Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

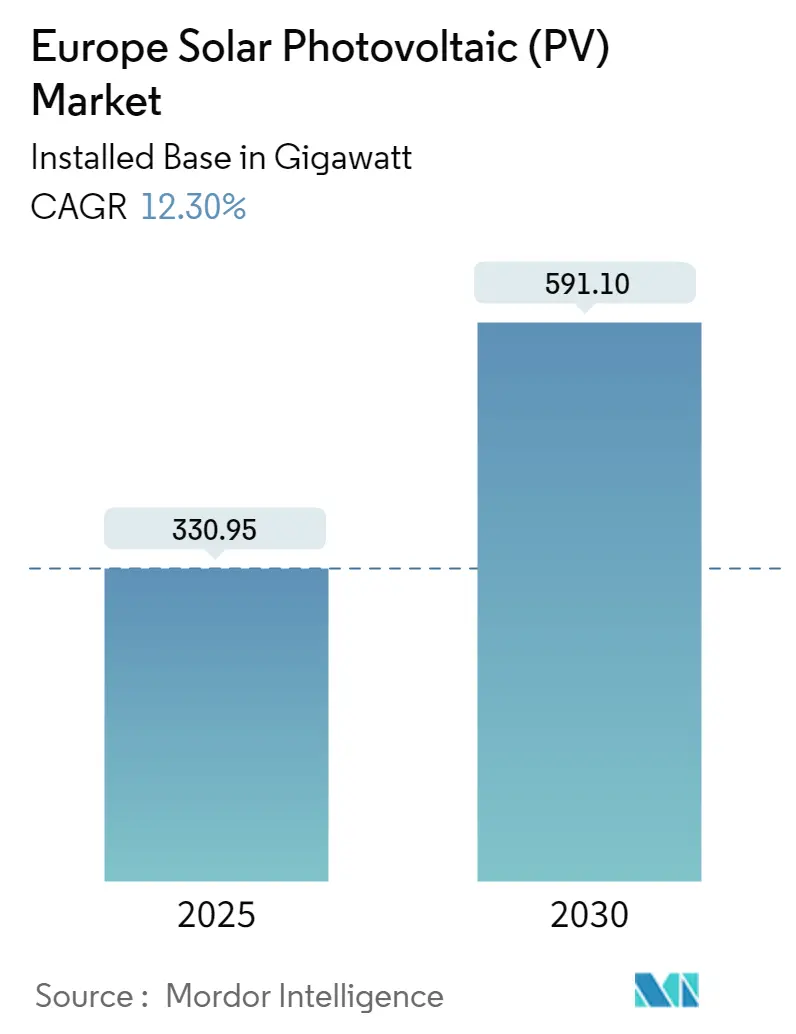

| Market Volume (2025) | 330.95 gigawatt |

| Market Volume (2030) | 591.10 gigawatt |

| Growth Rate (2025 - 2030) | 12.30% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Solar Photovoltaic (PV) Market Analysis by Mordor Intelligence

The Europe Solar Photovoltaic (PV) Market size in terms of installed base is expected to grow from 330.95 gigawatt in 2025 to 591.10 gigawatt by 2030, at a CAGR of 12.3% during the forecast period (2025-2030).

- Over the medium term, factors such as rising demand for electricity across the region, increasing investments in solar energy projects, and producing most of the electricity from renewable sources have driven the growth of the market.

- On the other hand, the rising emphasis on natural gas power generation and the availability of natural gas at lower prices for power generation restrain the market growth in the European region.

- However, the ambitious solar energy targets implemented to boost solar PV installation are expected to create lucrative opportunities for the market during the forecast period.

- Germany, with the largest installed capacity of solar photovoltaics, is expected to dominate the European solar photovoltaics (PV) market during the forecast period.

Europe Solar Photovoltaic (PV) Market Trends and Insights

The Rooftop Segment Anticipated to Witness Significant Market Growth

- The rooftop segment is estimated to witness significant growth during the forecast period in Europe. The European region's rooftop installation has lots of potential as most of Europe's roof surfaces are unused. Several countries in Europe are working on modifying their policies to assess remuneration levels.

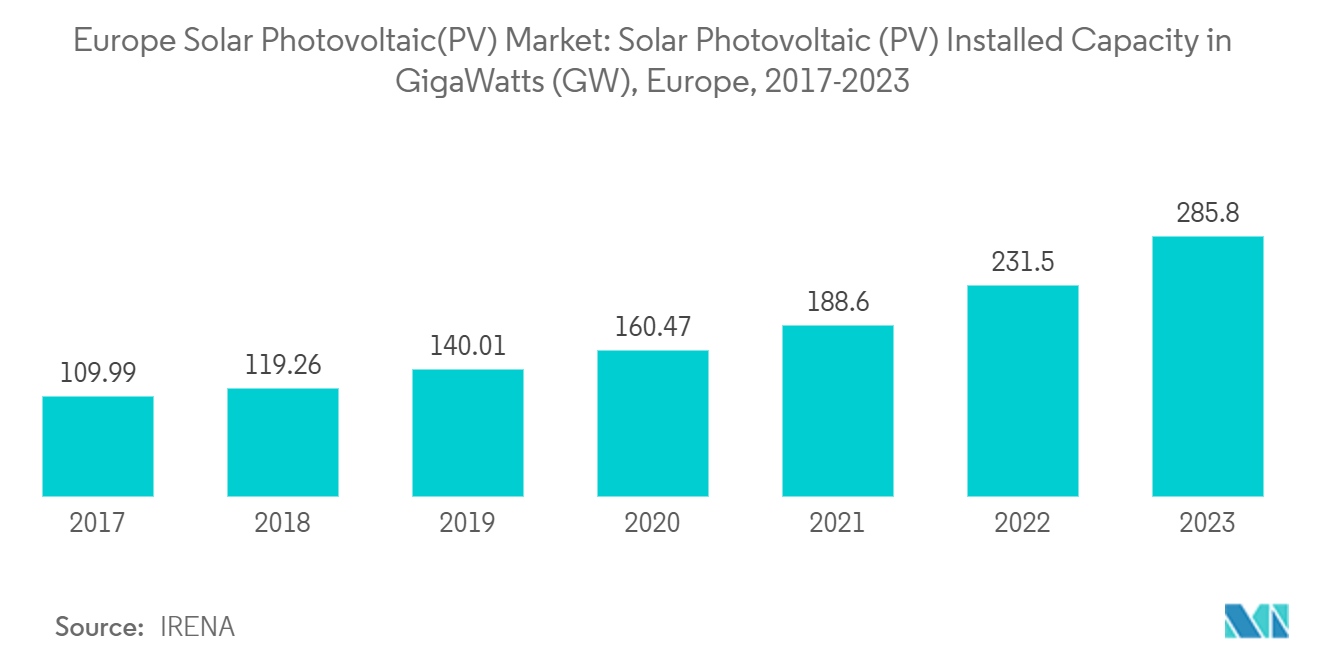

- Norway, the Baltic region, Ireland, and others have geographical conditions favorable to rooftop PV installation. This is expected to increase rooftop solar PV installation in Europe during the forecast period. Also, in several countries, homeowners are willing to install rooftop PV modules to reduce their electricity bills. According to the International Renewable Energy Agency (IRENA), in 2023, Europe's solar PV installed reached 285.80 GW, with a growth rate of 23.45% over the previous year.

- In December 2023, the European Parliament and the European Council reached an interim agreement on the strengthened Energy Performance of Buildings Directive (EPBD), aspiring to stimulate the energy performance of buildings and requiring new buildings to be solar-ready. The EPBD also mandates that EU member states ensure new buildings are fit to host rooftop solar PV or thermal installations. Existing public and non-residential building solar will require to be installed commencing from 2027.

- Governments in several countries have adopted supportive policies to increase the deployment of rooftop PV arrays within the region. For instance, in March 2023, the European government adopted the revised Energy Performance of Business Directive mandating rooftop solar systems for all new buildings by 2028 and renovating residential buildings by 2032.

- In 2023, Germany achieved a milestone by installing a record 14GW of solar energy capacity, facilitated by adding over a million new solar power systems, a significant portion of which were residential rooftop installations. This surge reflects an impressive 85% increase in capacity compared to the previous year, as the German Solar Association (BSW) reported. The surge in capacity was primarily fueled by residential demand, particularly for rooftop solar power systems. The BSW noted a substantial increase, with 159,000 PV systems operational in the first quarter of 2023, more than double the number recorded during the same period in 2022.

- Therefore, from the above points, the rooftop solar photovoltaic segment is anticipated to witness significant growth in the European solar photovoltaic market during the forecast period.

Germany Expected to Dominate the Market

- Germany is one of the most lucrative markets in the European region for renewable energy production, including solar. The country has experienced significant developments in solar PV installation due to its target of reducing carbon emissions, and it is likely to continue witnessing growth in solar installation.

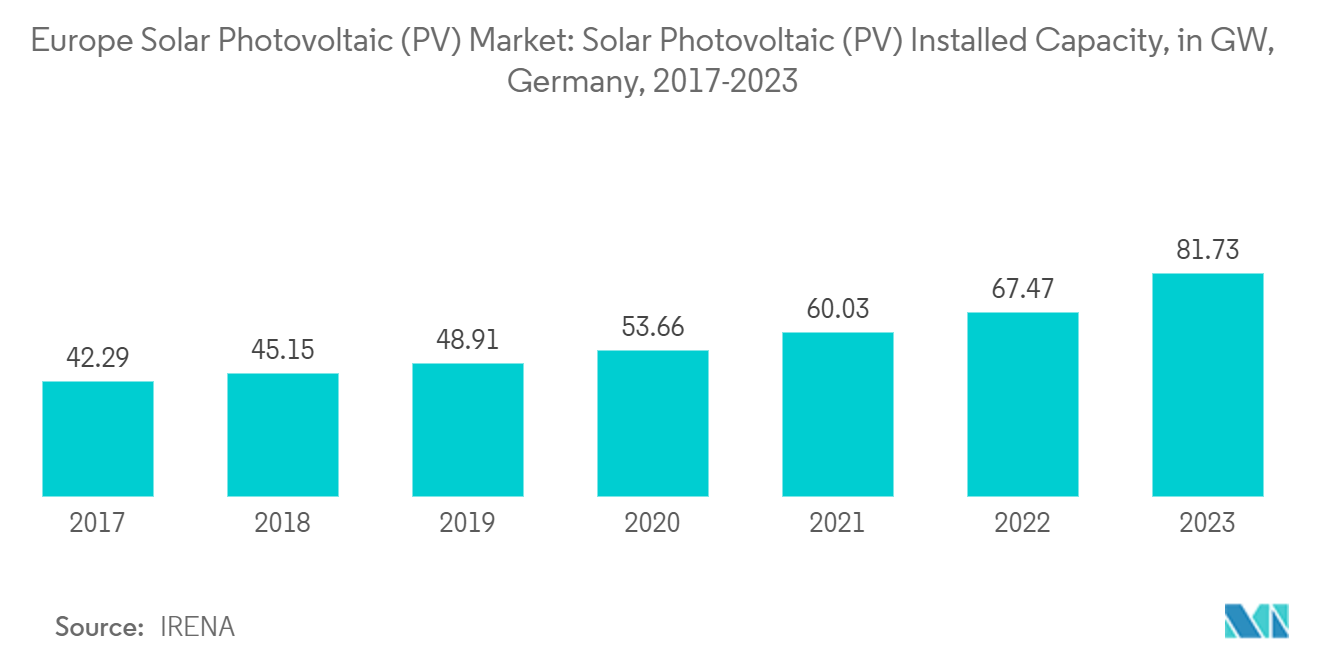

- The country's solar PV installed capacity has witnessed massive growth in recent years. In 2023, the installed solar PV was around 81.73 GW compared to 67.47 GW in 2022, registering a CAGR of over 21%, signifying the country's growing penetration of solar PV systems.

- The country has implemented several regulations and incentive schemes to promote the installation of solar modules in cities. In June 2023, Germany’s economy ministry announced new government funding to rebuild the country’s solar industry. The economy ministry is expected to present the new funding instrument soon and is preparing a tender in line with a new EU subsidy framework in the future.

- The mandates for solar photovoltaic installation on new buildings in a few German cities have helped expand the market in Germany. In December 2022, the European Union approved a EUR 28 billion German renewable energy scheme. The policy aims to increase the use of renewables, including solar power rapidly. It is designed to deliver Germany's target of producing 80% of its electricity from renewable sources by 2030.

- Therefore, based on the above points, solar photovoltaic in Germany will dominate the European solar photovoltaic market during the forecast period.

Competitive Landscape

The European solar photovoltaic (PV) market is fragmented. Some of the major companies in the market (in no particular order) include Hanwha Q CELLS Technology Co. Ltd, Iberdrola SA, SunPower Corporation, JinkoSolar Holding Co. Ltd, and Lightsource BP Renewable Energy Investments Limited.

Europe Solar Photovoltaic (PV) Industry Leaders

-

Lightsource BP Renewable Energy Investments Limited

-

Hanwha Q CELLS Technology Co., Ltd

-

SunPower Corporation

-

Iberdrola, S.A

-

JinkoSolar Holding Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2024: EDP Renováveis, the fourth-largest renewable energy producer globally, initiated operations at a 202-megawatt (MW) solar energy park in central Portugal, marking its largest installation in Europe. This venture is overseen by its parent company, EDP. Named the Cerca project and situated in the municipalities of Alenquer and Azambuja, north of Lisbon, it features over 310,000 solar panels. With an anticipated annual output of 330 gigawatt-hours (GWh), the facility can power approximately 100,000 households, equivalent to around 1% of Portugal's population.

- September 2023: the United Kingdom government announced the results of its latest renewable energy auction. Around 56 solar projects with a total capacity of 1,927.68 MW secured 15-year CfDs at a final price of USD 57/MW.

- February 2023: A German renewable energy project developed by RWE and Greek state-owned utility PPC announced that it reached an agreement to establish a 450 MW solar photovoltaic project in Greece through a joint venture company, Meton Energy. Construction will begin soon and is expected to come online by the end of 2024. Meton Energy has also signed a 10-year bilateral power purchase agreement (PPA) with PPC post-project completion.

Europe Solar Photovoltaic (PV) Market Report Scope

Solar PV stands for solar photovoltaic. It refers to the technology used to convert sunlight directly into electricity using solar panels, typically silicon-based materials. When sunlight hits the solar panels, it creates an electric current through the photovoltaic effect, generating electricity. Solar PV systems can be used for various applications, from small-scale residential installations to large utility-scale power plants. They are a key component of renewable energy systems, helping to reduce dependence on fossil fuels and mitigate climate change.

The European solar photovoltaic (PV) market is segmented by inverter type, end user, deployment, and geography. By type, the market is segmented into thin-film and crystalline silicon. By end user, the market is segmented into residential, commercial, and industrial (including SMEs). By deployment, the market is segmented into ground-mounted and rooftop. The report also covers the market size and forecasts for the solar photovoltaic market across major countries in the region. For each segment, the market sizing and forecasts have been done based on installed capacity (GW).

Type

| Thin Film |

| Crystalline Silicon |

End User

| Residential |

| Commercial and Industrial (including SMEs) |

Deployment

| Ground-Mounted |

| Rooftop Solar |

Geography Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)}

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Nordic |

| Turkey |

| Rest of Europe |

| Type | Thin Film |

| Crystalline Silicon | |

| End User | Residential |

| Commercial and Industrial (including SMEs) | |

| Deployment | Ground-Mounted |

| Rooftop Solar | |

| Geography Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)} | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Nordic | |

| Turkey | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Europe Solar Photovoltaic Market?

The Europe Solar Photovoltaic Market size is expected to reach 330.95 gigawatt in 2025 and grow at a CAGR of 12.30% to reach 591.10 gigawatt by 2030.

What is the current Europe Solar Photovoltaic Market size?

In 2025, the Europe Solar Photovoltaic Market size is expected to reach 330.95 gigawatt.

Who are the key players in Europe Solar Photovoltaic Market?

Lightsource BP Renewable Energy Investments Limited, Hanwha Q CELLS Technology Co., Ltd, SunPower Corporation, Iberdrola, S.A and JinkoSolar Holding Co., Ltd are the major companies operating in the Europe Solar Photovoltaic Market.

What years does this Europe Solar Photovoltaic Market cover, and what was the market size in 2024?

In 2024, the Europe Solar Photovoltaic Market size was estimated at 290.24 gigawatt. The report covers the Europe Solar Photovoltaic Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Solar Photovoltaic Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: