly depends on companies' ability to develop environmentally sustainable products while maintaining performance efficiency. Market leaders are investing in eco-friendly formulations and biodegradable alternatives to meet evolving regulatory requirements and changing farmer preferences. Companies are also focusing on developing integrated solutions that combine traditional additives with digital farming technologies, creating value-added offerings that provide comprehensive nutrient management solutions. Building strong distribution networks and maintaining close relationships with key stakeholders in the agricultural value chain has become crucial for market success.

For new entrants and smaller players, specialization in specific product categories or regional markets offers opportunities for growth. Companies need to focus on developing innovative solutions that address specific agricultural challenges while complying with increasingly stringent environmental regulations. The ability to provide technical support and demonstrate a clear value proposition to end-users is becoming increasingly important. Future success will depend on companies' ability to balance product innovation with cost-effectiveness, while building strong partnerships with fertilizer manufacturers and agricultural service providers. The growing emphasis on sustainable agriculture and precision farming creates opportunities for companies that can align their products with these trends, enhancing fertilizer efficiency and fertilizer enhancement.

Fertilizer Additives Market Leaders

-

Corteva Agriscience

-

BASF SE

-

Arkema (ARRMAZ)

-

Clariant International Ltd

-

KAO Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Fertilizer Additives Market News

- September 2024: Innovar Ag, a U.S.-based developer of chemical fertilizer additives, has set up a representative office in Tokyo. This move aims to bolster the profitability and sustainability of the agricultural sector. Furthermore, the company's exclusive "PENXCEL Technology" enhances fertilizer additives by enabling rapid penetration of ingredients into fertilizer granules, ensuring the production of highly concentrated and uniform fertilizers.

- August 2024: Koch Agronomic Services LLC has acquired OCI Global’s fertilizer plant located in Wever, Iowa, for a sum of USD 3.6 billion. This strategic investment bolsters Koch's capacity to cater to its customers over the long haul, offering increased adaptability to shifting nitrogen preferences.

Fertilizer Additives Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Raising Fertilizer Consumption

- 4.2.2 Increasing Strategic Activities By The Major Players

- 4.2.3 Enhanced Fertilizer Performance

-

4.3 Market Restraints

- 4.3.1 Raising Overall Cost Of Crop Production

- 4.3.2 High Environmental Effects

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Function

- 5.1.1 Inhibitors

- 5.1.2 Coating Agents

- 5.1.3 Granulation Aids

- 5.1.4 Anti-Caking Agent

- 5.1.5 Other Functions

-

5.2 Form

- 5.2.1 Solid

- 5.2.2 Liquid

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Germany

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Corteva Agriscience

- 6.3.3 Arkema (ARRMAZ)

- 6.3.4 Dorf Ketal Company LLC

- 6.3.5 Koch Agronomic Services LLC

- 6.3.6 Clariant International Ltd

- 6.3.7 KAO Corporation

- 6.3.8 Michelman Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Fertilizer Additives Industry Segmentation

Fertilizer additives are used to improve the quality and stability of the soil and fertilizer. It is also used to prevent the loss of nutrients like phosphorus, sulfur, nitrogen, and potassium from the soil and environment. The fertilizer additives market is segmented by Function (Inhibitors, Coating Agents, Granulation Aids, Anti-Caking Agents, and Other Functions), by Form (Solid and Liquid), and by Geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers market estimation and forecast in value (USD) for the above-mentioned segments.

| Function | Inhibitors | ||

| Coating Agents | |||

| Granulation Aids | |||

| Anti-Caking Agent | |||

| Other Functions | |||

| Form | Solid | ||

| Liquid | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Spain | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Fertilizer Additives Market Research Faqs

How big is the Fertilizer Additives Market?

The Fertilizer Additives Market size is expected to reach USD 3.35 billion in 2025 and grow at a CAGR of 4.10% to reach USD 4.10 billion by 2030.

What is the current Fertilizer Additives Market size?

In 2025, the Fertilizer Additives Market size is expected to reach USD 3.35 billion.

Who are the key players in Fertilizer Additives Market?

Corteva Agriscience, BASF SE, Arkema (ARRMAZ), Clariant International Ltd and KAO Corporation are the major companies operating in the Fertilizer Additives Market.

Which is the fastest growing region in Fertilizer Additives Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fertilizer Additives Market?

In 2025, the Asia Pacific accounts for the largest market share in Fertilizer Additives Market.

What years does this Fertilizer Additives Market cover, and what was the market size in 2024?

In 2024, the Fertilizer Additives Market size was estimated at USD 3.21 billion. The report covers the Fertilizer Additives Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fertilizer Additives Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Fertilizer Additives Market Research

Mordor Intelligence provides a comprehensive analysis of the fertilizer additive market, utilizing our extensive experience in agricultural chemical research. Our expert analysts offer detailed insights into various technologies. These include nitrification inhibitor and urease inhibitor applications, as well as advanced fertilizer coating technologies. The report examines how innovations in soil additive are transforming agricultural productivity. It thoroughly analyzes the latest developments in fertilizer additive technologies across global markets.

Stakeholders benefit from our detailed examination of fertilizer efficiency improvements and fertilizer stabilizer developments. The report is available in an easy-to-download PDF format. Our analysis covers emerging trends in fertiliser additive technologies and explores various aspects of fertilizer enhancement solutions, providing actionable insights for industry participants. The report offers strategic recommendations based on current market dynamics. This enables businesses to make informed decisions about their agricultural chemical investments and market positioning strategies.