Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

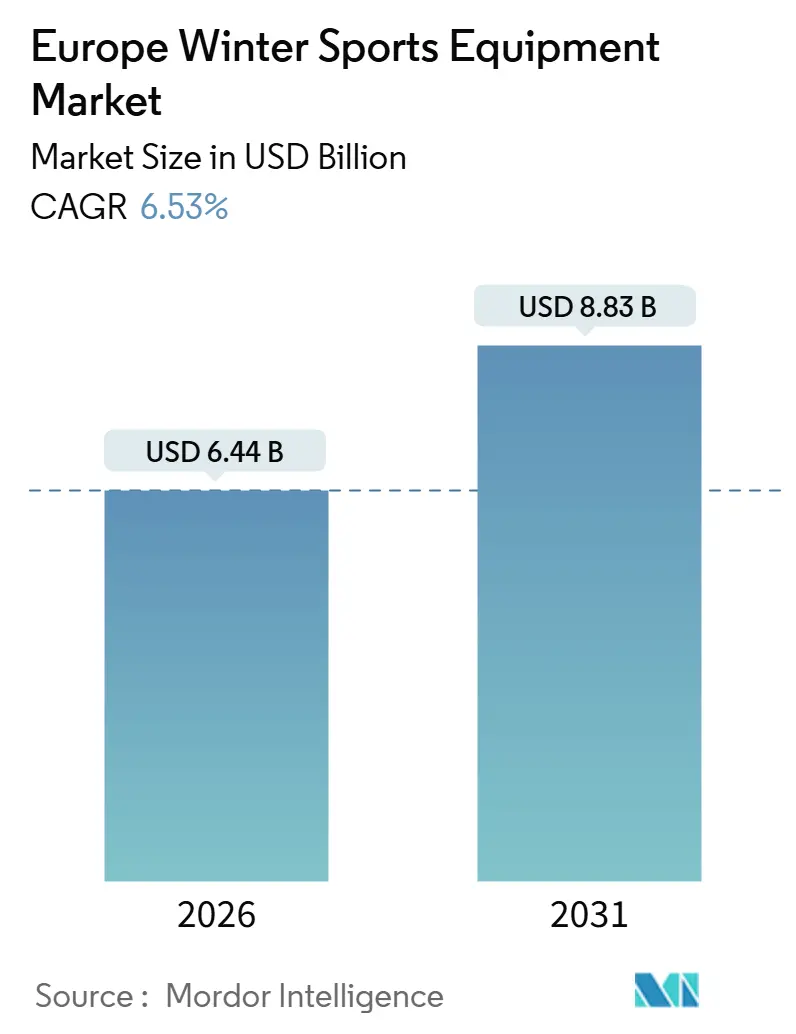

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 8.83 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Winter Sports Equipment Market Analysis by Mordor Intelligence

The European winter sports equipment market size is valued at USD 6.44 billion in 2026 and is projected to reach USD 8.83 billion by 2031, advancing at a 6.53% CAGR over the period. Demand is shifting beyond classic alpine skiing toward freestyle and backcountry disciplines as Gen Z and female participation programs gain traction, while lighter, bio-based composites meet EU chemical regulations and reduce product weight. Olympic visibility from Milano Cortina 2026, record Nordic-camp enrollments, and retailer investment in youth sizing accelerate equipment turnover. At the same time, rental models are shifting toward premium fleets and subscription bundles, challenging the ownership-centric revenue base that defined the sector prior to 2024. Manufacturers with in-house resin and fit-customization capabilities now squeeze development cycles into 18-24 months, defending share against agile startups that rely on contract production yet struggle with PFAS compliance costs.

Key Report Takeaways

- By sports type, skiing captured 63.55% of the European winter sports equipment market share in 2025, whereas snowboarding logged the highest growth at a 7.83% CAGR through 2031.

- By equipment category, skis and snowboards accounted for 48.24% of the European winter sports equipment market size in 2025; apparel and accessories are forecast to expand at a 7.27% CAGR to 2031.

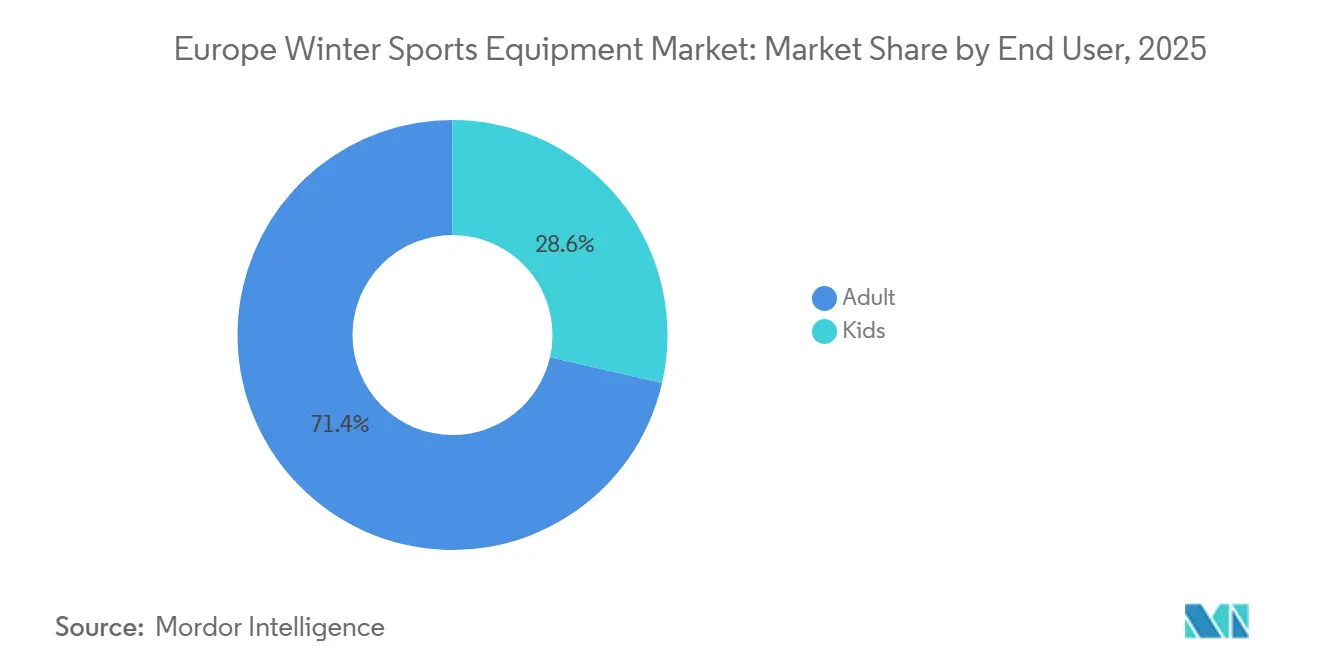

- By end user, adults generated 71.42% of revenue in 2025, but the kids segment is set to rise at a 7.57% CAGR as SnowKidz enrollment surges.

- By distribution channel, offline retail accounted for 71.69% of 2025 sales, while online platforms are expected to grow at an 8.49% CAGR, driven by virtual fitting tools and flexible rental subscriptions.

- By geography, Germany led with 22.83% of regional revenue in 2025, and Spain is poised for the fastest country-level CAGR at 8.14% thanks to Pyrenean resort upgrades.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Winter Sports Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Winter-tourism investment in Alpine and Nordic resorts | +0.9% | France, Switzerland, Austria, Italy; Norway, Finland, Sweden | Medium term (2-4 years) |

| Rising Gen Z demand for freestyle and snowboarding | +1.2% | Germany, France, Spain, UK | Short term (≤2 years) |

| Technological breakthroughs in lightweight equipment | +0.8% | Austria, Germany, Italy | Long term (≥4 years) |

| Female and youth participation programs | +0.7% | Switzerland, Norway, France | Medium term (2-4 years) |

| Visibility of marquee winter sports events | +0.6% | Italy, France, Switzerland | Short term (≤2 years) |

| EU carbon-tax incentives for bio-based materials | +0.5% | EU-27 member states across Western, Central, and Eastern Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Winter-Tourism Investment in Alpine and Nordic Resort Infrastructure

France’s Avenir Montagnes plan allocated EUR 331 million between 2021 and 2022 to modernize mountain infrastructure, including lift replacements and expanded snowmaking capacity, while Compagnie des Alpes, Europe’s largest ski-area operator, reported 2024 capital expenditures focused on high-altitude lifts and energy-efficient snow guns[1]Source: French Government, “Avenir Montagnes Investment Plan,” gouvernement.fr. These investments extend operating seasons by 3-4 weeks at mid-altitude resorts, directly boosting equipment utilization and rental turnover. Nordic destinations follow a similar trajectory: Finland’s Lapland region recorded 1.374 million foreign winter overnights in 2024–25, up 7% year-on-year, as resorts enhanced cross-country trail grooming and biathlon facilities, according to Visit Finland. The strategic implication is that infrastructure spending generates a multiplier effect, with each EUR 1 million invested in lifts and snowmaking estimated to produce approximately EUR 2.5 million in downstream equipment sales and rentals over five years, per Domaines Skiables de France[2]Source: Domaines Skiables de France, “Snowmaking Cost Analysis,” domaines-skiables.fr. However, the capital-intensive nature of these projects concentrates benefits among established resorts, leaving smaller operators reliant on natural snow and vulnerable to climate variability.

Growing Popularity of Snowboarding and Freestyle Disciplines Among Gen Z

Snowboarding is projected to grow at a 7.83% CAGR through 2031, driven by Gen Z’s preference for park-and-pipe progression over traditional downhill skiing and amplified by social-media visibility of freestyle tricks, as well as the FIS Alps Tour, which hosts competitions for 14–18-year-olds across European resorts. Burton’s Step On binding system reduces boot-to-board attachment time from 45 seconds to under 10 seconds, lowering barriers for casual participants, while competing systems from FASE and Nidecker’s Supermatic further validate this convenience trend, with step-in adoption rising to 18% of new snowboard sales in 2025, up from 9% in 2023. The FIS SnowKidz program enrolled 247,569 participants in 2022–23, an 84% increase from 134,578 in 2021–22, showing that early exposure to freestyle disciplines drives future adult equipment purchases. Brands targeting this cohort prioritize shorter, twin-tip boards and softer flex patterns for jib tricks, a design shift that increases SKU proliferation and inventory complexity for retailers.

Technological Advancements in Equipment Production

Material innovation in the European winter sports equipment market is advancing through carbon-fiber optimization, bio-based composites, and the integration of recycled content. Völkl has implemented carbon-fiber placement technology that reduces ski weight by 12% while preserving torsional rigidity. HEAD’s RENEW ski incorporates recycled materials, cutting 22% of virgin-plastic content, and Fairmat partnered with DPS Skis to supply recycled aerospace carbon fiber, reducing material costs by 15–18% and carbon footprint by 40%. Sweden’s RISE research institute developed a bio-based ski prototype using lignin-derived resins, aiming to commercialize it by 2027 under the EU’s Horizon Europe program. These advances respond to EU PFAS restrictions on fluorinated waxes and DWR coatings, enabling reformulation without compromising glide or water repellency. The strategic implication is that research and development cycles have shortened to 18–24 months, favoring vertically integrated manufacturers like Fischer and Rossignol, while smaller brands reliant on third-party suppliers face 6–9 month delays, limiting their ability to meet rising demand for compliant and sustainable products.

Increasing Female and Youth Participation Initiatives

The FIS Women Lead Sports program partners with national ski associations to train female coaches and officials, while the IOC’s WISH (Women in Sport High-Performance) initiative funds gender-balanced training camps across Europe. Switzerland’s ski camps reached a 20-year high of 128,498 participants, with female enrollment rising from 38% in 2020 to 44% in 2024, driven by targeted marketing and family-package pricing, according to Swiss Ski. The World Snowboard Federation’s Women's Project conducted development camps in Austria and France, resulting in a 29% increase in female competitive registrations between 2023 and 2025. Youth programs are also expanding: FIS SnowKidz grew to 247,569 participants in the 2022–23 season, while the FIS Plus Programme donated 70 roller skis to 15 national associations to broaden off-season training opportunities. A pan-European youth sport study reveals that skiing achieves gender-balanced engagement (49% female vs. 51% male), compared to football (68% male), highlighting untapped market potential for brands to tailor their sizing, graphics, and marketing to female preferences. Female participants also spend 18% more on protective gear and apparel than male counterparts, according to Decathlon and Intersport, shifting revenue toward higher-margin accessory categories.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-driven snowfall volatility and greater reliance on artificial snow | -1.1% | Alpine arc (France, Switzerland, Austria, Italy); Pyrenees (Spain); lower-altitude German resorts | Long term (≥ 4 years) |

| High upfront cost of premium gear vs. rental affordability | -0.8% | UK, Spain, emerging markets | Medium term (2-4 years) |

| Seasonal and weather dependency | -0.5% | Germany, UK, and Spain | Short term (≤ 2 years) |

| Tightening EU PFAS and safety regulations increasing compliance costs | -0.6% | EU-27, with strictest enforcement in Germany, France, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Snowfall Volatility and Greater Reliance on Artificial Snow

The Alps have warmed at twice the global average since 1980, with winter temperatures rising 1.8°C compared to the global mean of 0.9°C, according to the European Environment Agency, shortening naturally snow-reliable seasons by 2–3 weeks at resorts below 1,800 meters[3]Source: European Environment Agency, “Alps Warming Trends,” eea.europa.eu. To compensate, operators in Austria, Switzerland, and France deploy artificial snowmaking on 70–80% of pistes, consuming 1.2–1.5 cubic meters of water per cubic meter of snow and adding EUR 15,000–25,000 (USD 16,300–27,200) per hectare per season in energy costs, which are typically passed on to consumers through 8–12% annual lift-ticket price increases. This increases demand for rental equipment over ownership and introduces revenue volatility: warm winters can reduce equipment sales by 15–20%, as occurred in the 2022–23 Pyrenees season. Brands with diversified portfolios, like Amer Sports, which also sells running and cycling gear, are better insulated from climate-related shocks, creating consolidation pressure on smaller, pure-play winter sports manufacturers that lack cross-category revenue streams.

High Upfront Cost of Premium Gear vs. Rental Affordability

Premium alpine ski packages, including skis, bindings, boots, and poles, retail for EUR 1,200-2,000 (USD 1,304–2,173), while daily rentals range from EUR 25–45 (USD 27–49), making ownership economically viable only for skiers who hit the slopes 15+ days per season. Rental penetration reached 62% of total skier-days in 2025, up from 54% in 2020, driven by subscription-based models such as Decathlon’s “Rent and Return” program and Rossignol’s direct-to-consumer rental service. The UK and Spain show the highest rental ratios at 72% and 68%, respectively, as shorter domestic seasons and travel logistics favor renting at destination resorts over transporting owned equipment. The growth of rental services cannibalizes entry-level equipment sales, particularly in the EUR 300-600 (USD 326-652) price band, which historically accounted for 40% of unit volume. Brands are responding by offering premium rental fleets with the latest model seasons, capturing recurring revenue and maintaining brand visibility. However, this approach requires a significant upfront investment of EUR 800–1,200 (USD 870–1,304) per ski set, with replacement cycles of approximately three years. A secondary insight is that rental customers exhibit 25% lower brand loyalty than owners, according to Sport 2000 surveys, as they rotate equipment across multiple brands each season, reducing the lifetime value of customer acquisition[4]Source: Sport 2000, “Annual Sales Report 2024,” sport2000.de.

Segment Analysis

By Sports Type: Freestyle Momentum Challenges Alpine Dominance

Skiing remains the dominant segment in the European winter sports equipment market, capturing 63.55% of revenue in 2025, supported by its long-standing heritage and extensive infrastructure across Alpine and Nordic regions. However, growth is moderating due to aging demographics and climate volatility, which constrain participation in resort-based downhill skiing. Snowboarding is expanding faster, with a projected 7.83% CAGR through 2031, driven by Gen Z’s preference for park-and-pipe progression and innovations such as step-in bindings that reduce barriers to entry. Ice hockey maintains a stable niche in Nordic countries and Germany, underpinned by well-developed rink infrastructure, while figure skating remains concentrated in urban centers with specialized facilities. Other disciplines, including cross-country skiing, ski touring, and biathlon, are gaining popularity among climate-conscious consumers seeking low-impact, backcountry alternatives, exemplified by Norway, where 25.6% of the population (1.161 million people) participated in cross-country skiing in 2024[5]Source: Statistics Norway, “Cross-Country Skiing Participation 2024,” ssb.no. Youth development programs such as the FIS Alps Tour also channel recreational skiers into competitive freestyle disciplines, creating opportunities for manufacturers to target progression-oriented equipment.

Cross-country skiing and ski touring are particularly resilient, relying on minimal infrastructure and reducing exposure to resort-ticket inflation and artificial snow dependency. Brands like Swix reported double-digit growth in touring-binding sales during 2024–25 as consumers pursue self-guided experiences off crowded pistes. Ice hockey equipment sales correlate with youth league enrollment, which grew 12% in Germany between 2023 and 2025, while figure skating remains a high-margin niche with blade sets priced at EUR 400–800 and custom boots adding EUR 300–500, generating 40–50% gross margins despite limited volume. Consumer behavior is increasingly diversified, with sports-type participation rising from 1.3 disciplines per participant in 2020 to 1.7 in 2025, according to Sport 2000 surveys. This trend favors brands with broad portfolios, such as Amer Sports, which owns Atomic (alpine), Salomon (alpine and Nordic), and Arc’teryx (backcountry), that can capture cross-shopping behavior, while specialists risk obsolescence unless they adapt to evolving preferences. Cross-category bundles, like pairing alpine skis with touring bindings, have become an effective strategy for maximizing wallet share and enhancing participant engagement.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Equipment Category: Apparel Gains as Technical Textiles Advance

Skis and snowboards dominate the equipment category, accounting for 48.24% of revenue in 2025, driven by replacement cycles of 4-5 years for recreational users and 1–2 years for competitive athletes. However, their growth trails that of apparel and accessories, which are projected to expand at a 7.27% CAGR through 2031, fueled by innovations such as recycled carbon fiber, bio-based insulation, and PFAS-compliant DWR coatings. Boots and bindings remain a critical touchpoint, as improper fit contributes to 40% of early-season injuries, according to the International Society for Skiing Safety. Brands like HEAD and Tecnica have invested in 3D foot-scanning technology to customize boot shells for individual anatomy, thereby improving comfort and energy transfer. Meanwhile, Burton’s step-in binding systems have reduced boot-to-board attachment time from 45 seconds to under 10 seconds, eliminating a friction barrier that previously deterred casual participants. Protective gear and helmets have surged from 18% market penetration in 2015 to 67% in 2025, driven by FIS helmet mandates for youth competitions and insurance incentives in Austria and Switzerland, with POC Sweden AB and Uvex Group leading adoption of MIPS technology, which reduces rotational forces by 30–40% compared to conventional foam liners.

Apparel and accessories benefit from fashion-driven replacement cycles averaging 2.8 years, exceeding functional obsolescence as consumers refresh jackets, pants, and logo placements to align with seasonal trends. Brands such as Ortovox Sportartikel GmbH and Haglöfs emphasize merino-wool base layers and recycled-polyester shells, appealing to sustainability-conscious buyers willing to prioritize carbon footprint over price. Apparel also offers higher gross margins, typically 55-60% versus 35-40% for hardgoods, incentivizing expansion in textile offerings, though this requires careful management of SKUs across sizes, colors, and fits. Other high-margin accessories, including goggles, gloves, and bags, are commonly bundled with hardgoods to increase average transaction value. For example, Hestra AB, a Swedish glove specialist, reported 18% revenue growth in 2024-25 by introducing touchscreen-compatible fingertips and battery-heated liners. A secondary insight is that rental fleets prioritize hardgoods over apparel due to hygiene concerns, giving apparel brands a structural advantage with lower channel cannibalization and sustained premium pricing.

By End User: Kids Segment Outpaces Adults on Program Momentum

Adults dominate the end-user segment, accounting for 71.42% of revenue in 2025, driven by higher disposable incomes and multi-item purchases that typically include skis, boots, apparel, and accessories. In contrast, the kids segment is growing faster, with a projected 7.57% CAGR through 2031, fueled by rising youth participation in programs such as FIS SnowKidz, which increased from 134,578 participants in 2021–22 to 247,569 in 2022–23, and Switzerland’s ski camps reaching a 20-year high of 128,498 participants in 2024. Parents prioritize safety and fit over brand prestige, creating demand for adjustable-length skis and expandable boot shells that accommodate 2–3 years of growth. Brands such as Elan d.o.o. and K2 Sports have introduced rear-slider adjustable skis that reduce replacement frequency from annual to biennial, lowering the total cost of ownership by 30-35%. Although kids’ equipment generates lower per-unit revenue, averaging EUR 250-400 (USD 272-435) per ski package versus EUR 800-1,500 (USD 870-1,630) for adults, it benefits from higher unit velocity due to shorter replacement cycles of 1.5-2 years.

Initiatives promoting female participation, including FIS Women Lead Sports and the World Snowboard Federation’s Women Project, are expanding the adult market by normalizing competitive pathways and improving access to coaching. Retail data from Decathlon shows that female participants spend 18% more on protective gear and apparel than male participants, shifting revenue mix toward higher-margin accessory categories. Multi-generational family purchases, where parents acquire equipment for themselves and 2–3 children simultaneously, account for 34% of offline retail transactions during peak season, according to Sport 2000 point-of-sale data. This trend creates opportunities for bundled pricing strategies and loyalty programs, helping brands lock in repeat purchases as children transition into adult sizes.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Gains Share Despite Fitting Challenges

Offline retail stores continue to dominate the distribution landscape, accounting for 71.69% of revenue in 2025, largely due to their ability to provide in-store fitting expertise and immediate product availability, advantages that online channels struggle to replicate. Nevertheless, e-commerce is growing rapidly, with a projected 8.49% CAGR through 2031, as brands invest in virtual try-on tools, free-return policies, and direct-to-consumer rental subscriptions. Major players exemplify this trend: Decathlon Germany achieved a gross merchandise value of EUR 1.17 billion (USD 1.27 billion) in 2024, while Bergfreunde generated EUR 313 million (USD 340 million) in revenue, experiencing 17% growth in fiscal 2024–25. Omnichannel strategies, where consumers research online and purchase in-store or vice versa, have proven more effective in capturing wallet share than single-channel approaches. Sport 2000 GmbH leveraged its 2,000-store network to provide same-day ski tuning and binding adjustments, services that online-only retailers cannot match. Similarly, Bergzeit reported a 17% revenue growth by integrating in-store pickup for online orders, which reduced last-mile delivery costs while preserving the tactile evaluation that consumers demand for boots and helmets.

Online channels excel in offering long-tail SKU availability, providing 3-5 times more size and color options than physical stores, and improving seasonal clearance efficiency through dynamic pricing algorithms. Brands such as Rossignol and Burton launched direct-to-consumer rental subscriptions in 2024, priced at EUR 299-499 (USD 325–542) per season for unlimited equipment swaps, targeting urban consumers who ski 5–10 days annually and prefer access over ownership. While this growth pressures specialty retailers’ margins, allowing brands to capture the 40-50% delta between factory gate and retail shelf, it also risks straining relationships with retail partners that deliver critical boot-fitting and after-sales services. A secondary consideration is the higher return rate for online boot purchases, averaging 28-35% versus 8-12% for skis and apparel, due to the need for precise in-person fit. Online players mitigate this structural disadvantage through scale, automation, and logistics optimization, according to data from European e-commerce platforms and the European E-commerce Report.

Geography Analysis

Germany accounts for 22.83% of Europe’s winter sports equipment revenue in 2025, supported by the scale and reach of major sporting goods players such as Sport 2000 GmbH and Decathlon Germany, as well as fast-growing specialists Bergfreunde and Bergzeit. Strong omnichannel behavior, where consumers research online but finalize purchases in-store for services such as boot fitting, continues to lift sales. Meanwhile, Germany’s large population and proximity to Alpine destinations in Austria and Switzerland stimulate cross-border equipment purchases. Domestic resorts in Bavaria and the Black Forest further sustain demand, particularly through weekend rental bookings. Beyond alpine sports, Germany’s well-developed ice hockey ecosystem, backed by rising municipal investment in rinks, broadens the demand base and reduces reliance on snowfall conditions.

France benefits from sustained public and private investment in mountain infrastructure, notably through the Avenir Montagnes program, which has modernized lifts and expanded snowmaking across key regions. These upgrades, complemented by capital spending from Compagnie des Alpes, have lengthened ski seasons and increased equipment utilization. Italy plays a dual role as both a consumption and export hub, accounting for a significant share of the EU’s extra-regional winter sports exports, while the upcoming Milano Cortina 2026 Winter Olympics is expected to drive tourism, marketing activations, and equipment sales. Together, Germany, France, and Italy form the core revenue base of the European market, collectively contributing more than half of regional sales.

Southern and Northern Europe present contrasting growth dynamics. Spain is the fastest-growing market with a CAGR of 8.14%, driven by resort upgrades in the Pyrenees and wider adoption of artificial snow, though high rental penetration limits equipment ownership growth. In the Nordics, Norway and Finland benefit from deeply rooted participation in cross-country skiing and winter tourism, offering resilience to climate variability and steady demand for equipment and apparel. Switzerland shows rising engagement through ski camps and female participation, while Sweden’s stable but intense participation highlights a mature enthusiast base. The United Kingdom’s high reliance on rentals reflects shorter seasons and travel-driven consumption patterns, favoring rental-fleet suppliers over ownership sales. Austria remains Europe’s manufacturing backbone, producing nearly half of the EU’s skis and snowboards and benefiting from glacier resorts that support year-round activity. In contrast, Eastern European markets within the rest of Europe are emerging more gradually, driven by income growth and EU infrastructure funding but constrained by price sensitivity, requiring brands to balance volume expansion with margin protection.

Competitive Landscape

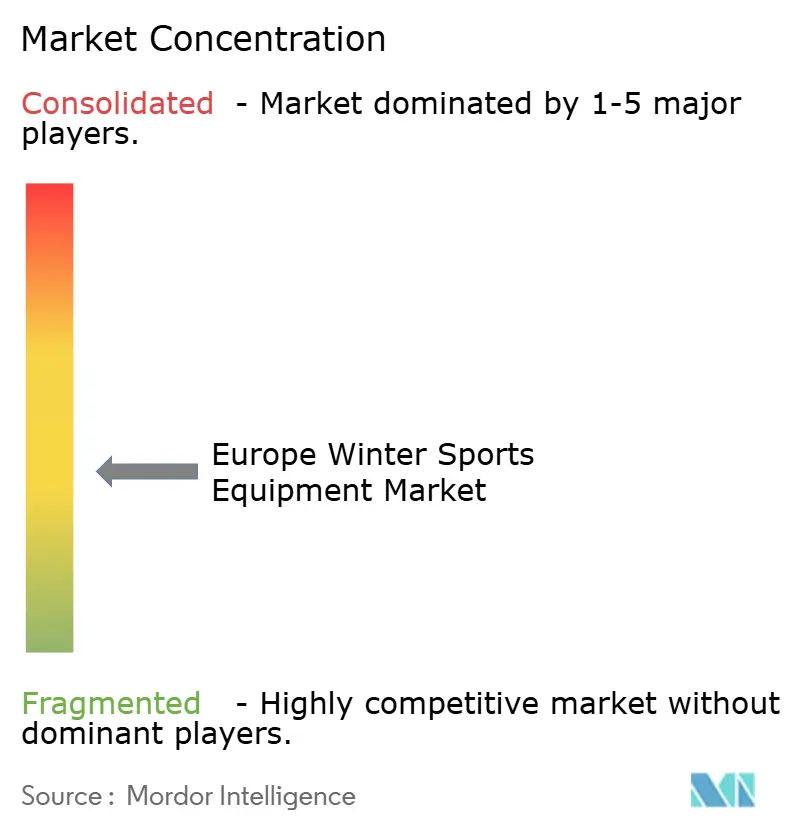

The European winter sports equipment market is moderately fragmented, with major players such as Amer Sports Oyj, Groupe Rossignol, HEAD Sport GmbH, Fischer Sports GmbH, and Tecnica Group SpA collectively accounting for a significant market share, leaving room for regional specialists and niche challengers. Amer Sports’ February 2024 New York Stock Exchange listing at a USD 8.7 billion valuation has strengthened its ability to fund acquisitions and invest in research and development, particularly in smart-boot sensors and AI-driven fit technologies. Rossignol and HEAD are pursuing vertical integration by internalizing resin formulation and carbon-fiber layup to accelerate compliance with EU PFAS regulations and reduce reliance on suppliers with long lead times, while Fischer leverages its Austrian manufacturing base to achieve scale efficiencies across branded and private-label production. Tecnica Group further mitigates risk through portfolio diversification across Blizzard, Nordica, and Rollerblade, spanning alpine, Nordic, and inline skating categories.

White-space growth opportunities are emerging in backcountry touring and adaptive equipment. Brands such as Black Crows and Dynafit are gaining traction among consumers seeking self-guided, off-piste experiences, while para-snowboarding equipment tailored for athletes with mobility impairments commands 35-40% price premiums due to low-volume, high-touch manufacturing. At the same time, smaller players including POC Sweden AB and Ortovox Sportartikel GmbH are strengthening their positions by targeting sustainability-focused consumers with transparent supply chains and carbon-neutral certifications, particularly in Germany, France, and the Nordic countries, where environmental credentials support 12–15% price premiums.

Innovation across the market is concentrated in three core areas: advanced materials such as recycled carbon fiber and bio-based resins; fit customization enabled by 3D foot scanning and heat-moldable liners; and digital engagement tools including virtual try-on and subscription-based rental models. Incumbents defend share through incremental innovation, as seen in HEAD’s RENEW ski and Völkl’s carbon-fiber placement technology, while disruptors such as Fairmat, through its partnership with DPS Skis, leverage recycled aerospace materials to differentiate. These dynamics are increasing consolidation pressure on sub-EUR 50 million revenue players, as EU PFAS compliance and carbon levies absorb 4-8% of sales, while vertically integrated rental strategies adopted by companies like Decathlon and Rossignol enhance recurring revenue but require significant upfront capital and working-capital intensity.

Europe Winter Sports Equipment Industry Leaders

Amer Sports Oyj

Groupe Rossignol

HEAD Sport GmbH

Fischer Sports GmbH

Tecnica Group SpA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Atomic announced a strategic partnership with Nordica to co-develop a performance ski boot and binding system targeting premium alpine and all-mountain segments.

- May 2025: Amer Sports Oyj has opened a binding production facility in Oradea, Romania, thereby strengthening European manufacturing and reducing its reliance on outsourced production.

- March 2025: Rossignol Group rolled out a line of snowboards with 85% recycled core materials as part of its sustainability push

- January 2025: HEAD Sport GmbH introduced the RENEW ski line made with recyclable and reusable core materials, reducing the carbon footprint.

Europe Winter Sports Equipment Market Report Scope

Winter sports or winter activities are competitive or non-competitive recreational activities played on snow. Most are variations of skiing, ice skating, and sledding, all of which are essential winter sports. The European Winter Sports Equipment Market is segmented by sport, equipment category, end-user, distribution channel, and geography. By sports type, the scope covers skiing, snowboarding, ice hockey, figure skating, and other winter sports, capturing both alpine- and rink-based equipment demand. By equipment category, the analysis includes skis and snowboards, boots and bindings, protective gear and helmets, apparel and accessories, and other related equipment, reflecting the full value chain from core performance gear to safety and lifestyle products. The report further segments the market by end user into adults and kids, highlighting differences in purchasing behavior, safety requirements, and product design. By distribution channel, it evaluates sales through both offline and online retail stores, assessing how digital commerce and omnichannel strategies are reshaping market access. Geographically, the study covers key European markets including Germany, the United Kingdom, Italy, France, Spain, Norway, Finland, Switzerland, and Sweden, along with the rest of Europe. The report offers the market size and forecast of the winter sports equipment market in value (USD million) for all the above segments.

By Sports Type

| Skiing |

| Snowboarding |

| Ice Hockey |

| Figure Skating |

| Other Sports Type |

By Equipment Category

| Skis and Snowboards |

| Boots and Bindings |

| Protective Gear and Helmets |

| Apparel and Accessories |

| Other Equipment Category |

By End User

| Adult |

| Kids |

By Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Norway |

| Finland |

| Switzerland |

| Sweden |

| Rest of Europe |

| By Sports Type | Skiing |

| Snowboarding | |

| Ice Hockey | |

| Figure Skating | |

| Other Sports Type | |

| By Equipment Category | Skis and Snowboards |

| Boots and Bindings | |

| Protective Gear and Helmets | |

| Apparel and Accessories | |

| Other Equipment Category | |

| By End User | Adult |

| Kids | |

| By Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Norway | |

| Finland | |

| Switzerland | |

| Sweden | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Europe winter sports equipment market by 2031?

The market is forecast to reach USD 8.83 billion by 2031.

Which sports type is growing fastest in Europe?

Snowboarding is expected to grow at a 7.83% CAGR through 2031, outpacing other disciplines.

How significant is online retail for European winter sports gear?

While offline stores still command 71.69% of revenue, online channels are projected to rise at an 8.49% CAGR due to virtual fitting and rental subscriptions.

Which country currently leads regional revenue?

Germany holds the top spot, contributing 22.83% of 2025 sales.

What is the outlook for kids’ equipment demand?

Kids gear is set to expand at a 7.57% CAGR as enrollment in programs like SnowKidz and Swiss ski camps reaches record highs.