Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

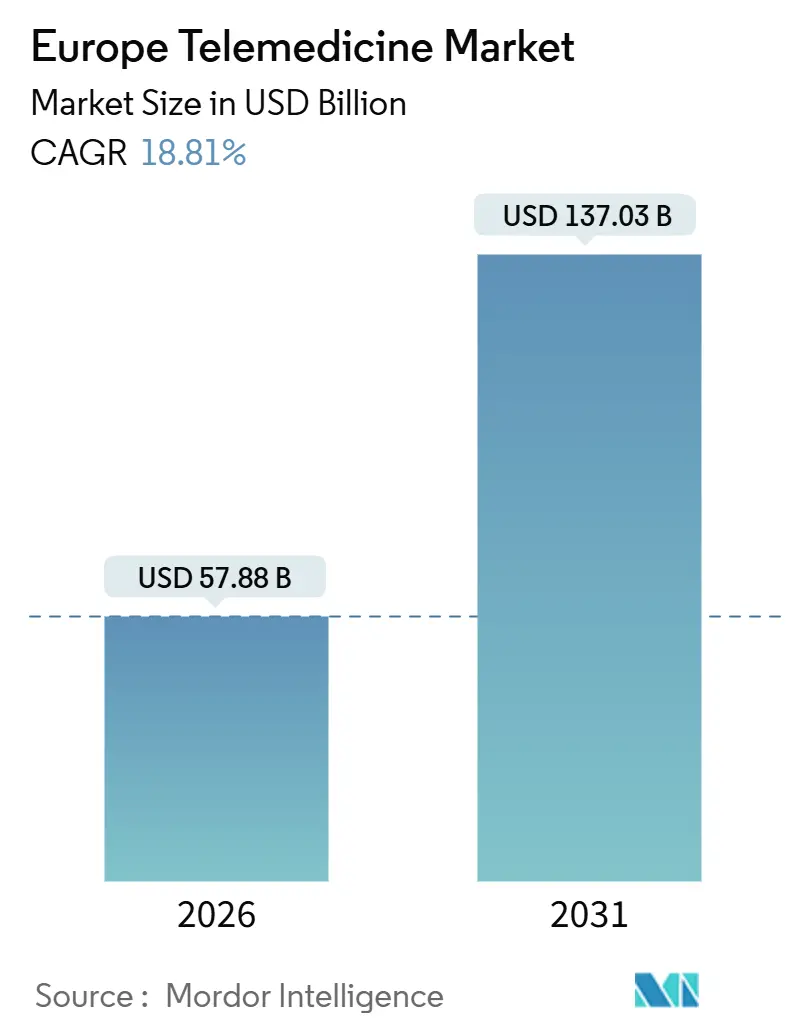

| Market Size (2026) | USD 57.88 Billion |

| Market Size (2031) | USD 137.03 Billion |

| Growth Rate (2026 - 2031) | 18.81% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Telemedicine Market Analysis by Mordor Intelligence

The Europe Telemedicine Market size is estimated at USD 57.88 billion in 2026, and is expected to reach USD 137.03 billion by 2031, at a CAGR of 18.81% during the forecast period (2026-2031).

Structural growth is anchored in the European Health Data Space Regulation, which requires cross-border health-data exchange and favors vendors with proven interoperability. The removal of Germany’s 30% video-consult cap in December 2023 triggered a 40% teleconsultation surge within six months, underscoring how reimbursement rules unleash latent demand. Cloud deployments are accelerating as 5G now covers 89% of EU residents, allowing mid-sized hospitals to avoid large upfront IT investments. Legacy PSTN telecare gear faces forced retirement ahead of the United Kingdom’s January 2027 switch-off, opening a USD 1.02 billion replacement cycle. Meanwhile, cybersecurity remains a top risk as 54% of European providers reported ransomware attacks in 2024.

Key Report Takeaways

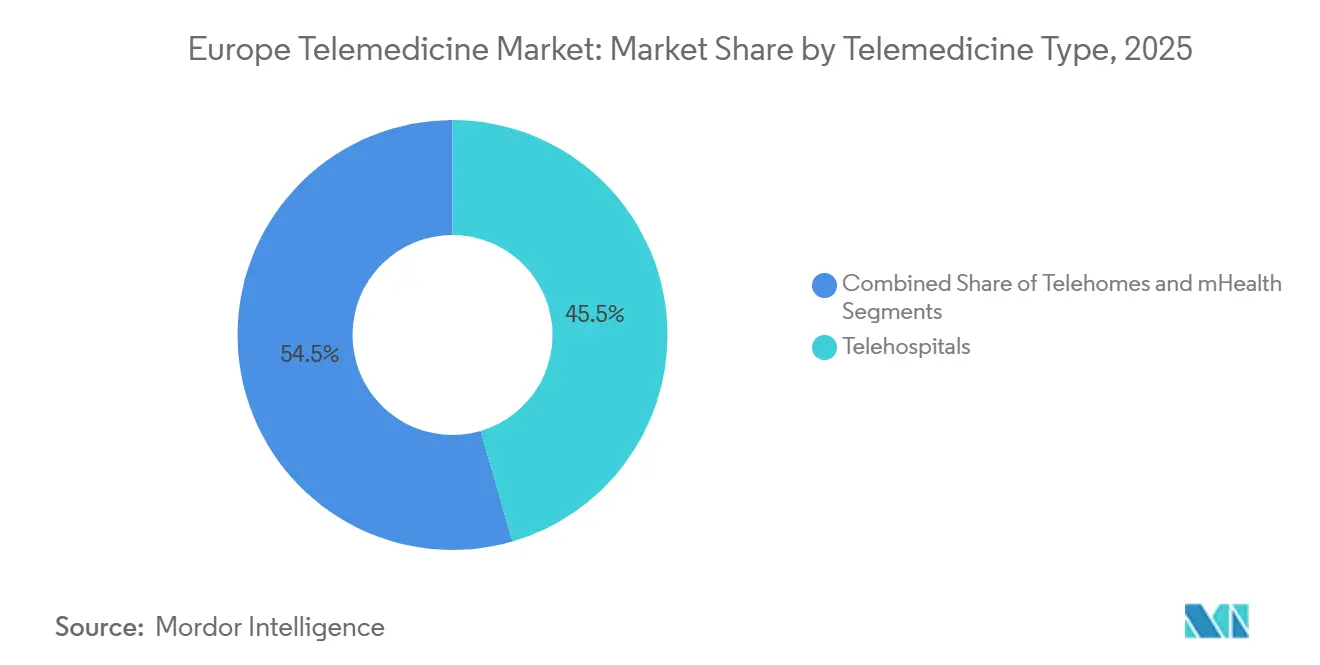

- By telemedicine type, telehospitals led with 45.55% revenue share in 2025, while telehomes are projected to expand at a 19.25% CAGR through 2031.

- By component, services accounted for 65.53% of the Europe telemedicine market size in 2025, whereas products are advancing at a 20.85% CAGR to 2031.

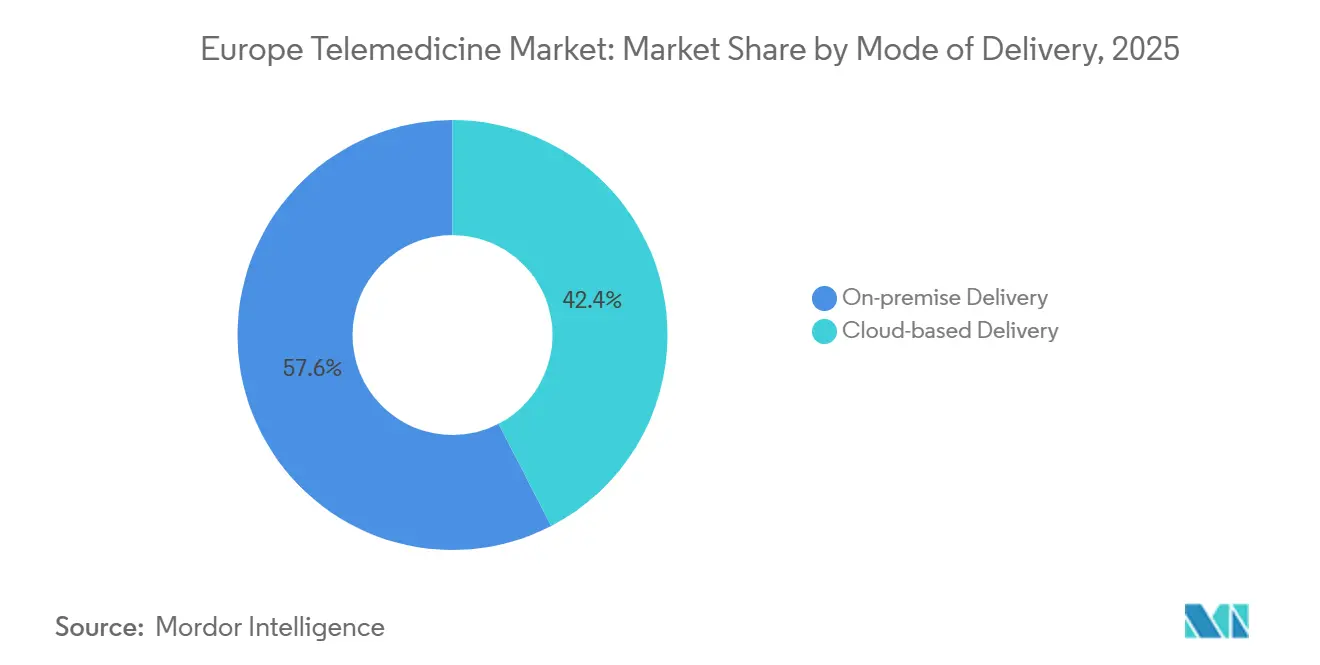

- By mode of delivery, on-premise systems held 57.63% share in 2025 and cloud solutions are growing at a 19.87% CAGR through 2031.

- By end-user, hospitals captured 52.13% share of the Europe telemedicine market size in 2025; home-care settings post the highest 22.7% CAGR over the period.

- By geography, Germany commanded 25.13% market share in 2025, while Spain records the fastest 19.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Telemedicine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing remote patient monitoring | +4.2% | Germany, United Kingdom, France, Nordics | Medium term (2-4 years) |

| Growing burden of chronic diseases | +3.8% | EU-27, especially Germany, Italy, Spain | Long term (≥ 4 years) |

| Government reimbursement reforms for digital health | +3.5% | Germany, France, Spain, Netherlands | Short term (≤ 2 years) |

| Expansion of 5G & fibre connectivity | +2.9% | Urban EU-27; rural Eastern Europe gaps | Medium term (2-4 years) |

| Cross-border value-based hospital procurement | +2.1% | Denmark, Sweden, Netherlands | Long term (≥ 4 years) |

| Pan-EU AI-triage APIs integrated into national EHR nodes | +2.4% | EU-27 under EHDS mandate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Increasing Remote Patient Monitoring

Remote monitoring converts episodic encounters into continuous data streams, allowing clinicians to intervene before decompensation and reduce emergency visits. Germany’s cap removal showed reimbursement, not preference, limited uptake, and Norway’s e-consult law cut primary-care backlogs by 18%. Wearable biosensors transmit glucose, blood pressure, and ECG data, letting specialists manage triple the patient load asynchronously. A 2024 European heart-failure study found 25% fewer 30-day readmissions, saving EUR 3,200 per patient annually. Remote programs therefore anchor demand growth for the Europe telemedicine market.

Growing Burden of Chronic Diseases

Chronic conditions drive 70% of European health spending, but only 30% of patients receive guideline-level monitoring due to capacity limits. Telemedicine lets endocrinologists review continuous glucose data remotely, replacing quarterly clinic visits. Every 1% shift from in-person to virtual chronic-disease follow-up saves EUR 2.1 billion annually across the bloc. Mental-health demand mirrors this trend; Norway’s eMeistring platform treated 40,000 users in 2024 at 60% of the face-to-face cost. These savings reinforce sustained expansion of the Europe telemedicine market.

Government Reimbursement Reforms for Digital Health

Eight of nine studied EU markets reimburse digital services. Germany’s DiGA pathway has approved 54 apps with negotiated prices, proving that clear tariffs spark adoption. France’s Ségur program allocated EUR 2 billion to hospital digitization. Spain pays 85% of physical-visit fees for teleconsults, while the United Kingdom targets 30% virtual outpatients by 2028. Policy alignment continues to amplify growth in the Europe telemedicine market.

Expansion of 5G & Fibre Connectivity

Europe counts 460,000 5G base stations, delivering the bandwidth for high-definition consults and teleradiology image transfers in under four hours. Fibre penetration tops 50% in 12 member states, enabling home-based tele-ICU programs. The United Kingdom’s full-fibre rollout supports migration from analog PSTN devices, critical before the 2027 switch-off. Edge nodes in 23 hospitals process AI locally while meeting GDPR residency rules. Connectivity progress widens the addressable base for the Europe telemedicine market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legal & reimbursement complexity | −1.8% | EU-27, high in Southern and Eastern states | Short term (≤ 2 years) |

| GDPR-driven data-privacy concerns | −1.5% | EU-27; Germany, France strictest | Medium term (2-4 years) |

| PSTN switch-off risking legacy telecare hardware | −1.2% | United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| Clinician digital-fatigue lowering post-COVID retention | −0.9% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legal & Reimbursement Complexity

Twenty-seven distinct licensing and billing regimes raise compliance costs that hinder smaller entrants, freezing Polish adoption at 3% of consultations. Cross-border care still demands multi-country licensure despite EHDS interoperability. Liability rules vary, inflating insurance premiums by up to 50% for multi-jurisdiction operators. Teleconsult fees range from EUR 15 in Spain to EUR 45 in Germany, forcing granular pricing engines. EU attempts to harmonize codes remain in committee, dragging on the Europe telemedicine market.

GDPR-Driven Data-Privacy Concerns

The CJEU’s 2024 ruling broadened “health data” to include pharmacy orders, exposing platforms to EUR 20 million fines for breaches[1]Court of Justice of the European Union, “Case C-252/21,” curia.europa.eu. Eighteen vendors exited Europe since 2023 over compliance costs. Germany demands on-shore hosting; France allows EU storage with safeguards, compelling multi-site data centers. Interoperability goals clash with national veto powers on exports. Frequent ransomware incidents erode trust, tempering growth in the Europe telemedicine market.

Segment Analysis

By Telemedicine Type: Hospitals Anchor, Homes Accelerate

Telehospitals accounted for 45.55% of the Europe telemedicine market share in 2025, with ICU and radiology workflows justifying dedicated cameras and secure networks. Remote intensivist oversight lowered hospital mortality by 15% that year. Telehomes, though smaller, will outpace the Europe telemedicine market at a 19.25% CAGR to 2031 as wearables support continuous chronic-care surveillance. National mandates to cut bed use, such as France’s EUR 400 million home-monitoring fund, accelerate adoption[2]French Ministry of Health, “Ségur du numérique en santé,” solidarites-sante.gouv.fr .

Hospital-at-home pilots in 42 facilities already show equal outcomes at 30% lower cost, fuelling policy momentum. mHealth apps leverage smartphone ubiquity yet still hunt viable revenue models. The NHS App hit 35 million users in 2024, giving governments scale but constraining innovation. Norway’s e-consult sick-leave feature saved EUR 25 million in productivity. Convergence across settings will blur categories, supporting diversified growth in the Europe telemedicine market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Services Dominate, Products Surge

Services held 65.53% of the Europe telemedicine market size in 2025, led by teleradiology, telepsychiatry, and tele-ICU consults. AI image assistance cut radiologist time per study by nearly half in Norway. Telepsychiatry volumes remain elevated, with eMeistring delivering CBT at 60% of traditional costs.

Products—hardware, software, connectivity—will grow 20.85% CAGR as the PSTN sunset drives device refreshes. Remote-monitoring kits and AI-stethoscopes integrate software subscriptions at EUR 50-150 per clinician monthly. Smartphone cameras now meet dermatology resolution standards, reducing hardware prices by 70%. Integration of predictive analytics into devices differentiates offerings and underpins long-term expansion of the Europe telemedicine market.

By Mode of Delivery: Cloud Gains on Premises

On-premise deployments owned 57.63% share in 2025, favored by large systems complying with data-residency mandates such as Germany’s BSI rule. However, cloud solutions will rise at 19.87% CAGR as mid-size providers pursue elasticity and lower capex. Doctolib processed 90 million visits on a French-hosted cloud in 2024, validating scale economics.

Hybrid models retain data locally while streaming video and analytics from the cloud, balancing compliance and performance. EHDS interoperability favors shared cloud connectors over bespoke interface builds, improving time-to-market. Edge servers in 23 hospitals already run AI inference with sub-100 ms latency, illustrating the architecture likely to dominate the Europe telemedicine market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Hospitals Lead, Homes Outpace

Hospitals commanded 52.13% share of the Europe telemedicine market size in 2025, leveraging economies across multiple departments. NHS tariffs now reward 30% virtual outpatients by 2028. Yet home-care settings will grow fastest at 22.7% CAGR, enabled by remote cardiac, pulmonary, and diabetic monitoring that cut 30-day readmissions by 25%.

Payers reward enrollment, offering 5-10% premium discounts, and Spain commits EUR 1.5 billion for home infrastructure. Decentralized clinical trials share technology stacks, spurring vendor scale. Hospital-at-home schemes demonstrate inpatient-equivalent outcomes at 30% lower cost, ensuring sustained penetration of home models within the Europe telemedicine market.

Geography Analysis

Germany led the Europe telemedicine market with 25.13% share in 2025 thanks to DiGA reimbursement, e-prescriptions, and post-cap teleconsult surges. Strict data-residency rules raise hosting costs but sustain local IT demand. The United Kingdom ranks second, supported by 35 million NHS App users and upgraded digital infrastructure, yet faces PSTN-hardware migration risks. France benefits from Doctolib network effects that entrench user loyalty.

Spain is poised for 19.81% CAGR, double the bloc average, as teleconsults already exceed one-quarter of visits and EUR 1.5 billion funds digital integration. Italy’s PNRR sets aside EUR 1.7 billion for rural digital health, promising catch-up momentum. Nordic nations maintain highest maturity scores, while Eastern Europe lags on funding and reimbursement. Estonia’s near-universal e-records showcase scalable models for small states. Denmark’s outcome-based tenders demand 15% readmission cuts, shaping procurement.

EHDS will force convergence by 2029, yet linguistic differences still depress satisfaction by 22% in cross-language consults, limiting cross-border telemedicine to bilingual regions. Overall, geographic disparities present both risk and opportunity within the Europe telemedicine market.

Competitive Landscape

No company commands over signficaint share, leaving moderate fragmentation, yet network effects accelerate consolidation. Doctolib’s 90 million consults exhibit winner-take-most dynamics. Large med-techs—Philips, Medtronic, IBM—bundle telemedicine with existing devices, locking clients into multi-year contracts[3]Koninklijke Philips N.V., “Investor Presentation 2025,” philips.com. Pure-plays struggle as fee parity erodes margins; 18 exited since 2023.

Specialty niches such as rare diseases and mental health offer white-space growth. AI-triage patents rose 35% year-over-year, signaling hardware-software convergence. EHDS will commoditize video functions, shifting competition toward predictive analytics and outcome contracts. Persistent ransomware risks, with 71% of breaches disrupting care, elevate security as a differentiator. Overall, competitive intensity remains high as the Europe telemedicine market evolves toward platform ecosystems.

Europe Telemedicine Industry Leaders

IBM Corporation

Koninklijke Philips NV

Medtronic Plc

Veradigm LLC

AMD Global Telemedicine

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: EPA Secretary for Sections and Editor-in-Chief of European Psychiatry joined an EU focus group on telemedicine in mental health, an initiative commissioned by the European Health and Digital Executive Agency (HaDEA) and delivered by ICF to assess how existing Union legislation applies to telemedicine services.

- May 2025: A telemedicine pilot launched in the Traunstein district under the Technical University of Munich (TUM) to enable primary-care physicians to provide faster, more efficient care to nursing-home residents, with the goal of reducing avoidable hospital admissions and improving overall patient outcomes.

Europe Telemedicine Market Report Scope

As per the scope of the report, telemedicine refers to the remote diagnosis and treatment of patients with the help of telecommunications technology. Various kinds of telemedicine services, along with devices, have been tracked in the report.

The Europe telemedicine market is segmented by telemedicine type, component, mode of delivery, end-user, and country. By telemedicine type, the market is categorized into telehospitals, telehomes, and mHealth (mobile health). By component, it is divided into products, which include hardware, software, and other products, and services, which encompass telepathology, telecardiology, teleradiology, teledermatology, telepsychiatry, and tele-ICU. By mode of delivery, the segmentation includes on-premise delivery and cloud-based delivery. By end-user, the market is segmented into hospitals and clinics, home-care settings, payers and insurers, and others (NGOs and pharma-sponsored programs). By country, the market is analyzed across Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe.

By Telemedicine Type

| Telehospitals |

| Telehomes |

| mHealth (Mobile Health) |

By Component

| Products | Hardware |

| Software | |

| Other Products | |

| Services | Telepathology |

| Telecardiology | |

| Teleradiology | |

| Teledermatology | |

| Telepsychiatry | |

| Tele-ICU |

By Mode of Delivery

| On-premise Delivery |

| Cloud-based Delivery |

By End-user

| Hospitals & Clinics |

| Home-care Settings |

| Payers & Insurers |

| Others (NGOs, Pharma-sponsored Programs) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Telemedicine Type | Telehospitals | |

| Telehomes | ||

| mHealth (Mobile Health) | ||

| By Component | Products | Hardware |

| Software | ||

| Other Products | ||

| Services | Telepathology | |

| Telecardiology | ||

| Teleradiology | ||

| Teledermatology | ||

| Telepsychiatry | ||

| Tele-ICU | ||

| By Mode of Delivery | On-premise Delivery | |

| Cloud-based Delivery | ||

| By End-user | Hospitals & Clinics | |

| Home-care Settings | ||

| Payers & Insurers | ||

| Others (NGOs, Pharma-sponsored Programs) | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe telemedicine market in 2026?

It stands at USD 57.88 billion with an 18.81% CAGR outlook to 2031.

Which segment grows fastest by 2031?

Home-care settings lead with a 22.7% CAGR as aging populations adopt remote monitoring.

Why is Spain the quickest-growing geography?

High teleconsultation penetration plus EUR 1.5 billion government funding drive a 19.81% CAGR.

What triggers the product-replacement boom?

The January 2027 U.K. PSTN switch-off requires 1.8 million legacy telecare devices to migrate to IP.

How do EU rules shape data exchange?

Regulation EU 2025/327 mandates AI-triage APIs in all national EHR nodes by 2029, forcing interoperability.

What cybersecurity risks influence adoption?

Ransomware hit 54% of European providers in 2024, prompting 72-hour breach reporting under GDPR.