Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

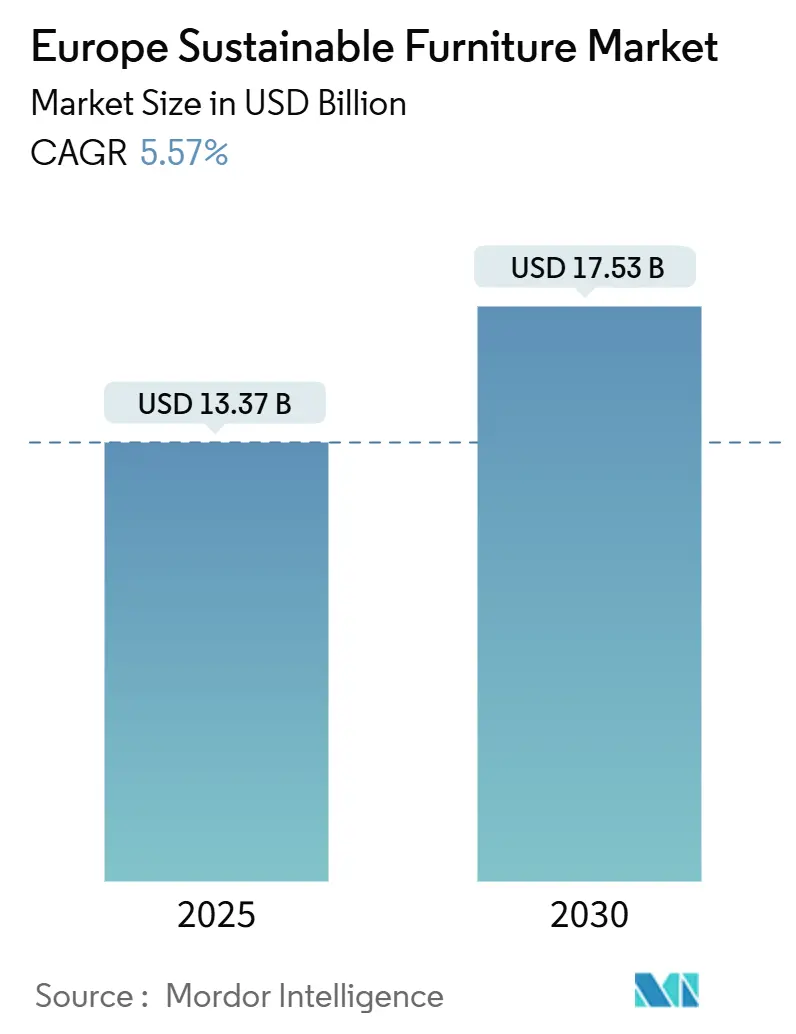

| Market Size (2025) | USD 13.37 Billion |

| Market Size (2030) | USD 17.53 Billion |

| Growth Rate (2025 - 2030) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sustainable Furniture Market Analysis by Mordor Intelligence

Europe sustainable furniture market size reached USD 13.37 billion in 2025 and is forecast to advance to USD 17.53 billion by 2030, translating into a 5.57% CAGR over the period. Market momentum stems from EU-wide circular-economy legislation, rising corporate ESG mandates, and consumer willingness to pay for certified low-VOC products. Regulatory shifts have converted sustainability from a differentiator into a de facto license to operate, prompting incumbents and start-ups alike to invest in material traceability, repairability, and take-back systems. Demand has broadened beyond eco-niche buyers to mainstream residential and commercial customers, with furniture-as-a-service (FaaS) subscriptions accelerating digital penetration and boosting the secondary-market value of certified assets. Competitive intensity is migrating toward end-of-life services, digital product passports, and innovative bio-based materials that reduce embodied carbon and improve recyclability[1]Source: European Commission, “Ecodesign for Sustainable Products Regulation,” ec.europa.eu .

Key Report Takeaways

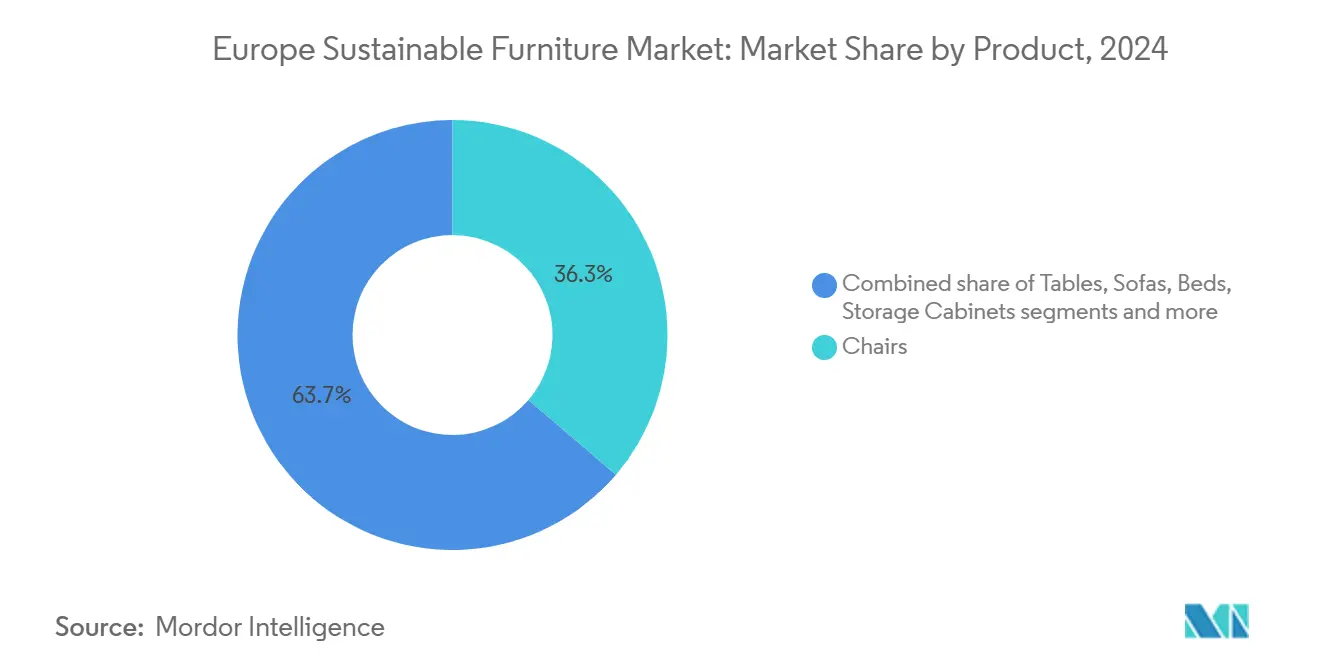

- By product, chairs held 36.25% of Europe sustainable furniture market share in 2024, while beds are set to expand at a 7.10% CAGR through 2030.

- By material, reclaimed and FSC-certified wood commanded a 31.84% share of Europe sustainable furniture market size in 2024, whereas recycled and bio-based plastics will grow at a 6.71% CAGR to 2030.

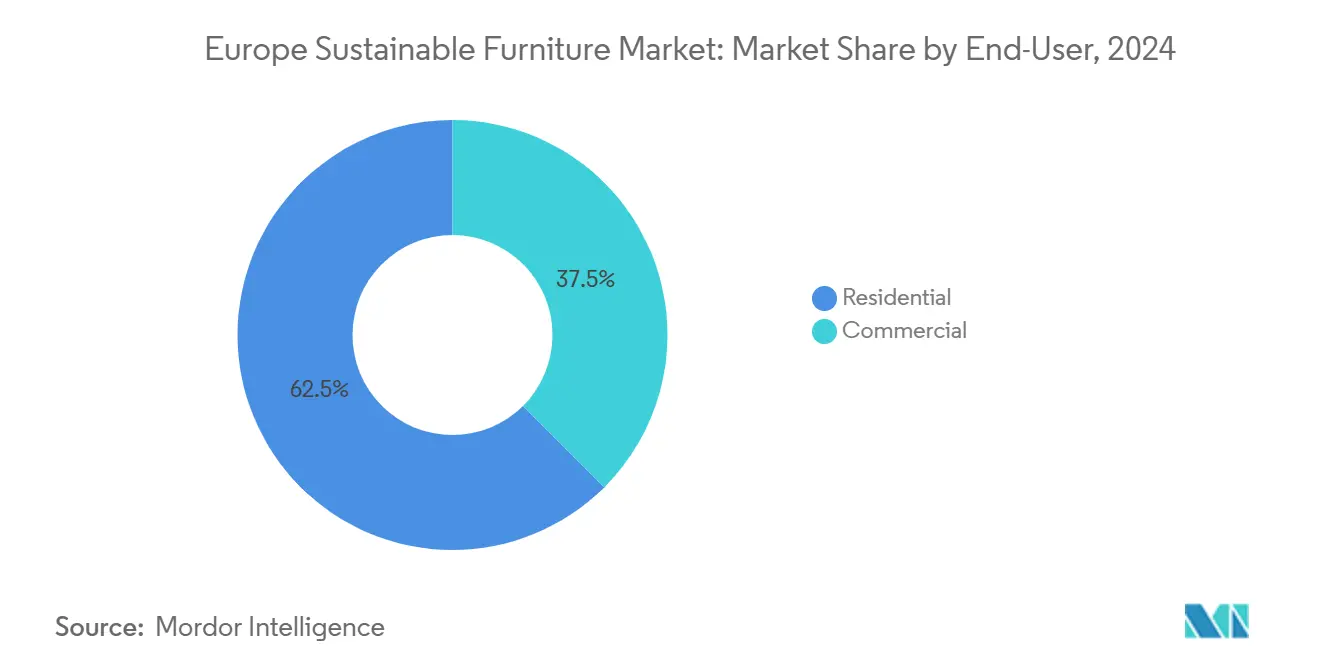

- By end-user, the residential segment controlled 62.46% share of Europe sustainable furniture market size in 2024, but commercial applications are rising at a 6.26% CAGR through 2030.

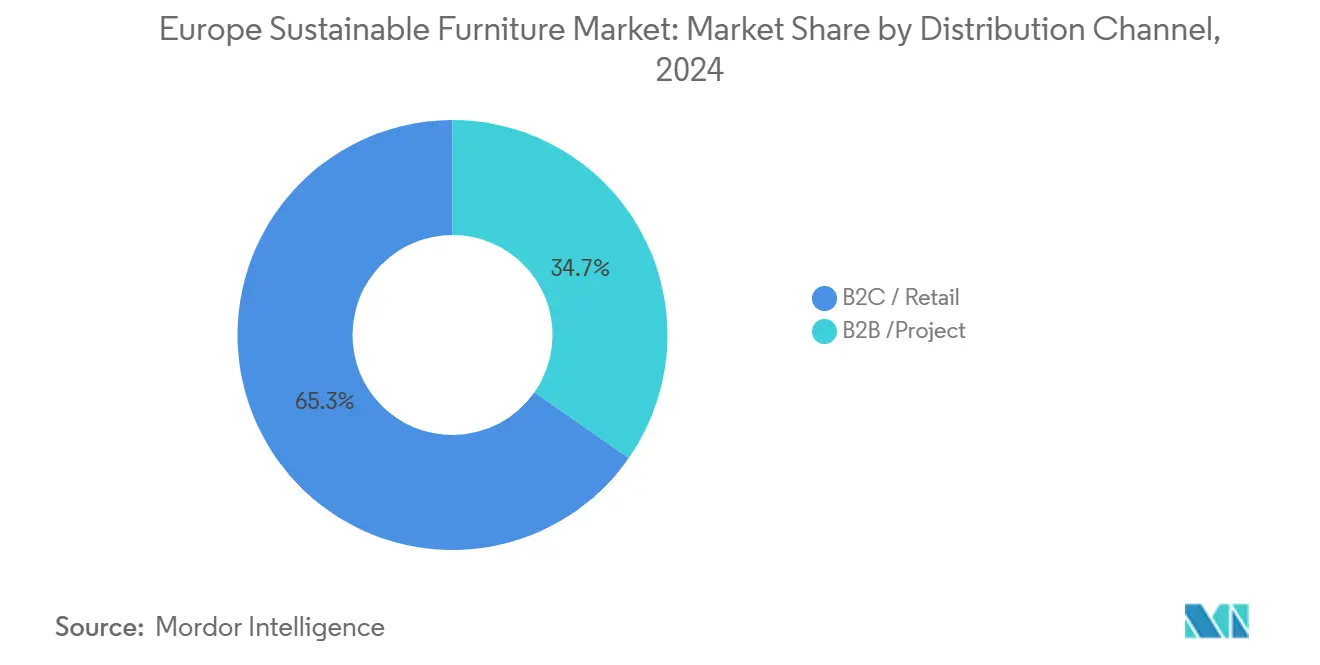

- By distribution channel, the B2C/retail segment held 65.31% of Europe sustainable furniture market share in 2024. Within B2C/retail, the online segment is set to expand to a 7.25% CAGR through 2030.

- By geography, Germany led with an 18.43% revenue share in 2024; the Nordics region is forecast to post the fastest 7.83% CAGR to 2030.

Europe Sustainable Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Ecodesign & Circular-Economy Legislation | +1.2% | EU-wide; strongest in Germany, France, the Nordics | Medium term (2–4 years) |

| Certified Sustainable Wood & Low-VOC Materials | +0.9% | Western Europe | Short term (≤2 years) |

| Green Building Projects & LEED/BREEAM Uptake | +0.8% | UK, Germany, Netherlands, Nordics | Medium term (2–4 years) |

| Furniture-as-a-Service Expansion | +0.7% | Urban EU, led by Nordics, BENELUX | Long term (≥4 years) |

| Advances in Bio-based Adhesives & Finishes | +0.6% | Germany, Italy, Poland | Medium term (2–4 years) |

| Digital Product Passports | +0.5% | EU-wide, early adoption in Germany | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EU Ecodesign & Circular-Economy Legislation Implementation (2025-2030)

The ESPR officially prioritized furniture on July 18, 2024, mandating material circularity, reparability, and recyclability. Draft delegated acts due 2025-2027 will make digital product passports obligatory, compelling transparent disclosure of material origin, carbon footprint, and end-of-life pathways. Vertically integrated groups able to track inputs from forest to factory gain a compliance edge, while legacy manufacturers reliant on opaque imports face 3-5% cost inflation for data gathering and design redesigns. Modular construction tailored for component replacement dovetails with FaaS contracts in which producers keep ownership and handle maintenance. Early adopters that internalize regulatory costs now are positioned to build durable competitive moats.

Rising Consumer Demand for Certified Sustainable Wood & Low-VOC Materials

European households are willing to pay a premium for eco-certified furniture and consider sustainable living essential. FSC labels have therefore shifted from marketing claim to purchase prerequisite in Germany, Denmark, and France. Manufacturers are now compelled to invest in supply chain verification systems as material transparency shifts from being a mere marketing differentiator to a key purchasing criterion. Vendors have responded by digitizing chain-of-custody records and expanding low-formaldehyde product lines, especially in the bedroom, where sleep wellness is paramount. Premiums remain 15-30% above conventional offers, yet improved durability and lower off-gassing reinforce value perceptions over lifetime ownership[2]Source: Forest Stewardship Council, “Global Certification Data,” fsc.org.

Rapid Expansion of Green Building Projects & LEED/BREEAM Certifications

Institutional buyers increasingly bake furniture criteria into tenders as they chase certification points. Ireland’s Green Public Procurement Strategy, for example, requires environmental attributes in all state furniture bids by 2027. Builders now demand Environmental Product Declarations (EPDs) for desks, chairs, and storage systems to address whole-building Global Warming Potential calculations. Suppliers providing turnkey EPD packs plus take-back services enjoy preferred-vendor status. Growth is steepest in the UK retrofit market, where landlords refurbish aging stock to meet Minimum Energy Efficiency Standards.

Growth of Furniture-as-a-Service Subscription Models Supporting Re-use

FaaS providers such as NORNORM logged 50% year-on-year growth in leased square meters during 2024, reinforced by a EUR 110 million (USD 114.5 million) funding round backed by the European Investment Fund. Corporate tenants value the opex model for cash-flow smoothing and rapid layout changes. They can sidestep hefty upfront furniture costs while enjoying the flexibility to reconfigure their spaces. Because ownership remains with the vendor, products are engineered for multiple life cycles, lowering waste and embedding circular principles[3]Source: NORNORM, “EIF-Backed Financing Press Release,” nornorm.com. European waste statistics reveal that 11 million tonnes of furniture end up in landfills each year, with a mere 3% being recycled. This underscores the potential of circular economy initiatives, particularly those championed by FaaS models.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Up-front Costs vs. Conventional Furniture | -0.8% | Eastern & Southern Europe | Short term (≤2 years) |

| Supply-Chain Complexity for Certified Materials | -0.6% | Import-dependent markets | Medium term (2–4 years) |

| Fragmented Sustainability Standards Across EU States | -0.4% | Multinational manufacturers | Medium term (2–4 years) |

| Insufficient Reverse-Logistics Infrastructure | -0.3% | Rural EU regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Higher Up-front Costs vs. Conventional Furniture

Despite consumers expressing a preference for sustainability, sustainable furniture often comes with a 15-30% price premium compared to conventional options, creating a barrier to adoption. This price hike is largely due to the costs associated with certified materials, third-party verifications, and the complexities of circular design. Such pricing challenges are especially pronounced in price-sensitive segments, notably in residential markets where decisions are predominantly driven by cost, even amidst a growing awareness of sustainability. Yet, models like furniture-as-a-service are addressing these upfront cost concerns. By allowing expenses to be spread over subscription periods, companies like NORNORM have seen corporate clients embrace their premium offerings.

Supply-Chain Complexity in Sourcing Certified Materials

Certified inputs such as FSC timber often come from a handful of specialized mills, so even modest shifts in demand can trigger bottlenecks and sudden price swings that upend production schedules. Access is uneven across the continent; Nordic factories enjoy local certified logs, while plants in Spain or Italy must import wood and absorb extra freight and currency risks. Manufacturers juggling several eco-labels for wood, fabrics, and finishes find that each audit cycle adds paperwork, supplier vetting, and costly safety stock to avoid line stoppages. Progress on bio-based glues is encouraging, yet many promising formulas, such as brown-algae or soy-protein resins, remain stuck at pilot scale, limiting commercial volumes and driving up costs for early adopters. The EU’s new Ecodesign rules will further raise the bar, requiring every tier of the supply chain to prove material provenance and processing steps, a task that small and midsize firms may find especially daunting.

Segment Analysis

By Product: Chairs Sustain Leadership while Beds Accelerate

Chairs generated 36.25% of Europe sustainable furniture market share in 2024, reflecting ergonomic upgrades in hybrid workplaces and institution tenders specifying FSC timber frames. Average selling prices climbed 4.2% as buyers prioritized height-adjustable and repairable designs. Over the forecast, beds record the quickest 7.10% CAGR, helped by sleep-wellness spending and stricter formaldehyde limits in bedroom air standards. Europe sustainable furniture market size for beds is projected to climb from USD 2.03 billion in 2025 to USD 2.86 billion by 2030, backed by organic mattress cores and certified wood slats. Tables and storage units log steady mid-single-digit growth on the back of home-organization trends, while outdoor lines are experimenting with recycled aluminum frames to lower embodied carbon.

Product innovators stress modularity: snap-fit components simplify repair and enable FaaS operators to refresh worn parts rather than replace units. Chair makers incorporate ocean-bound plastics in seat shells, and bed firms introduce bolt-less joinery for tool-free assembly. Mass-market retailers bundle repair kits and extend warranties to signal durability. As ESPR right-to-repair provisions crystallize, SKUs with component access points should outperform, reinforcing the leadership of brands already running circular design audits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Recycled & Bio-based Plastics Outpace Certified Wood Growth

Reclaimed and FSC wood kept a 31.84% revenue lead in 2024, yet recycled and bio-based plastics will deliver a 6.71% CAGR through 2030 as polymer-recycling plants mature. Europe sustainable furniture market size tied to recycled plastics is forecast to move from USD 1.87 billion in 2025 to USD 2.59 billion in 2030, supported by design freedom and color stability. Ocean-bound resin programs feed office-chair shells, while bio-PU foams derived from castor oil enter soft seating. Supply risk is lower because recycling infrastructure for PET and PP has been scaled under EU packaging rules.

Wood remains indispensable for aesthetic appeal and carbon-sequestration narratives, yet manufacturers diversify into bamboo and agrifiber panels to hedge cost swings. Recycled steel and aluminum see demand from architects targeting net-zero buildings, leveraging infinite recyclability. Adhesive innovations allow clean debonding of multi-material assemblies, raising recovery rates. Material choices increasingly factor into EPD scores as developers target embodied-carbon caps set by national building codes.

By End-User: Commercial Purchases Gain Pace on ESG Mandates

Residential buyers accounted for 62.46% of 2024 sales, reflecting pandemic-era home-office upgrades and lifestyle alignment. However, commercial clients will outgrow them at a 6.26% CAGR to 2030 because corporations face ESG scorecard scrutiny and seek LEED points. Europe sustainable furniture market size for offices alone is expected to reach USD 4.41 billion by 2030. FaaS meets corporate demand for adaptability amid fluctuating occupancy, while hospitals and schools pursue antimicrobial, low-VOC furnishings that support wellness ratings.

Procurement teams now run lifecycle cost analyses that favor durable goods with buy-back clauses, shifting contracts from capex to service subscriptions. Hospitality groups refresh guest rooms on shorter cycles and thus value refurbishment programs that minimize landfill. Public-sector agencies increasingly bundle furniture with building retrofits to satisfy national climate targets, giving certified suppliers queue-jump privileges.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Acceleration Reshapes B2C

B2C retail stayed dominant at 65.31% of 2024 turnover, but e-commerce within that channel is expanding 7.25% annually as consumers research eco-labels online and appreciate direct-to-door delivery of flat-pack goods. Click-through rates improve when listings show carbon scores and digital product passports. Europe sustainable furniture market size arising from online sales is forecast to break USD 3.06 billion by 2030. Traditional showrooms answer with VR visualization and in-store repair demos. Home centers carve out “circular corners” where shoppers can trade in outdated pieces.

B2B project integrators bundle furniture with acoustic panels and carpets under holistic fit-out contracts. They demand single-window accountability and KPI reporting, pressuring manufacturers to aggregate environmental data across multivendor bills of materials. QR-code scanning at site handover increasingly verifies compliance. Hybrid distributors marrying online configurators with local refurb hubs are capturing both transparency and service proximity advantages.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany captured 18.43% of 2024 revenue, driven by rigorous indoor-air regulations and the country’s leadership in engineered-wood production. Builders and corporate occupiers view FSC and EPD documentation as default bid criteria, enabling premium pricing. Digital passport pilot consortia in Bavaria illustrate early alignment with ESPR transparency. Growth is steady rather than explosive, reflecting market maturity and saturation of green-office retrofits.

The Nordics will post the swiftest 7.83% CAGR through 2030 on the back of high disposable income, cultural environmentalism, and abundant certified forestry resources. Denmark’s FaaS penetration already exceeds 8% of new office installations, and Sweden’s tax incentives for repair services reduce lifecycle costs. Municipal waste systems recover over 60% of bulky furniture, feeding industrial material loops. Nordic design’s minimalist ethos aligns with lower-material-intensity strategies.

France, Italy, Spain, BENELUX, and the UK form a diversified tier. France enforces the AGEC anti-waste law that extends producer responsibility to furniture, triggering investments in take-back logistics. Italy’s design houses merge artisanal craftsmanship with bio-based innovation to sustain export premiums. The UK post-Brexit is crafting its own eco-design rules, fostering start-ups unchecked by EU red tape. BENELUX’s dense urbanization supports FaaS pilot clusters linking Amsterdam, Brussels, and Luxembourg. Central and Eastern Europe remain cost-sensitive yet will gradually harmonize under ESPR enforcement, unlocking delayed demand in Poland and the Baltics.

Competitive Landscape

The arena is fragmented. IKEA, Steelcase, Herman Miller, and Haworth are leaving room for regional specialists and FaaS disruptors. IKEA earmarked EUR 1 billion (USD 1.04 billion) in 2025 for European recycling hubs, signaling a pivot from volume to circular retention. MillerKnoll eliminated PFAS across all lines by December 2024, pre-empting chemical bans. Steelcase partners with BASF on ocean-plastic seat shells, while Vestre runs carbon-negative outdoor furniture factories powered by hydro.

NORNORM and Enky champion subscription furniture, targeting tenant flexibility and lower embodied emissions. Both deploy IoT tags for asset monitoring and predictive maintenance, ensuring ≥5 life cycles per item. Regional carpentry houses in Portugal and Slovenia differentiate through locally sourced cork and beech while leveraging EU digital platforms to reach urban buyers. Competitive parity increasingly hinges on verified transparency; blockchain-backed passports and AI-based lifecycle scoring tools are replacing glossy catalogs.

Supply security is another battleground. Multinationals purchase forest concessions in Finland and Latvia to lock up FSC feedstock, whereas start-ups experiment with mycelium-based panels grown in-house. Cost advantage alone no longer assures sales; buyers demand demonstrable CO₂ reductions, toxic-chemical elimination, and convenient take-back. As ESPR enforcement tightens post-2027, players without end-of-life pathways risk losing tender eligibility, accelerating consolidation around circular-capable brands.

Europe Sustainable Furniture Industry Leaders

-

IKEA Group

-

Vitra International AG

-

Steelcase Inc.

-

Herman Miller Inc.

-

Haworth Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Henkel Adhesive Technologies earned USDA BioPreferred labels on three adhesive ranges containing up to 53% biobased content, offering sustainable bonding alternatives for manufacturers.

- January 2025: XXXLutz acquired 140 stores across Germany, the Czech Republic, and Slovakia, expanding its regional footprint and unlocking scale for circular-economy rollouts.

- July 2024: NORNORM secured debt financing from Santander CIB, guaranteed by the European Investment Fund, to scale FaaS across the UK, France, and Germany.

- May 2024: Fiberwood raised EUR 7.7 million (USD 8 million) to commercialize fossil-free insulation and packaging made from forestry side streams.

Europe Sustainable Furniture Market Report Scope

Sustainable furniture, is an emerging concept, and largely includes furniture made from eco-friendly or recycled materials that are sustainably sourced. Some of the prevalent raw materials used for green furniture include recycled textiles, oak, birch, hemp, wood, and bamboo. A complete analysis of the Europe Sustainable Furniture Market, which includes an assessment of the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report. The Europe Sustainable Furniture Market is segmented By Application (Residential and Commercial), By Material (Wood, Bamboo, PET, Others), By Distribution Channel (Online and Offline), By Country (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe).

By Product

| Chairs |

| Tables |

| Sofas |

| Beds |

| Storage Cabinets |

| Other Products |

By Material

| Reclaimed / FSC-Certified Wood |

| Bamboo & Rapidly Renewable Grass |

| Recycled Metals (Steel & Aluminum) |

| Recycled & Bio-Based Plastics |

| Organic / Natural Fibers (Rattan, Jute, Hemp) |

| Other Materials (parawood, rubberwood, natural fabrics, etc.) |

By End-User

| Residential | |

| Commercial | Offices |

| Hospitality | |

| Healthcare Facilities | |

| Educational Institutes | |

| Other Commercial Users (public places, retail malls, government offices, etc.) |

By Distribution Channel

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B /Project |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product | Chairs | |

| Tables | ||

| Sofas | ||

| Beds | ||

| Storage Cabinets | ||

| Other Products | ||

| By Material | Reclaimed / FSC-Certified Wood | |

| Bamboo & Rapidly Renewable Grass | ||

| Recycled Metals (Steel & Aluminum) | ||

| Recycled & Bio-Based Plastics | ||

| Organic / Natural Fibers (Rattan, Jute, Hemp) | ||

| Other Materials (parawood, rubberwood, natural fabrics, etc.) | ||

| By End-User | Residential | |

| Commercial | Offices | |

| Hospitality | ||

| Healthcare Facilities | ||

| Educational Institutes | ||

| Other Commercial Users (public places, retail malls, government offices, etc.) | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B /Project | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe sustainable furniture market?

The market stands at USD 13.37 billion in 2025.

How fast is the market expected to grow?

It is projected to register a 5.57% CAGR and reach USD 17.53 billion by 2030.

Which product category leads in revenue?

Chairs lead with a 36.25% share of Europe sustainable furniture market size in 2024.

Why are the Nordics growing the fastest?

Comprehensive circular-economy policies, high disposable income, and robust reverse-logistics systems are driving a 7.83% CAGR.

What business model is reshaping procurement?

Furniture-as-a-Service subscriptions are gaining traction, offering flexibility and circular benefits to corporate clients.

Which material segment is expanding the quickest?

Recycled and bio-based plastics are forecast to grow at a 6.71% CAGR through 2030.

Page last updated on: