Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 7.25 Billion |

| Market Size (2030) | USD 9.65 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Specialty Fertilizers Market Analysis by Mordor Intelligence

The Europe specialty fertilizers market size stands at USD 7.25 billion in 2025 and is projected to reach USD 9.65 billion by 2030, reflecting a 5.9% CAGR over the period. Momentum comes from protected-cultivation expansion, rapid fertigation uptake, and the Farm to Fork mandate that targets a 50% cut in nutrient losses by 2030. Input-cost pressures and sustainability requirements are steering growers toward controlled-release, water-soluble, and carbon-verified formulations, while policy incentives in France and Germany accelerate precision fertilization equipment purchases. Manufacturers adapt by bundling digital advisory services with specialty products, creating value beyond the bag. Competitive focus, therefore, pivots to formulations compatible with fertigation, low-cadmium phosphate sourcing, and green-ammonia feedstocks. The market is experiencing a fundamental shift toward precision agriculture and sustainable farming, with advanced irrigation systems enabling more efficient fertilizer application. Manufacturers are increasingly developing balanced nutrient formulations that enhance crop yields while contributing to long-term soil health.

Key Report Takeaways

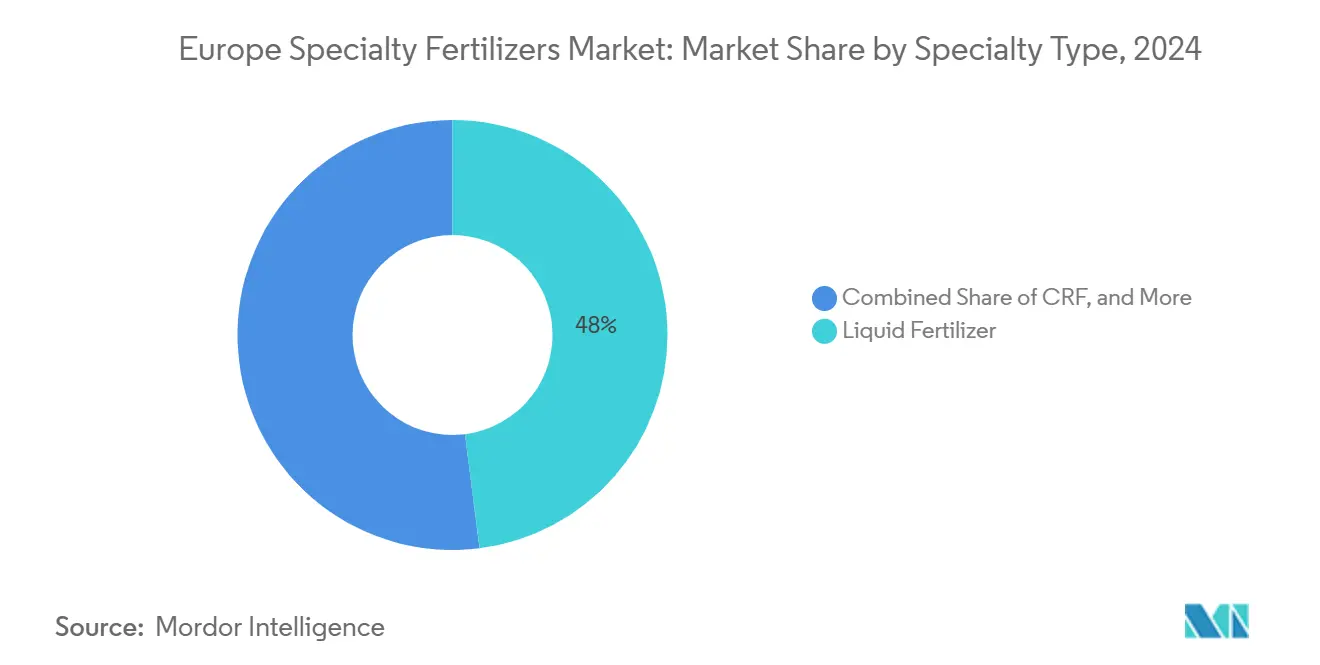

- By specialty type, liquid fertilizers led with 48.0% revenue share in 2024, and controlled-release fertilizers are forecast to expand at a 6.3% CAGR through 2030.

- By application mode, fertigation systems captured 48.1% share of the Europe specialty fertilizers market size in 2024, while soil application is poised to grow at a 7.6% CAGR through 2030.

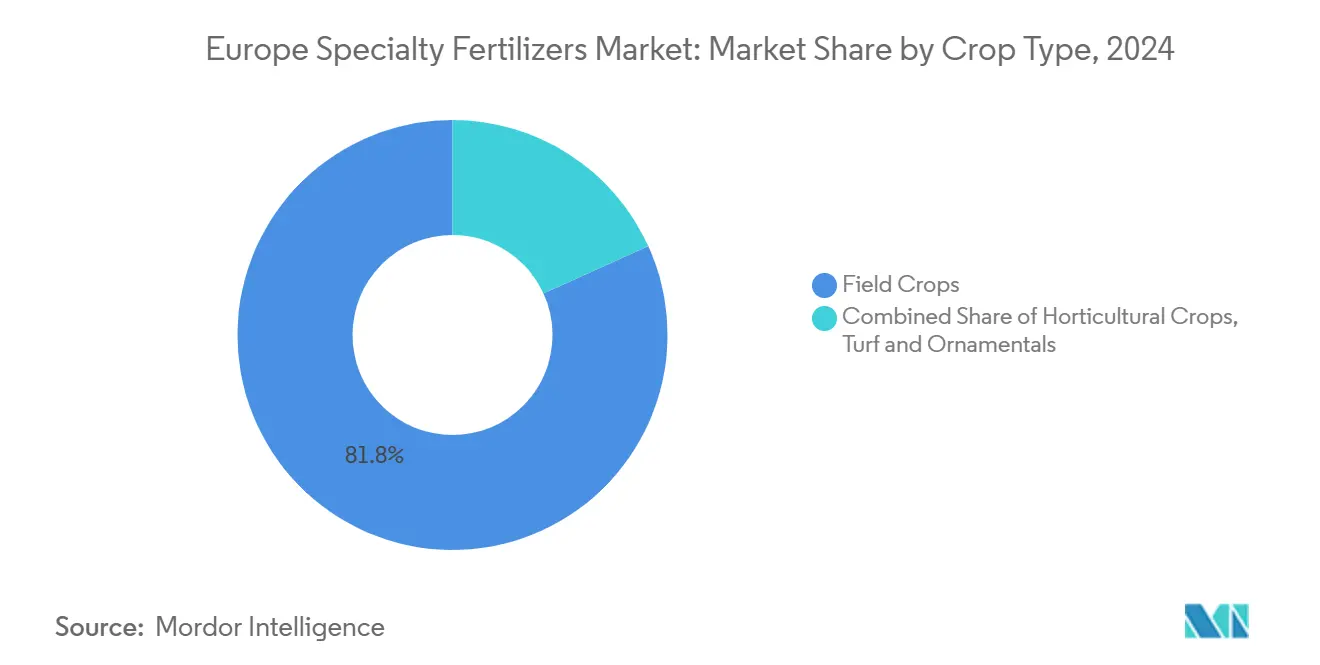

- By crop type, field crops accounted for an 81.8% share of the Europe specialty fertilizers market in 2024, and horticultural crops are anticipated to advance at a 5.9% CAGR through 2030.

- By geography, Russia held 14.9% of the Europe specialty fertilizers market share in 2024 and is projected to expand at a 7.1% CAGR to 2030.

Europe Specialty Fertilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in protected-cultivation acreage | +1.2% | Netherlands, Spain, Italy, and Eastern Europe | Medium term (2–4 years) |

| Surge in fertigation system installations | +1.4% | Mediterranean zone, Netherlands, and Belgium | Short term (≤ 2 years) |

| EU (European Union) Farm to Fork sustainability targets | +0.9% | UK, Switzerland | Long term (≥ 4 years) |

| Recovery of horticulture exports post-Brexit | +0.6% | UK, Netherlands, Belgium | Medium term (2–4 years) |

| Scale-up of green-ammonia hubs | +0.7% | Spain, Netherlands, Germany, Nordics | Long term (≥ 4 years) |

| On-farm carbon-credit monetization pilots | +0.4% | France, Germany, Italy, Sweden | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Growth in Protected-Cultivation Acreage

Protected growing sites now cover 10,500 hectares in the Netherlands and 64,000 hectares in Spain, advancing 15% in 2024 on export-oriented vegetable demand. Soilless systems dominate these expansions and require water-soluble or controlled-release blends that prevent nutrient lockup. Nordic countries add greenhouse capacity to improve food security, sustaining consumption of pH-balanced specialty fertilizers. Liquid products suit closed-loop recirculating systems, helping growers minimize discharge. The European specialty fertilizer market, therefore, captures volume as greenhouse operators standardize year-round nutrition programs.

Surge in Fertigation System Installations

Mediterranean farms installed fertigation at a 25% annual pace in 2024, led by Spanish olive groves and Italian vineyards facing water scarcity. Integrated sensors now trigger variable-rate dosing that can trim fertilizer use by 30-40% while maintaining yield. German and French field-crop producers also attach drip or pivot injectors to comply with nitrate-directive limits. Fertigation readiness steers buyers toward liquid and fully soluble powders, reinforcing the Europe specialty fertilizer market trajectory.

EU Farm to Fork Sustainability Targets

The Farm to Fork plan sets a 50% nutrient-loss reduction by 2030, pushing growers toward polymer-coated nitrogen, urease inhibitors, and bio-based phosphate sources[1].European Commission, “Farm to Fork Strategy,” europa.eu France offers 40% equipment subsidies, and Germany grants tax credits for carbon-verified inputs. Producers that certify cradle-to-gate emissions gain market access advantages. Consequently, controlled-release fertilizers record the fastest volume growth in the Europe specialty fertilizer market.

Recovery of Horticulture Exports Post-Brexit

EU vegetable shipments to the UK rebounded 18% in 2024 after customs workflows stabilized. Dutch and Belgian exporters now specify calcium-fortified programs to boost shelf life. Specialty blends addressing post-harvest firmness, therefore gain share. Logistics-driven quality demands help the Europe specialty fertilizer industry secure higher margins in premium produce channels. This growth highlights the importance of streamlined logistics and innovative solutions in meeting market demands. The European specialty fertilizer industry is well-positioned to capitalize on these trends, driving further advancements in premium produce quality.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking arable land in Eastern Europe | -0.8% | Ukraine, Poland, and Romania | Long term (≥ 4 years) |

| Volatility in natural-gas derived feedstocks | -1.1% | Germany, Netherlands, and Poland | Short term (≤ 2 years) |

| Stringent cadmium limits in EU fertilizer law | -0.6% | EU-27 | Medium term (2–4 years) |

| Slow digital-ag adoption among smallholders | -0.4% | Southern & Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shrinking Arable Land in Eastern Europe

Poland removed 180,000 hectares from cultivation in 2024, while Ukrainian fields faced labor shortages and infrastructure damage[2]Polish Ministry of Agriculture, “Land Use Changes 2024,” gov.pl. Consolidation favors capital-intensive operations that adopt specialty inputs, yet total addressable hectares decline, trimming aggregate demand. Larger farms cushion the Europe specialty fertilizer market, but regional volume headwinds persist. Despite these challenges, the adoption of specialty inputs by larger farms may help stabilize the market.

Slow Digital-ag Adoption Among Smallholders

Farms below 15 hectares in Southern Europe show 20-30% lower GPS and sensor use than larger peers.[3]European Commission. "Market Observatories," europa.euWithout data, precision fertilizer ROI is hard to quantify, slowing specialty penetration. Cooperative equipment sharing and training programs are underway, but full benefits will unfold over a longer horizon. Addressing these challenges through enhanced data collection and targeted support programs could accelerate technology adoption. This would enable smaller farms to achieve greater efficiency and competitiveness in the long term.

Segment Analysis

By Specialty Type: Liquid formulations drive market leadership

Liquid fertilizers commanded 48.0% of the Europe specialty fertilizers market share in 2024 due to drip-ready compatibility and uniform distribution. Growers value rapid plant uptake and lower labor needs, especially in greenhouse vegetables. Controlled-release lines post 6.3% CAGR to 2030, lifted by Farm to Fork rules that reward nutrient-use efficiency. The Europe specialty fertilizers market size for controlled-release options is forecast to widen as polymer-coated urea and sulfur-coated urea stretch feeding intervals to 120 days.

Water-soluble crystals dominate hydroponic basil, cucumber, and strawberry systems in the Netherlands and Belgium, while slow-release granules retain niche turf and ornamental users. Micronutrient blends with zinc, boron, and iron now bundle biostimulants for stress mitigation, a trend aligned with shifting climate patterns. Patent activity for novel encapsulation rose 15% in 2024, underscoring innovation depth.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application Mode: Fertigation systems reshape delivery methods

Fertigation application absorbed 48.1% of sales in 2024 due to expanding drip networks across olives, vines, and greenhouse perennials. Real-time flow meters let growers meter nutrients with milliliter precision, lifting uptake efficiency above 80%. The Europe specialty fertilizers market size tied to fertigation keeps expanding as sensors integrate seamlessly with cloud dashboards. Soil placement nevertheless records the briskest 7.6% CAGR, propelled by variable-rate spreaders that chart prescription maps from satellite imagery.

Foliar sprays hold relevance when phenological windows require quick correction of calcium or magnesium deficiencies in grapes or tomatoes. Spanish trials cut nutrient use 24-33% via multispectral-guided foliar programs. These savings validate payback for drone-enabled sprayers, unlocking fresh demand across high-value crops.

By Crop Type: Field crops anchor volume demand

Field cereals and oilseeds accounted for 81.8% of 2024 purchases, reflecting the sheer scale of wheat, corn, and rapeseed acreage across France, Germany, and Poland. Producers integrate nitrification-inhibitor packages to stay inside groundwater nitrate caps, ensuring compliance while maximizing output. The Europe specialty fertilizers market attributed to field crops thus provides the core revenue bedrock.

Horticulture logs 5.9% CAGR through 2030, driven by greenhouse peppers, berries, and leafy greens sold under traceability labels. Yield gains of 20-25% at Dutch tomato clusters show the pay-for-performance economics that justify premium programs. Turf and ornamentals maintain modest scale yet secure consistent municipal and golf-course budgets that prize slow-release uniformity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Russia secured a 14.9% share in 2024 and is tracking a 7.1% CAGR to 2030. Large grain exporters shift to enhanced-efficiency nitrogen to limit labor passes across vast hectares, and government rebates accelerate the adoption of precision spreaders. Domestic appetite cushions suppliers from sanctions-linked trade frictions. Large-scale farming operations spanning millions of hectares create substantial volume demand for specialty products, particularly controlled-release formulations that reduce application frequency and labor requirements.

Germany and France exhibit high technology readiness with GPS equipment penetration above 70%. Carbon-footprint labels on retail produce incentivize growers to adopt low-cadmium and green-ammonia inputs. The Netherlands, despite a limited land area, records the world’s highest per-hectare specialty fertilizer spend because greenhouse clusters operate year-round.

Spain and Italy leverage Mediterranean climates for export vegetables, justifying liquid and water-soluble regimes that preserve shelf life during long hauls. Poland and the Czech Republic deploy EU modernization funds to expand variable-rate machinery fleets, although fragmented land ownership slows full market potential. Ukraine faces infrastructure disruptions yet keeps specialty purchases steady on export wheat acreage.

Competitive Landscape

The market is moderately fragmented. Yara International ASA, ICL Group Ltd, and EuroChem Group AG integrate mining, production, and distribution to secure feedstock and shorten lead times. Each now bundles satellite-derived nutrient maps within subscription packages, shifting revenue toward service-based models. Companies are increasingly investing in sustainability credentials and carbon footprint verification to capture premium pricing in environmentally conscious market segments.

Green-ammonia partnerships with utilities position frontrunners to deliver net-zero nitrogen at premium pricing. EuroChem Group AG’s Baltic terminals shorten logistics to Nordic buyers, while ICL’s Spanish assets target Mediterranean horticulture. Regional mid-tier players, such as Timac Agro and Haifa Group, differentiate themselves via crop-specific water-soluble lines.

Start-ups deploy nanotechnology carriers that raise nutrient-use efficiency above 90%. Patent filings across polymer science and microbial enhancers rose by double digits in 2024, signaling a steady pipeline. Buyers increasingly value verified emission reductions, so suppliers invest in blockchain traceability systems to capture price uplifts.

Europe Specialty Fertilizers Industry Leaders

-

ICL Group Ltd

-

Kingenta Ecological Engineering Group Co., Ltd.

-

Yara International ASA

-

EuroChem Group AG.

-

FERTIBERIA, S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Haifa Group introduced new water-soluble fertilizer formulations specifically designed for greenhouse cucumber production, targeting the Netherlands and Belgian growers. This initiative is anticipated to strengthen the specialty fertilizers market in Europe by addressing the specific needs of greenhouse growers and enhancing crop productivity.

- August 2024: Timac Agro received ISO 14001 environmental management certification for its French production facilities, supporting sustainability positioning in European specialty fertilizer markets.

- July 2024: ICL Group Ltd completed the acquisition of specialty fertilizer assets from a regional competitor for USD 45 million, expanding its controlled-release fertilizer portfolio in Mediterranean markets. The transaction includes manufacturing facilities and distribution networks in Spain and Italy.

Europe Specialty Fertilizers Market Report Scope

CRF, Liquid Fertilizer, SRF, Water Soluble are covered as segments by Speciality Type. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type. France, Germany, Italy, Netherlands, Russia, Spain, Ukraine, United Kingdom are covered as segments by Country.

Speciality Type

| CRF | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

Country

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Ukraine |

| United Kingdom |

| Rest of Europe |

| Speciality Type | CRF | Polymer Coated |

| Polymer-Sulfur Coated | ||

| Others | ||

| Liquid Fertilizer | ||

| SRF | ||

| Water Soluble | ||

| Application Mode | Fertigation | |

| Foliar | ||

| Soil | ||

| Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf & Ornamental | ||

| Country | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF