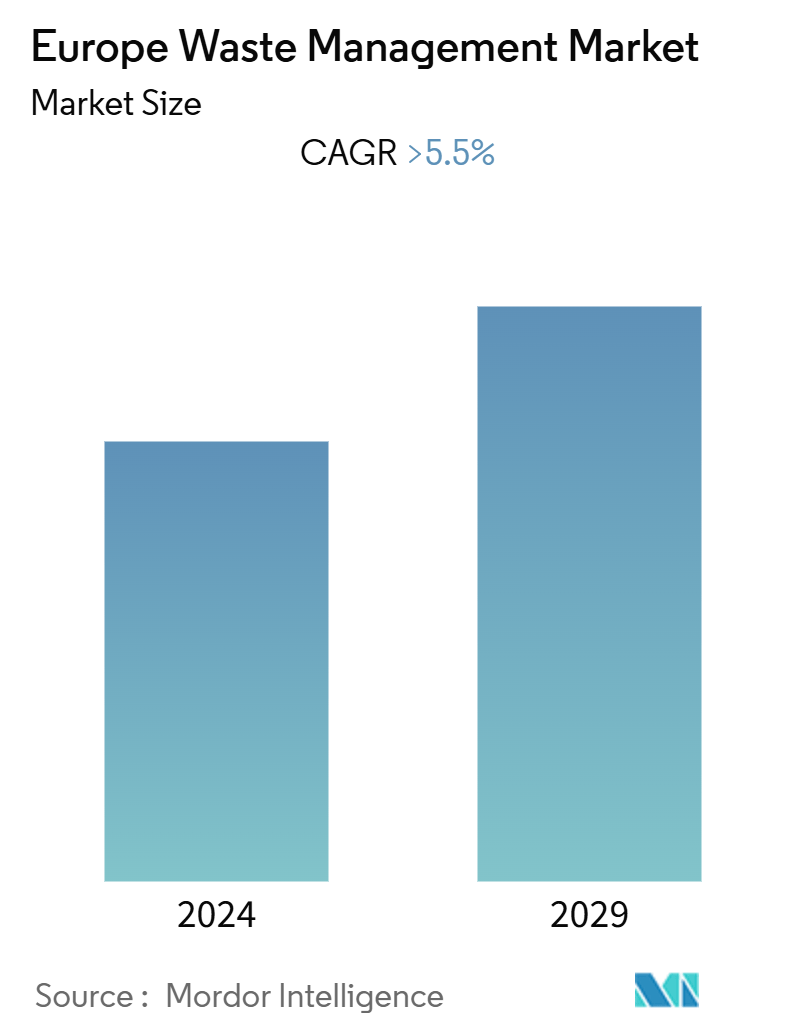

Market Size of Europe Waste Management Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR (2024 - 2029) | > 5.50 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Waste Management Market Analysis

The Europe Waste Management Market is expected to register a CAGR of greater than 5.5% during the forecast period.

- The outbreak of COVID-19 created several unforeseen pressures on municipal waste management. In most jurisdictions, services were permitted to continue despite various lockdown and curfew measures put in place to thwart transmission of the virus. Waste management personnel who continued to work throughout the pandemic were more likely to be exposed to the virus through close contact with other employees or contact with contaminated materials.

- For decades, Europe has poured millions of tons of its trash into incinerators each year, often under the green-sounding label "waste to energy." Now, concerns about incineration's outsized carbon footprint and fears it may undermine recycling are prompting European Union officials to ease their long-standing embrace of a technology that once seemed an appealing way to make waste disappear. By raising composting and recycling targets, mandating that plastic bottles contain 30% recycled content by 2030, and prohibiting the use of cutlery, cups, and stirrers, the EU is attempting to decrease waste, notably plastic waste. The EU has also developed a new "circular economy" plan, which intends to encourage better product design in the long run, making reuse and recycling easier.

- Two Belgian regions are likewise attempting to restrict incineration capacity. However, few other European countries are following suit. Some countries are planning new plants. Greece, Bulgaria, and Romania now landfill the majority of their waste and will likely require additional incinerator capacity in the future. Other countries that may develop additional plants include Italy and Spain.

- When it comes to e-waste, Norwegians are the worst offenders in Europe, with an average of 57 kg generated per household each year. Six tiny business printers weigh the same amount. The United Kingdom is in second place, with British families producing 55 kilograms of e-waste each year. Irish families generate an average of 52.4 kg of e-waste per year, putting them in third place. The weight of five adult bicycles is equivalent to Irish household e-waste. Spain (49.4 kg), the Netherlands (47.5 kg), Cyprus (47 kg), France (46.2 kg), and Luxembourg (45.4 kg) are the other European nations with homes producing more than 45 kg of e-waste, placing fifth, sixth, seventh, eighth, and ninth, respectively.

Europe Waste Management Industry Segmentation

The Waste Management (or waste disposal) market includes the activities and actions required to manage waste from its inception to its final disposal. This includes the collection, transport, treatment, and disposal of waste, together with monitoring and regulation of the waste management process.

Europe Waste Management Market is segmented By Waste Type (Industrial Waste, Municipal Solid Waste, Hazardous Waste, E-waste, Plastic Waste, Bio-Medical Waste and Other Waste Types), By Disposal Methods (Landfill, Incineration, Dismantling, Recycling), By Type of Ownership (Public, Private, Public-private Partnership), By Country (United Kingdom, Germany, France, Italy, Russia, Switzerland, Netherlands, Poland, Luxembourg, Belgium, Denmark, Sweden, Norway, Rest of Europe).

A comprehensive background analysis of the Europe Waste Management Market covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

| By Waste Type | |

| Industrial Waste | |

| Municipal Solid Waste | |

| Hazardous Waste | |

| E-waste | |

| Plastic Waste | |

| Bio-medical Waste |

| By Disposal Methods | |

| Landfill | |

| Incineration | |

| Dismantling | |

| Recycling |

| By Type of Ownership | |

| Public | |

| Private | |

| Public-private Partnership |

| By Country | |

| United Kingdom | |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Switzerland | |

| Netherlands | |

| Poland | |

| Luxembourg | |

| Belgium | |

| Denmark | |

| Sweden | |

| Norway | |

| Rest of Europe |

Europe Waste Management Market Size Summary

The Europe Waste Management Market is experiencing a dynamic transformation, driven by regulatory changes and technological advancements. The European Union is actively shifting its focus from traditional waste-to-energy solutions, such as incineration, due to concerns over their environmental impact and potential to hinder recycling efforts. This shift is part of a broader strategy to enhance recycling and composting targets, reduce plastic waste, and promote a circular economy. The EU's initiatives include mandating recycled content in plastic products and prohibiting certain single-use plastics, aiming to foster sustainable waste management practices. Despite these efforts, some regions, like Greece and Bulgaria, continue to rely heavily on landfilling, indicating a varied approach across Europe. The market is also witnessing a rise in e-waste generation, with countries like Norway and the UK leading in per-household e-waste production, prompting the EU to implement stricter regulations on hazardous materials and promote recycling.

The market landscape is characterized by a mix of global and local players, with companies like Veolia, Suez, Remondis, FCC, and Urbaser playing significant roles. The demand for waste-to-energy solutions is driven by increasing waste generation and the need for sustainable urban living, although the focus is gradually shifting towards recycling due to its energy-saving potential. Emerging technologies, such as Dendro Liquid Energy, offer promising opportunities for market players by enhancing efficiency and reducing emissions. Germany stands out as a key player in the market, with rapid urbanization and the development of municipal waste energy plants fueling growth. The market is fragmented, with ongoing mergers and partnerships aimed at expanding service offerings and gaining competitive advantages, as seen in recent acquisitions by companies like Saica Group and Beauparc.

Europe Waste Management Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Value Chain / Supply Chain Analysis

-

1.5 Industry Attractiveness - Porters Five Force's Analysis

-

1.5.1 Threat of New Entrants

-

1.5.2 Bargaining Power of Buyers/Consumers

-

1.5.3 Bargaining Power of Suppliers

-

1.5.4 Threat of Substitute Products

-

1.5.5 Intensity of Competitive Rivalry

-

-

1.6 Insights into Technological Advancements and Innovation in Effective Waste Management

-

1.7 Insights on Strategies of Rising Startups Venturing into the Europe Waste Management Industry

-

1.8 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION (Market Size by Value and Volume)

-

2.1 By Waste Type

-

2.1.1 Industrial Waste

-

2.1.2 Municipal Solid Waste

-

2.1.3 Hazardous Waste

-

2.1.4 E-waste

-

2.1.5 Plastic Waste

-

2.1.6 Bio-medical Waste

-

-

2.2 By Disposal Methods

-

2.2.1 Landfill

-

2.2.2 Incineration

-

2.2.3 Dismantling

-

2.2.4 Recycling

-

-

2.3 By Type of Ownership

-

2.3.1 Public

-

2.3.2 Private

-

2.3.3 Public-private Partnership

-

-

2.4 By Country

-

2.4.1 United Kingdom

-

2.4.2 Germany

-

2.4.3 France

-

2.4.4 Italy

-

2.4.5 Russia

-

2.4.6 Switzerland

-

2.4.7 Netherlands

-

2.4.8 Poland

-

2.4.9 Luxembourg

-

2.4.10 Belgium

-

2.4.11 Denmark

-

2.4.12 Sweden

-

2.4.13 Norway

-

2.4.14 Rest of Europe

-

-

Europe Waste Management Market Size FAQs

What is the current Europe Waste Management Market size?

The Europe Waste Management Market is projected to register a CAGR of greater than 5.5% during the forecast period (2024-2029)

Who are the key players in Europe Waste Management Market?

Veolia, Suez, Remondis, FCC and Urbaser are the major companies operating in the Europe Waste Management Market.