| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.66 Billion |

| Market Size (2030) | USD 3.07 Billion |

| CAGR (2025 - 2030) | 13.07 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Warranty Management System Market Analysis

The Europe Warranty Management System Market size is estimated at USD 1.66 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 13.07% during the forecast period (2025-2030).

The European warranty management landscape is experiencing a significant digital transformation, driven by the increasing adoption of digital warranty management solutions across industries. According to recent data, 41% of EU businesses have adopted cloud computing services, highlighting the region's growing acceptance of digital solutions in business operations. This shift is particularly evident in the manufacturing sector, where companies are leveraging cloud-based warranty management systems to streamline their operations and enhance customer service delivery. The integration of these systems has become crucial for businesses seeking to maintain competitive advantages in increasingly complex supply chains and production processes.

The industrial sector's evolution towards smart manufacturing is creating new opportunities for warranty management solutions. According to the International Trade Administration, Italy's commitment to advanced manufacturing is demonstrated through its allocation of EUR 13.4 billion in tax credits for investment in advanced manufacturing technologies. This investment trend is reflected across Europe, with the Netherlands' machinery and equipment manufacturing sector showing significant growth, recording an increase of EUR 517.8 million in production value. These developments are driving the need for more sophisticated warranty management software that can handle complex industrial equipment and processes.

A notable disparity exists in the adoption of Industrial Internet of Things (IIoT) solutions between large enterprises and SMEs, which directly impacts warranty management system implementation. Research indicates that while 94% of large Italian companies are familiar with IIoT solutions, only 41% of SME companies demonstrate awareness, highlighting a significant adoption gap in the market. This divergence is creating a two-tiered market where large enterprises are implementing advanced warranty management solutions while SMEs are still in the early stages of digital transformation.

The European market is witnessing a strategic shift towards sovereign cloud solutions for warranty management systems, driven by data protection regulations and security concerns. In 2023, major technology providers announced plans to introduce new sovereign cloud zones in the European Union, with initial implementations in Germany and Spain. This development coincides with increased investment in critical industries, exemplified by France's defense sector allocation of EUR 43.9 billion in 2023, creating new opportunities for specialized warranty management system solutions in highly regulated sectors. These investments reflect the growing importance of data sovereignty and security in warranty management implementations across Europe.

Europe Warranty Management System Market Trends

Rising Adoption of warranty management systems in the Manufacturing and Automotive Industries

The manufacturing and automotive sectors are experiencing significant transformation in warranty management system practices driven by increasing digitalization and complexity of products. Manufacturers have evolved from simply offering basic product coverage to implementing comprehensive warranty management software that encompasses everything from product coverage to customer service and logistics. This evolution is particularly evident in the European manufacturing sector, where companies like German machinery and equipment manufacturers, comprising nearly 6,600 enterprises with 90% being SMEs, are actively adopting digital warranty solutions to manage their complex supply chains and product warranties. The integration of warranty service management enables manufacturers to track customer service experiences and product performance in near real-time, leveraging connected devices and automated warranty systems to collect and analyze data throughout the service lifecycle.

The automotive industry's transition toward electric and connected vehicles has created additional imperatives for sophisticated warranty claims management solutions. With the European automotive sector experiencing a significant shift toward electric mobility, OEMs must manage an increasing number of technical warranty requests from their dealers. The complexity is amplified as electric vehicles introduce new components not covered by traditional auto warranty programs, such as plugs, sockets, inverters, and power pack coolers. This transformation has prompted automotive manufacturers to implement advanced warranty management systems that can handle these new complexities while simultaneously reducing administration costs and improving customer satisfaction. The systems help in tracking warranty claims, managing supplier recovery, and providing valuable insights for product quality improvements through comprehensive data analytics.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Adoption of AI and ML Capabilities in Next-Generation Warranty Management Systems to Ensure Customer Satisfaction

The integration of artificial intelligence and machine learning capabilities in warranty lifecycle management represents a transformative shift in how companies handle warranty lifecycle management. Modern warranty management systems are leveraging these technologies to enhance customer satisfaction through improved claim processing accuracy and fraud detection capabilities. AI-based systems employ sophisticated image recognition technology to efficiently and cost-effectively identify fraudulent claims, with machine learning algorithms trained on tens of thousands of images to distinguish between genuine issues and manipulated or recycled claims. This technological advancement has enabled companies to significantly reduce warranty costs while simultaneously improving the speed and accuracy of claim processing.

The implementation of warranty analytics powered by AI and ML provides manufacturers with unprecedented insights into product performance and customer behavior patterns. These advanced analytical capabilities enable companies to transform raw warranty data into actionable intelligence, leading to more accurate warranty forecasting and, in some cases, even preventing warranty claims altogether. For instance, technology companies are now utilizing data lakes and sophisticated algorithms to analyze customer feedback and social media sentiments, allowing them to proactively identify potential warranty claims before customers contact support desks. This proactive approach has demonstrated significant results, with some companies reporting up to a 15% reduction in warranty expenditures through the implementation of these advanced analytical tools. Furthermore, the integration of these technologies allows manufacturers to modify their warranty policies based on actual product usage patterns rather than engineering theories, leading to more accurate and customer-centric warranty offerings.

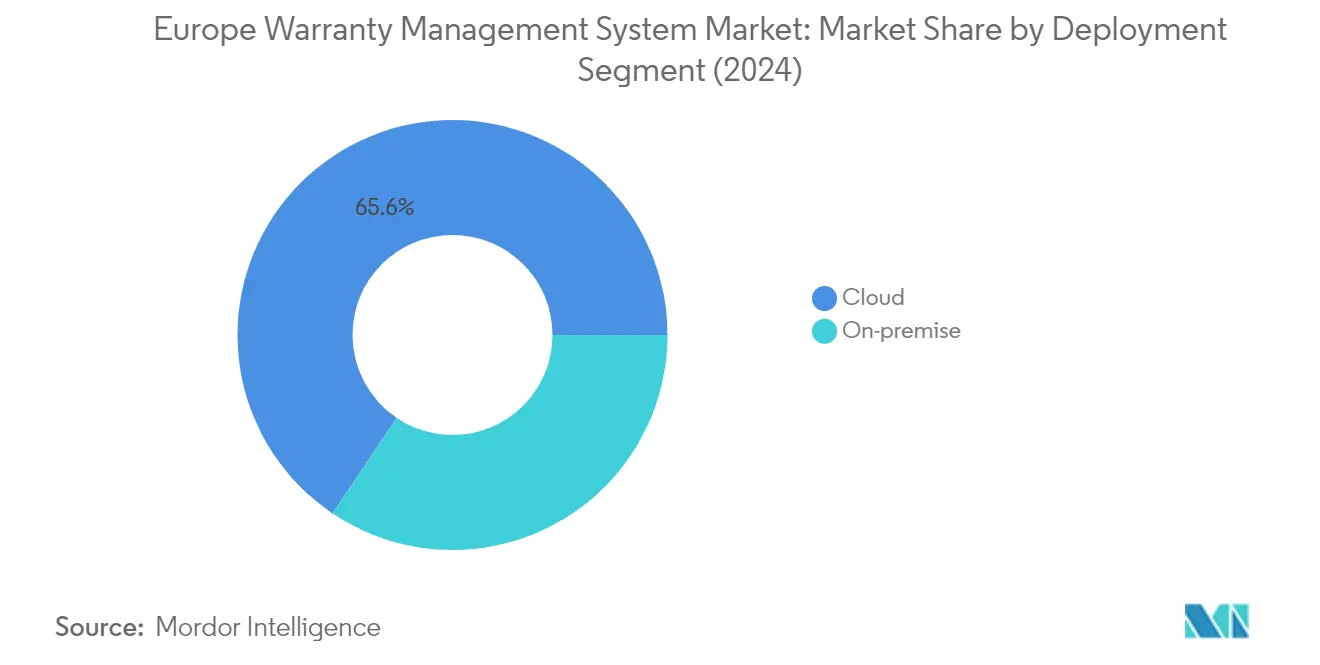

Segment Analysis: By Deployment

Cloud Segment in Europe Warranty Management System Market

The cloud segment has emerged as the dominant force in the European warranty management system market, commanding approximately 66% market share in 2024. This substantial market presence is driven by the increasing realization among enterprises about the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage. The deployment of cloud-based warranty management platforms has been particularly influenced by the convergence of numerous technologies in the manufacturing sector, including predictive analytics, big data, cloud computing, digital twins, and smart factories. Cloud-based solutions benefit from lower capital expenditure requirements, as companies do not need to invest in hardware components, making the business case much more compelling. Additionally, hardware and IT support savings make cloud-based solutions much more affordable and accessible to organizations of all sizes.

Cloud Segment Growth Trajectory in Europe WMS Market

The cloud segment is experiencing remarkable growth momentum, projected to expand at approximately 12% through 2024-2029. This accelerated growth is fueled by the increasing adoption of cloud services across European enterprises, particularly in highly regulated industries. The growth is further supported by various government initiatives and digital transformation programs across Europe. For instance, the European Union's emphasis on cloud adoption and data sovereignty has led to significant investments in cloud infrastructure and services. The segment's growth is also driven by the enhanced flexibility cloud solutions offer, allowing businesses to rapidly scale their warranty management system capabilities up or down based on operational needs. Furthermore, the integration of advanced technologies like artificial intelligence and machine learning in cloud-based warranty management platforms is attracting more organizations to adopt these solutions.

Segment Analysis: By End-User Industry

Industrial Equipment Segment in Europe Warranty Management System Market

The industrial equipment segment maintains its dominant position in the European warranty management system market, commanding approximately 33% market share in 2024. This significant market presence is driven by the increasing complexity of industrial machinery and equipment, which requires sophisticated warranty tracking systems and management solutions. The segment's strength is particularly evident in heavy equipment and machinery sectors, where product warranty management solutions help organizations reduce downtime costs and improve operational efficiency. Industrial equipment manufacturers are increasingly adopting automated warranty management systems to handle complex warranty claims, manage supplier recovery processes, and enhance customer satisfaction through improved service delivery. The segment's robust performance is further supported by the strong growth in industrial manufacturing capacity across Europe, leading to a sharp rise in assets requiring warranty management beyond their original manufacturers' warranty period.

Automotive and Transportation Segment in Europe Warranty Management System Market

The automotive and transportation segment is emerging as the fastest-growing segment in the European warranty management system market, with an expected growth rate of approximately 12% during 2024-2029. This remarkable growth is driven by the increasing complexity of vehicle warranties, particularly with the rise of electric and connected vehicles. The segment's expansion is fueled by automotive manufacturers' growing focus on warranty analytics and predictive maintenance capabilities to enhance customer satisfaction and reduce warranty-related costs. The integration of AI and machine learning technologies in warranty management solutions is enabling automotive companies to better predict and prevent potential warranty claims, while also streamlining the claims processing workflow. The transition to electric vehicles is creating new opportunities for warranty management solutions, especially in handling specialized components like battery warranties and electric powertrain systems.

Remaining Segments in End-User Industry

The consumer durable and other verticals segments continue to play vital roles in shaping the European warranty management system market. The consumer durable segment is particularly significant in managing warranties for major residential appliances and HVAC systems, with manufacturers increasingly focusing on digital warranty solutions to enhance customer experience and reduce operational costs. The other verticals segment, encompassing medical devices, aerospace, and defense industries, contributes to market diversity through specialized warranty management requirements for high-value equipment and critical systems. These segments are witnessing increased adoption of cloud-based warranty management solutions and integration of advanced analytics capabilities to improve warranty claim processing and fraud detection.

Europe Warranty Management System Market Geography Segment Analysis

Warranty Management System Market in the United Kingdom

The United Kingdom dominates the European warranty management system market, commanding approximately 35% of the total market value in 2024. The country's leadership position is strengthened by its robust manufacturing sector and progressive approach to digital transformation. The UK government's active support for cloud computing, particularly through initiatives like G-Cloud and the 'Cloud First' policy, has created a conducive environment for warranty management software adoption. The region has witnessed significant traction in warranty analytics solutions, with companies leveraging data and predictive analytics to enhance their warranty claim processes. The presence of strong automotive and industrial sectors, coupled with increasing demand for HVAC systems, has further catalyzed market growth. Additionally, the country's emphasis on medical device regulations and healthcare technology adoption has created new opportunities for warranty management system providers.

Warranty Management System Market in Germany

Germany stands out as the most dynamic market in the European warranty management system landscape, projected to grow at approximately 12% CAGR from 2024 to 2029. The country's market is driven by its strong industrial base, particularly in machinery and equipment manufacturing, with nearly 6,600 enterprises along the value chain. Recent legislative changes in warranty regulations have strengthened consumer protection, creating increased demand for sophisticated warranty management solutions. The country's leadership in automotive manufacturing and Industry 4.0 initiatives has spurred the adoption of advanced warranty management systems. The integration of artificial intelligence and machine learning in warranty analytics has become increasingly prevalent among German manufacturers. Furthermore, the country's emphasis on electric vehicle production and associated warranty complexities has created new opportunities for warranty management solution providers. The presence of innovative startups and established technology firms has fostered a competitive environment for warranty management software.

Warranty Management System Market in France

France's warranty management system market demonstrates robust growth driven by its strong industrial base and increasing digitalization initiatives. The country's strategic focus on e-invoicing and digital transformation has created a favorable environment for warranty management system adoption. French manufacturers are increasingly embracing cloud-based warranty solutions to enhance their operational efficiency and customer service capabilities. The defense sector's modernization efforts have created new opportunities for warranty administration software providers, particularly in tracking and managing warranties for complex military equipment. The country's emphasis on industrial automation and Industry 4.0 has led to increased integration of warranty management systems with other enterprise solutions. French companies are particularly focused on developing innovative warranty management solutions that incorporate artificial intelligence and predictive analytics capabilities. The market has also benefited from the growing adoption of warranty management systems in the consumer durables and automotive sectors.

Warranty Management System Market in Other Countries

The warranty management system market in other European countries, including Italy and the Netherlands, demonstrates varying levels of maturity and adoption patterns. These markets are characterized by their unique industrial strengths and regulatory frameworks, which influence the implementation of warranty management solutions. The manufacturing sector in these countries has shown increasing interest in digital warranty management solutions, particularly in automotive and industrial equipment segments. Cloud-based warranty management solutions are gaining traction, driven by the need for cost-effective and scalable solutions. The markets are witnessing a gradual shift from traditional warranty management approaches to more sophisticated, data-driven solutions. Regional players are focusing on developing customized warranty management solutions that address specific industry requirements while complying with local regulations. The increasing emphasis on customer experience and after-sales service has created new opportunities for warranty management system providers in these markets.

Get Analysis on Important Geographic Markets

Download PDF

Europe Warranty Management System Industry Overview

Top Companies in Europe Warranty Management System Market

The European warranty management system market features prominent players like Oracle, IBM, Syncron AB, IFS AB, and PTC Inc. leading the competitive landscape. These companies are heavily investing in cloud-based warranty management software solutions and artificial intelligence capabilities to enhance their product offerings and maintain market leadership. Strategic partnerships with technology providers and system integrators have become a crucial trend, enabling companies to expand their service capabilities and geographical reach. The focus on research and development remains strong, with companies developing innovative features like automated claims processing, supplier recovery management, and predictive analytics. Market leaders are also emphasizing customer-centric approaches through customized solutions and dedicated support services, while simultaneously expanding their presence through strategic acquisitions and collaborations.

Market Dominated by Global Tech Conglomerates

The European warranty management system market structure is characterized by the strong presence of global technology conglomerates that leverage their extensive resources and established customer relationships across multiple industries. These major players benefit from their comprehensive product portfolios, strong brand recognition, and ability to offer integrated solutions that combine warranty management software with broader enterprise software capabilities. The market also includes specialized regional players like Syncron AB and SKYLYZE, who have carved out niches by focusing on specific industries or geographical regions, particularly in the automotive and manufacturing sectors.

The market demonstrates moderate consolidation, with larger players actively pursuing strategic acquisitions to enhance their technological capabilities and expand their market presence. Companies are increasingly focusing on building partner ecosystems, collaborating with local system integrators and technology providers to strengthen their market position and delivery capabilities. The competitive dynamics are further shaped by the growing trend of cloud-based solutions, which has lowered entry barriers for innovative startups while simultaneously providing established players with opportunities to expand their service offerings.

Innovation and Customer Focus Drive Success

Success in the European warranty management platform market increasingly depends on providers' ability to deliver innovative, scalable solutions that address evolving customer needs while ensuring regulatory compliance, particularly with GDPR and other data protection requirements. Companies that can effectively combine warranty management with advanced technologies like artificial intelligence, machine learning, and IoT are better positioned to capture market share. The ability to offer flexible deployment options, seamless integration capabilities, and industry-specific solutions has become crucial for both established players and new entrants.

Market participants must focus on developing strong service capabilities and maintaining close customer relationships to succeed in this competitive landscape. The growing emphasis on sustainability and product lifecycle management creates opportunities for providers to expand their warranty management solution with environmental compliance features. Companies need to invest in building robust partner networks and maintaining a strong local presence while offering solutions that can be easily customized for different industries and geographical markets. The ability to provide comprehensive analytics and reporting capabilities, along with proven expertise in handling complex warranty processes, will continue to be key differentiators in the market.

Europe Warranty Management System Market Leaders

-

Syncron AB

-

Tavant Technologies Inc

-

Servicemax Inc

-

Oracle Corporation

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Warranty Management System Market News

- Oct 2022: Fiat Professional UK announced that the E-Ducato electric van comes with a five-year warranty, a service plan, and roadside support as standard equipment. The warranty spans up to 125,000 miles or the first of the standard three years plus an additional two. While free service is designed to be provided once every two years or every 30,000 miles, roadside help would be available around the clock, creating a demand for the applications of warranty management systems in the European market.

- Oct 2022: ServiceMax Inc., a field service management company for asset management, has gained a contract from Horiba Europe GmbH to deploy its field service management platform to digitize Horiba's operations across Europe, including the warranty management of the products. Additionally, as part of its global business transformation efforts, HORIBA Europe GmbH has planned to replace its traditional field management system to automate manual tasks and improve customer service, creating a demand for the market in Europe.

Europe Warranty Management System Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rising Adoption of Warranty Management Systems in the Manufacturing and Automotive Industries

- 5.1.2 Increasing Adoption of AI and ML Capabilities in Next-generation Warranty Management Systems to Ensure Customer Satisfaction

-

5.2 Market Restraints

- 5.2.1 Intense Competition Between Independent Service Providers in Price-sensitive Markets

6. MARKET SEGMENTATION

-

6.1 By Deployment

- 6.1.1 On-Premise

- 6.1.2 Cloud

-

6.2 By End-user Industry

- 6.2.1 Industrial Equipment

- 6.2.2 Automotive and Transportation

- 6.2.3 Consumer Durable

- 6.2.4 Other End-user Industries (Medical Devices, Aerospace, Defense, Etc.)

-

6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Rest of Europe

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Syncron AB

- 7.1.2 IFS AB

- 7.1.3 Tavant Technologies Inc.

- 7.1.4 ServiceMax Inc.

- 7.1.5 SKYLYZE

- 7.1.6 Pegasystems Inc.

- 7.1.7 PTC Inc.

- 7.1.8 Oracle Corporation

- 7.1.9 IBM Corporation

- 7.1.10 Wipro Limited

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Warranty Management System Industry Segmentation

The Europe Warranty management system primarily caters to the software and services of warranty and post-warranty support management solutions. The solutions include warranty registration, claim submission, processing and settlement, fraud detection, supplier recovery, returns management, extended warranty marketing, replacement parts logistics, and inventory management.

Europe's Warranty Management System Market is Segmented by Deployment (On-premise and Cloud), End-user Industry (Industrial Equipment, Automotive and Transportation, and Consumer Durable), and Country. The report offers the market size in value terms in USD for all the abovementioned segments.

| By Deployment | On-Premise |

| Cloud | |

| By End-user Industry | Industrial Equipment |

| Automotive and Transportation | |

| Consumer Durable | |

| Other End-user Industries (Medical Devices, Aerospace, Defense, Etc.) | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe Warranty Management System Market Research FAQs

How big is the Europe Warranty Management System Market?

The Europe Warranty Management System Market size is expected to reach USD 1.66 billion in 2025 and grow at a CAGR of 13.07% to reach USD 3.07 billion by 2030.

What is the current Europe Warranty Management System Market size?

In 2025, the Europe Warranty Management System Market size is expected to reach USD 1.66 billion.

Who are the key players in Europe Warranty Management System Market?

Syncron AB, Tavant Technologies Inc, Servicemax Inc, Oracle Corporation and IBM Corporation are the major companies operating in the Europe Warranty Management System Market.

What years does this Europe Warranty Management System Market cover, and what was the market size in 2024?

In 2024, the Europe Warranty Management System Market size was estimated at USD 1.44 billion. The report covers the Europe Warranty Management System Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Warranty Management System Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Warranty Management System Market Research

Mordor Intelligence offers comprehensive expertise in analyzing the warranty management system landscape, providing detailed insights into the evolving WMS industry. Our extensive research covers the complete spectrum of warranty management software solutions. This includes digital warranty management implementations and advanced warranty management solutions. The report delivers an in-depth analysis of service contract management practices, examining how modern warranty management platforms are transforming traditional business operations. Available as an easy-to-read report PDF for download, this analysis encompasses warranty claims management processes and emerging technological trends.

Stakeholders benefit from our detailed examination of warranty tracking systems and product warranty management strategies. The report is supported by comprehensive data and actionable recommendations. It explores warranty lifecycle management developments, warranty registration systems, and innovative approaches to warranty service management. Our analysis includes detailed insights into warranty administration software implementations, providing decision-makers with valuable intelligence for strategic planning. The research methodology combines primary industry data with expert analysis, delivering a thorough understanding of current market dynamics and future opportunities in the European WMS sector.