Market Size of Europe Security Services Industry

| Study Period | 2022 - 2029 |

| Base Year For Estimation | 2023 |

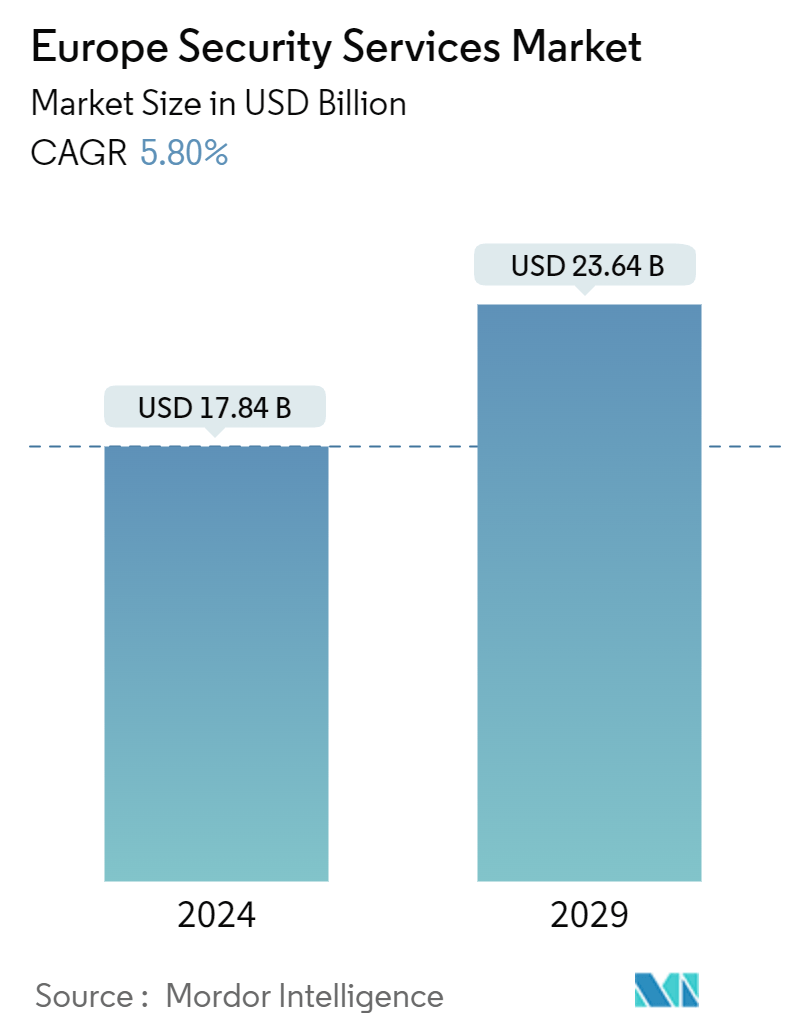

| Market Size (2024) | USD 17.84 Billion |

| Market Size (2029) | USD 23.64 Billion |

| CAGR (2024 - 2029) | 5.80 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Security Services Market Analysis

The Europe Security Services Market size is estimated at USD 17.84 billion in 2024, and is expected to reach USD 23.64 billion by 2029, growing at a CAGR of 5.80% during the forecast period (2024-2029).

- The demand for security services in Europe is rising due to various factors, such as regulatory requirements, an ever-changing threat environment, heightened awareness of cybersecurity threats, and the digital revolution. In addition, European organizations must adhere to industry-specific and international regulations, necessitating the provision of security services to ensure and sustain compliance. People increasingly recognize the value of SaaS (software-as-a-service) solutions, and integrating the physical and digital realms is leading to the development of increasingly sophisticated security systems, particularly in more developed markets.

- Cloud adoption has fundamentally altered how organizations store and exchange data, thus necessitating the demand for security services. As a result, cloud computing is enabling more efficient multi-site administration, integration of security technology solutions, and the ability to conduct security operations remotely. For instance, Flexera Software has identified cost savings and the migration of more workloads into the cloud as the most essential cloud initiatives in 2023 for European organizations, with 62% of respondents citing this as their top priority.

- Cyber threats are rising in Europe, as in any region worldwide. The prevalence of cyberattacks, ransomware attacks, data breaches, and other malicious activities is increasing, prompting organizations to invest in comprehensive cybersecurity strategies. For instance, according to ANSSI (National Information Systems Security Agency), in 2023, there were 110 major ransomware attacks in Europe. Additionally, in 2023, SMEs (small and medium enterprises) continued to be the primary victims of ransomware attacks. Hence, European organizations are exploring cybersecurity strategies to safeguard digital resources in a rapidly digitalizing environment.

- Organizations in the public sector may be subject to budgetary restrictions and administrative obstacles that may prevent them from utilizing security services. Many European organizations still use legacy IT infrastructure and technology that may need to be equipped with the most up-to-date security capabilities. The upkeep of these systems can prove to be laborious and expensive. In addition, as technology progresses, new vulnerabilities and threats are created. As a result, security services must be continually adjusted to address these new threats effectively. This factor can result in a need for more security service options, which can impede the market's growth.

- Moreover, in the current scenario, the macroeconomic situation remains volatile, and players continue to see macro trends such as high interest rates, inflation, fear of recession, and geopolitical tensions increasing in some parts of the world. For instance, the macroeconomic situation did not improve in 2023, with inflation rates and interest rates staying relatively high, and the fear of recession amid geopolitical conflicts remained. The continued macroeconomic uncertainty means customers in different market segments have remained cautious. A later recovery of markets is expected, and the timing and shape of the recovery slope remain unclear.

Europe Security Services Industry Segmentation

Security services are processes or comprehensive services that improve an organization's protection and security against common cyberattacks, including phishing, malicious software, and ransomware. These services encompass design and integration, deployment, risk and threat analysis, and consultation. Managed and hosted security services and solutions can be supplemented using cloud services, artificial intelligence (AI), biometrics, Internet of Things (IoT), and other remote services.

The European security services market is segmented by service type (managed security services, professional security services, consulting services, and threat intelligence security services), mode of deployment (on-premise and cloud), end-user industry (IT and infrastructure, government, industrial, healthcare, transportation and logistics, banking, and other end-user industries), and country (United Kingdom, Germany, France, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Service Type | |

| Managed Security Services | |

| Professional Security Services | |

| Consulting Services | |

| Threat Intelligence Security Services |

| By Mode of Deployment | |

| On-premise | |

| Cloud |

| By End-user Industry | |

| IT and Infrastructure | |

| Government | |

| Industrial | |

| Healthcare | |

| Transportation and Logistics | |

| Banking | |

| Other End-User Industries |

| By Country*** | |

| United Kingdom | |

| Germany | |

| France | |

| Italy | |

| Spain |

Europe Security Services Market Size Summary

The European security services market is experiencing significant growth, driven by the increasing demand for robust security solutions across various sectors. This demand is fueled by the need to comply with stringent regulatory requirements, the evolving threat landscape, and the rapid digital transformation. Organizations are increasingly adopting cloud-based solutions, which offer flexibility and cost savings but also introduce new security challenges. The integration of physical and digital security systems is becoming more sophisticated, particularly in developed markets, as businesses seek to protect sensitive data and ensure compliance with regulations like the General Data Protection Regulation (GDPR). The rise in cyber threats, including ransomware and data breaches, has further propelled the need for comprehensive cybersecurity strategies, prompting organizations to invest in managed security services and advanced security technologies.

The market is characterized by a fragmented landscape with numerous players offering a wide range of security services. Companies are leveraging partnerships and collaborations to enhance their service offerings and expand their market presence. The transition from on-premises to cloud platforms is accelerating the development of cloud-based security solutions, which are essential for managing the increasing volume of data and processing requirements. Despite the challenges posed by macroeconomic uncertainties, such as high inflation and geopolitical tensions, the market is poised for growth as organizations continue to prioritize cybersecurity investments. Key players in the market, including Fortra LLC, G4S Limited, and Palo Alto Networks, are actively developing and deploying innovative security solutions to address the evolving needs of European businesses.

Europe Security Services Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Service Type

-

2.1.1 Managed Security Services

-

2.1.2 Professional Security Services

-

2.1.3 Consulting Services

-

2.1.4 Threat Intelligence Security Services

-

-

2.2 By Mode of Deployment

-

2.2.1 On-premise

-

2.2.2 Cloud

-

-

2.3 By End-user Industry

-

2.3.1 IT and Infrastructure

-

2.3.2 Government

-

2.3.3 Industrial

-

2.3.4 Healthcare

-

2.3.5 Transportation and Logistics

-

2.3.6 Banking

-

2.3.7 Other End-User Industries

-

-

2.4 By Country***

-

2.4.1 United Kingdom

-

2.4.2 Germany

-

2.4.3 France

-

2.4.4 Italy

-

2.4.5 Spain

-

-

Europe Security Services Market Size FAQs

How big is the Europe Security Services Market?

The Europe Security Services Market size is expected to reach USD 17.84 billion in 2024 and grow at a CAGR of 5.80% to reach USD 23.64 billion by 2029.

What is the current Europe Security Services Market size?

In 2024, the Europe Security Services Market size is expected to reach USD 17.84 billion.