| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 16.36 Billion |

| Market Size (2030) | USD 20.44 Billion |

| CAGR (2025 - 2030) | 4.55 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe Wood Pellet Market Analysis

The Europe Wood Pellet Market size is estimated at USD 16.36 billion in 2025, and is expected to reach USD 20.44 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

The European wood pellet industry has witnessed substantial infrastructure development and capacity expansion in recent years, reflecting the growing importance of wood biomass in the region's energy transition. As of 2023, the total production capacity reached 27.2 million metric tons, supported by approximately 774 wood pellet plants across Europe. This robust infrastructure development demonstrates the industry's maturity and readiness to meet increasing demand. The sector has also seen significant technological advancements in pellet production and combustion efficiency, leading to improved product quality and reduced environmental impact.

The industry is experiencing a notable shift in power generation applications, particularly in Northwest Europe. Since January 2024, the combined wood pellet-fired power output has dramatically increased to 2.9 GW from 150 MW, indicating growing adoption in the power generation sector. This transformation is further supported by various government initiatives and policy frameworks designed to promote renewable energy sources. For instance, in April 2024, the European Commission approved a EUR 900 million French scheme to support companies investing in sustainable biomass and renewable hydrogen energy production, demonstrating strong institutional backing for the industry.

The market is witnessing significant developments in industrial-scale conversions and infrastructure upgrades. A notable example is France's announcement in October 2023 to convert two coal-fired power plants with a combined capacity of 1.8 GW to biomass pellet by 2027. This type of large-scale conversion project represents a growing trend across Europe as countries seek to reduce their reliance on fossil fuels while maintaining existing power generation infrastructure. The industry is also seeing innovations in pellet manufacturing processes, storage solutions, and transportation systems to improve efficiency and reduce costs.

The European wood pellet market is experiencing a transformation in its supply chain dynamics and quality standards. The industry has developed sophisticated certification systems and quality control measures to ensure consistent product quality and sustainability. This evolution has led to improved standardization across the industry, with manufacturers increasingly adhering to stringent quality parameters for both industrial and residential applications. The market has also adapted to changing supply patterns, particularly following the EU's import ban on Russian industrial wood pellet in summer 2022, which has created new opportunities for transatlantic trade and prompted the development of alternative supply routes.

Europe Wood Pellet Market Trends

Clean Energy Generation to Drive Wood Pellets Market

The transition towards cleaner energy sources has positioned wood pellets as a viable alternative for power generation, particularly in replacing coal-fired plants. When combusted, wood pellets produce 80-85% less CO2 emissions than coal, while also releasing lower levels of sulfur, chlorine, and nitrogen, making them an environmentally responsible choice for power generation. The conversion of existing coal-fired plants to pellet fuel provides a significantly higher CO2 reduction at a lower net monetary cost per avoided metric ton compared to other renewable technologies, with studies showing a 26.3% lower cost per avoided metric ton of CO2 for modern pulverized coal power station conversions to sustainably sourced wood fuel pellets.

Recent governmental support and initiatives have further strengthened the position of wood pellets in clean energy generation. In December 2023, the UK government announced the extension of its Contract for Difference (CfD) program to support bioenergy with carbon capture and storage (BECCS), aiming to develop a competitive market in carbon capture, usage, and storage by 2035. Additionally, in April 2024, the European Commission approved a EUR 900 million French scheme to support companies investing in biomass and renewable hydrogen for energy production, aligning with the Green Deal Industrial Plan. These developments, coupled with the fact that biomass-fueled power stations accounted for 11% of total UK electricity generation in 2022 (up from 8% in 2010), demonstrate the growing role of wood pellets in clean energy generation.

Understand The Key Trends Shaping This Market

Download PDF

Heat-Supply Applications to Drive Wood Pellets Market

The residential and commercial heating sector has emerged as a significant driver for the wood pellet market, driven by the increasing adoption of wood pellet heating systems and their cost-effectiveness compared to traditional heating methods. According to the Stove Industry Alliance, wood-based heating fuels are proving to be substantially more economical, costing households 74% less per kWh than electric heating and 21% less than gas heating. The superior burning characteristics of heating pellets, including high density, low moisture content (below 10%), and minimal ash content (less than 2%), make them more efficient than conventional firewood and traditional open-wood fireplaces, while also producing cleaner combustion with reduced smoke and soot emissions.

The market has witnessed substantial growth in heating system installations, particularly in countries with prolonged winter seasons. In Germany alone, the number of wood pellet heating systems has increased by approximately 60% since 2021, reaching almost 800,000 installations by 2024. This growth is supported by innovative service models, such as heat supply contracts offered by companies like Balcas Energy, where consumers only pay for the kilowatt-hours of heat they use while the company manages the biomass heating infrastructure. The expansion of district heating networks, especially in urban areas, has created additional opportunities for wood energy consumption. For instance, Poland, which has the most extensive district heating infrastructure in Europe, aims to achieve 28% renewable-generated heat by 2030, indicating significant potential for wood energy adoption in district heating applications.

Segment Analysis: Application

Heating Segment in Europe Wood Pellet Market

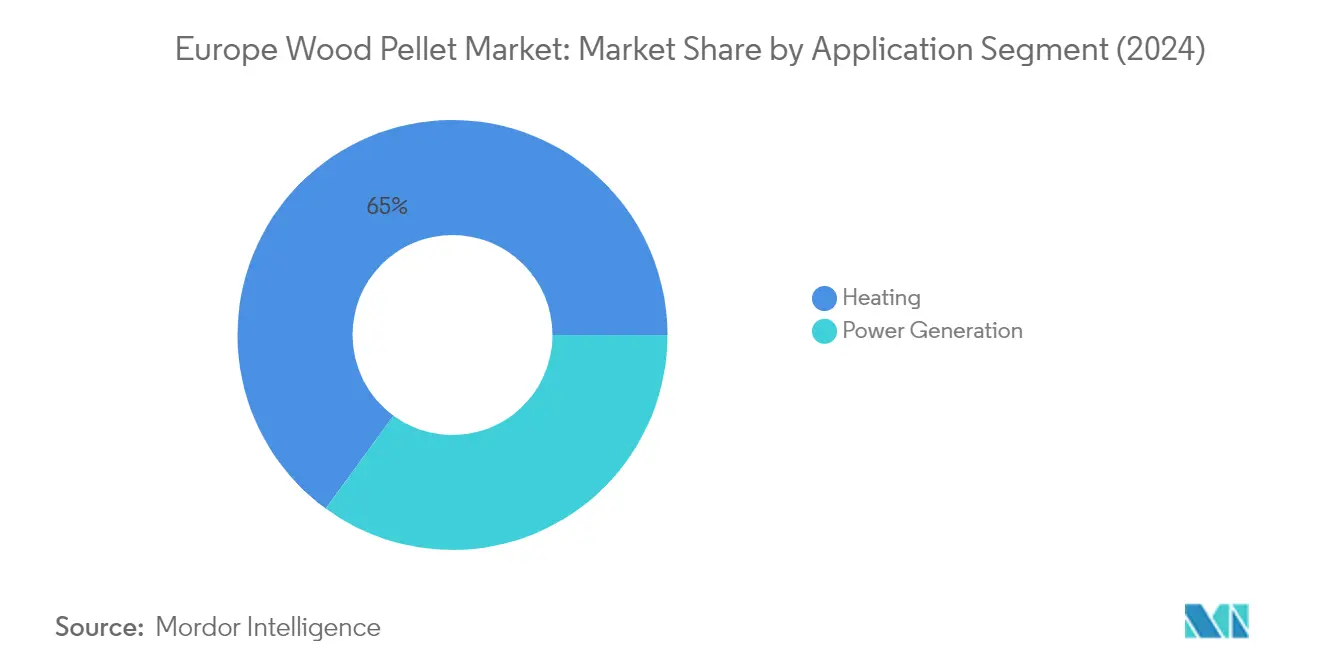

The heating segment dominates the Europe wood pellet market, commanding approximately 65% market share in 2024, while also exhibiting the strongest growth trajectory with a projected growth rate of around 6% from 2024-2029. The residential and commercial sectors primarily drive this segment's dominance, using heating pellets for home heating applications through heat stoves and furnaces. Due to the prolonged winter season, heating applications are extensively utilized in European countries such as Iceland, Poland, the Netherlands, Germany, Finland, the Czech Republic, Austria, and France. The growth in wood pellet heat supply contracts, particularly in cold countries, continues to establish a robust market presence. Companies like Balcas Energy provide tailored heat contracts to end consumers, bearing the responsibility of setting up biomass heating infrastructure at consumer premises, where consumers pay only for the kilowatt-hour of heat they use. Additionally, the number of consumers using district heating systems driven by biomass fuels such as wood pellets is gaining momentum, supported by the European Union's mandate to reduce fossil fuel incorporation in heating applications.

Power Generation Segment in Europe Wood Pellet Market

The power generation segment represents a significant portion of the Europe wood pellet market, accounting for approximately 35% of the market share in 2024. This segment utilizes pellet fuel as a renewable alternative to coal in power plants, offering a more environmentally sustainable solution for electricity generation. Several methods are employed for power generation, including direct firing, where wood fuel pellets are directly fed into boilers powering steam turbines, co-firing with coal in existing power plants, cogeneration for both electricity and heat production, and gasification processes. The segment's growth is particularly driven by government initiatives and policies promoting clean energy generation, such as the European Union's mandate to reduce carbon emissions. For instance, in October 2023, the French government announced plans to convert two coal-fired power plants with a combined capacity of 1.8 GW to wood biomass by 2027, demonstrating the ongoing transition toward more sustainable power generation methods.

Europe Wood Pellet Market Geography Segment Analysis

Wood Pellet Market in the United Kingdom

The United Kingdom represents the largest wood pellet market in Europe, commanding approximately 21% of the total market share in 2024. The country's wood pellet industry is primarily driven by power generation, with the Drax power station in North Yorkshire being a cornerstone facility. This facility, which has converted four of its six 65 MWe generating units to run exclusively on wood pellets, produces around 5% of the United Kingdom's total electricity. The UK's commitment to clean energy transition is evident through its Contract for Difference (CFD) program, which was extended in December 2023 to support bioenergy with carbon capture and storage (BECCS). The government's plan to develop a competitive market in Carbon Capture, Usage, and Storage (CCUS) by 2035 is expected to boost the economy by EUR 5 billion annually by 2050. The residential construction sector's growth, driven by population growth, urbanization, and government initiatives addressing housing shortages, is creating additional demand for wood pellets in heating applications.

Wood Pellet Market in France

France's wood pellet market is projected to demonstrate remarkable growth, with an expected CAGR of approximately 9% from 2024 to 2029. The country has positioned itself as a rapidly evolving market in the European biogas plant sector, supported by progressive government policies and abundant feedstock availability. The collective pellet heating method has shown significant expansion, with around 2,500 collective, tertiary, and industrial boiler rooms utilizing wood pellets by the end of 2023. The residential sector has been a major contributor to the industry's development, with more than 80% of the country's consumption directed towards residential applications. The Heat Fund, established by the French government and managed by ADEME, has been instrumental in supporting renewable heat systems, having aided over 7,100 projects between 2009 and 2022. The country's commitment to carbon neutrality by 2050 has created a favorable environment for wood pellet market growth, with biomass pellets playing a crucial role in achieving this target.

Wood Pellet Market in Germany

Germany has established itself as a significant player in the European wood pellet market, with its strategic approach to renewable energy transition. The country's market benefits from government programs that indirectly support wood pellet consumption for newly erected buildings and retrofitting heating systems with biomass boilers in existing buildings. As of 2023, Germany operated 50 production facilities for wood pellet manufacturing with a total annual production capacity of 3.9 million metric tons. The German law mandates that all buildings erected after 2009 must use a certain share of renewable energy for heating and cooling requirements, which has been a significant driver for increasing wood pellet consumption in residential and commercial sectors. The country's commitment to phasing out coal-fired power plants and its position as a frontrunner in renewable energy adoption has created a favorable environment for wood pellet market growth.

Wood Pellet Market in the Netherlands

The Netherlands has developed a robust wood pellet market infrastructure, primarily focused on power generation through co-firing processes. The country's transition towards cleaner energy sources is guided by the Dutch Climate Law, which aims for significant emissions reduction and carbon neutrality by 2050. The Dutch cabinet recognizes biomass as an essential energy source in achieving a climate-neutral and circular economy. The market has benefited from the Dutch Energy Accord, which emphasized reducing CO2 emissions by around 80% by 2050. The country's strategic location and well-developed port infrastructure have facilitated efficient import and distribution networks. Despite having domestic production capabilities, the Netherlands maintains a significant import volume to meet its demand, primarily sourcing from countries like the United States, Portugal, and the Baltics. The focus on wood energy and solid biofuel is integral to the country's energy strategy.

Wood Pellet Market in Other Countries

The wood pellet market in other European countries, including Belgium, Spain, and Russia, demonstrates varying degrees of market maturity and growth potential. Belgium, despite being a relatively young market, has established itself in the power generation sector through co-firing applications. Spain has positioned itself as a major producer and net exporter of wood pellets, with significant forest resources providing a strong foundation for industry growth. Russia, despite recent geopolitical challenges, maintains its production capabilities and has diversified its export destinations. These countries are implementing various support schemes and incentives to promote wood pellet adoption, particularly in the residential heating sector. The market dynamics in these regions are influenced by factors such as government policies, infrastructure development, and the increasing emphasis on renewable energy sources.

Get Analysis on Important Geographic Markets

Download PDF

Europe Wood Pellet Industry Overview

Top Companies in European Wood Pellet Market

The European wood pellet market is led by established players like Stora Enso Oyj, Enviva Partners LP, AS Graanul Invest, Drax Group, and German Pellets GmbH. These companies are increasingly focusing on product innovation through advanced technologies like torrefaction to improve pellet quality and energy content. Operational agility is demonstrated through strategic supply chain improvements, with companies implementing blockchain and AI technologies for real-time tracking and efficiency optimization. Market leaders are pursuing aggressive expansion strategies through acquisitions and new plant establishments across Europe, particularly in regions with abundant forest resources. There is also a growing trend toward vertical integration, with companies investing in both wood pellet manufacturing facilities and distribution networks to maintain better control over the value chain. Sustainability certifications and environmental compliance have become key differentiators, with major players obtaining multiple certifications to enhance their market positioning.

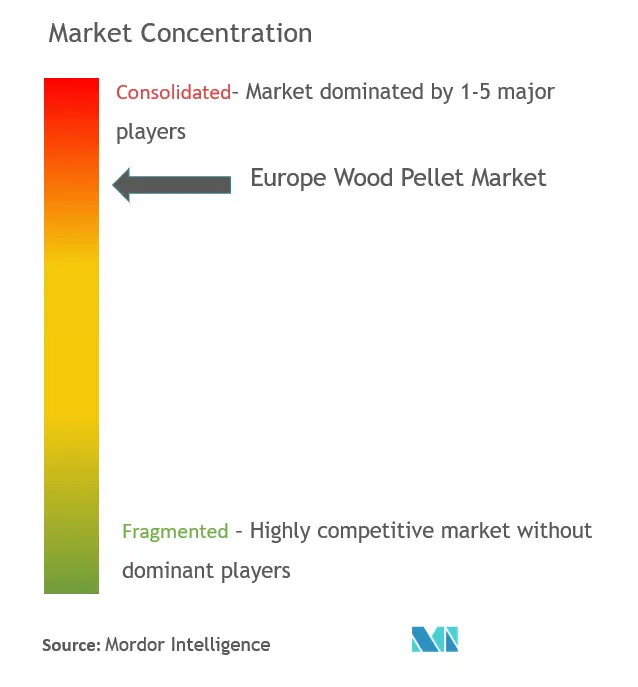

Fragmented Market with Strong Regional Players

The European wood pellet market exhibits a moderately fragmented structure, characterized by a mix of large multinational corporations and specialized regional manufacturers. The market features both vertically integrated forest product companies that have diversified into pellet production and specialized pellet manufacturers focused solely on this segment. While global players like Drax Group and Enviva Partners maintain significant market presence through their extensive production and distribution networks, regional players have carved out strong positions in their respective local markets through deep customer relationships and efficient supply chains.

Recent market activities indicate an increasing trend toward consolidation through strategic acquisitions and partnerships. Notable examples include LEAG Group's acquisition of Wismar Pellets and Rotom Europe's expansion through the purchase of GPP and All Pallets Limited. These moves reflect the industry's evolution toward more integrated operations and broader geographic coverage. The market also sees active participation from forest product companies that are expanding their renewable energy portfolios through pellet production, creating a diverse competitive landscape with varying business models and operational scales.

Innovation and Sustainability Drive Future Success

Success in the European wood pellet market increasingly depends on companies' ability to innovate while maintaining strong sustainability credentials. Market leaders are investing in research and development to improve production efficiency and product quality, with technologies like ZeroFlame combustion and advanced torrefaction processes becoming key differentiators. The ability to secure reliable raw material supply chains while meeting stringent environmental standards has become crucial for maintaining market position. Companies are also focusing on developing strong relationships with end-users across both industrial and residential segments, as customer concentration in certain sectors poses both opportunities and risks.

Future market success will require companies to navigate evolving regulatory landscapes, particularly regarding renewable energy policies and environmental standards. New entrants face moderate barriers but can gain ground through technological innovation and strategic partnerships with established players. The threat of substitution from alternative renewable energy sources necessitates continuous product development and market adaptation. Companies that can effectively balance cost competitiveness with environmental sustainability, while maintaining operational flexibility to meet varying customer demands, will be better positioned for long-term success. The development of value-added products and services, combined with strong distribution networks, will be crucial for both incumbents and new market entrants. Additionally, the integration of industrial wood pellet production into existing operations offers potential for growth in the sustainable biomass sector.

Europe Wood Pellet Market Leaders

-

Stora Enso Oyj

-

Enviva Partners LP

-

AS Graanul Invest

-

Segezha Group PJSC

-

Drax Group PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Europe Wood Pellet Market News

- February 2024: Graanul Invest announced the launch of the premium pellet brand, g Graanul, which is expected to provide Baltic customers with an affordable, high-quality renewable energy solution. This launch is an initiative taken by the company to broaden its network and presence in the Baltic region.

- October 2023: The French government announced its plans to convert two coal-fired power plants to biomass by 2027. The study showed that the potential demand for pellet fuel is significant at the two French power generating stations with a combined capacity of 1.8 GW. The two plants, namely the 1.2 GW Cordemais and 600 MW Emile Hutchet plant in Saint Avold, were initially set to close by 2022. However, the energy crisis instigated by Russia's invasion of Ukraine and the shutdown of nuclear reactors in France led to a delay.

Europe Wood Pellets Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Heat-supply Applications

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternative Clean Energy Sources and Ending of Supportive Government Schemes for Wood Pellets

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

-

5.2 Geography

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Netherlands

- 5.2.5 Belgium

- 5.2.6 Spain

- 5.2.7 Russia

- 5.2.8 Rest of Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Stora Enso Oyj

- 6.3.2 Enviva Partners LP

- 6.3.3 AS Graanul Invest

- 6.3.4 Drax Group PLC

- 6.3.5 Segezha Group PJSC

- 6.3.6 Svenska Cellulosa Aktiebolaget SCA

- 6.3.7 German Pellets GmbH

- 6.3.8 Pure Biofuel Ltd

- 6.3.9 Pfeifer Group

- 6.3.10 Erdenwerk Gregor Ziegler GmbH

- *List Not Exhaustive

- 6.4 Market Ranking Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications and Advancements in the Wood Pellet Technology

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Wood Pellet Industry Segmentation

Wood pellets are renewable fuels manufactured from compressed sawdust or wood chips. They can be used to heat houses and businesses as a biomass fuel. Wood pellets can be made from forest residues and low-quality logs that can be handled as rubbish.

The European wood pellet market is segmented by application and geography. By application, the market is segmented into heating and power generation. The report also covers the market size and forecasts across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Application | Heating |

| Power Generation | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Belgium | |

| Spain | |

| Russia | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe Wood Pellets Market Research FAQs

How big is the Europe Wood Pellet Market?

The Europe Wood Pellet Market size is expected to reach USD 16.36 billion in 2025 and grow at a CAGR of 4.55% to reach USD 20.44 billion by 2030.

What is the current Europe Wood Pellet Market size?

In 2025, the Europe Wood Pellet Market size is expected to reach USD 16.36 billion.

Who are the key players in Europe Wood Pellet Market?

Stora Enso Oyj, Enviva Partners LP, AS Graanul Invest, Segezha Group PJSC and Drax Group PLC are the major companies operating in the Europe Wood Pellet Market.

What years does this Europe Wood Pellet Market cover, and what was the market size in 2024?

In 2024, the Europe Wood Pellet Market size was estimated at USD 15.62 billion. The report covers the Europe Wood Pellet Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Wood Pellet Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Wood Pellet Market Research

Mordor Intelligence provides a comprehensive analysis of the wood pellet and wood fuel pellet industry. We leverage extensive expertise in sustainable biomass research. Our detailed examination covers the entire value chain. This includes wood pellet manufacturing processes such as wood densification and compressed wood fuel production. We also explore end-use applications like wood pellet heating systems. The report encompasses various product segments, including timber pellet, wood chip, and sawdust pellet manufacturing. It provides crucial insights into biomass pellet market dynamics across Europe.

Stakeholders in the wood energy sector benefit from our actionable intelligence. This information is available in an easy-to-read report PDF for immediate download. The analysis covers critical aspects of industrial wood pellet production and solid biofuel applications. It examines the growing importance of wood biomass in renewable energy strategies. Our research thoroughly evaluates heating pellet technologies and their market potential. This offers valuable insights for businesses involved in pellet fuel production and distribution. The report's comprehensive coverage of wood densification technologies and market trends enables informed decision-making. Industry participants can thus capitalize on emerging opportunities.