Fatty Alcohol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

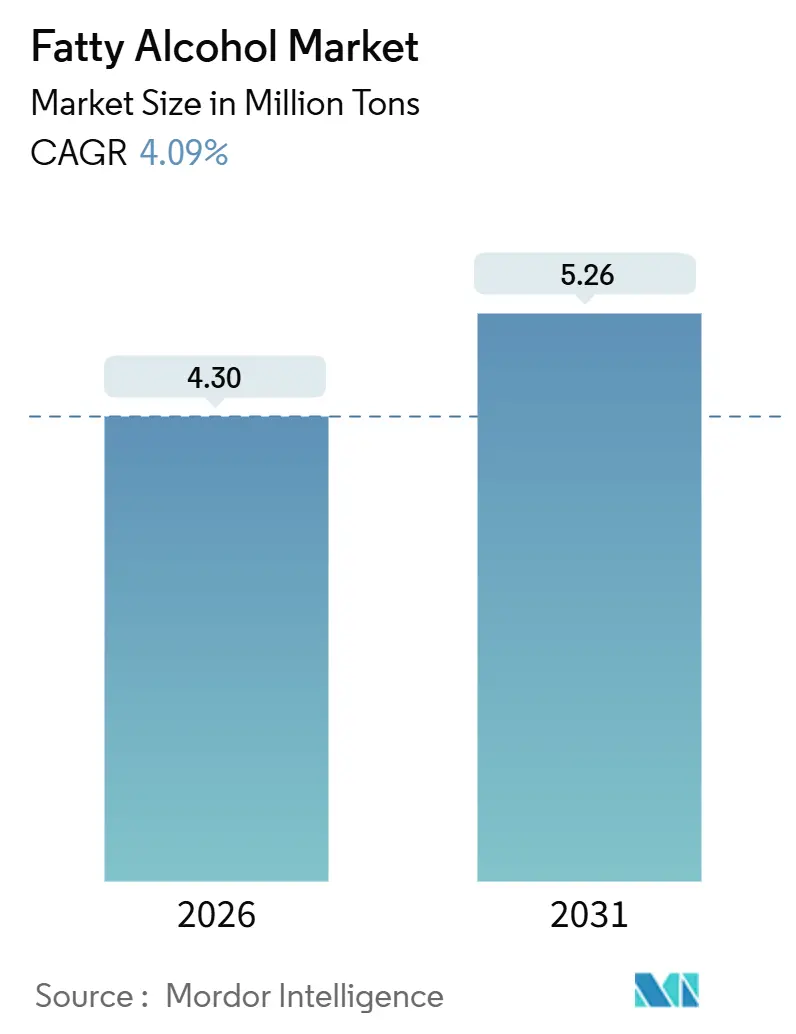

| Market Volume (2026) | 4.30 Million tons |

| Market Volume (2031) | 5.26 Million tons |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

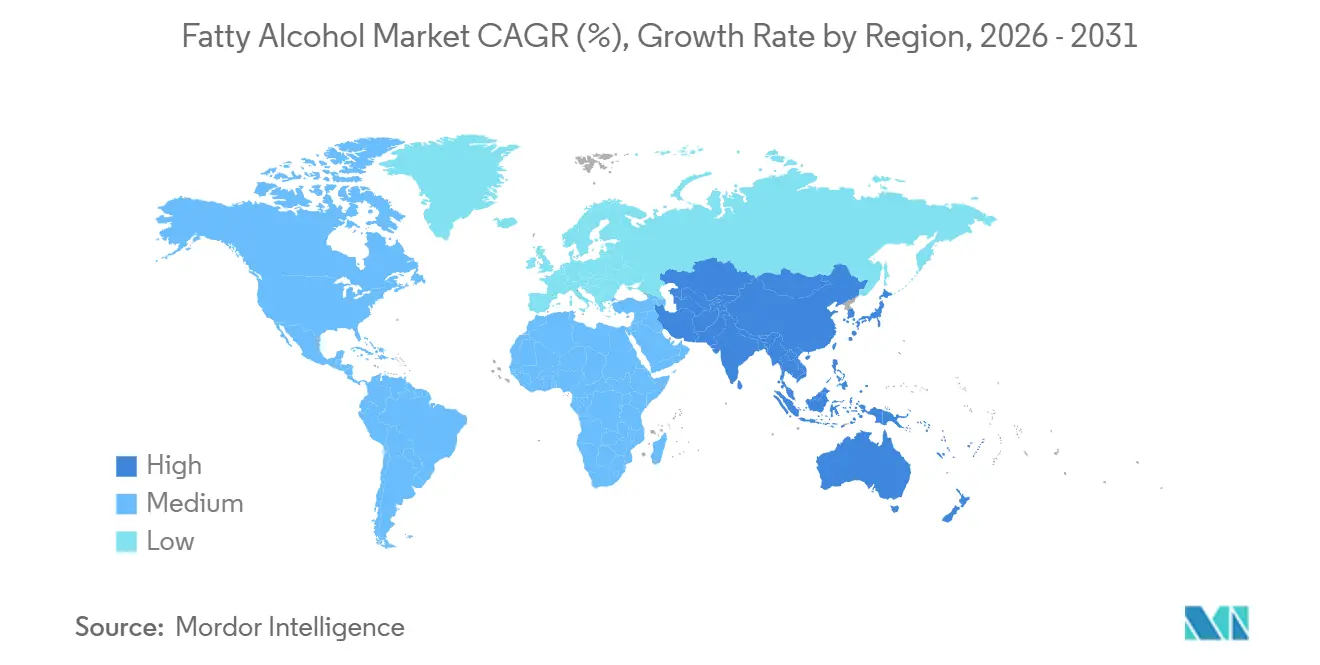

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fatty Alcohol Market Analysis by Mordor Intelligence

The Fatty Alcohol Market size is estimated at 4.30 Million tons in 2026, and is expected to reach 5.26 Million tons by 2031, at a CAGR of 4.09% during the forecast period (2026-2031). Natural sources continued to dominate 2025 volumes, yet petrochemical routes are capturing share where ethylene costs remain under USD 0.20 per gallon and lauric-oil premiums exceed 75%, tilting economics toward synthetic capacity. Reformulation momentum in fast-moving consumer goods, rising personal-care premiumization, and regulatory pushes for biodegradable lubricants are the pivotal demand catalysts. Asia-Pacific leads growth on the back of Indonesia’s vast oleochemical footprint and China’s coal-derived syngas pathways that bypass palm-oil exposure. At the same time, feedstock arbitrage, over-capacity in Southeast Asia, and unresolved technical hurdles in next-generation routes inject volatility into industry margins. Competitive strategies diverge sharply: Southeast Asian natural-alcohol producers are integrating downstream into specialty grades, whereas European and North American suppliers leverage EUDR exemptions for petrochemical alcohols to gain share in deforestation-sensitive segments.

Key Report Takeaways

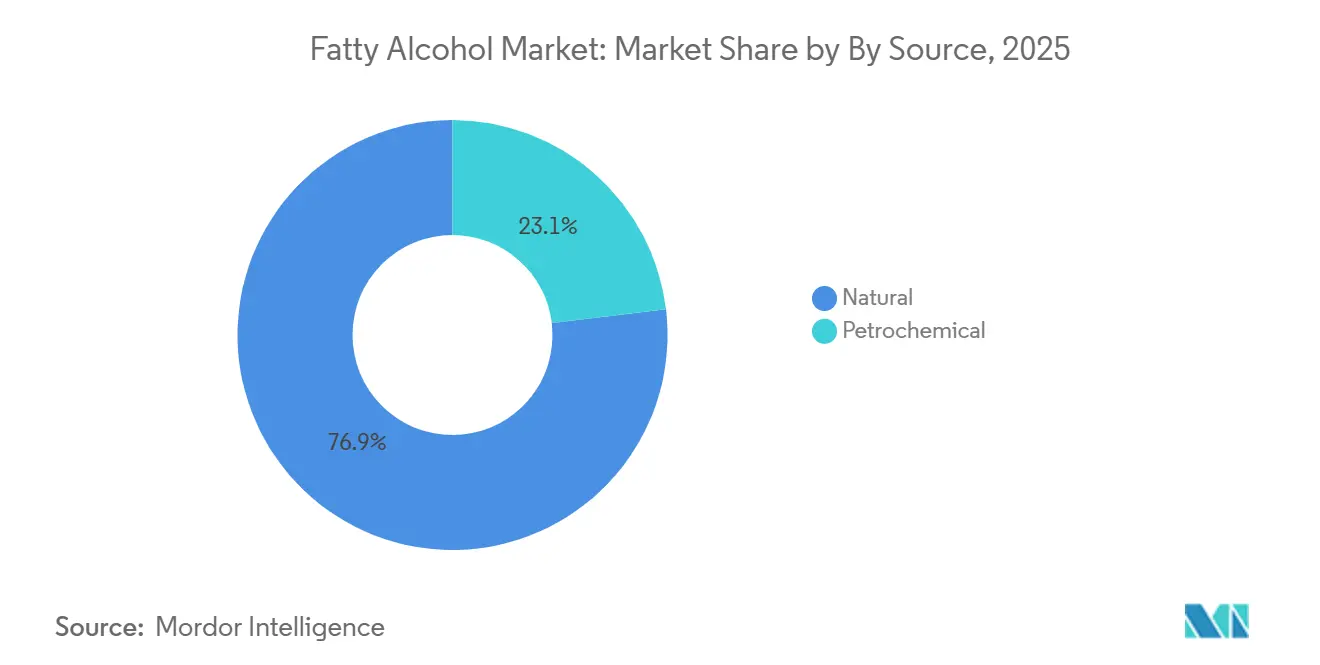

- By source, natural alcohols retained 76.91% of 2025 volume, while petrochemical routes are advancing at a 4.39% CAGR through 2031.

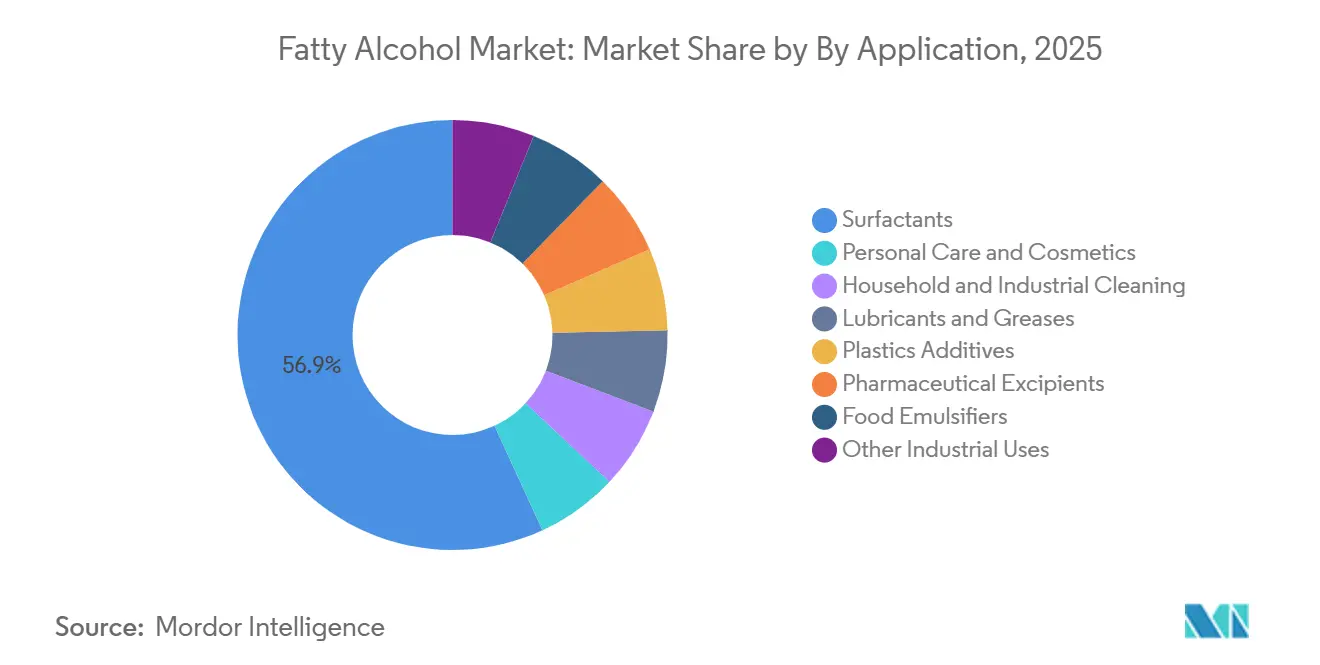

- By application, surfactants held 56.88% of 2025 volume; personal care is forecast to expand at a 4.72% CAGR through 2031.

- By geography, Asia-Pacific captured 44.28% share of the fatty alcohol market size in 2025 and is projected to post a 5.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fatty Alcohol Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surfactant demand boom in FMCG sector | +1.8% | Global with APAC core, spill-over to MEA | Medium term (2–4 years) |

| Shift toward sulfate-free personal-care lines | +1.2% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Regulatory push for biodegradable lubricants | +0.7% | North America & EU marine sectors | Long term (≥ 4 years) |

| Rising pharmaceutical-grade demand | +0.4% | North America & EU, early adoption in India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surfactant Demand Boom in FMCG Sector

Nonionic surfactants built on fatty-alcohol ethoxylates represented 40% of global surfactant use in 2024, and FMCG majors are cutting anionic ratios to improve hard-water performance[1]American Cleaning Institute, “2024 Surfactant Trends,” cleaninginstitute.org. Procter & Gamble’s patent filings reveal sulfate-free shampoos that raise fatty-alcohol loading by up to 20% per bottle. Asia-Pacific is the epicenter; urban detergent consumption already stands above 8 kg per capita, driven by rising disposable income. Biosurfactant scale-up delays keep fatty-alcohol ethoxylates below USD 1,500 per ton, reinforcing their cost advantage. Southeast Asian producers are back-integrating into palm-kernel crushing to secure feedstock, but the strategy escalates exposure to EU deforestation rules that came into force in 2024[2]European Commission, “EU Deforestation Regulation,” ec.europa.eu .

Shift Toward Sulfate-Free and Milder Personal-Care Formulations

Sulfate-free personal-care products grew twice as fast as conventional lines in 2024, propelled by dermatological concerns and social-media amplification. The trend lifts demand for C16–C18 alcohols, valued for emolliency, and C12–C14 alcohols that co-surfact in mild cleansing bases. Although EU Cosmetics Regulation does not mandate sulfate-free claims, proactive reformulation has become brand risk management. Clariant’s USD 810 million purchase of Lucas Meyer Cosmetics underscores premium multiples paid for specialty ingredient portfolios enabling “clean beauty” claims. Cross-category adoption extends to body washes and facial cleansers, expanding the fatty-alcohol addressable market by roughly 12–15% over the forecast horizon.

Regulatory Push for Biodegradable Lubricants

EPA’s 2024 Vessel General Permit obliges stern-tube lubricants to meet 60% biodegradability within 28 days, a specification fatty-alcohol esters pass more readily than mineral oils. Parallel EU Ecolabel rules require ≥50% biobased carbon, steering marine and hydraulic systems toward fatty-alcohol esters. Adoption is uneven; compliance monitoring in Southeast Asia and the Middle East remains limited, muting global uptake. Industrial OEMs now pre-qualify ester fluids to future-proof warranties, pulling demand ahead of stricter mandates.

Increasing Demand from Pharmaceutical Applications

Fatty alcohols serve as hydrophobic excipients in controlled-release tablets and stabilize proteins during lyophilization, yet uptake trails consumer segments because of extractables- and leachables hurdles under ICH Q3E. Cetostearyl alcohol complies with European Pharmacopoeia standards for hydroxyl value and heavy metals, enabling broader use in oral solid dosage forms. FDA GRAS Notice 895 for glyceryl behenate in sustained-release matrices demonstrates regulatory clarity, encouraging innovators to exploit lipid-based delivery systems. Petrochemical supply is favored for pharma grade due to tighter trace-metal control, whereas natural sources risk contamination through palm-oil refining.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile lauric-oil and ethylene feedstock prices | –1.1% | Global, acute for APAC natural-alcohol producers | Short term (≤ 2 years) |

| Over-capacity in Southeast Asian natural-alcohol plants | –0.6% | Malaysia, Indonesia, Thailand | Medium term (2–4 years) |

| Technical hurdles in catalytic hydro-downgrading of CO₂-derived alkanes | –0.4% | Global R&D centers, early pilots in Europe and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Lauric-Oil and Ethylene Feedstock Prices

Palm-kernel-oil prices surged 75% year-on-year to USD 2,063.59 per ton in March 2025 after El Niño trimmed yields in Indonesia and Malaysia, and feedstock represents up to 70% of natural-alcohol production cost. U.S. ethane stayed below USD 0.20 per gallon through 2024, sharpening cost gaps between American Ziegler plants and European naphtha crackers exposed to higher Brent prices. China’s coal-to-syngas path shields Zhejiang Jiahua from both lauric oil and ethylene volatility, highlighting regional cost asymmetry. Limited hedging practices—only 30% of oleochemical firms lock in palm-kernel-oil prices—leave margins exposed to 40% intra-year swings.

Over-Capacity in Southeast Asian Natural-Alcohol Plants

Indonesia’s oleochemical nameplate exceeds 23 million tpa, while regional demand grows below 3% per year, triggering price competition that eroded margins in 2H 2025 despite higher lauric-oil costs. Smaller non-integrated players lacking upstream assets faced the deepest squeeze, prompting KLK’s expansion in China to 500,000 tpa of specialty C16–C18 alcohols aimed at higher-margin personal-care grades. The EU Deforestation Regulation adds USD 50–80 per ton compliance cost to RSPO-certified feedstock, yet European buyers prefer petrochemical alcohols free from deforestation scrutiny, further hobbling Southeast Asian exports.

Segment Analysis

By Source: Petrochemical Routes Edge Up Market Share

Natural sources delivered 76.91% of the 2025 volume, but petrochemical routes are forecast to outpace the fatty alcohol market at a 4.39% CAGR through 2031 on the back of sub-USD 0.20-per-gallon U.S. ethane and coal-syngas economics in China. Sasol explicitly markets EUDR-exempt synthetic grades, a value proposition resonating with European detergent formulators wary of deforestation audits. Natural producers counter with RSPO and renewable-energy credentials, yet price overlooks provenance in commodity surfactant segments. Emerging bio-routes offer a third path: BASF’s CO₂-to-methanol pilot and Yanchang Petroleum’s 150 ktpa Fischer–Tropsch demo each aim to decouple fatty-alcohol output from both palm oil and fossil ethylene, though commercialization hinges on carbon-credit economics.

Natural alcohols maintain dominance in the fatty alcohol market share for surfactant applications. To defend volume, Southeast Asian players are investing in specialty applications—emollient-grade cetyl and stearyl alcohols fetch 30% premiums over C12–C14 detergent grades. Petrochemical producers, meanwhile, chase efficiency gains; U.S. Gulf Coast sites leverage cheap shale-ethane feedstock and Gulf logistics to supply Latin America at a lower delivered cost than Malaysian exporters despite the longer voyage.

Note: Segment shares of all individual segments available upon report purchase

By Application: Premiumization Lifts Personal Care

Surfactants retained 56.88% of 2025 demand, underpinning detergent and institutional cleaning volumes, yet personal-care lines are set to post a 4.72% CAGR—outstripping the fatty alcohol market. Sulfate-free shampoos and conditioners use 15–20% more fatty alcohol per unit and command 20–30% retail premiums, enabling brand owners to absorb higher input costs. Institutional laundries are reformulating toward concentrated liquids, raising fatty-alcohol ethoxylate dosage by 8–10% to achieve equivalent cleaning at lower dosages.

Lubricants and greases occupy a small slice of the fatty alcohol market size but enjoy regulatory tailwinds. EPA and EU criteria are diverting marine and hydraulic fluids toward fatty-alcohol esters, whereas high-temperature automotive oils remain mineral-oil territory. Plastics additives, pharmaceutical excipients, and food emulsifiers collectively account for under 10% of volume yet provide higher margins. Baerlocher’s global stearate expansions target PVC stabilization demand, and pharma-grade fatty alcohol faces supply tightness due to stringent batch traceability and heavy-metal limits.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific owned 44.28% of the 2025 volume and is projected to post a 5.09% CAGR to 2031, making it the epicenter of the fatty alcohol market. China runs more than 5 million tpa of oleochemical capacity, with Zhejiang Jiahua’s 200 ktpa coal-syngas plant achieving cost parity with Southeast Asian natural-alcohol providers. Yanchang Petroleum’s Fischer–Tropsch pilot further diversifies feedstock risk, potentially insulating Chinese producers from lauric-oil and ethylene volatility. India’s demand growth is consumption led; Godrej exports to 65 countries yet still imports pharma-grade alcohols, illustrating a quality-grade supply gap. Japan and South Korea remain technology exporters, with Kao’s proprietary alkoxylation lines serving premium personal care. Despite massive capacity, ASEAN suppliers face price pressure as Chinese and U.S. synthetic feedstocks undercut landed costs.

North America contributed about one-fifth of global volume in 2025. Shale-driven ethane output averaging 2.8 mbpd underpins sub-USD 3 per MMBtu feedstock, cementing the cost advantage of Gulf Coast Ziegler plants. Shell’s Monaca cracker expansion tightened Eastern U.S. ethane balances but also added synthetic capacity for export to Latin America. EPA lubricant mandates and sulfate-free personal-care adoption sustain growth, albeit below APAC rates.

Europe accounted for the significant consumption of fatty alcohol in 2025. While detergent consumption is saturated, specialty growth abounds; BASF’s bio-methanol alcoholates unit slated for 2027 targets high-purity niches where EUDR compliance raises barriers for natural imports. Sasol’s petrochemical grades find ready buyers because they circumvent deforestation rules. Nordic shipping lines lead marine lubricant conversion, aided by IFF–Kemira’s EUR 130 million Finnish biopolymer investment.

South America and the Middle East-Africa are witnessing rising demand for fatty alcohols. Brazil’s biodiesel boom supplies glycerine streams for hydrogenation, yet capacity lags demand, prompting imports of fatty-alcohol intermediates. Saudi Arabia leverages advantaged ethane from Aramco, with SABIC funneling surplus olefins into synthetic alcohols for Asian export. Sub-Saharan Africa remains small but is served by Sasol’s regional footprint.

Competitive Landscape

The fatty alcohol market is moderately fragmented, with many regional and international players operating in the market. Natural-alcohol giants like KLK are doubling down on backward integration to secure palm-oil feedstock. Technology intensity is rising. BASF commercialized castor-derived 2-Octyl Acrylate, demonstrating the readiness of renewable C8 alcohols, although castor acreage limitations in India and Brazil impede rapid scaling. REACH aquatic-toxicity updates tighten formulation leeway, nudging producers toward higher-purity derivatives.

Fatty Alcohol Industry Leaders

KLK OLEO

Wilmar International Ltd.

Sasol

BASF

Musim Mas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: BASF linked with Acies Bio to pursue CO₂-to-methanol fermentation that feeds fatty-alcohol synthesis, with pilot trials set for 2025 and commercial rollout dependent on carbon-credit pricing.

- July 2024: KLK Oleo lifted Zhangjiagang capacity to 500 ktpa, refocusing on C16–C18 specialty alcohols for personal-care formulations.

Global Fatty Alcohol Market Report Scope

Fatty alcohols are typically high-molecular-weight, straight-chain primary alcohols with as few as 4-6 carbons or as many as 22-26 carbons generated from natural fats and oils. The traditional sources of fatty alcohols have largely been various vegetable oils, which remain a large-scale feedstock. Fatty alcohols are also prepared from petrochemical sources. In the Ziegler process, ethylene is oligomerized using triethylaluminium, followed by air oxidation.

The fatty alcohol market is segmented by source, application, and geography. By source, the market is segmented into natural sources and petrochemical sources. By application, the market is segmented into surfactants, personal care and cosmetics, household and industrial cleaning, lubricants and greases, plastics additives, pharmaceutical excipients, food emulsifiers, and other industrial uses. The report also covers the market size and forecasts for the fatty alcohol market in 15 countries across major regions. For each segment, market sizing and forecasts are done in volume (tons).

| Natural |

| Petrochemical |

| Surfactants |

| Personal Care and Cosmetics |

| Household and Industrial Cleaning |

| Lubricants and Greases |

| Plastics Additives |

| Pharmaceutical Excipients |

| Food Emulsifiers |

| Other Industrial Uses |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Natural | |

| Petrochemical | ||

| By Application | Surfactants | |

| Personal Care and Cosmetics | ||

| Household and Industrial Cleaning | ||

| Lubricants and Greases | ||

| Plastics Additives | ||

| Pharmaceutical Excipients | ||

| Food Emulsifiers | ||

| Other Industrial Uses | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current volume of the fatty alcohol market and its forecast growth?

The market reached 4.3 million tons in 2026 and is projected to hit 5.26 million tons by 2031, reflecting a 4.09% CAGR.

Which application segment is expanding fastest?

Personal care leads with a 4.72% CAGR to 2031 as sulfate-free shampoos and conditioners raise fatty-alcohol loadings.

Why are petrochemical fatty alcohols gaining share despite sustainability concerns?

Sub-USD 0.20-per-gallon U.S. ethane and coal-syngas feedstocks yield lower production costs and allow EUDR-exempt positioning in Europe.

How is regulation shaping lubricant demand?

EPA Vessel General Permit and EU Ecolabel rules require high biodegradability, driving marine and hydraulic systems toward fatty-alcohol esters.

Which region will contribute most to future demand?

Asia-Pacific, led by China and India, is set to post a 5.09% CAGR through 2031 on rising FMCG and personal-care consumption.

What technological advances could disrupt supply?

BASF’s CO₂-to-methanol route and Yanchang Petroleum’s coal-syngas Fischer–Tropsch unit may introduce feedstock-agnostic synthetic capacity post-2027.