Europe Van Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

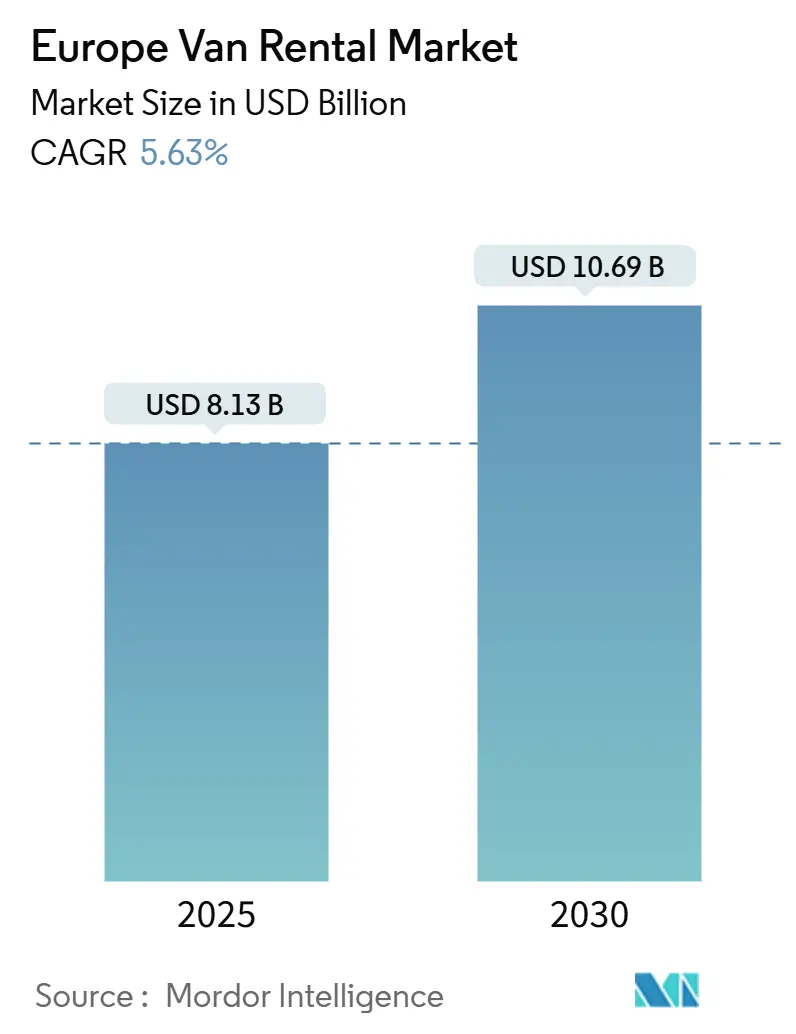

| Market Size (2025) | USD 8.13 Billion |

| Market Size (2030) | USD 10.69 Billion |

| Growth Rate (2025 - 2030) | 5.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Van Rental Market Analysis by Mordor Intelligence

The European van rental market size is expected to be USD 8.13 billion in 2025 and is forecasted to reach USD 10.69 billion by 2030, advancing at a 5.63% CAGR. E-commerce logistics demand, stricter low-emission rules, rising tourism, and the corporate shift to asset-light mobility strategies drive growth. Cargo vans provide the backbone of last-mile delivery, while passenger vans are gaining traction as Mediterranean travel rebounds. Digital platforms expand reach through instant booking and keyless access, while established operators accelerate fleet electrification to stay compliant with the growing Low Emission Zones. Competitive intensity is rising as scale players pursue acquisitions, technology upgrades, and manufacturer alliances that secure scarce electric van supply.

Key Report Takeaways

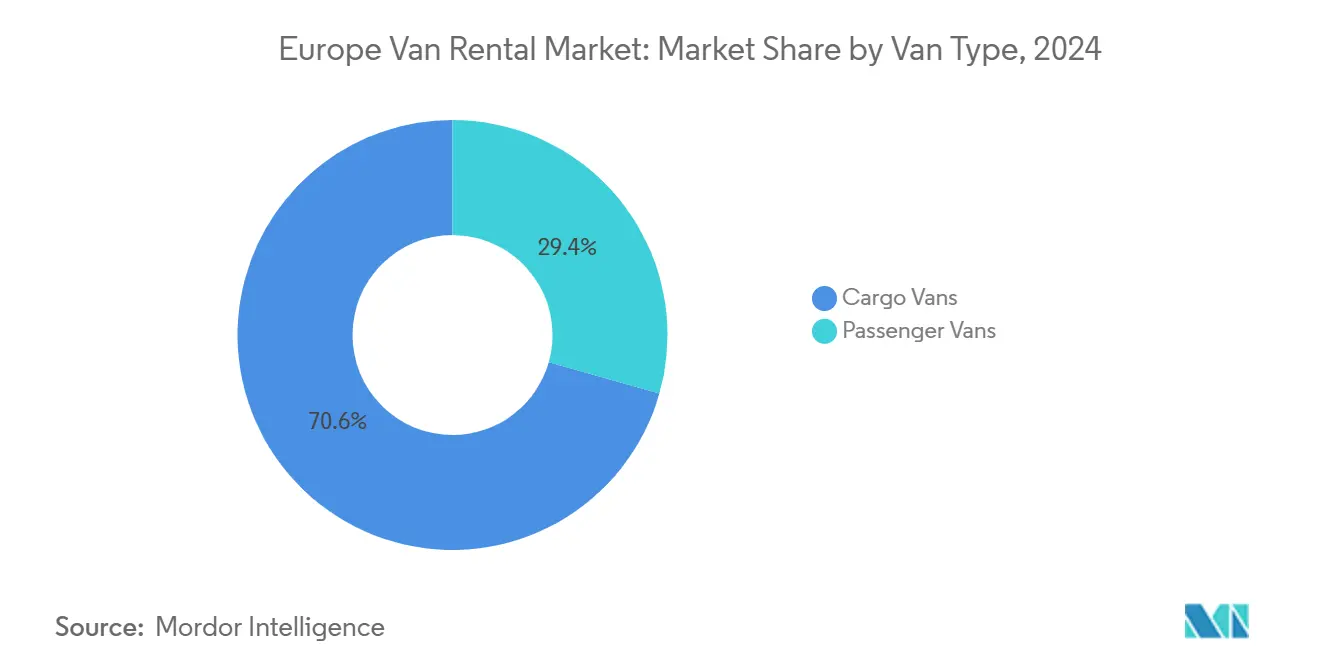

- By van type, cargo models led with 70.61% revenue share in 2024; passenger vans are projected to rise at 5.98% CAGR to 2030.

- By rental duration, daily contracts held 44.23% of the European van rental market share in 2024, whereas long-term leasing is projected to record the highest CAGR at 6.07% through 2030.

- By application, commercial usage accounted for a 59.29% share of the European van rental market size in 2024; personal usage is expanding at a faster rate of 5.79% CAGR over the same period.

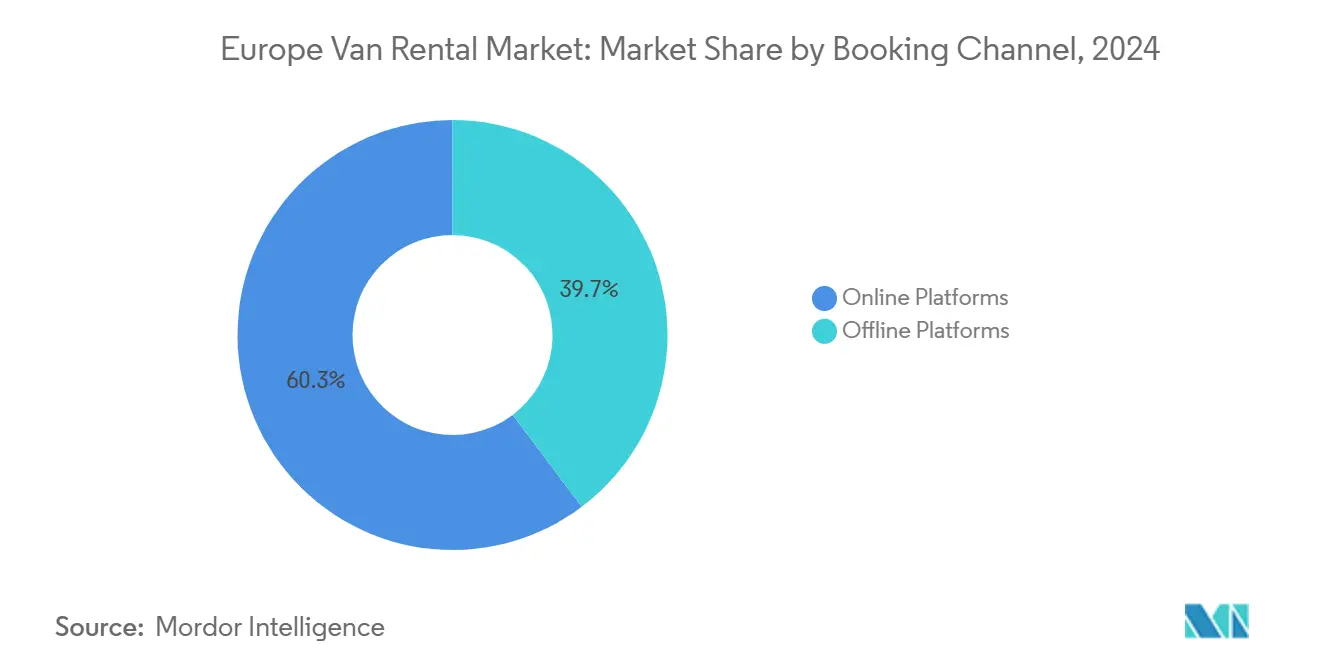

- Through the booking channel, online platforms captured a 60.33% revenue share in 2024 and are expected to continue climbing at a 6.16% CAGR to 2030.

- By customer type, corporate accounts accounted for 42.43% of bookings in 2024, while travel agencies posted the fastest growth, at a 6.28% CAGR, from 2024 to 2030.

- By country, Germany led with a 25.19% share in 2024; Spain is forecast to grow at a 6.11% CAGR through 2030.

Europe Van Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-Mile Delivery Boom | +1.2% | Germany, United Kingdom, France | Short term (≤ 2 years) |

| ESG-Driven EV Van Leasing | +1.1% | Germany, Netherlands, Scandinavia | Long term (≥ 4 years) |

| SME Shift to Flexible Rentals | +0.9% | Urban centers across Europe | Medium term (2-4 years) |

| Tourism Boosts Van Demand | +0.8% | Spain, Italy, France | Short term (≤ 2 years) |

| CO₂ Tolling and Low Emission Zones Impact | +0.7% | London, Paris, Amsterdam | Medium term (2-4 years) |

| App-Based Micro Rentals Rise | +0.6% | Berlin, Paris, Madrid | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce-Driven Last-Mile Delivery

The rise of e-commerce across Europe is reshaping logistics strategies. Providers are adopting flexible solutions to manage fluctuating demand. Short-notice van rentals, for instance, help logistics companies handle seasonal peaks without long-term fleet investments that risk depreciation. This trend is evident with major players like Amazon, whose same-day delivery services have raised expectations for speed and reliability. Logistics firms, such as DHL Express, have increased rental van usage, reflecting the industry's shift toward more agile delivery models. These changes highlight the evolving retail logistics landscape, where adaptability and responsiveness are key competitive advantages[1]“Operational Review 2024,”, DHL Express, Dhl.com. Retailers outside the logistics sphere, including Zara and H&M, also utilize rental pools to fulfill direct-to-consumer orders. The European van rental market yields immediate scalability for carriers operating inside crowded urban hubs where depot space is scarce. High-density delivery routes further reinforce the demand for cargo vans equipped with telematics that enhance route accuracy and reduce idle time.

Corporate ESG Targets Pushing Electric-Van Leasing

Large multinationals, such as Unilever and Nestlé, require logistics vendors to curb Scope 3 emissions, triggering a fresh demand for electric van capacity [2]“Supply Chain Climate Roadmap,”, Unilever, Unilever.com. Corporate procurement teams favor rentals that deliver zero-tailpipe transport without locking balance sheets into vehicle purchases. Fleet electrification is hindered by 8-12 month lead times for new e-vans, yet rental operators secure priority allocations via frame agreements with manufacturers like Mercedes-Benz. Northern European markets provide extra impetus through carbon taxes and green public procurement rules, making electric vans a compliance must-have rather than a public-relations choice.

SME Cap-Ex Avoidance Via Flexible Rentals

Europe saw an 8.3% rise in new commercial van registrations in 2024, straining SME budgets [3]“European Vehicle Market Report 2024,”, European Automobile Manufacturers’ Association, Acea.auto. Ever-higher borrowing costs intensify scrutiny of asset purchases, nudging small firms toward the European van rental market for pay-as-you-go mobility that preserves cash flow. Project-driven sectors, such as construction, favor rentals that match contract durations, and expanded pay-per-use contracts provide the granularity needed to right-size fleets every week. Embedded maintenance and insurance simplify back-office burdens, and rental portals now offer dynamic pricing that drops idle-day charges, improving transparency and uptake among cost-sensitive operators.

Tourism Rebound Boosting Passenger Van Demand

Spain's tourism industry, having set records for international visitor numbers, is reshaping how leisure travelers approach mobility. Tourists in groups are increasingly turning to multi-seat passenger vans, particularly for scenic coastal drives and outdoor adventures. They prefer these vans for their spacious cabins, which comfortably fit both passengers and their gear. This shift not only streamlines bookings—reducing the need for multiple vehicles—but also reduces travel costs per person. In response to this growing trend, leading tour operators such as TUI have expanded their van fleets. The van rental market across Europe is riding the wave of a broader experiential travel movement. Regions such as Provence and the French Alps are witnessing a surge in van rentals, especially for camping and nature-centric trips. For rental companies, incorporating passenger vans into their fleet is a strategic move. It allows them to diversify from the fiercely competitive small-car market and cater to the growing demand for flexible, group-oriented travel experiences.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV Van Costs | −1.4% | Northern Europe | Medium term (2-4 years) |

| Driver Shortage Worsens | −0.8% | Germany, United Kingdom, France | Short term (≤ 2 years) |

| Diesel Van Tax Incoming | −0.7% | Netherlands and potential adopters | Short term (≤ 2 years) |

| Cross-Border License Gaps | −0.5% | EU wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-Front Cost / Limited Supply of Electric Vans

Despite mounting regulatory pressures and environmental incentives, Europe's rental market is facing challenges in its transition to electric vans. Electric models, still pricier than their diesel counterparts, face hurdles like extended delivery wait times. These delays stem from constraints in battery supply, shortages in semiconductors, and a sparse charging infrastructure, all of which hinder fleet renewals. Moreover, rising insurance premiums further escalate the total cost of ownership, making electric vans a less appealing choice for rental operators. These operators also face additional challenges, including investing in depot charging stations and training drivers for electric vehicle operations. While declining battery prices are slowly bridging the cost divide, ongoing availability issues are stalling the pace of electric van adoption, falling short of policymakers' projections. Consequently, the electrification trajectory for Europe's van rental sector is lagging behind expectations, underscoring the need for synchronized efforts in the manufacturing, infrastructure, and policy realms to accelerate this transition.

Cross-Border Licensing Age Inconsistencies

Member-state rules set driver minimum ages between 18 and 21, forcing rental systems to embed complex eligibility checks that frustrate cross-border users. Younger drivers relocating for work face confined operating rights, shrinking the talent pool. Insurance underwriters overlay stricter age limits, compounding the restriction. EU efforts to harmonize standards under the Professional Driver Qualification Directive will take years to implement, leaving near-term friction intact and adding admin overhead to the European van rental market.

Segment Analysis

By Van Type: Cargo Dominance Amid Passenger Revival

Cargo vans accounted for 70.61% of 2024 revenue, representing the largest share of the European van rental market. Demand stems from last-mile shippers, such as Amazon and Zalando, which treat rentals as elastic delivery capacity. Cargo units equipped with live telematics enable route optimization, enhancing uptime and reducing per-drop costs. Meanwhile, passenger vans are projected to post the strongest growth, at a 5.98% CAGR, through 2030, tied to the resurgence of tourism and group travel preferences. Indie Campers confirmed a 34% rise in passenger van bookings across Mediterranean countries in 2024, a trend driven by family trips and outdoor pursuits. Cargo’s scale advantage is unlikely to fade; yet, the elevated growth pace of passenger models adds diversity and enhances seasonal balancing within the European van rental market.

Passenger demand also benefits corporate shuttle contracts and airport transfers, although the scarcity of professional drivers limits the availability of fully serviced offerings. Operators counteract the shortage by expanding self-drive packages, which are supported by mobile check-in and insurance bundles. For cargo fleets, electrification looms large; the expansion of Low Emission Zones nudges Amazon’s delivery partners to switch to electric vans once supply permits. Early adopters enjoy premium rates and improved access to the city center, locking in a competitive edge.

By Rental Duration: Daily Rentals Lead While Long-Term Gains

Daily rentals accounted for 44.23% in 2024, reflecting short-cycle e-commerce peaks and tourist use cases that require flexible capacity. Promotions tied to weekend leisure drives and instant online confirmation keep daily hires top of mind. However, long-term leasing shows the fastest expansion at 6.07% CAGR through 2030 as corporations secure maintenance-inclusive contracts that flatten monthly outlays. Predictable cost lines align with operating expense budgets and support asset-light strategies. Hourly hires, facilitated by micro-duration apps, remain niche but rising inside dense cities, where parking scarcity and congestion charges deter personal van ownership. The European van rental market share for weekly and monthly agreements fills interim needs for construction projects and seasonal retail campaigns, balancing vehicle utilization for operators.

In revenue terms, daily hires still dominate due to their higher rate per day, but the margin structure on long-term leases is attractive because of lower vehicle churn. Operators deploy subscription models that blend fixed payments with mileage caps, appealing to SMEs seeking transparency. Electrification aligns well with long-term contracts, providing rental providers with ample time to recover higher capital costs through multi-year fees. At the same time, daily renters still favor diesel due to its lower upfront price.

By Application: Commercial Strength Meets Personal Growth

Commercial customers generated 59.29% of turnover in 2024, supported by logistics, utilities, and construction firms that need scalable transport without capital tie-up. The European van rental market size for commercial use is expanding in response to regulatory compliance needs, as environmental regulations prompt the adoption of fleet-as-a-service models that deliver ready-to-comply vehicles. Yet personal hires advance faster at 5.79% CAGR through 2030, propelled by holidaymakers and DIY movers using digital apps to spot nearby vans. Cargo-bike adoption and compact e-trucks offer partial alternatives, but van versatility remains a key factor in making the segment attractive.

Corporate sustainability agendas are driving commercial clients toward electric van options, although supply gaps and higher lease rates are moderating uptake. Personal renters are showing a growing awareness of urban emission rules, seeking LEZ-approved units for weekend shopping runs within city centers. Transparent fee structures and damage-waiver packages smooth uptake among first-time users.

By Booking Channel: Digital Transformation Accelerates

Online channels accounted for 60.33% of bookings in 2024 and are projected to grow 6.16% CAGR by 2030. Real-time inventory, instant payment, and QR-code vehicle unlock streamline the journey. Kiosk-free processes shrink wait times, fostering loyalty among time-pressed users. Mobile apps further enrich offers via add-on insurance and navigation bundles. Physical counters still matter for complex corporate contracts and oversized specialty vehicles, yet their share is eroding as even large buyers adopt self-serve portals that integrate approval workflows. The European van rental market benefits from reduced overhead when bookings migrate online, enabling sharper price competition and data-driven upselling.

Digitized bookings provide granular demand records, informing fleet allocation decisions by hour and postcode. Integration with telematics closes the loop, optimizing utilization and maintenance scheduling. Keyless technology also reduces lost-key incidents and simplifies vehicle turnover, thereby enhancing customer satisfaction and reviews.

By Customer Type: Corporate Leadership Amid Agency Growth

Corporate accounts held 42.43% of 2024 revenue, driven by national and cross-border contracts that bundle services, telematics, and insurance. Larger firms favor multi-year master agreements that lock in pricing and secure priority access during peak seasons. Travel agencies show the quickest climb at 6.28% CAGR as group itineraries regain traction and business travel resumes. Agencies embed vans into package deals covering lodging and activities, capturing value beyond the ride itself. Individual consumers maintain a consistent share, although their growth trails that of commercial categories due to the emergence of alternative mobility options. Government buyers represent a specialized but stable segment, often prioritizing electric or low-emission vans to meet public procurement targets.

Fleet-management companies partner with rental brands to provide turnkey mobility, blurring the line between leasing and renting. Such tie-ups expand the European van rental market’s corporate reach, while loyalty apps and volume rebates cement relationships.

Geography Analysis

Germany accounted for 25.19% of the European van rental market revenue in 2024. Industrial clusters in Bavaria, Baden-Württemberg, and North Rhine-Westphalia create steady cargo van rotations, while Low Emission Zones in Berlin, Hamburg, and Munich accelerate electric vehicle adoption despite supply shortages. Enterprise and Sixt each expand their warehouse charging hubs to maintain e-van uptime. Driver scarcity remains Germany’s critical pain point, lifting wage bills and compressing margins.

Spain posts a 6.11% CAGR through 2030, the highest among regional growth rates. International visitors surpassed pre-pandemic totals in 2024, and van tours in Andalusia and Catalonia experienced a sharp rise. Domestic logistics networks expand as online sales grow, utilizing rental vans to circumvent ownership costs. Madrid and Barcelona introduce LEZ extensions that incentivize the conversion to electric fleets, but infrastructure density remains uneven outside the principal corridors.

The United Kingdom, France, and Italy provide a stable scale. UK rental providers juggle post-Brexit cabotage rules and driver eligibility checks, yet home-delivery volumes offset cross-border friction. France combines robust domestic tourism with strong e-commerce adoption, with passenger van rentals supporting access to rural destinations. Italy’s north-south economic split yields mixed demand, with Milan’s logistics growth balancing southern leisure hires. Eastern European nations gain relevance as EU funds upgrade highways and logistics parks, unlocking new van traffic; yet, heterogeneous compliance standards demand agile operating models.

Competitive Landscape

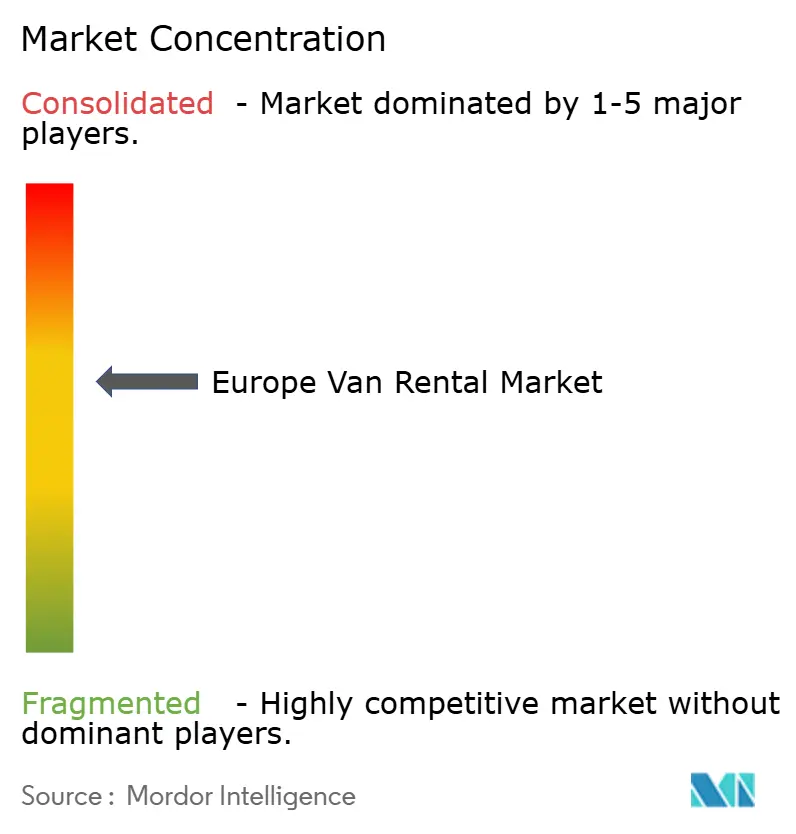

The European van rental market features moderate fragmentation. Sixt SE, Enterprise Holdings, and Europcar Mobility Group top the table, pursuing acquisitions to enlarge their footprint and secure OEM quotas for electric models. The European van rental market is expanding through acquisitions, electrification, and the introduction of new business models. Enterprise's acquisition of Europcar's commercial-van unit expanded its fleet and corporate mobility services. Sixt is investing in electrifying its vans, partnering with Mercedes-Benz and Ford. New entrants like MILES Mobility are disrupting urban markets with 30-minute micro-rentals, leveraging high vehicle density for strong utilization rates.

Technology drives efficiency and customer experience. Telematics enables predictive maintenance, while app-based integrations streamline operations. Peer-to-peer platforms like GoMore expand supply in Nordic countries, allowing private van rentals. Specialty vans, such as refrigerated and high-roof models, form a premium sub-segment with limited supply and higher profitability. Operators addressing regulatory differences, EV shortages, and driver availability gain a competitive edge. The market remains moderately concentrated, with the top five players accounting for just under half of the total revenue, leaving room for consolidation and innovation.

Europe Van Rental Industry Leaders

-

Europcar Mobility Group

-

Fraikin

-

Enterprise Holdings, Inc.

-

Avis Budget Group

-

SIXT SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Europcar UK has announced a significant expansion of its commercial vehicle fleet, introducing new Small, Short Wheelbase (SWB) and Long Wheelbase (LWB) vans. This expansion also includes a broader selection of electric short wheelbase models, catering to the increasing demand for sustainable and versatile transportation solutions.

- July 2025: Roadsurfer, a German outdoor mobility specialist, has secured a EUR 25 million venture debt deal from BBVA. This funding is set to bolster Roadsurfer's international expansion and expedite its growth in Europe and North America. The financing will enable the company to strengthen its position as a leading camper van rental platform, catering to the growing demand for outdoor travel experiences. Additionally, the investment aligns with BBVA's strategy to support innovative businesses with high growth potential.

Europe Van Rental Market Report Scope

The Europe Van Rental Market Report is Segmented by Van Type (Passenger Vans and Cargo Vans), Rental Duration (Hourly, Daily, Weekly, Monthly, and Long-Term Leasing), Application (Personal, and Commercial), Booking Channel (Online Platforms and Rental Counters), Customer Type (Individual Consumers, Corporate Clients, Travel Agencies, and Government and Institutional Users), and Geography (Germany, United Kindom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD)

| Passenger Vans |

| Cargo Vans |

| Hourly Rentals |

| Daily Rentals |

| Weekly Rentals |

| Monthly Rentals |

| Long-Term Leasing (12-24 m+) |

| Personal Application |

| Commercial Application |

| Online Platforms |

| Rental Counters |

| Individual Consumers |

| Corporate Clients |

| Travel Agencies |

| Government & Institutional Users |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Van Type | Passenger Vans |

| Cargo Vans | |

| By Rental Duration | Hourly Rentals |

| Daily Rentals | |

| Weekly Rentals | |

| Monthly Rentals | |

| Long-Term Leasing (12-24 m+) | |

| By Application | Personal Application |

| Commercial Application | |

| By Booking Channel | Online Platforms |

| Rental Counters | |

| By Customer Type | Individual Consumers |

| Corporate Clients | |

| Travel Agencies | |

| Government & Institutional Users | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the Europe van rental market by 2030?

The Europe van rental market is projected to reach USD 10.69 billion by 2030.

Which van type currently leads demand?

Cargo vans led with 70.61% share in 2024, anchored by e-commerce last-mile delivery.

Which country shows the highest growth rate?

Spain is expected to grow at a 6.11% CAGR through 2030, driven by tourism and e-commerce expansion.

How fast are online booking channels growing?

Online platforms are expanding at a 6.16% CAGR, already securing 60.33% of bookings in 2024.

What is the main challenge to electric van adoption?

High upfront cost and limited supply of electric models reduce near-term fleet electrification speed.

Page last updated on: