Europe Sports Team And Clubs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

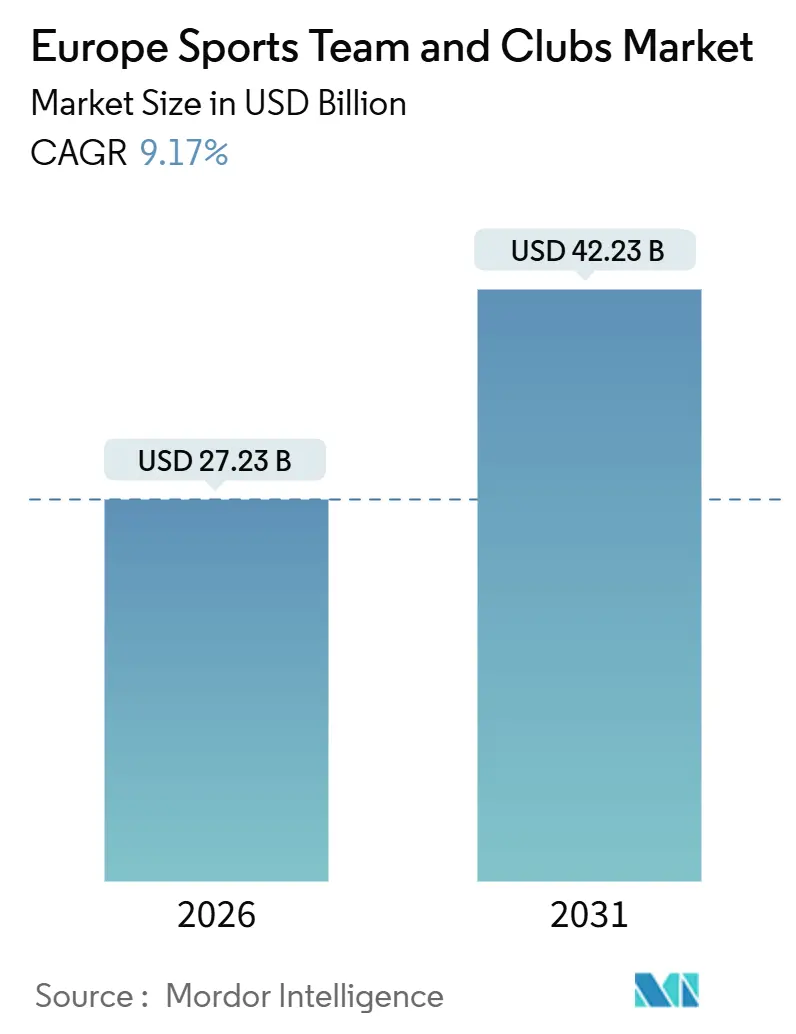

| Market Size (2026) | USD 27.23 Billion |

| Market Size (2031) | USD 42.23 Billion |

| Growth Rate (2026 - 2031) | 9.17% CAGR |

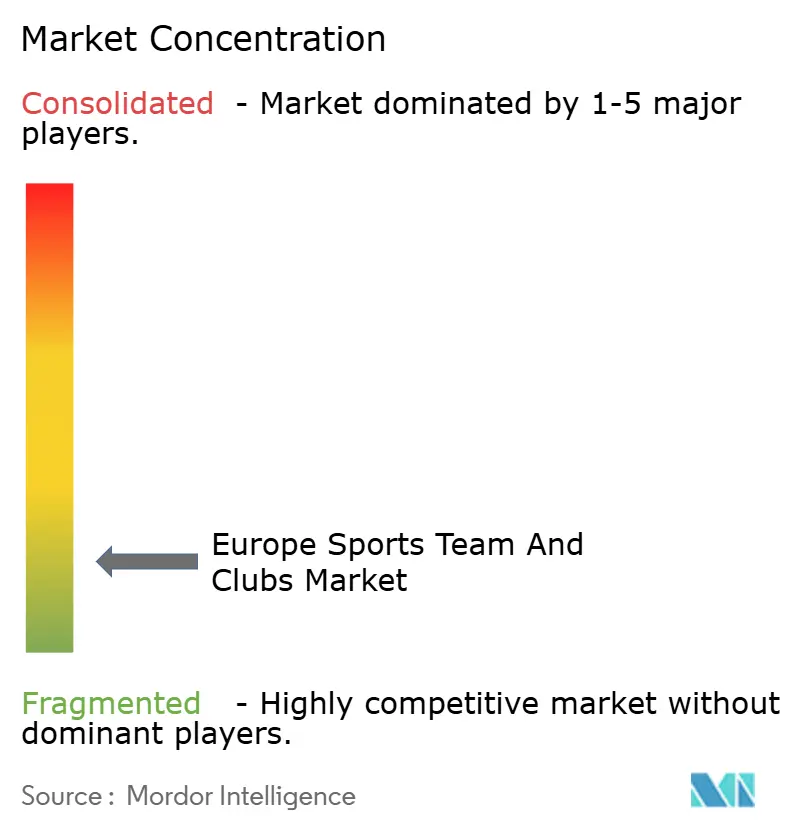

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sports Team And Clubs Market Analysis by Mordor Intelligence

The Europe sports team and club market size is USD 27.23 billion in 2026 and is projected to reach USD 42.23 billion by 2031, registering a 9.17% CAGR. The European sports team and club market is experiencing significant growth driven by structural transformation rather than cyclical recovery. Top clubs are shifting focus from expanding volume to optimizing profitability and efficiency. Media rights inflation, fueled by competition among streaming platforms, is enhancing clubs’ pricing power. Financial regulations, such as squad cost controls, are encouraging more disciplined spending and strategic commercial planning. Restrictions on gambling sponsorship are prompting clubs to diversify their partnerships and prioritize fan engagement. Investments in infrastructure and premium hospitality are unlocking new revenue streams and strengthening matchday earnings. Women’s football and emerging regional markets are seeing rapid expansion due to targeted funding and innovative ownership models. Overall, the market is being propelled by elite club branding, digital monetization, regulatory adaptation, and fan-centric growth strategies.

Key Report Takeaways

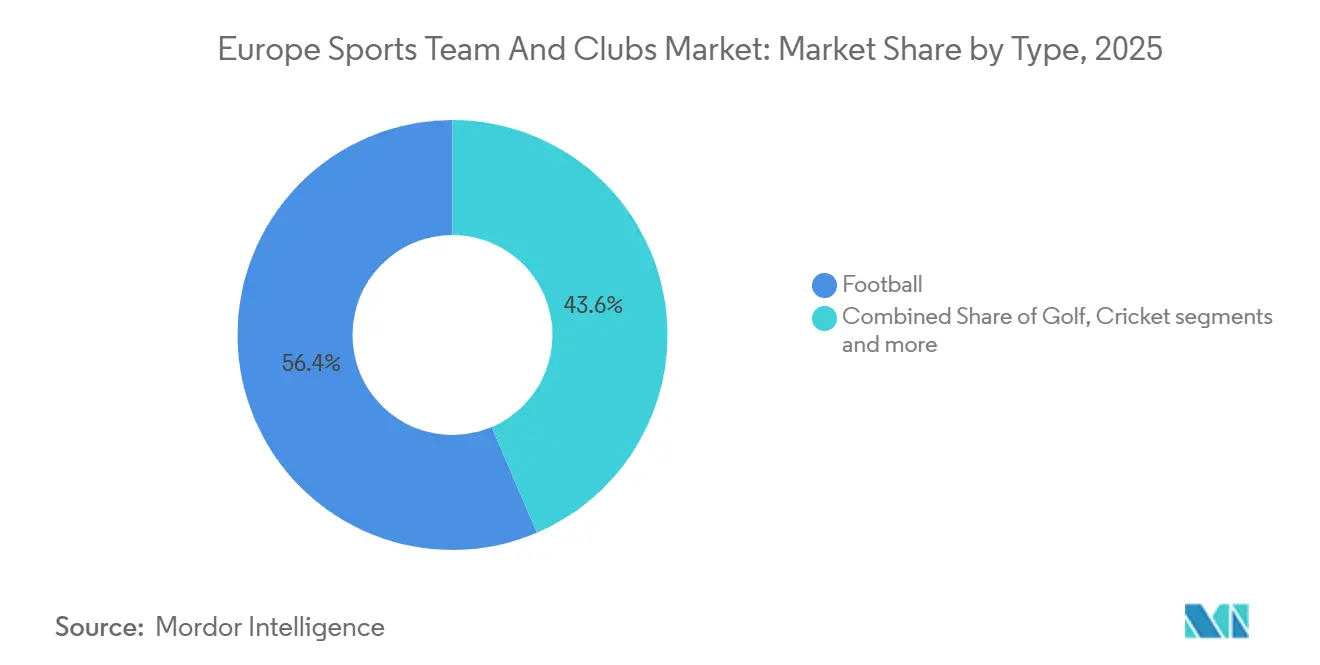

- By type, football led with a 56.43% of the Europe sports team and club market share in 2025, and women’s football is forecast to expand at an 11.87% CAGR during 2026-2031.

- By revenue source, media rights accounted for 37.44% of the Europe sports team and club market share in 2025, while NFT-enabled merchandising is projected to advance at a 16.75% CAGR through 2031.

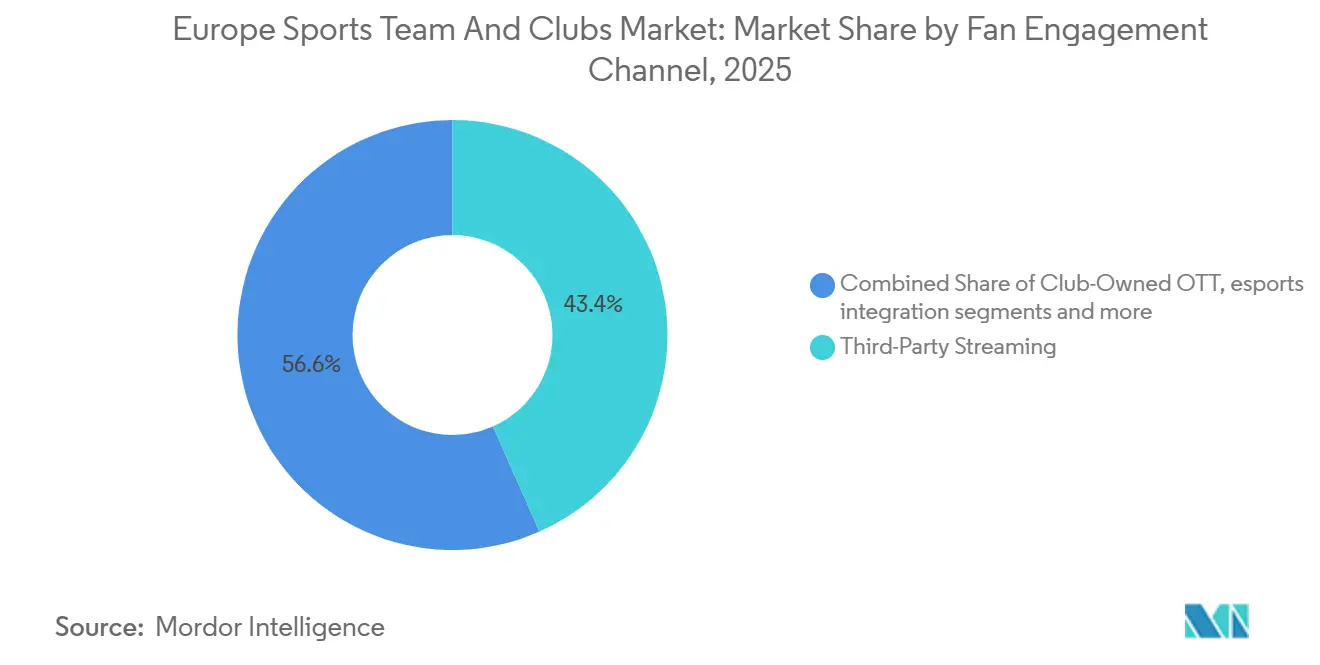

- By fan engagement channel, third-party streaming services held 43.36% of the Europe sports team and club market share in 2025, and club-owned OTT platforms are set to grow at an 18.48% CAGR over 2026-2031.

- By geography, the United Kingdom held 28.38% of the Europe sports team and club market share in 2025, and the NORDICS region records the fastest growth with a 10.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Sports Team And Clubs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring valuations of tier-1 football clubs | +1.2% | Global, concentrated in the United Kingdom, Spain, Italy | Medium term (2-4 years) |

| Media-rights inflation driven by streaming wars | +2.8% | Global, strongest in the United Kingdom, Germany, Spain, and France | Short term (≤ 2 years) |

| Post-pandemic stadium attendance recovery | +1.5% | Global, most pronounced in the United Kingdom, Germany, and Spain | Short term (≤ 2 years) |

| Surge in women's professional leagues | +1.1% | Europe-wide, led by the United Kingdom, Germany, and Spain, with spill-over to NORDICS, BENELUX. | Long term (≥ 4 years) |

| NFT-based fan-token monetisation | +0.4% | Global with higher uptake in Italy and Spain, relatively muted in the United Kingdom | Medium term (2-4 years) |

| Rise of Saudi investment creating spill-over transfer fees | +0.9% | Europe-wide, notably the United Kingdom, France, and Spain, as the exit markets for player sales | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Valuations of Tier-1 Football Clubs

Apollo Sports Capital is driving soaring valuations of Tier‑1 football clubs by injecting capital into Atlético de Madrid to expand infrastructure, enhance commercial operations, and strengthen long-term competitiveness. This investment preserves the club’s brand and fan loyalty while professionalizing revenue streams from media, sponsorship, and hospitality. By showing how institutional investors can scale clubs into global brands, the deal highlights a pathway for increasing market value across European football[1]Apollo Global Management, “Atlético de Madrid to Welcome Apollo Sports Capital as Majority Shareholder,” apollo.com.. More broadly, private capital is increasingly treating clubs as durable, multi-cycle assets, driving enterprise value growth. Leading European clubs are achieving record valuations, opening opportunities for premium sponsorships, long-term media rights agreements, and infrastructure-led expansion. Stadium projects enhance pricing power and unlock additional revenue from associated real estate, while liquidity in the player market supports asset values and overall balance-sheet stability. Collectively, these trends are powering the rapid increase in valuations of Tier 1 football clubs across Europe.

Media-Rights Inflation Driven by Streaming Wars

Media-rights values are rising as streaming platforms compete for top domestic and international content, boosting revenue across the European sports team and club market. Leagues are leveraging this competition to capture strong pricing power and expand global distribution, enhancing financial resilience. Expanded UEFA competitions provide clubs with additional opportunities to monetize league and tournament participation. Bundled distribution deals allow platforms to preserve premium pricing while reaching wider audiences. Stable domestic rights, combined with international streaming partnerships, are driving higher fan engagement and broader market exposure. This media-rights inflation encourages clubs to invest strategically in commercial operations and infrastructure to maximize returns. It also attracts institutional and private capital, which views clubs as durable, multi-cycle assets with scalable revenue potential. Collectively, these factors are key drivers behind the growth and rising valuations of European sports clubs.

Post-Pandemic Stadium Attendance Recovery

German football has seen a strong post-pandemic rebound, with Bundesliga and Bundesliga 2 clubs selling about 10.38 million tickets in the first half of the 2024‑25 season. Bundesliga matches drew around 5.83 million fans at an average of 38,079 per game, while Bundesliga 2 set a record with 4.55 million attendees, averaging 29,761 per match. High stadium occupancy and moderate ticket pricing highlight fan loyalty and broad access. This recovery is boosting matchday revenues and reinforcing the financial and cultural importance of clubs. Robust attendance is a key driver of growth in the European sports team and club market[2]Football Ground Guide, “Emirates Stadium expansion,” footballgroundguide.com.. Dynamic pricing strategies and growth in secondary-market ticket sales are driving higher values for marquee fixtures. The market is also benefiting from new stadiums and venue upgrades, which enhance capacity, fan experience, and commercial opportunities. Overall, the return of fans to stadiums is a key driver of growth for the European sports team and club market.

Surge in Women’s Professional Leagues

The surge in women’s professional leagues is being driven by UEFA’s increased financial support, with around USD40 million allocated across the Women’s Champions League and the newly introduced Women’s Europa Cup. Clubs advancing to the Champions League phase receive about USD19 million in base and performance payments, while early-stage participants receive USD8 million, and the Europa Cup distributions add roughly USD6 million. Solidarity payments of approximately USD6.5 million to other top-division clubs further support league development and competitive balance. These higher financial incentives, combined with growing media and sponsorship revenues, are encouraging clubs to professionalize operations, invest in infrastructure, and retain top talent. Expanded competition formats are enhancing exposure and commercial appeal. Overall, rising prize money, improved facilities, and broader competitive opportunities are key drivers behind the rapid growth of women’s professional football and its increasing contribution to the European sports team and club market[3]UEFA, “UEFA budget 2025/26,” uefa.com. .

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating player wage-to-revenue ratios | -1.4% | Global, acute in France, the United Kingdom, and Italy | Medium term (2-4 years) |

| Regulatory caps on sports gambling sponsorship | -0.6% | United Kingdom, Italy, Netherlands, Germany | Short term (≤ 2 years) |

| Macroeconomic squeeze on discretionary spend | -0.9% | Europe-wide, most severe in the United Kingdom, France, and Austria | Medium term (2-4 years) |

| Fragmented data ownership curbs direct-to-fan plays | -0.3% | Primarily, the United Kingdom, Germany, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Player Wage-to-Revenue Ratios

High player wage-to-revenue ratios continue to constrain operating margins across Europe’s top leagues, creating financial pressure for clubs. While the Premier League has normalized ratios from pandemic-era peaks, overall wage bills remain elevated, limiting flexibility in other areas of spending. France carries the highest wage burden among major leagues, whereas Germany’s governance rules keep costs lower by restricting external capital inflows. New UEFA and domestic spending controls cap squad costs at a percentage of revenue and impose penalties for exceeding limits, forcing clubs to manage expenses more carefully. Clubs with disciplined cost structures can protect margins, but many still rely on occasional player sales to maintain cash flow. Overall, escalating wage obligations and regulatory limits act as a key restraint on market growth, restricting clubs’ ability to invest freely in infrastructure, talent, and commercial initiatives.

Regulatory Caps on Sports Gambling Sponsorship

Regulatory limits on sports gambling sponsorship are constraining revenue opportunities for European clubs. The Premier League’s voluntary ban on front-of-shirt gambling deals from 2026/27 is expected to reduce income, particularly for mid-tier clubs that historically relied heavily on these partnerships. Similar restrictions across European countries, including tighter rules in Germany, limit advertising, athlete endorsements, and event activations. As a result, sponsorship losses are unevenly distributed, hitting clubs outside the top commercial earners the hardest. Research has highlighted the extent of gambling marketing in football, reinforcing regulatory pressures. To mitigate the impact, clubs are seeking alternative sponsors in sectors such as financial services, tourism, and technology. Overall, these regulatory changes act as a key restraint on the market by reducing a significant source of commercial revenue and limiting financial flexibility for many clubs.

Segment Analysis

By Type: Women’s Football Anchors 11.87% Expansion

Football held 56.43% in 2025 and remained the anchor of the Europe sports team and club market, while women’s football recorded the fastest growth trajectory at an 11.87% CAGR for 2026-2031. Within the sport, women’s football is emerging as the fastest-growing segment, driven by sustained investment from UEFA and increasing domestic revenue streams in key leagues such as England. Top-tier men’s competitions remain supported by large-scale broadcast arrangements, while clubs are adapting to cost controls and shifts in sponsorship by focusing on premium hospitality, digital subscriptions, and data-driven pricing to protect margins. Other sports, including rugby union, cricket, golf, and boxing, contribute to the market through stable broadcast windows, international tournaments, and event-driven income, though they are more dependent on venue throughput and event cadence. Diversified multi-sport clubs also help smooth earnings across cycles, adding stability to the overall market.

The strategic implication for the Europe sports team and club market is a clear reallocation of resources toward women’s football, where growth potential remains strong, and investment intensity delivers above-market returns. Leading clubs are increasingly prioritizing the expansion of women’s programs while continuing to optimize revenue from men’s football and other sports through innovative commercial strategies. Digital content, sponsorship integration, and fan engagement initiatives are becoming key levers across all segments, allowing clubs to diversify income and enhance resilience in a dynamic market environment. Overall, category leaders are balancing stability in established segments with aggressive growth in emerging areas, particularly women’s football, to drive long-term market expansion.

Note: Segment shares of all individual segments available upon report purchase

By Revenue Source: Media Rights at 37.44%, NFT Merchandising Surges 16.75%

Media rights contributed 37.44% of the revenue mix in 2025 and reinforced the central role of long-term broadcast agreements in the Europe sports team and club market. Media rights continue to play a central role in the European sports team and club market, underpinning long-term broadcast agreements and providing predictable cash flows for top-tier competitions. Sponsorship, merchandising, and ticketing remain important complementary streams, with clubs increasingly focusing on premium experiences, dynamic pricing, and hospitality to enhance matchday revenue. Expanded UEFA competitions further boost media and prize opportunities for clubs that qualify and perform at high levels. Redevelopment of stadiums and venue enhancements also strengthen ancillary commercial income, contributing to a more diversified revenue mix beyond traditional media channels.

Merchandising is evolving toward digital extensions, including NFTs, fan tokens, and limited-edition releases, reflecting experimentation with new ways to engage supporters and monetize the fan base. Ticketing strategies emphasize premiumization and personalized offerings to increase per-capita yields while maintaining attendance. Sponsorship is increasingly fragmented, with smaller and mid-tier clubs exploring alternative categories in response to tighter gambling regulations. Overall, the market is balancing media-led revenue with growing direct-to-fan commerce, leveraging data, digital assets, and innovative commercial strategies to drive sustainable growth across the European sports team and club ecosystem.

By Fan Engagement Channel: Third-Party Streaming 43.36%, Club OTT Sprints 18.48%

Third-party streaming services held 43.36% of fan engagement in 2025, underscoring consumers’ preference for aggregated sports portfolios across markets. Club-owned OTT platforms posted the fastest growth at an 18.48% CAGR through 2031, but started from a small base as live match rights mostly reside with leagues and broadcasters. Fan loyalty is evident as supporters return to stadiums, while moderate ticket pricing ensures broad access. Clubs are using dynamic pricing and secondary-market sales to increase revenue from high-demand fixtures. Renovated and new stadiums are enhancing fan experiences and unlocking additional hospitality opportunities. Matchday revenue growth is reinforcing club finances and supporting long-term investment in infrastructure. The recovery in live attendance is also strengthening the cultural and social significance of clubs. Overall, robust stadium engagement is a key driver of growth in the European sports team and club market.

Growth in direct-to-fan platforms is limited by the economics of live rights and the need to achieve scale, yet clubs continue to invest in behind-the-scenes content and personalized experiences to boost engagement. The European sports team and club market is balancing reliance on third-party aggregators with the value of first-party data, with many clubs tailoring their OTT offerings to niche content and membership benefits. Social media channels extend reach, support sponsorship activations, and enable new content formats, including the rapidly expanding women’s football segment. Stadium and live activations enhance premium per-capita revenue while strengthening fan experiences, particularly at renovated venues. As media rights cycles evolve, third-party platforms continue to bundle football with other sports, keeping aggregated access central to fan engagement. Clubs are leveraging these channels to maintain strong connections with supporters and diversify monetization strategies.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United Kingdom held 28.38% of the Europe sports team and club market in 2025, supported by the Premier League’s rights strength and the presence of several of the most valuable global club brands. Ongoing broadcast deals maintain competitiveness and extensive coverage across key territories. Germany holds a significant position with stable domestic media rights, high attendance, and consistent ticket pricing that support fan-friendly league operations. France’s market is concentrated around its largest clubs, with domestic broadcasting still evolving, shaping near-term growth prospects. Spain and Italy benefit from strong club brands, commercial depth, and steady media rights arrangements, which support market stability and moderate expansion.

The Nordics region is leading growth with a 10.31% CAGR through 2031, due to professionalization across leagues and consistent participation in European competitions, which expands revenue opportunities for clubs. The Benelux markets also show strong growth, supported by clubs leveraging talent pipelines and continental competition exposure. Other European markets are expanding through stadium openings, naming rights deals, and other commercial initiatives that enhance income streams. Local regulations on state aid and tax frameworks continue to influence club capital plans and wage structures. Together, these regional differences shape pricing power, revenue potential, and the pace of commercialization across Europe.

Comparisons to prior periods highlight mature growth in the United Kingdom, while the Nordics accelerate as institutional investment and continental competition broaden club revenues. Germany benefits from high attendance and the depth of its second-tier leagues, while France is stabilizing following earlier broadcasting adjustments. Spain’s next-cycle media rights and infrastructure improvements support mid-term revenue gains, particularly for clubs completing major renovations. Italy maintains steady growth, supported by its top brands and disciplined sponsorship strategies. Overall, the European sports team and club market reflects a mix of established scale markets and emerging growth corridors that sustain the baseline and future pipeline.

Competitive Landscape

The European sports team and club market is highly fragmented, with top clubs capturing a significant portion of total revenues, which limits pricing power for any single entity. Competitive advantage in 2026 is increasingly driven by infrastructure programs that enhance matchday yields and generate income from non-matchday events, as demonstrated by stadium redevelopments at elite clubs. Multi-club ownership models continue to be central for select investors, allowing portfolio-level cost efficiencies and optimized talent movement. Clubs are also expanding direct-to-fan channels, including mobile apps, OTT platforms, and tokenized experiences, while maintaining presence on large streaming platforms to protect audience reach. These strategies collectively aim to strengthen brand value and diversify revenue streams across the market.

Selected strategic moves highlight the momentum of 2025 and execution priorities for 2026. Institutional investment, such as major stakes in leading clubs, is funding mixed-use developments, commercial scaling, and balance-sheet flexibility for acquisitions. Platform partnerships between streaming services are expanding access to European football while enabling bundling economics that support broader distribution. Renovation-led pricing power is a key trend, with clubs upgrading facilities to unlock premium hospitality demand and recurring revenue from seat licenses. Cost governance frameworks, including UEFA’s financial sustainability rules and league-level squad cost ratios, reinforce disciplined capital allocation across top clubs.

Emerging market dynamics are also shaping competitive behavior and valuation outcomes. Spill-over liquidity from high-spending leagues abroad has supported European clubs’ transfer market values and enabled favorable player sales. Clubs are increasingly segmenting fan engagement by channel, using social video and short-form content to amplify sponsorship revenue beyond traditional broadcast exposure. Investments in analytics, personalization, and technology have demonstrated a stronger correlation with commercial revenue growth than on-field performance, encouraging clubs to prioritize monetization capabilities. Overall, the market rewards programs that compound stadium economics, maintain disciplined wage structures, and scale direct-to-fan engagement effectively. These approaches define the competitive landscape for leading European sports teams and clubs.

Europe Sports Team And Clubs Industry Leaders

Real Madrid CF

FC Barcelona

Manchester United FC

FC Bayern München AG

Paris Saint-Germain FC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Apollo Sports Capital, the sports investment division of Apollo Global Management, became the majority shareholder of Atlético de Madrid, retaining the club's CEO and president. The investment improved the club's financial position and competitiveness, supporting player development and infrastructure projects, including a new sports and entertainment district.

- June 2025: UEFA confirmed the revenue distribution framework for the 2025/26 UEFA club competition cycle, outlining how commercial revenues from the Champions League, Europa League, Conference League, and Super Cup will be shared among participating and non‑participating clubs.

- May 2025: The Premier League announced new live audiovisual broadcast deals securing rights holders across multiple regions for the 2025/26–2028/29 seasons, ensuring broad global coverage and competitive distribution of its matches ahead of the upcoming campaigns.

Europe Sports Team And Clubs Market Report Scope

The Europe sports teams and clubs market comprises professional and semi-professional sports organizations across football, basketball, rugby, and other sports that generate revenue from media rights, sponsorships, ticketing, and merchandising. It is driven by strong fan engagement, established leagues, and growing commercialisation across major European markets.

The Europe Sports Team and Club Market Report is Segmented by Type (Football, Golf, Rugby Union, Cricket, Boxing, Others), Revenue Source (Media Rights, Merchandising, Tickets, Sponsorship), Fan Engagement Channel (Club-Owned OTT Platforms, Third-Party Streaming Services, Social-Media Direct-to-Fan, Stadium & Live Activations, eSports Integration, Official Mobile Apps), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe).

| Football |

| Golf |

| Rugby Union |

| Cricket |

| Boxing |

| Others |

| Media Rights |

| Merchandising |

| Tickets |

| Sponsorship |

| Club-Owned OTT Platforms |

| Third-Party Streaming Services |

| Social-Media Direct-to-Fan |

| Stadium & Live Activations |

| eSports Integration |

| Official Mobile Apps |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Type | Football |

| Golf | |

| Rugby Union | |

| Cricket | |

| Boxing | |

| Others | |

| By Revenue Source | Media Rights |

| Merchandising | |

| Tickets | |

| Sponsorship | |

| By Fan Engagement Channel | Club-Owned OTT Platforms |

| Third-Party Streaming Services | |

| Social-Media Direct-to-Fan | |

| Stadium & Live Activations | |

| eSports Integration | |

| Official Mobile Apps | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size and growth outlook for the Europe sports team and club market by 2031?

The Europe sports team and club market size is USD 27.23 billion in 2026 and is projected to reach USD 42.23 billion by 2031 at a 9.17% CAGR.

Which revenue stream contributes the most to European clubs today?

Media rights contributed 37.44% in 2025, reflecting the central role of long-term broadcast deals and international distribution.

Which country leads the regional landscape in 2026?

The United Kingdom leads with 28.38% in 2025, supported by strong Premier League rights and global brand valuations among top clubs.

What is the fastest-growing engagement channel for European clubs?

Club-owned OTT platforms are set to grow at an 18.48% CAGR through 2031, though they start from a smaller base than third-party platforms.

Which sports segment is expanding the quickest through 2031?

Women’s football is projected to expand at an 11.87% CAGR over 2026-2031, supported by UEFA distributions and domestic league growth.