Europe Ultrasound Device Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

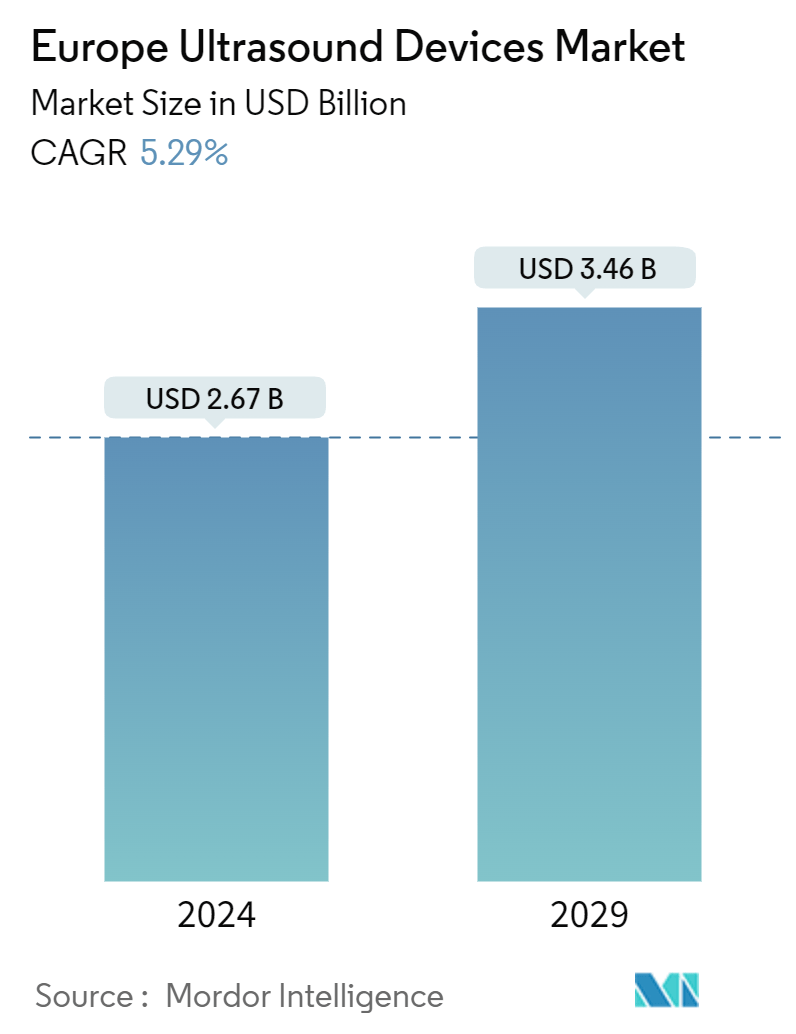

| Market Size (2024) | USD 2.67 Billion |

| Market Size (2029) | USD 3.46 Billion |

| CAGR (2024 - 2029) | 5.29 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe Ultrasound Device Market Analysis

The Europe Ultrasound Devices Market size is estimated at USD 2.67 billion in 2024, and is expected to reach USD 3.46 billion by 2029, at a CAGR of 5.29% during the forecast period (2024-2029).

The Europe Ultrasound Devices Market is witnessing significant growth, driven by essential megatrends like the increasing prevalence of chronic diseases, rapid technological advancements in Medical Imaging technologies, and a growing emphasis on early diagnosis and preventive healthcare. These megatrends, aligned with specific market drivers, are laying a solid foundation for sustained expansion in the sector.

Growing Burden of Chronic Diseases: The rising incidence of chronic diseases across Europe plays a crucial role in driving the ultrasound devices market. Diagnostic Ultrasound technology has become indispensable in diagnosing and managing chronic conditions, especially in fields like cardiology, oncology, and nephrology. For instance, the high prevalence of chronic kidney disease (CKD) in countries such as the United Kingdom and Germany is increasing demand for ultrasound devices, which are vital for assessing fibrosis and cirrhosis. The aging population in Europe further accelerates this demand, as older individuals are more susceptible to chronic diseases, requiring frequent Diagnostic Imaging.

Increased Adoption of Diagnostic Imaging: European healthcare systems are seeing a significant surge in the adoption of Diagnostic Imaging techniques, particularly ultrasound. The increasing awareness of early diagnosis and the non-invasive nature of Medical Ultrasound technology contribute to this trend. European governments and healthcare providers are heavily investing in advanced diagnostic centers, equipped with cutting-edge ultrasound systems. For instance, the United Kingdom's Community Diagnostic Centers (CDCs) and France's public hospital deployments of new radiology machines have made ultrasound technology more accessible, supporting early diagnosis in medical specialties like cardiology and obstetrics.

Technological Advancements: Technological innovations are pushing the ultrasound devices market forward. Advanced features such as 3D Ultrasound and 4D Ultrasound imaging, real-time computer imaging, and AI integration are improving the accuracy and efficiency of diagnoses. AI-enabled applications for prenatal care and liver disease diagnosis are being implemented across Europe. Furthermore, the introduction of Portable Ultrasound and Handheld Ultrasound devices expands the reach of diagnostic tools, making point-of-care diagnostics more versatile and accessible across different medical settings.

Focus on Women's Health: The gynecology/obstetrics segment is a significant driver in the European ultrasound devices market. The rising birth rates in countries like Germany, coupled with an increased focus on maternal and fetal health, are boosting demand for advanced ultrasound devices, including Obstetric Ultrasound equipment. Government support for routine prenatal ultrasound scans plays a major role in shaping the demand for ultrasound technology in women's health, making these devices integral to prenatal care and diagnostics.

Research and Development Initiatives: The market benefits from robust research and development activities, with collaborative initiatives driving innovation. European academic institutions, healthcare providers, and industry players are partnering to develop AI-based diagnostic tools that enhance ultrasound imaging capabilities. These innovations are expected to yield more specialized applications, further expanding the market's reach into new diagnostic areas such as liver disease management.

In summary, the Europe Ultrasound Devices Market is fueled by the rising burden of chronic diseases, growing adoption of Diagnostic Imaging, significant technological advancements, and research-driven innovations. These factors are collectively fostering a dynamic and accessible market that is integral to modern healthcare delivery in Europe.

Europe Ultrasound Device Market Trends

3D and 4D Ultrasound Imaging: Revolutionizing Diagnostic Capabilities

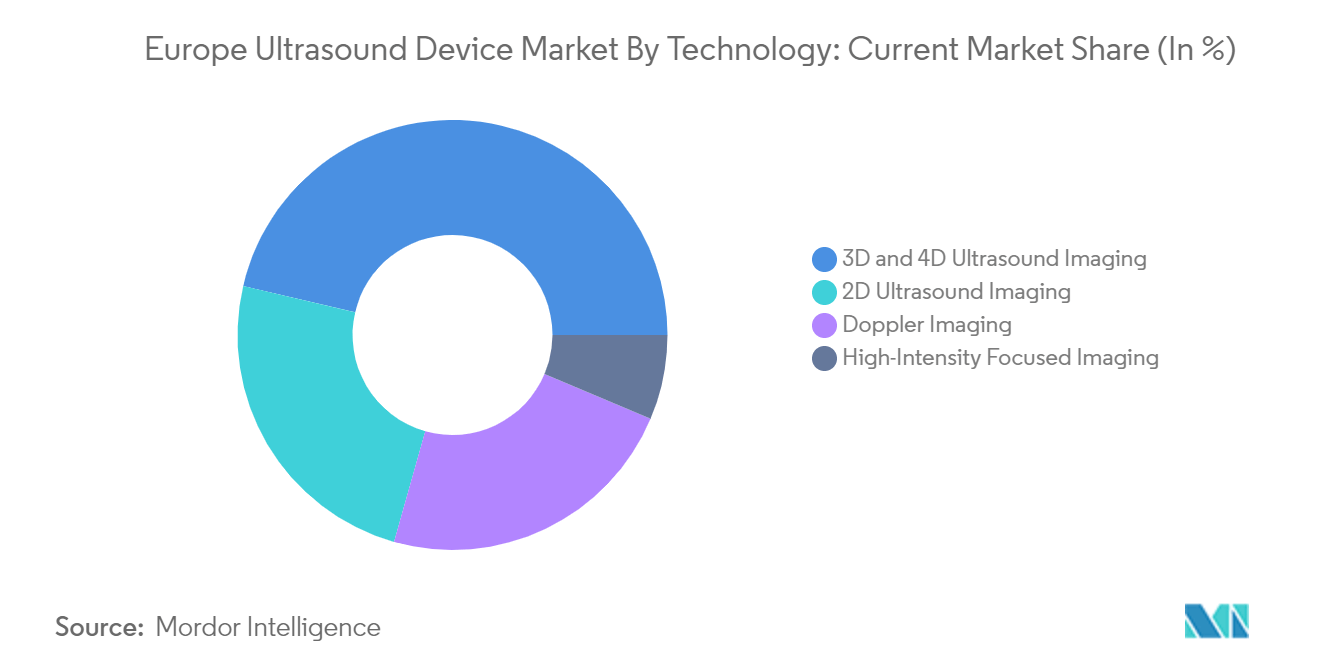

Segment Dominance: 3D and 4D Ultrasound imaging technology has become the cornerstone of the Europe Ultrasound Device Market, accounting for approximately 46% of the market size. This prominence is due to the enhanced visualization and detailed anatomical data these technologies offer, transforming diagnostic capabilities across various medical disciplines.

Driving Forces: The growth of 3D Vascular Ultrasound Imaging Market is driven by continuous improvements in imaging software and transducer technology. Adoption of these systems in specialties like obstetrics, cardiology, and oncology is rapidly increasing, as they enable non-invasive diagnostics. The rising prevalence of chronic diseases is also boosting demand for these advanced diagnostic tools, making them a key growth catalyst.

Competitive Landscape: Leading players are focusing on continuous innovation to maintain their edge. This includes developing AI-integrated systems that improve image quality and automate analysis. Companies are also enhancing operator efficiency by introducing user-friendly interfaces and ergonomic designs. As the market continues to evolve, AI-powered diagnostics and cross-modality imaging systems are expected to further enhance growth.

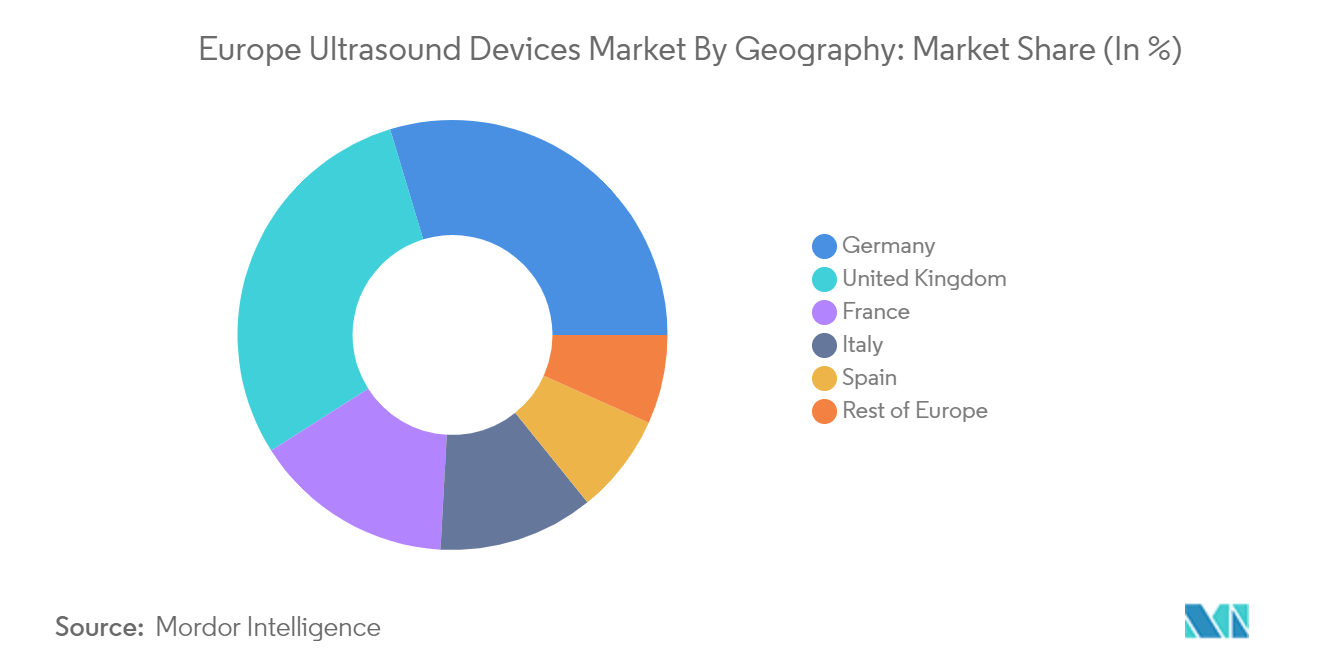

Germany: Leading the Charge in Ultrasound Device Adoption

Market Dynamics: Germany is emerging as the fastest-growing regional market in the Europe Ultrasound Devices sector, with a projected CAGR of 5.77% from 2024 to 2029. This is attributed to the country's robust healthcare infrastructure, high adoption rates of advanced medical technologies, and emphasis on early disease detection.

Growth Catalysts: The country's high birth rate—over 700,000 children born annually—drives demand for obstetric ultrasounds. Additionally, the increasing incidence of chronic diseases and governmental support for routine diagnostic tests are expanding the market. Germany's focus on technological innovation and its leadership in Medical Imaging research are also playing a significant role in shaping market dynamics.

Strategic Imperatives: To tap into the growth potential in Germany, companies are adopting localized strategies, such as forming partnerships with healthcare providers and research institutions. Manufacturers are tailoring their ultrasound products to regional healthcare needs, while staying attuned to regulatory changes and evolving reimbursement policies.

Europe Ultrasound Device Industry Overview

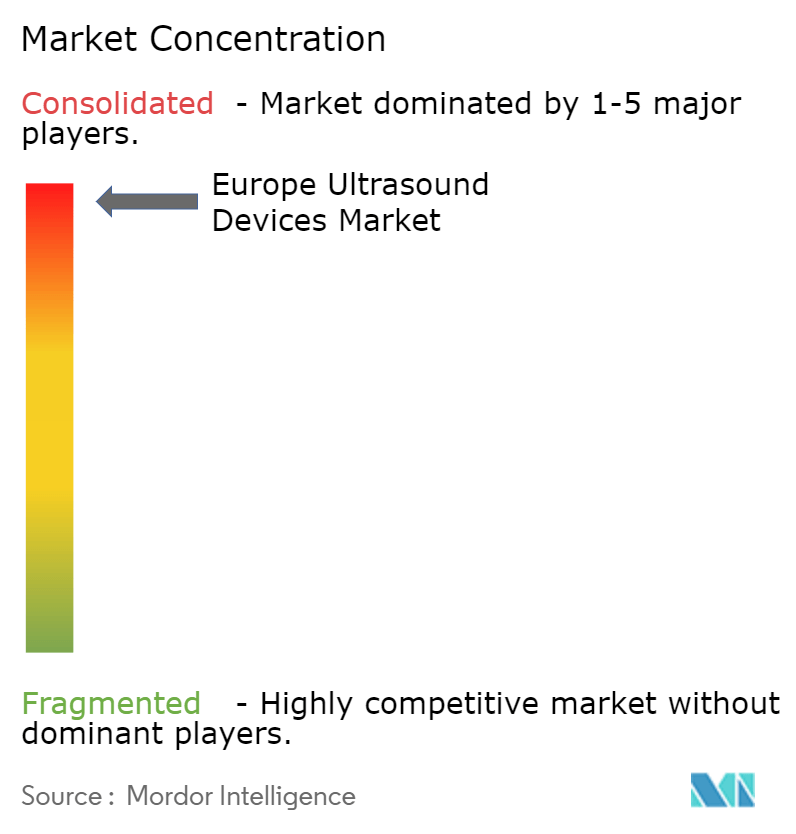

Global Players Dominate Consolidated Market

The Europe Ultrasound Devices Market is consolidated, with a few global players like GE Healthcare, Koninklijke Philips NV, Siemens Healthcare, and Esaote SpA holding dominant market positions. These companies leverage extensive R&D capabilities, broad product portfolios, and established distribution networks to maintain their leadership.

Innovation and Technological Prowess Drive Leadership

Market leaders invest heavily in R&D, with a strong focus on innovations like AI, imaging technology, and workflow optimization. Top players offer a diverse portfolio, covering 2D Ultrasound, 3D, and 4D Ultrasound systems, catering to a wide range of medical applications. Companies like Esaote SpA, with their advanced MyLab series, continue to lead the market by integrating features like iQView and XBeam for enhanced diagnostic precision.

Strategies for Future Market Success

To strengthen market share, companies must focus on continuous innovation, particularly in AI integration and point-of-care applications. Strategic collaborations with universities and healthcare providers, like Intelligent Ultrasound's partnership with the University of Dundee, will also be key to advancing AI-based diagnostics. Additionally, addressing regulatory challenges and investing in training programs to overcome skilled workforce shortages are critical strategies for future growth.

Europe Ultrasound Device Market Leaders

-

Esaote SpA

-

Fujifilm Holdings Corporation

-

GE Healthcare

-

Siemens Healthcare

-

Mindray Medical International Ltd.

*Disclaimer: Major Players sorted in no particular order

Europe Ultrasound Device Market News

- April 2024: Mobile ultrasound company Clarius Mobile Health partnered with AI ultrasound firm ThinkSono to launch ThinkSono Guidance, an AI-enabled application. It received Class IIb CE mark approval and is available in Europe and the UK.

- March 2024: Insighttec, based in Berlin, received NUB status 1 for its MR-guided focused ultrasound (MRgFUS) treatment of essential tremor in Germany, further expanding advanced ultrasound treatment availability.

Europe Ultrasound Device Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increased Adoption of Diagnostic Imaging

4.2.2 Growing Burden of Chronic Diseases

4.2.3 Technological Advancements

4.3 Market Restraints

4.3.1 Stringent Regulatory Reforms

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Application

5.1.1 Anesthesiology

5.1.2 Cardiology

5.1.3 Gynecology/Obstetrics

5.1.4 Musculoskeletal

5.1.5 Vascular

5.1.6 Other Applications

5.2 By Technology

5.2.1 2D Ultrasound Imaging

5.2.2 3D and 4D Ultrasound Imaging

5.2.3 Doppler Imaging

5.2.4 High-intensity Focused Ultrasound

5.3 By Type

5.3.1 Stationary Ultrasound

5.3.2 Portable Ultrasound

5.4 By End User

5.4.1 Hospitals

5.4.2 Diagnostic Centers

5.4.3 Other End Users

5.5 Geography

5.5.1 Germany

5.5.2 United Kingdom

5.5.3 France

5.5.4 Italy

5.5.5 Spain

5.5.6 Rest of Europe

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Esaote SpA

6.1.2 Fujifilm Holdings Corporation

6.1.3 GE Healthcare

6.1.4 Hitachi Medical Corporation

6.1.5 Philips Healthcare

6.1.6 Samsung

6.1.7 Siemens Healthcare

6.1.8 Canon Medical Systems Corporation

6.1.9 Mindray Medical International Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Europe Ultrasound Device Industry Segmentation

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. These devices are being utilized for the assessment of various conditions in the kidney, liver, and other abdominal conditions. They are also majorly used in chronic diseases, which include health conditions, such as heart disease, asthma, cancer, and diabetes. Therefore, these devices are being utilized as both diagnostic imaging and therapeutic modality, and have a wide range of applications in the medical field.

The Europe ultrasound devices market is segmented by application, technology, type, end user, and geography. By application, the market is segmented into anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, vascular and other applications. By technology, the market is segmented into 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging and high-intensity focused ultrasound. By type, the market is segmented into stationary ultrasound and portable ultrasound. By end user, the market is segmented into hospitals, diagnostic centers and other end users. By geography, the market is segmented into Germany, United Kingdom, France, Italy, Spain and Rest of Europe. The report offers the value (USD) for the above segments.

| By Application | |

| Anesthesiology | |

| Cardiology | |

| Gynecology/Obstetrics | |

| Musculoskeletal | |

| Vascular | |

| Other Applications |

| By Technology | |

| 2D Ultrasound Imaging | |

| 3D and 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-intensity Focused Ultrasound |

| By Type | |

| Stationary Ultrasound | |

| Portable Ultrasound |

| By End User | |

| Hospitals | |

| Diagnostic Centers | |

| Other End Users |

| Geography | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Europe Ultrasound Device Market Research FAQs

How big is the Europe Ultrasound Devices Market?

The Europe Ultrasound Devices Market size is expected to reach USD 2.67 billion in 2024 and grow at a CAGR of 5.29% to reach USD 3.46 billion by 2029.

What is the current Europe Ultrasound Devices Market size?

In 2024, the Europe Ultrasound Devices Market size is expected to reach USD 2.67 billion.

Who are the key players in Europe Ultrasound Devices Market?

Esaote SpA, Fujifilm Holdings Corporation, GE Healthcare, Siemens Healthcare and Mindray Medical International Ltd. are the major companies operating in the Europe Ultrasound Devices Market.

What years does this Europe Ultrasound Devices Market cover, and what was the market size in 2023?

In 2023, the Europe Ultrasound Devices Market size was estimated at USD 2.53 billion. The report covers the Europe Ultrasound Devices Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Europe Ultrasound Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe Ultrasound Device Industry Report

Statistics for the 2024 Europe Ultrasound Device market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe Ultrasound Device analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Europe Ultrasound Device Market Report Snapshots