Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

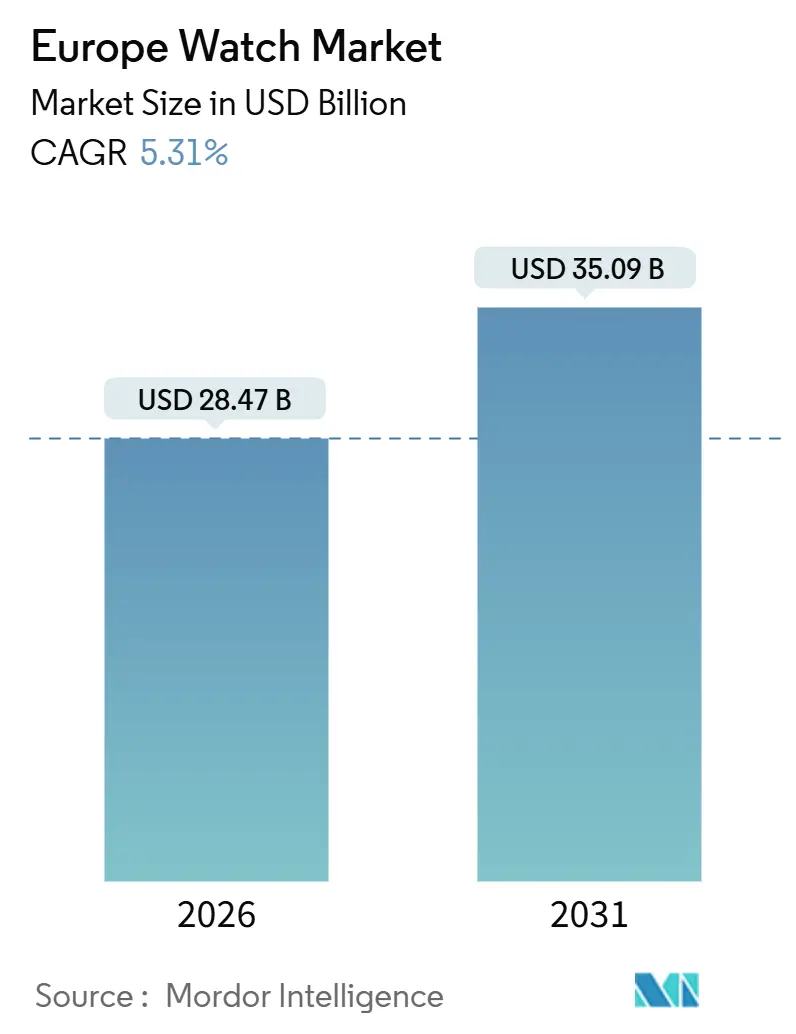

| Market Size (2026) | USD 28.47 Billion |

| Market Size (2031) | USD 35.09 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Watch Market Analysis by Mordor Intelligence

The Europe watch market size stands at USD 28.47 billion in 2026 and is projected to reach USD 35.09 billion by 2031, expanding at a 6.86% CAGR over 2026-2031. Mechanical craftsmanship is increasingly merging with biometric integration, driven by strict EU Extended Producer Responsibility rules that nudge brands towards modular and repair-friendly designs. Demand is bolstered by adventure-sports wearables that seamlessly combine heart-rate sensing and GPS with shock resistance. Additionally, affluent buyers are now viewing watches as alternative investments, especially in light of uncertainties in real estate. While competitive intensity is moderate, tightening Swiss export quotas are limiting component supply, benefiting vertically integrated houses. Simultaneously, crowdfunding is energizing micro-brand launches throughout Northern Europe. Key drivers of this momentum include Germany's premium market appetite, a rebound in Spain's tourism, and a swift shift towards direct-to-consumer e-commerce, which is broadening the certified pre-owned trade. However, challenges persist: the proliferation of counterfeits, dwindling foot traffic in urban boutiques, tariff fluctuations on Swiss imports, and a notable rejection of exotic-skin straps by Gen Z. Despite these hurdles, the European watch market is buoyed by a robust Swiss employment figure surpassing 65,000 and an uptick in higher-education roles, underscoring a commitment to technical investment even amidst geopolitical tensions[1]Source: Federation of the Swiss Watch Industry, "Swiss Watch Industry Employers’ Association: census", fhs.swiss.

Key Report Takeaways

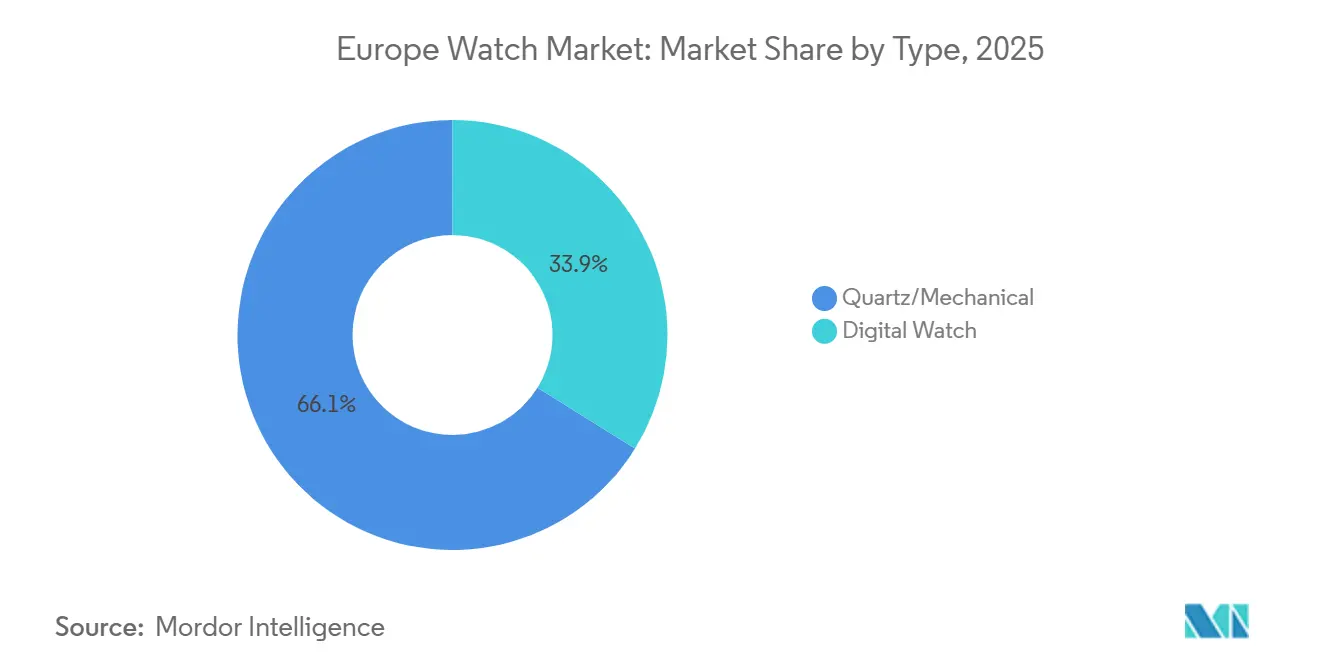

- By type, quartz/mechanical watches commanded 66.14% Europe watch market share in 2025 and the digital segment is forecast to expand at a 5.18% CAGR to 2031.

- By category, the mass-market segment held 58.57% of the Europe watch market size in 2025, while the premium tier is set to grow at a 7.34% CAGR through 2031.

- By geography, Germany led with 27.15% revenue share in 2025; Spain is projected to post the fastest 7.34% CAGR between 2026-2031.

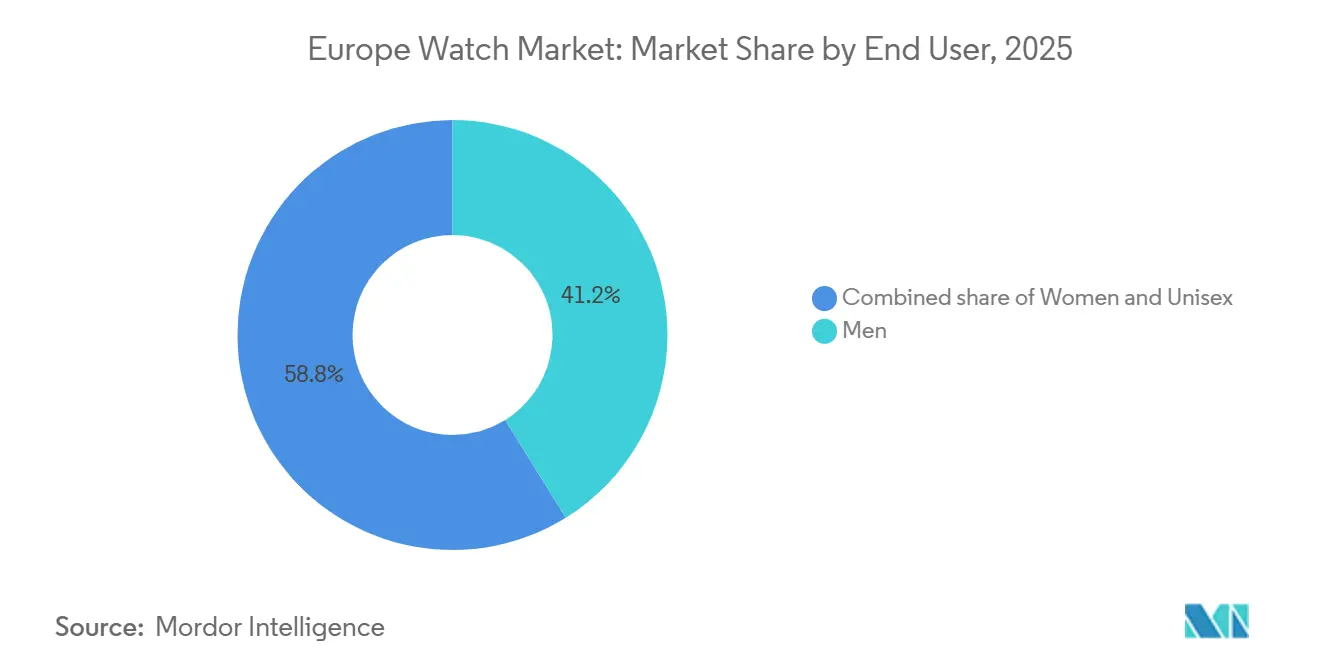

- By end user, men represented 41.17% of 2025 sales, but unisex designs are advancing at a 6.14% CAGR to 2031.

- By distribution, specialty stores retained 45.52% share in 2025, whereas online channels are projected to rise at a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Watch Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Blending adventure sports with smarter wearables | +1.2% | Global, with early adoption in Nordic countries and Alpine regions | Medium term (2-4 years) |

| Preference for luxury timepiece | +1.5% | Germany, United Kingdom, France, Italy; spillover to Benelux | Long term (≥ 4 years) |

| Rising disposable income and fashion consciousness | +1.0% | Spain, Poland, Sweden; urban centers across Western Europe | Medium term (2-4 years) |

| Resurgence of mechanical heritage brands via crowdfunding | +0.6% | United Kingdom, Germany, Netherlands; niche communities in France | Short term (≤ 2 years) |

| EU EPR rules triggering modular, repairable designs | +0.8% | EU-27, with strictest enforcement in Germany, France, Netherlands | Long term (≥ 4 years) |

| Biometric-enabled luxury hybrid timepieces | +0.9% | Germany, United Kingdom, Nordics; affluent segments in Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Blending adventure sports with smarter wearables

Rugged smartwatches, equipped with altimeters, GPS, and optical heart-rate monitors, now blur the lines between fitness trackers and traditional sports watches, boasting a commendable 200-meter water resistance. Casio's G-SHOCK GSW-H1000 exemplifies this evolution, featuring Wear OS, a dual-layer display, and premium titanium casebacks, all priced at USD 779. This offering has found favor among outdoor enthusiasts in Germany and Scandinavia, who value both durability and data for their demanding activities, such as hiking, mountaineering, and water sports. While Garmin and Suunto have long held sway in this niche, even storied Swiss brands are introducing hybrid models, underscoring a growing appetite for devices that meld narrative with performance metrics. These hybrid models often combine traditional craftsmanship with advanced technology, appealing to a broader audience. Notably, younger consumers are increasingly shunning the age-old dilemma of choosing between prestige and practicality, leading to a surge in adoption as they seek products that align with their active lifestyles and modern preferences.

Preference for luxury timepiece

In Germany, the UK, France, and Italy, affluent collectors view mechanical watches as a hedge against inflation. This perspective has driven demand, resulting in multi-year waitlists for highly sought-after models from Rolex and Patek Philippe. These timepieces are not only seen as luxury items but also as investment assets that retain or even appreciate in value over time. Even as the broader luxury sales landscape shows signs of softening, the demand for these watches remains robust. Highlighting a shift in demographics, Sotheby’s has noted a 70% increase in female bidders since 2015, reflecting growing interest among women in the watch market. Furthermore, premiums in the secondary market underscore the effectiveness of managed scarcity in preserving value and exclusivity. As a result, the European watch market continues to wield significant pricing power, even in the face of challenges posed by rising interest rates.

Rising disposable income and fashion consciousness

In Spain, Poland, and Sweden, urbanization and rising wages are driving up demand for quartz and entry-level mechanical watches, priced between EUR 200 and EUR 1,500. This trend reflects a growing middle class with increased disposable income, seeking stylish yet affordable timepieces. Brands like Daniel Wellington see their sales surge, thanks to social media discovery, which plays a pivotal role in influencing consumer preferences and expanding brand visibility. Meanwhile, Casio's Bright Metallics line, priced at EUR 142, caters to Gen Z's quest for affordable style, offering vibrant designs that resonate with younger consumers and bolstering volume growth. The luxury market is also evolving, with fashion-driven consumption leading brands like Tiffany & Co. and Jaeger-LeCoultre to introduce modular designs that serve a dual purpose as jewelry, appealing to consumers who value versatility and innovation in high-end products.

Resurgence of mechanical heritage brands via crowdfunding

Micro-brands in the UK, Germany, and Netherlands are leveraging Kickstarter and Indiegogo campaigns to swiftly fund limited runs, build collector communities, and bypass traditional wholesale channels. These platforms provide an accessible avenue for small-scale brands to secure funding without relying on traditional financial institutions or large-scale investors. Backers, viewing their early pledges as quasi-investments, frequently enjoy premium returns once deliveries start, echoing trends seen in sneaker culture. This model underscores the transformative impact of digital finance tools on traditional distribution norms, enabling brands to directly connect with niche audiences. At the same time, it is infusing the European watch market with innovative design insights, fostering a dynamic environment for creativity and growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased prevalence of counterfeit products | -0.7% | Global, with highest incidence in Southern and Eastern Europe | Short term (≤ 2 years) |

| Declining footfall in brick-and-mortar watch stores | -0.9% | UK, Germany, France, Italy; urban retail districts | Medium term (2-4 years) |

| Swiss movement export quotas creating supply bottlenecks | -0.6% | Switzerland-dependent brands across EU; spillover to UK post-Brexit | Long term (≥ 4 years) |

| Gen-Z aversion to exotic-material straps | -0.4% | Western Europe, Nordics; urban millennial and Gen Z segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased prevalence of counterfeit products

Every year, EU border agencies confiscate millions of counterfeit watches. However, social media platforms often provide a loophole for sellers to evade customs checks, enabling the distribution of fake products directly to consumers. This trend disproportionately affects mid-tier brands, which lack the resources of luxury brands to combat counterfeiting effectively.The Federation of the Swiss Watch Industry operates anti-counterfeiting initiatives including public guidance pages and a reporting mechanism, but the scale of the problem persists as counterfeiters adopt sophisticated manufacturing techniques laser-etched serial numbers, near-identical packaging, and functional movements that make detection difficult for casual buyers[2]Source: Federation of the Swiss Watch Industry, "Latest anti-counterfeiting initiatives", fhs.swiss. The challenge intensifies with the use of laser-etched serials and replicated movements, which closely mimic genuine products, making detection increasingly difficult for authorities. In response, many firms are turning to blockchain passports as a solution to authenticate their products, ensure traceability throughout the supply chain, and build consumer trust. While this technology offers a robust method to combat counterfeiting, it also introduces additional costs, which can be a significant burden for smaller brands.

Declining footfall in brick-and-mortar watch stores

As shoppers increasingly turn to online platforms, urban boutiques are witnessing a decline in foot traffic. This shift in consumer behavior is driven by the convenience, variety, and competitive pricing offered by e-commerce platforms. In H1 FY26, Watches of Switzerland Group reported a modest 2% revenue growth in the U.K., a stark contrast to the 20% surge seen in the U.S., highlighting the mounting pressures in the U.K. market. The disparity underscores the challenges faced by traditional retailers in adapting to changing consumer preferences and regional market dynamics. In response, retailers are shifting their focus towards mono-brand flagship stores that offer immersive experiences, such as personalized services, exclusive product showcases, and brand storytelling. At the same time, they are streamlining their multi-brand footprints by consolidating operations, optimizing store locations, and enhancing the overall customer experience to remain competitive in a rapidly evolving retail landscape.

Segment Analysis

By Type: Mechanical Heritage Anchors Value, Digital Gains Utility Share

In 2025, quartz and mechanical watches together held a dominant 66.14% share of Europe's watch market. This leadership position is anchored in a deep-rooted consumer trust in the precision, craftsmanship, and heritage these timepieces represent. Prestige mechanical watches, often limited editions, command premium prices bolstered by their brand equity, even as their unit sales stabilize. These high-end watches are often associated with luxury and exclusivity, appealing to collectors and connoisseurs who value intricate designs and traditional watchmaking techniques. On the other hand, brands like Casio, with offerings such as the EUR 307 EDIFICE automatic, are making mechanical watches more accessible. These options cater to enthusiasts who desire authenticity without the hefty Swiss price tag, bridging the gap between luxury and affordability. Collectively, these dynamics not only uphold the value of these watches but also cement their pivotal role in Europe's horological landscape.

Digital watches are on a rapid ascent, with projections indicating a 5.18% CAGR growth rate through 2031. This surge is largely attributed to the seamless blend of technology with modern lifestyle demands. There's a notable uptick in the demand for fitness-centric smartwatches that marry functionality with aesthetics. These devices are increasingly equipped with advanced features such as heart rate monitoring, GPS tracking, and sleep analysis, catering to health-conscious consumers. Industry leaders like Apple and Garmin are setting the gold standard for performance and connectivity, offering products that integrate effortlessly with smartphones and other digital ecosystems. Meanwhile, Casio's G-SHOCK hybrid stands out, showcasing a robust design paired with advanced digital features, appealing to consumers who prioritize durability alongside innovation. The growth trajectory is especially pronounced among urban, active consumers who value wellness monitoring and a smooth connection to their digital lives. This trend firmly establishes digital watches as the most agile and evolving segment in Europe's watch market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Mass Scale Meets Premium Acceleration

In 2025, mass-market watches secured a commanding 58.57% share of the European watch market, solidifying their status as the dominant segment. Brands such as Casio, Swatch, Fossil, and Timex lead the charge, thanks to their widespread availability, trendy designs, and competitive pricing. These strategies resonate with a diverse consumer base in both urban and suburban locales. The brands' collaborations, like Swatch Group's MoonSwatch priced at USD 385, showcase their ability to blend everyday utility with fashion-forward appeal, leveraging hype tactics often associated with luxury tiers. While direct-to-consumer disruptors have squeezed margins, mass-market brands counter with innovative limited drops and dynamic marketing, ensuring brand loyalty. This segment's resilience underscores a consistent demand for reliable, affordable timepieces, even amidst economic uncertainties. In essence, mass-market watches not only anchor the industry's volume base but also adeptly navigate the shifting retail landscape.

Meanwhile, the premium watch segment is on a rapid ascent, projected to grow at a 7.34% CAGR through 2031. This surge is largely driven by affluent consumers increasingly viewing timepieces as portable stores of value. Strategies emphasizing scarcity and craftsmanship have cultivated an inelastic demand. Limited-edition releases, for instance, command premium prices even in the secondary market, which boasts a global valuation of USD 27 billion and is expanding at double-digit rates. Notably, there's a demographic shift: female collectors are making their mark, increasingly participating in high-profile auctions, such as those at Sotheby's, expanding the segment's appeal beyond its traditional base. Premium watch houses are adeptly navigating challenges, striking a balance between maintaining exclusivity and addressing Gen Z's priorities, such as sustainability and ethical sourcing. The secondary trading market bolsters liquidity, allowing for resale value appreciation, further enhancing the allure of watches as investments. Given these dynamics, premium watches are poised to capture significant value in Europe's evolving luxury landscape.

By End User: Men Lead, Unisex Designs Capture Gen Z

In 2025, men's watches commanded a 41.17% share of the European watch market, reinforcing their status as the leading segment amidst a continued preference for classic masculinity. Established brands, with their traditional case sizes and robust designs, cater to professionals and collectors who prioritize heritage and precision. Urban markets anchor this demand, where watches serve as status symbols in both business and leisure. While competition from inclusive options rises, men's models enjoy the advantages of loyal repeat purchases and gifting traditions during holidays and milestones. Brands are subtly integrating technology into their offerings, ensuring they remain relevant without straying from core aesthetics. This segment's continued dominance highlights a steady reliability, even as the market shifts towards broader personalization.

Unisex models are emerging as the fastest-growing segment, boasting a 6.14% CAGR through 2031. Their rise is fueled by gender-neutral designs that challenge traditional marketing norms. Case diameters, ranging from the Rolex Oyster Perpetual to the Cartier Tank, resonate with millennials and Gen Z, who prioritize fluidity in style and self-expression. Women's enthusiasm for mechanical watches is on the rise, especially with increased participation in auctions, merging craftsmanship with modern empowerment. Brands adopting inclusive sizing strategies are tapping into a broader demographic, from non-binary consumers to couples in search of matching pairs. Marketing strategies are shifting to spotlight shared values like sustainability and versatility, cultivating loyalty across diverse lifestyles. This growth trajectory underscores the significance of unisex watches in shaping Europe's evolving consumer landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Specialty Holds Ground, Online Surges

In 2025, specialty boutiques secured 45.52% of the revenue in Europe's watch market, solidifying their status as the dominant channel. These boutiques leverage personalized expertise and exclusive access to high-end inventories. They thrive on tactile experiences, host in-store events, and curate trusted selections, fostering long-term relationships, especially for premium and luxury purchases. Affluent buyers, drawn to curated selections from brands like Rolex and Patek Philippe, seek authenticity and immediate gratification. Even with the digital shift, boutiques maintain revenue dominance by emphasizing scarcity narratives and offering after-sales services to bolster loyalty. Multi-brand settings encourage discovery, appealing to collectors who prioritize heritage storytelling over quick transactions. This channel's stronghold underscores a lasting preference for human touch in a premium-driven retail landscape.

Online platforms are rapidly emerging as the fastest-growing segment, boasting a 7.61% CAGR projected through 2031. They are revolutionizing distribution with enhanced accessibility and technological innovations. A case in point is Watches of Switzerland Group, which has expanded its Rolex Certified Pre-Owned line to digital channels, highlighting the ultra-luxury sector's growing embrace of e-commerce. Innovations like virtual try-on tools, blockchain verification, and direct-to-consumer models are bolstering trust and convenience, particularly resonating with Gen Z's digital-first approach. These platforms are not just about selling; they offer global inventories, tailored recommendations, and flexible financing options, all amidst the surge of mobile commerce. This online growth challenges the exclusivity of boutiques, leveraging data-driven personalization and swift delivery. As a result, online channels are poised to redefine the retail landscape of Europe's watch market, steering it towards hybrid experiences.

Geography Analysis

In 2025, Germany commands a dominant 27.15% share of the market, bolstered by robust domestic demand for premium mechanical watches, a widespread network of specialty retailers, and a cultural emphasis on horological craftsmanship and engineering precision. The country's long-standing tradition of valuing high-quality engineering and precision manufacturing has positioned it as a key player in the luxury watch market, with German consumers showing a strong preference for established brands that emphasize heritage and innovation. Additionally, germany exports significant number of watches acrosss the world. In 2024, Swiss watch exports to Germany reached CHF 1,107.5 million, marking a 3.8% decline from 2023. This drop occurred as the broader industry witnessed a 2.8% dip, bringing total exports down to CHF 26.0 billion[3]Source: Federation of the Swiss Watch Industry, "Watch industry statistics", fhs.swiss.

Spain emerged as the fastest-growing market, boasting a CAGR of approximately 7.14%. Meanwhile, Russia's market faced a sharp contraction, grappling with the fallout from Western sanctions and the exit of luxury brands post the 2022 Ukraine invasion. This led to a notable decline in Swiss exports to Russia, with numerous global brands halting operations and redirecting their inventory to other European nations and the Middle East. Countries like the Netherlands, Poland, Belgium, and Sweden together hold mid-to-high single-digit market shares. Poland's growth is fueled by increasing disposable incomes and a burgeoning middle class, while the Netherlands reaps benefits from Amsterdam's logistics hub status. Belgium's luxury-watch demand is bolstered by its ties to Antwerp's diamond trade.

The geographic landscape reveals varied consumer inclinations: while Germany and the UK lean towards mechanical luxury and heritage brands, Spain and Poland emphasize fashion and value. The Nordics, on the other hand, champion sustainability and adventure wearables. Starting August 2025, U.S. tariffs on Swiss imports will see an added 39% on the landed cost, casting a shadow of uncertainty for brands reliant on transatlantic supply chains. Yet, European demand has shown resilience. Notably, Watches of Switzerland Group reported no significant shifts in consumer behavior up to October 2025, even with price hikes from luxury names like Rolex, Tudor, Omega, and Audemars Piguet.

Competitive Landscape

In the European watch market, a moderate concentration prevails. Competing for dominance are Swiss luxury giants LVMH, Richemont, and Swatch Group alongside independent manufacturers like Rolex and Patek Philippe. The competition also includes Japanese multinationals such as Seiko, Citizen, and Casio, and tech behemoths like Apple, Samsung, and Garmin, especially in the burgeoning smartwatch segment. At the premium tier, vertically integrated players hold sway. For instance, Rolex and Patek Philippe boast proprietary foundries, movement factories, and case-manufacturing facilities.

Emerging opportunities are evident in areas like biometric luxury hybrids, certified pre-owned platforms, and circular-economy models emphasizing repair and buy-back schemes. Rolex's late 2022 introduction of its Certified Pre-Owned initiative, which expanded to all U.S. agencies by October 2025, not only legitimizes the secondary market but also allows Rolex to reclaim margins previously enjoyed by gray-market dealers and auction houses. New entrants are shaking up the landscape: micro-brands leveraging crowdfunding to sidestep traditional retail, direct-to-consumer brands like Daniel Wellington and MVMT harnessing the power of Instagram influencers, and sustainability-centric startups such as Circular Clockworks, which designs for disassembly and offers take-back programs.

Technology is redefining the competitive landscape. The Apple Watch, leading the global smartwatch market, sets the standard with health features like ECG and fall detection. These benchmarks are now the gold standard for luxury hybrids. Additionally, blockchain-based digital passports and NFC chips are becoming essential tools for counterfeiting prevention and resale verification. The Federation of the Swiss Watch Industry is ramping up anti-counterfeiting measures. Concurrently, the EU's Corporate Sustainability Reporting Directive, which began rolling out in January 2023, will impose heightened transparency requirements. By 2028, Swiss groups with an EU turnover exceeding EUR 150 million will need to comply. Brands that weave circularity and traceability into their product design and supply-chain management stand to benefit the most.

Europe Watch Industry Leaders

-

Rolex SA

-

Compagnie Financire Richemont SA

-

The Swatch Group Ltd

-

Fossil Group Inc.

-

LVMH SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Buhlmann, in collaboration with DAN Europe, unveiled its Decompression 02 watches. Featuring a mechanical decompression display based on the Bühlmann ZH-L16B algorithm, the Decompression 02 allows divers to time their stops. This is facilitated by a distinctive Twin Safety Bezel, which differentiates between total dive time and decompression timing. These watches are available for purchase throughout Europe.

- November 2025: Seiko introduced its latest automatic stainless-steel watches, boasting a 40-hour power reserve and 10-bar water resistance. The SRE021 sports a dark navy dial, the SRE023 opts for a soft champagne hue, and the SRE024 showcases a two-tone gold accent on its bracelet and bezel.

- October 2025: Orient unveiled its new mechanical watch collection, dubbed the European Exclusive collection. The AC0F European Exclusive collection boasts five distinct options, each in muted tones, perfectly complementing their sophisticated style.

- June 2025: Casio debuted its inaugural automatic timepieces from the new EFK-100 collection, featuring five unisex models. Notably, the EFK-100CD and EFK-100XPB are equipped with forged carbon dials, a result of blending carbon fiber with resin and subjecting it to high temperature and pressure. These timepieces are being sold across various European nations.

Europe Watch Market Report Scope

A watch is a small, wearable timepiece that may be carried around. It is made to maintain a constant motion despite any motions brought on by the person's activities.

The scope of the European watch market includes segmentation of the market based on type, category, end users, distribution channel, and country. Based on type, the market is segmented under quartz/mechanical and digital watches.Based on category, the market is segmented into mass and premium. By end users, the market is segmented under women, men, and unisex. Further segmentation under the distribution channels includes supermarkets/hypermarkets, specilaty stores, online retail stores and others. By country, the market is segmented into the United Kingdom, Germany, Spain, Italy, Russia, France, Switzerland, and the Rest of Europe.

By Type

| Quartz/Mechanical | |

| Digital Watch | Smart Watches |

| Other Digital Types |

Category

| Mass |

| Premium |

End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Online Retail Stores |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Distribution Channels |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Quartz/Mechanical | |

| Digital Watch | Smart Watches | |

| Other Digital Types | ||

| Category | Mass | |

| Premium | ||

| End User | Men | |

| Women | ||

| Unisex | ||

| By Distribution Channel | Online Retail Stores | |

| Specialty Stores | ||

| Supermarkets/Hypermarkets | ||

| Other Distribution Channels | ||

| Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Europe watch market

The market is valued at USD 28.47 billion in 2025 and is forecast to reach USD 35.09 billion by 2031.

Which country leads European sales?

Germany holds the largest share at 27.15% of regional revenue in 2024.

How fast is the premium watch segment growing?

Premium timepieces priced above EUR 1,500 are projected to expand at a 7.34% CAGR between 2025-2030.

What channel is growing the quickest?

Online retail, including direct-to-consumer and certified pre-owned platforms, is projected to rise at a 7.61% CAGR through 2030.