Market Size of Europe Warehouse Automation Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

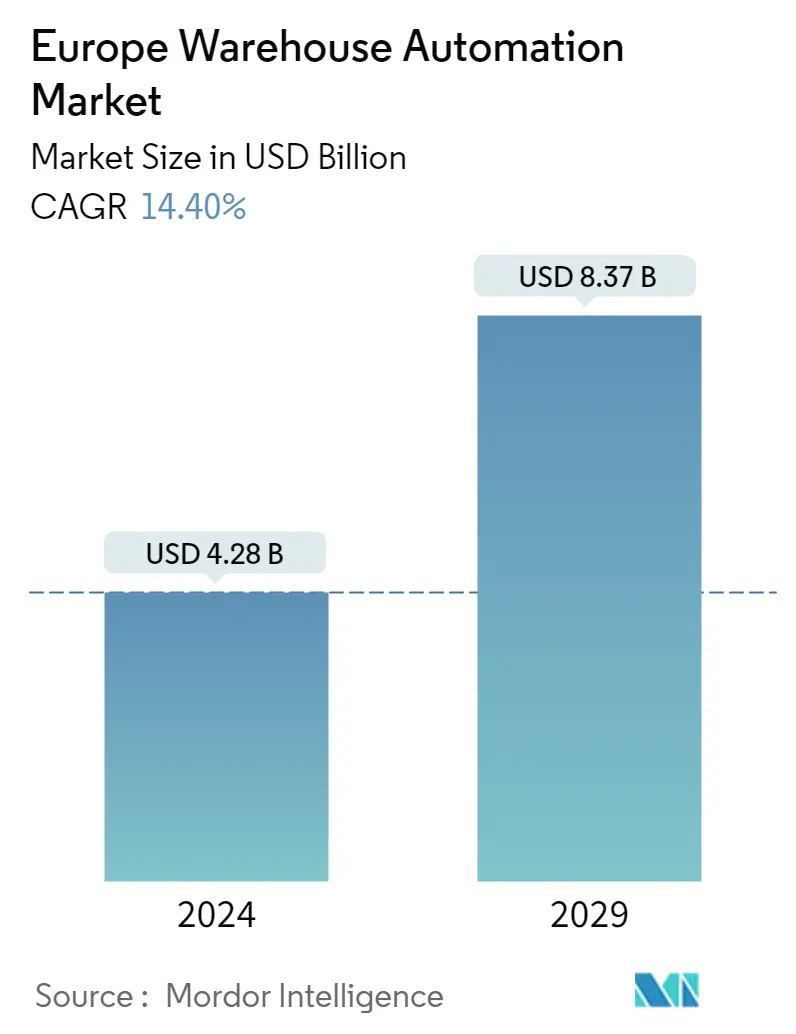

| Market Size (2024) | USD 4.28 Billion |

| Market Size (2029) | USD 8.37 Billion |

| CAGR (2024 - 2029) | 14.40 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Warehouse Automation Market Analysis

The Europe Warehouse Automation Market size is estimated at USD 4.28 billion in 2024, and is expected to reach USD 8.37 billion by 2029, growing at a CAGR of 14.40% during the forecast period (2024-2029).

Furthermore, whereas warehouse robots have had enormous deployments, COVID-19 is likely to significantly increase deployment speed. The COVID-19 outbreak has prompted warehouse owners to explore expediting their automation and robotics implementation timelines. Those who have successfully adopted automation have also demonstrated the establishment of safer workplaces by limiting worker interactions while raising productivity to meet rising e-commerce needs. Thousands of brick-and-mortar stores have closed their doors due to the recent increase in e-commerce.

- In Europe, the warehouse automation growth increased post-pandemic. This results from two interconnected trends: a seemingly unstoppable rise in e-commerce and a persistent labor shortage resulting in rising labor prices. The market for warehouse robots in Europe has been driven by the growing number of warehouses and increased expenditures on warehouse automation, rising labor costs, and the availability of scalable technical solutions.

- Regarding demand and the presence of OEMs and System Integrators, Germany is one of the leading countries in warehouse automation. OEMs are well-represented in Europe, with strongholds in Germany, Italy, France, the Netherlands, and Spain. Central and Eastern Europe is a rapidly growing region within Europe, with Poland and the Czech Republic emerging as logistical hubs with promising economic potential. However, expansion and investment plans have been put on hold due to the present geopolitical circumstances, including the Russia-Ukraine conflict.

- The Internet of Things is driving inventory and warehouse automation developments. It's contributing to the transformation of the warehouse into a connected and coordinated system. In 2021 and beyond, lower costs and enhanced IoT sensors are expected to boost the use of IoT in warehouses. For Instance, In May 2020, DHL, a German logistics company, said that it had partnered with Cisco, a US technology company, to introduce IoT to three large warehouse operations across Europe.

- However, warehousing automation is extremely beneficial when it comes to lowering overall business expenditures and eliminating product delivery faults. Despite the benefits, 80 percent of warehouses are "still manually operated with no supporting automation," according to DHL, a notable 3PL business and a major end-user of warehouse automation technologies. Furthermore, conveyor-based, sorter-based, and pick-and-place warehouses account for 15% of all warehouses. In comparison, only 5% of today's warehouses are automated.

Europe Warehouse Automation Industry Segmentation

The European warehouse automation market study involves segmentation by component wherein hardware (AGV/AMR, AS/AR, piece picking, etc.), software (warehouse management systems, warehouse execution systems), and services (value-added services, maintenance, etc.) sub-segments are being analyzed.

Further, the warehouses and fulfillment centers perform activities across end-users, such as food and beverage, post and parcel, apparel, general merchandise, and manufacturing, to name a few. The manufacturing industry majorly includes the automotive, electronics, and pharmaceutical sectors. The study also provides the impact of COVID-19 on the market studied.

| Component | ||||||||

| ||||||||

| Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES)) | ||||||||

| Services (Value Added Services, Maintenance, etc.) |

| End-User | |

| Food and Beverage (Including Manufacturing Facilities and Distribution Centers) | |

| Post and Parcel | |

| Groceries | |

| General Merchandise | |

| Apparel | |

| Manufacturing (Durable and Non-Durable) | |

| Other End-user Industries |

| Country | |

| United Kingdom | |

| Germany | |

| France | |

| Rest of Europe |

Europe Warehouse Automation Market Size Summary

The European warehouse automation market is experiencing significant growth, driven by the increasing demand for efficient logistics solutions amid the rise of e-commerce and labor shortages. The market is characterized by the adoption of advanced technologies such as autonomous mobile robots (AMRs) and the Internet of Things (IoT), which are transforming traditional warehouses into connected and automated systems. The COVID-19 pandemic has accelerated this trend, prompting businesses to expedite their automation timelines to enhance productivity and safety. Despite the benefits, a substantial portion of warehouses remain manually operated, indicating a vast potential for growth in automation adoption across the region.

Germany, along with other European countries like Italy, France, and the Netherlands, is at the forefront of this automation wave, supported by a strong presence of original equipment manufacturers (OEMs) and system integrators. The automotive sector, in particular, is a significant driver of warehouse automation, with companies like Exmac Automation and Industore providing advanced storage solutions. The market is competitive, with major players such as Dematic Group, Swisslog Holding AG, and WITRON Logistik + Informatik GmbH focusing on expanding their market share through strategic initiatives like product launches and acquisitions. The ongoing geopolitical challenges, such as the Russia-Ukraine conflict, pose potential risks to expansion plans, but the overall outlook for the European warehouse automation market remains positive, with substantial growth anticipated in the coming years.

Europe Warehouse Automation Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Value Chain / Supply Chain Analysis

-

1.3 Industry Attractiveness -Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Industry Value Chain Analysis

-

1.5 Warehouse Investment Scenario

-

1.6 Impact of Macro-economic Factors on the Warehouse Automation Market

-

1.7 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Component

-

2.1.1 Hardware

-

2.1.1.1 Mobile Robots (AGV, AMR)

-

2.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

-

2.1.1.3 Automated Conveyor & Sorting Systems

-

2.1.1.4 De-palletizing/Palletizing Systems

-

2.1.1.5 Automatic Identification and Data Collection (AIDC)

-

2.1.1.6 Piece Picking Robots

-

-

2.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

-

2.1.3 Services (Value Added Services, Maintenance, etc.)

-

-

2.2 End-User

-

2.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

-

2.2.2 Post and Parcel

-

2.2.3 Groceries

-

2.2.4 General Merchandise

-

2.2.5 Apparel

-

2.2.6 Manufacturing (Durable and Non-Durable)

-

2.2.7 Other End-user Industries

-

-

2.3 Country

-

2.3.1 United Kingdom

-

2.3.2 Germany

-

2.3.3 France

-

2.3.4 Rest of Europe

-

-

Europe Warehouse Automation Market Size FAQs

How big is the Europe Warehouse Automation Market?

The Europe Warehouse Automation Market size is expected to reach USD 4.28 billion in 2024 and grow at a CAGR of 14.40% to reach USD 8.37 billion by 2029.

What is the current Europe Warehouse Automation Market size?

In 2024, the Europe Warehouse Automation Market size is expected to reach USD 4.28 billion.