Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

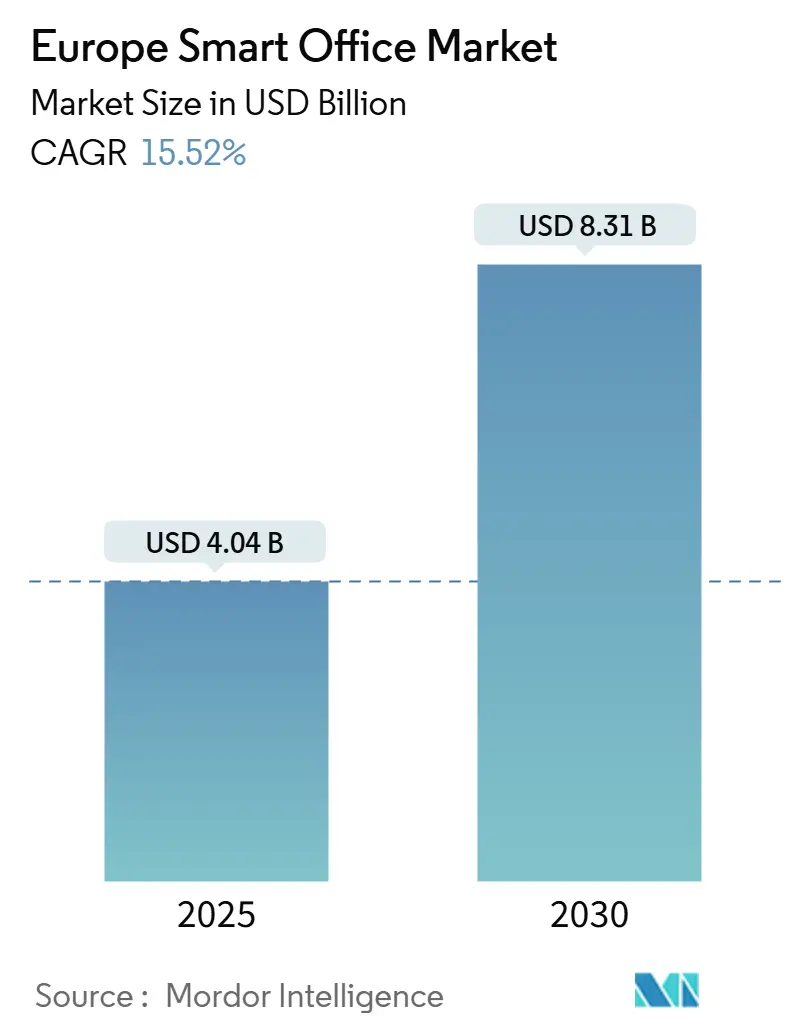

| Market Size (2025) | USD 4.04 Billion |

| Market Size (2030) | USD 8.31 Billion |

| Growth Rate (2025 - 2030) | 15.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Smart Office Market Analysis by Mordor Intelligence

The Europe Smart Office Market Size stood at USD 4.04 billion in 2025 and is forecast to reach USD 8.31 billion by 2030, advancing at a 15.52% CAGR over the period. Firm European Union efficiency rules shape growth, the spread of hybrid work patterns, and a steady fall in Internet of Things (IoT) sensor prices. Real-time workplace analytics running on 5G private networks are cutting operating costs by as much as 30% in pilot sites.[1] GSMA Intelligence, “Connectivity for Good,” gsma.com Germany leads the current adoption, buoyed by federal retrofit incentives, while Italy forms the fastest-growing cluster due to grants from the National Recovery and Resilience Plan. Smart lighting retains the largest revenue slice, yet space-focused workplace analytics tools hold the strongest forward momentum. Vendors battle interoperability gaps in older heating, ventilation, and access control hardware, but the arrival of open standards such as Matter and Thread is reducing lock-in barriers.

Key Report Takeaways

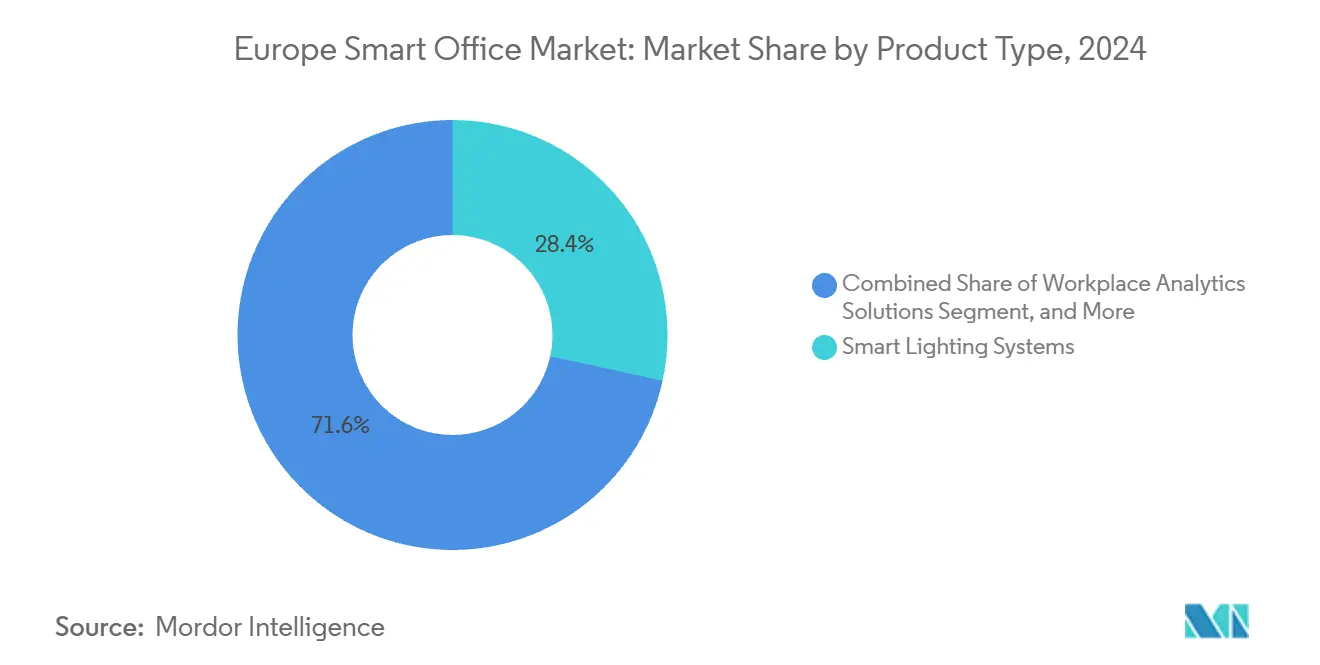

- By product category, Smart Lighting Systems led with a 28.41% Europe Smart Office Market Share in 2024. Workplace Analytics Solutions are projected to post the fastest 15.92% CAGR through 2030.

- By building type, retrofits captured 55.34% share of the Europe Smart Office Market Size in 2024. New Buildings are forecast to expand at a 16.24% CAGR between 2025 and 2030.

- By geography, Germany accounted for 18.14% Europe Smart Office Market Share in 2024; Italy is set to grow at a 16.81% CAGR to 2030.

- Siemens, Schneider Electric, Honeywell, Johnson Controls, and ABB together held 42% share of the Europe Smart Office Market in 2024.

Europe Smart Office Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU energy efficiency regulations | +3.2% | Pan-European, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Hybrid and flexible work models | +2.8% | Major cities, IT and BFSI hubs | Short term (≤ 2 years) |

| Decline in IoT sensor and connectivity costs | +2.5% | Nordics, Germany, United Kingdom | Medium term (2-4 years) |

| 5G private networks in offices | +2.1% | Germany, United Kingdom, France, Italy | Long term (≥ 4 years) |

| Corporate ESG and net-zero goals | +2.4% | Publicly listed firms across Europe | Medium term (2-4 years) |

| Digital twins for predictive management | +1.9% | Nordics, Germany, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent European Union Energy Efficiency Regulations

The 2024 revision of the Energy Performance of Buildings Directive forces every new commercial building to reach zero-emission status by 2030.[2]Energy Directorate, “New Energy Performance of Buildings Directive Comes into Force,” energy.ec.europa.eu Germany set aside EUR 14.5 billion (USD 15.5 billion) in retrofit grants that favor AI-driven energy optimization. The directive introduces smart readiness indicators that score a building’s response to occupant needs and grid signals, pushing demand for dense sensor networks. France’s RE2020 code limits lifecycle carbon, steering developers toward prefabricated modules with embedded controls. Together, these rules replace incremental upgrades with full digital orchestration across lighting, HVAC, and security.

Growing Adoption of Hybrid and Flexible Work Models

Average office footprints shrank 18% between 2020 and 2024, yet daily occupancy swings from 40% to 70% create planning uncertainty. Finance regulators note that 82% of U.K. financial firms now run flexible policies, accelerating hot-desking and analytics investments. Real-time data lets facility teams shut unused floors and trim energy budgets. Activity-based working also demands granular comfort controls that legacy systems lack.

Rapid Decline in IoT Sensor and Connectivity Costs

Component prices for occupancy sensors slid 42% from 2020 to 2024, while wireless modules dropped 38%. Siemens cut materials costs for its Enlighted sensor by 35% in two years, expanding mid-market reach. Battery-free, energy-harvesting devices erase maintenance overhead, and Schneider Electric now manages over 1.2 million sensors across Europe.

Integration of Digital Twins for Predictive Workplace Management

Siemens deployed digital twins in 450 European buildings, predicting failures 72 hours ahead. Johnson Controls reported a 28% cut in heating and cooling energy for OpenBlue users. Although setup costs of up to USD 213,000 curb mass uptake, headquarters and premium assets see rapid payback from reduced downtime and optimized layouts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit capital outlay | -1.8% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Legacy system interoperability gaps | -1.5% | Buildings built before 2010 | Medium term (2-4 years) |

| GDPR-driven privacy and cyber concerns | -1.2% | Germany, France, Netherlands | Medium term (2-4 years) |

| Skilled labor shortages | -1.1% | Nordics and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Retrofit Projects

Smart office retrofits can cost EUR 150-400 (USD 160-426) per square meter, placing a EUR 1.6 million bill on a 5,000 square-meter site.[3]Royal Institution of Chartered Surveyors, “Construction Standards,” rics.org Italy’s generous Superbonus fell from 110% to 70% coverage, slowing activity until fresh deductions arrived. Payback horizons stretching beyond seven years deter smaller landlords, even as European Investment Bank grants remain oversubscribed.

Heightened Data Privacy and Cybersecurity Concerns under GDPR

A Paris real estate firm was fined EUR 800,000 (USD 931520.00) for sensor over-tracking without consent. Legal uncertainty around cloud hosting outside the European Economic Area fuels audit costs. The U.K. National Cyber Security Centre now urges network segmentation and regular penetration tests, yet market compliance varies widely.

Segment Analysis

By Product Type: Workplace Analytics Platforms Gain Strategic Priority

Smart Lighting Systems held 28.41% of Europe Smart Office Market Share in 2024. Europe Smart Office Market Size for workplace analytics is on track to expand at 15.92% CAGR, driven by demand for real-time space data. Microsoft’s Viva Insights covers 3,200 locations and links with Azure Digital Twins to offer predictive heatmaps. Security and access systems stay resilient due to growing biometric use. Energy management tools see rising orders as Germany’s commercial power price averaged EUR 0.28 (USD 0.30) per kilowatt-hour in 2024.[4]Eurostat, “Electricity Price Statistics,” ec.europa.eu

Hardware advances spur audio-video systems with spatial audio and auto-framing, while fire and safety controls integrate deeper into building networks. Commodity pressure on sensors pushes suppliers toward bundling hardware with analytics subscriptions. The Europe Smart Office Industry continues to emphasize interoperability so that lighting, HVAC, and security data converge in one analytics layer.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Building Type: New Construction Gains Momentum

Retrofits represented 55.34% of deployments yet face higher labor costs. Europe Smart Office Market Size for new buildings is projected to rise at 16.24% CAGR. Skanska embeds AI-ready building management in every project started after January 2024, adding 3% to cost but earning 8-12% rental premiums. Mass timber structures demand precise humidity control, pushing early adoption of smart sensors.

Retrofit activity remains vast because 70% of offices pre-date 2010 and must meet new efficiency rules. However, unforeseen legacy wiring issues and the need for live-occupied installation prolong payback. Developers increasingly choose smart-enabled rebuilds where local rules allow demolition, especially in Germany, France, and the Nordics.

By Connectivity Technology: Wireless Protocols Dominate

Wireless links covered 62.49% of the market in 2024 and will grow at 17.14% CAGR. Wi-Fi 6 and soon Wi-Fi 7 handle audio-video loads and analytics dashboards. Zigbee and Bluetooth Low Energy underpin most smart lighting and occupancy sensors. Thread adoption surged after Apple and Google enabled cross-vendor support. Europe Smart Office Market Size for wired Ethernet remains stable for life-safety systems where deterministic latency is vital.

Power over Ethernet Plus supplies up to 90 watts, allowing a single cable for lights, sensors, and access readers. Z-Wave stays niche in small offices, and legacy BACnet and Modbus persist for HVAC backbones. Hybrid designs that feed wireless edge nodes through wired backhaul are emerging as the default topology.

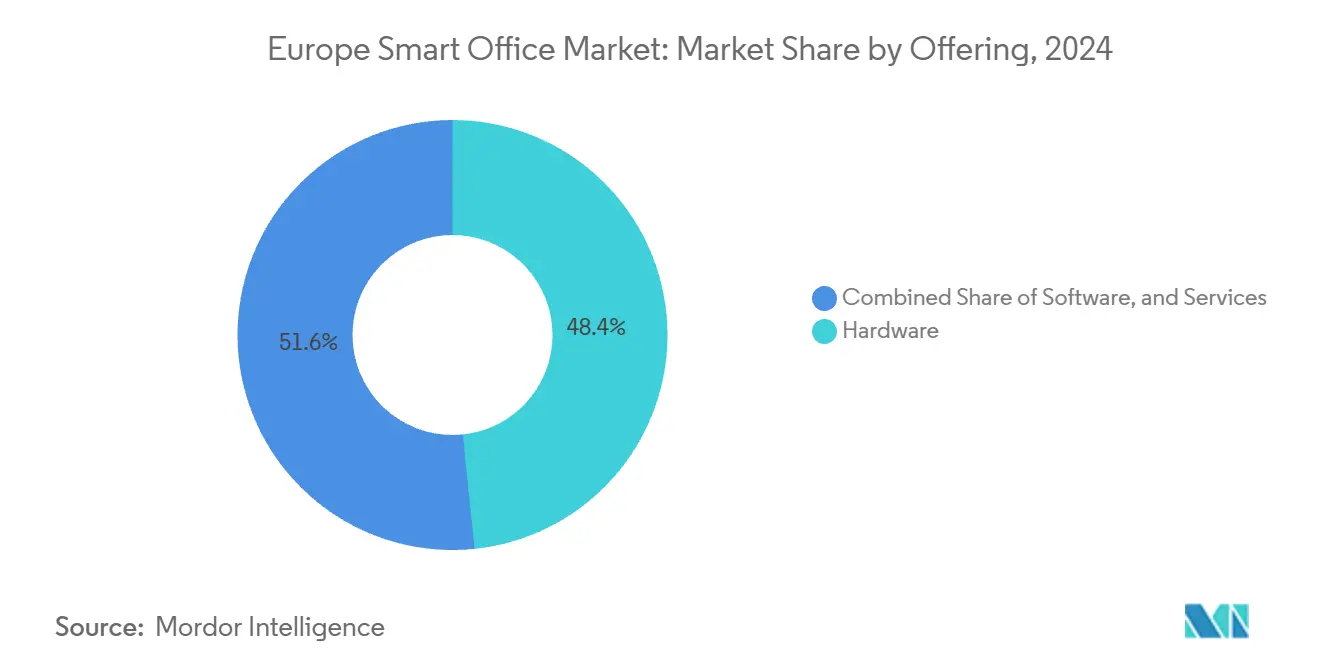

By Offering: Services Segment Accelerates

Hardware produced 48.36% of revenue in 2024, but services will climb at 16.31% CAGR. Professional design and commissioning dominate today, followed by managed services with uptime guarantees. Honeywell Forge logged 32% European revenue growth with average contracts above USD 150,000 per year.

Europe Smart Office Market Size for software expands as AI modules forecast faults and give efficiency guidance. Sensors commoditize, so vendors pair them with cloud dashboards. Controllers gain edge logic that trims latency and safeguards against connectivity loss. Europe Smart Office Industry participants are steering toward annual subscription models rather than one-off equipment sales.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Healthcare Leads Growth

IT and Telecom captured 26.72% of the Europe Smart Office Market in 2024. Healthcare and Life Sciences will grow at 17.12% CAGR as laboratories need strict environmental control and audit trails. Roche linked 8,500 sensors in Basel to its lab information system for instant deviation alerts. Banking rules also keep physical security budgets strong. Government retrofits accelerate through the United Kingdom’s GBP 1.2 billion program to outfit 600 offices with smart energy platforms. Manufacturing, retail, and education continue prioritizing energy-saving lighting and HVAC, with advanced analytics often deferred to later phases.

Geography Analysis

Germany held 18.14% of the Europe Smart Office Market in 2024, supported by EUR 14.5 billion of federal retrofit subsidies and strict building codes. The country benefits from deep integrator networks established by Siemens and Bosch, which shorten project lead times. The United Kingdom continues to invest, driven by London’s financial hub and the 2050 net-zero mandate. France benefits from RE2020 rules that favor sensor-embedded prefabricated modules.

Italy shows the fastest 16.81% CAGR outlook. EUR 15.2 billion (USD 17.70 billion) of Recovery Plan grants cover up to 65% of qualifying retrofit costs, driving rapid adoption in Milan and Rome. Nordic nations maintain an early adoption of digital twins, aided by high digital literacy and robust broadband infrastructure. Sweden funds pilots that merge building data with vehicle-to-grid systems. Spain and the Netherlands continue to grow steadily, with the latter focusing on circular economy goals that align with real-time material tracking.

Russia remains muted amid sanctions and vendor exits. Central and Eastern European capitals exhibit healthy demand for smart offices, but secondary cities lag due to financing gaps. Overall, the Europe Smart Office Market continues to broaden as EU policy coherence increases technology confidence among landlords and tenants alike.

Competitive Landscape

The top five vendors Siemens, Schneider Electric, Honeywell, Johnson Controls, and ABB commanded 42% of Europe Smart Office Market revenue in 2024. Traditional automation firms use installed bases and service arms to defend share, yet face commoditizing hardware margins. Cloud giants Microsoft and Google chase recurring analytics income through platform ties with Office 365 and Google Workspace.

Open standards advocacy and proprietary ecosystem battles run in parallel. Siemens and Schneider Electric back the Matter alliance yet also extend proprietary APIs for differentiated controls. Cybersecurity accreditation such as IEC 62443 certification is now a key tender requirement in health and finance sectors. Mid-market offices, often between 2,000 and 10,000 square meters, form a white-space opportunity for modular, cloud-managed bundles.

Partnership moves abound. Schneider Electric embedded Azure Digital Twins into EcoStruxure, while Johnson Controls linked OpenBlue with Google Vertex AI. Edge computing inside controllers allows local fault detection even if cloud links fail. Disruptors that combine desk booking, visitor check-in, and environmental feedback in one mobile app challenge incumbents by focusing on the employee experience rather than only infrastructure.

Europe Smart Office Industry Leaders

ABB Ltd.

Bosch Building Technologies GmbH

Cisco Systems, Inc.

CommScope Holding Company, Inc.

Crestron Electronics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Siemens bought a 60% stake in Italian automation firm Smartek to deepen mid-market reach.

- March 2025: Schneider Electric launched EcoStruxure Building Operation 2025 with generative AI chat for facility managers.

- February 2025: Honeywell won a USD 85 million contract to retrofit 120 NHS hospitals with smart systems.

- January 2025: Johnson Controls partnered with Google Cloud to add Vertex AI forecasting to OpenBlue.

Europe Smart Office Market Report Scope

The Europe smart office market refers to the ecosystem of digitally enabled workplace solutions such as connected hardware, intelligent software, and integrated services that enhance building efficiency, employee productivity, and workplace safety. It encompasses technologies such as smart lighting, HVAC control, energy management, security systems, sensors, and analytics, deployed across both new and retrofit buildings. Overall, the market focuses on creating automated, energy-efficient, and data-driven office environments across Europe.

The Europe Smart Office Market Report is Segmented by Product Type (Security and Access Control Systems, Energy Management Systems, Smart HVAC Control Systems, Smart Lighting Systems, Audio-Video Conferencing Systems, Fire and Safety Control Systems, Smart Sensors, Workplace Analytics Solutions, Others), Building Type (Retrofits, New Buildings), Connectivity Technology (Wired, Wireless), Offering (Hardware, Software, Services), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Government and Public Sector, Manufacturing, Retail and Hospitality, Education, Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Nordics, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Security and Access Control Systems |

| Energy Management Systems |

| Smart HVAC Control Systems |

| Smart Lighting Systems |

| Audio-Video Conferencing Systems |

| Fire and Safety Control Systems |

| Smart Sensors |

| Workplace Analytics Solutions |

| Others |

By Building Type

| Retrofits |

| New Buildings |

By Connectivity Technology

| Wired | |

| Wireless | Wi-Fi |

| Zigbee | |

| Bluetooth | |

| Z-Wave | |

| Thread | |

| Others |

By Offering

| Hardware | Sensors |

| Controllers and Actuators | |

| Networking Equipment | |

| Software | Building Management Platforms |

| Analytics and AI Software | |

| Services | Professional Services |

| Managed Services |

By End-User Industry

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing |

| Retail and Hospitality |

| Education |

| Others |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics |

| Russia |

| Rest of Europe |

| By Product Type | Security and Access Control Systems | |

| Energy Management Systems | ||

| Smart HVAC Control Systems | ||

| Smart Lighting Systems | ||

| Audio-Video Conferencing Systems | ||

| Fire and Safety Control Systems | ||

| Smart Sensors | ||

| Workplace Analytics Solutions | ||

| Others | ||

| By Building Type | Retrofits | |

| New Buildings | ||

| By Connectivity Technology | Wired | |

| Wireless | Wi-Fi | |

| Zigbee | ||

| Bluetooth | ||

| Z-Wave | ||

| Thread | ||

| Others | ||

| By Offering | Hardware | Sensors |

| Controllers and Actuators | ||

| Networking Equipment | ||

| Software | Building Management Platforms | |

| Analytics and AI Software | ||

| Services | Professional Services | |

| Managed Services | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Retail and Hospitality | ||

| Education | ||

| Others | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe Smart Office Market?

The market is worth USD 4.04 billion in 2025.

How fast is the Europe Smart Office Market expected to grow?

It is set to expand at a 15.52% CAGR through 2030.

Which product category leads revenue?

Smart Lighting Systems lead with 28.41% share in 2024.

Which country shows the quickest growth outlook?

Italy is projected to post a 16.81% CAGR from 2025 to 2030.

Who are the top vendors in the region?

Siemens, Schneider Electric, Honeywell, Johnson Controls, and ABB hold the largest combined share.

What is the main barrier for retrofits?

High upfront capital costs ranging from EUR 150-400 (USD 174.66 - 465.76) per square meter deter smaller landlords.