Europe Satellite Launch Vehicle Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.47 Billion |

| Market Size (2030) | USD 1.09 Billion |

| Growth Rate (2025 - 2030) | 18.26% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Satellite Launch Vehicle Market Analysis by Mordor Intelligence

The Europe Satellite Launch Vehicle Market size is estimated at 0.47 billion USD in 2025, and is expected to reach 1.09 billion USD by 2030, growing at a CAGR of 18.26% during the forecast period (2025-2030).

The European satellite launch vehicle industry has established itself as a cornerstone of space manufacturing, representing the second-largest space manufacturing activity after commercial satellite development. The industry's infrastructure is anchored by Europe's spaceport in French Guiana, which serves as the primary launch site for major vehicles including Ariane 5, Soyuz, and Vega. The European Space Agency (ESA) has demonstrated its commitment to strengthening the industry's foundation by requesting a substantial budget of ¬18.5 billion for 2023-2025 from its 22 member nations. This strategic investment reflects the growing importance of space capabilities and the need to maintain European autonomy in space launch access.

The market is witnessing significant technological advancement and modernization of launch services capabilities. A prime example is the development of Ariane 6, which represents the next generation of European launch vehicles with its maiden flight scheduled for late 2023. The new launcher has already secured eleven contracts for launches between 2023-2027, demonstrating strong market confidence in European launch capabilities. These developments are complemented by the industry's focus on developing reusable and eco-friendly launchers, with multiple projects being pursued under the European Commission's Horizon Europe research framework program.

Individual European nations are making substantial investments to strengthen their space capabilities and infrastructure. France has allocated approximately $9 billion to space activities, marking a significant commitment to the sector, while Germany has dedicated ¬2.37 billion for various space-related projects. These investments are driving innovation in launch system technology and supporting the development of more efficient and cost-effective launch solutions. The industry's robust financial backing is enabling the development of diverse satellite launcher options, from light to heavy-lift capabilities, meeting various payload requirements and mission objectives.

The market is characterized by a strong emphasis on international collaboration and commercial partnerships. Space organizations like ESA have established strategic partnerships with private players, fostering innovation and competitive service offerings in the launch vehicle sector. The industry has demonstrated remarkable efficiency in satellite deployment, with over 590 satellites launched during the 2017-2022 period, showcasing the region's growing launch capabilities and infrastructure maturity. This collaborative approach, combined with technological advancement, is positioning Europe as a key player in the global space transportation market, capable of serving both institutional and commercial launch requirements.

Europe Satellite Launch Vehicle Market Trends and Insights

Growing demand and competition in the European launch vehicle market

- European launch vehicles are known for their versatility, capable of launching a wide range of payloads into various orbits. A key factor driving the demand for European launch vehicles is the growing commercial space industry. As more and more companies seek to launch satellites and other space-based assets into orbit, they are turning to European launch vehicles as a reliable and cost-effective solution. European launch companies are investing in new technologies, such as reusable launch vehicles, electric propulsion systems, and artificial intelligence, to improve their launch capabilities and stay competitive in the market. For example, ArianeGroup is developing the Ariane Next reusable rocket, and Airbus is developing the Adeline concept, which involves a reusable first stage for the Ariane rocket.

- Additionally, the demand for small satellite launches is increasing, which is driving the development of smaller launch vehicles by European companies. For example, PLD Space is developing the Miura 1 and Miura 5 rockets for small satellite launches, while Isar Aerospace is developing the Spectrum rocket for the same purpose. There is a growing trend toward international collaboration in the space industry, with European launch vehicle manufacturers partnering with companies and organizations across the world. This is driven by the increasing complexity of space missions, as well as the need to share resources and expertise. On this note, Arianespace has partnerships with the European Space Agency and the French Space Agency, and PLD Space is working with the European Space Agency and the Spanish government.

Increasing investment opportunities in the European satellite launch vehicle market is the driver

- European countries are recognizing the importance of various investments in the space domain. They are increasing their spending on various space programs to stay competitive and innovative in the global space industry. In November 2022, the European Space Agency (ESA) announced that it requested its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. Europe plans to launch the first Ariane 6 rocket, its next-generation space launcher, in the fourth quarter of 2023. Developed at a cost of just under USD 3.9 billion and originally set for an inaugural launch in July 2020, the project has been hit by a series of delays. The governments of France, Germany, and Italy announced that they had signed an agreement on "the future of launcher exploitation in Europe" to enhance the competitiveness of European vehicles while also ensuring independent European access to space.

- In September 2022, the French government announced that it is planning to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years. In November 2022, Germany announced that about EUR 2.37 billion was allocated for various space-related projects. The country mentioned that from the end of 2023, Ariane 6 is expected to be the new European launcher to carry payloads into space. Germany is contributing a total of EUR 162 million to the further development of Ariane 6 and its market introduction. The country is investing around EUR 52 million in the optional LEAP (Launchers Exploitation Accompaniment) program, which also includes the operation of DLR's test facility for rocket engines in Lampoldshausen.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The demand for satellite miniaturization is the driver in Europe

Segment Analysis: Orbit Class

LEO Segment in Europe Satellite Launch Vehicle Market

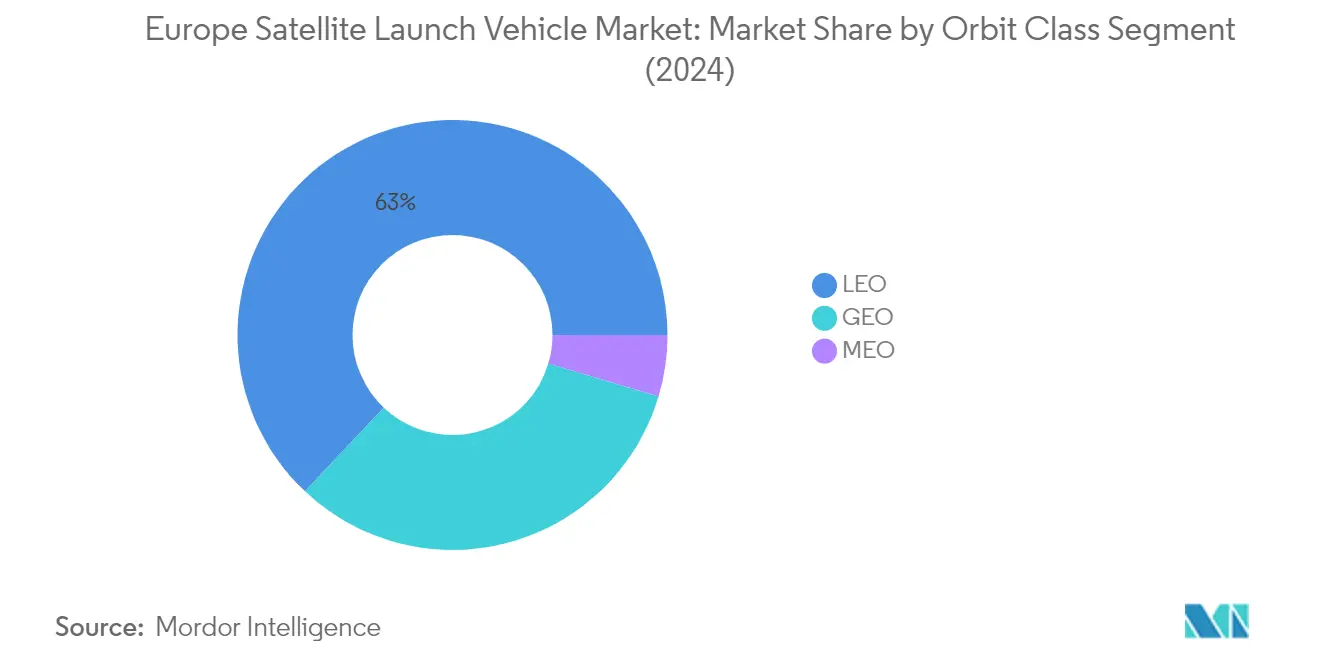

The Low Earth Orbit (LEO) segment dominates the Europe Satellite Launch Vehicle Market, commanding approximately 63% market share in 2024. This significant market position is primarily driven by the increasing deployment of communication satellites, military surveillance systems, and Earth observation platforms in low Earth orbit. The segment's dominance is further strengthened by the growing demand from commercial operators who prefer LEO satellites for their lower latency and reduced signal propagation delays. European organizations have been particularly active in this segment, with multiple satellites being utilized for various applications including communication, military, government, and commercial purposes. The preference for LEO launches is also influenced by factors such as lower operational costs, reduced risks, and shorter mission timeframes compared to other orbital deployments.

LEO Segment Growth in Europe Satellite Launch Vehicle Market

The Low Earth Orbit (LEO) segment is projected to experience the most rapid growth in the Europe Satellite Launch Vehicle Market, with an expected growth rate of approximately 24% during 2024-2029. This remarkable growth trajectory is driven by several factors, including the increasing miniaturization of satellites, advancements in launch vehicle technology, and the growing demand for high-speed internet connectivity through satellite constellations. European space companies are actively developing strategic partnerships and investing in new launch vehicle capabilities specifically designed for LEO missions. The segment's growth is further supported by the expanding applications of LEO satellites in Earth observation, climate monitoring, and telecommunications, along with the increasing adoption of small satellite constellations by both commercial and government entities.

Remaining Segments in Orbit Class

The Geostationary Earth Orbit (GEO) and Medium Earth Orbit (MEO) segments continue to play vital roles in the European satellite launch vehicle market. GEO launches remain crucial for telecommunications and weather monitoring satellites, offering advantages in terms of continuous coverage over specific geographical areas. The MEO segment serves as an essential middle ground, particularly valuable for navigation and positioning satellites, offering a balance between orbital height and signal strength. Both segments complement the LEO market by providing different capabilities and serving specific mission requirements that cannot be fulfilled by low Earth orbit satellites, thereby maintaining a comprehensive orbital infrastructure for various space applications.

Segment Analysis: Launch Vehicle MTOW

Medium Segment in Europe Satellite Launch Vehicle Market

The medium launch vehicle segment dominates the European satellite launch vehicle market, accounting for approximately 51% market share in 2024. Medium launch vehicles are critical for launching satellites, conducting scientific missions, and resupplying the International Space Station, with payload capacities between 2,000 kg and 20,000 kg. Key players like Arianespace's Ariane 5 can carry payloads weighing more than 10 metric tons to geostationary transfer orbit and 20 metric tons to LEO, while Soyuz family rockets (Soyuz-2.1a and Soyuz-2.1b) can lift 7,020-8,200 kg to LEO. The segment's prominence is driven by the versatility of medium launch vehicles in accommodating a wide range of payload requirements, from commercial satellites to government missions. The increasing number of satellites being launched into orbit due to rising space activities continues to fuel demand for medium-range launch vehicles, making them an essential component of Europe's space infrastructure.

Light Segment in Europe Satellite Launch Vehicle Market

The light launch vehicle segment is experiencing the most rapid growth in the European satellite launch vehicle market, with a projected growth rate of approximately 31% during 2024-2029. This exceptional growth is driven by the expanding capabilities of small satellites and the space industry's strategic development of next-generation small satellite launchers. Light launch vehicles, designed for payloads under 2,000 kg (ESA classification) or 5,000 kg (Roscosmos classification), are gaining traction due to their cost-effectiveness and flexibility in launching small satellites. The European Space Agency's initiatives in testing new navigation satellites that orbit closer to Earth than existing ones have created additional opportunities for light launch vehicles. The segment's growth is further supported by various stakeholders, including governments, space agencies, and private companies, who are investing in expanding small satellite launch capabilities to meet the increasing demand for dedicated small satellite launch services.

Remaining Segments in Launch Vehicle MTOW

The heavy launch vehicle segment represents a crucial component of Europe's space launch capabilities, designed for payloads exceeding 20,000 kg. These vehicles are essential for launching large communication satellites, major ISS resupply missions, and interplanetary missions. The segment benefits from ongoing developments in reusable launch technology and next-generation heavy-lift vehicles. Major space agencies in the region, including ESA, have developed heavy launch vehicles and collaborated with private players such as SpaceX and Blue Origin for advancing heavy-lift launch vehicle technology. The segment's significance is particularly evident in missions requiring substantial payload capacity, such as launching multiple satellites in a single mission or deploying large space station modules.

Europe Satellite Launch Vehicle Market Geography Segment Analysis

Europe Satellite Launch Vehicle Market in Russia

Russia maintains its dominant position in the European satellite launch vehicle market, holding approximately 40% market share in 2024. The country's space program is primarily driven by Roscosmos, which has established itself as a key player in both commercial and military satellite launches. Russia's commitment to expanding its space capabilities is evident through its focus on developing anti-access/area-denial capabilities in outer space, enhancing communication systems sustainability, and advancing offensive capabilities against ground-based space infrastructure. The country operates more than 160 satellites, including 100 military satellites, demonstrating its strong military space presence. The Russian government's substantial investment in space programs, particularly in military satellite constellation development and space transportation vehicles, underscores its commitment to maintaining its competitive edge in the space sector. The country's success in developing advanced launch vehicles like the Proton rocket series, featuring sophisticated technologies such as the six-first-stage RD-276 engine setup, has further strengthened its market position.

Europe Satellite Launch Vehicle Market in France

France has emerged as a significant player in the European satellite launch vehicle market, with its space activities primarily coordinated by the National Centre for Space Studies (CNES). The country's strategic approach to space exploration is evident through its comprehensive regulatory framework and substantial investments in space infrastructure. France's space industry benefits from its hosting of Europe's primary spaceport in French Guiana, which serves as the launch site for major European launch vehicles including Ariane 5 and Vega. The country's space sector is characterized by strong collaboration between public and private entities, with companies like ArianeGroup playing crucial roles in developing next-generation launch vehicles. France's commitment to advancing its space capabilities is reflected in its focus on developing reusable and eco-friendly launchers, as well as its emphasis on maintaining independent European access to space. The country's space industry also benefits from robust government support and clear regulatory guidelines under the French Space Operations Act.

Europe Satellite Launch Vehicle Market in Germany

Germany has established itself as a crucial player in the European satellite launch vehicle market through its advanced technological capabilities and strong institutional framework. The German Aerospace Center (DLR) leads the country's space activities, coordinating various space programs and representing Germany's interests at the international level. The country's space industry is characterized by its focus on innovative technologies and sustainable space operations. Germany's contribution to European space initiatives is particularly notable in the development of launch vehicle components and systems. The country's space sector benefits from strong collaboration between research institutions, industry players, and government agencies. Germany's commitment to advancing space technology is evident through its investment in various space-related projects and its active participation in European space programs. The country's space industry also focuses on developing cutting-edge technologies for satellite operations and launch vehicle systems.

Europe Satellite Launch Vehicle Market in United Kingdom

The United Kingdom has positioned itself as an emerging force in the European space vehicle market, with a strong focus on developing its domestic space capabilities. The country's space sector is regulated by the Civil Aviation Authority (CAA), which oversees all Space Industry Act regulatory functions and orbital activities. The UK's approach to space activities is characterized by its emphasis on commercial space operations and innovative launch technologies. The country has developed a comprehensive regulatory framework that encourages private sector participation while maintaining high safety and environmental standards. The UK's space industry benefits from strong government support and clear regulatory guidelines under the Space Industry Act 2018. The country's focus on developing domestic launch capabilities and supporting international collaboration has helped create a dynamic and growing space sector. The UK's strategic approach to space activities includes emphasis on both orbital and suborbital spaceflight activities.

Europe Satellite Launch Vehicle Market in Other Countries

Other European countries contribute significantly to the continent's space carrier market through various specialized capabilities and collaborative initiatives. These nations participate in European space programs through partnerships with major space agencies and private sector entities. Countries like Italy, with its expertise in launch vehicle components, and Spain, with its growing space technology sector, play important roles in the European space ecosystem. The collaborative nature of European space activities allows smaller nations to contribute specialized technologies and expertise to major launch vehicle programs. These countries often focus on developing specific components or technologies that complement the larger European space infrastructure. The integrated approach to space activities in Europe enables these nations to participate in major launch vehicle programs while developing their domestic space capabilities. This collaborative framework has helped create a robust and diverse European space sector that continues to advance launch vehicle technologies and capabilities.

Competitive Landscape

Top Companies in Europe Satellite Launch Vehicle Market

The European satellite launch vehicle market features established players like Roscosmos, Ariane Group, Mitsubishi Heavy Industries, Avio, and China Aerospace Science and Technology Corporation leading the industry. These companies are heavily investing in developing next-generation launch vehicles with enhanced capabilities and reusability features to meet evolving market demands. Product innovation focuses on developing eco-friendly launchers, improving payload capacity, and incorporating advanced propulsion technologies. Companies are expanding their operational footprint through strategic partnerships with space agencies and commercial entities while simultaneously working on cost reduction through manufacturing optimization and supply chain improvements. The industry is witnessing increased collaboration between established players and emerging companies to develop innovative launch services, particularly in the small satellite segment, while maintaining high reliability standards and safety protocols.

Consolidated Market with Strong Government Ties

The European satellite launch vehicle market demonstrates high consolidation, with the top players accounting for a significant market share through their established launch system programs and government contracts. These dominant players are primarily large aerospace conglomerates with diverse portfolios spanning multiple segments of the space industry, supported by strong government backing and extensive research and development capabilities. The market structure is characterized by high entry barriers due to substantial capital requirements, complex technological expertise, and stringent regulatory requirements.

The competitive dynamics are shaped by long-term relationships between launch service providers and government space agencies, particularly ESA and national space organizations. Market participants are increasingly focusing on vertical integration strategies to maintain control over critical components and technologies. While mergers and acquisitions activity remains limited due to national security considerations and government oversight, strategic partnerships and joint ventures are becoming more common, especially in developing new space launch vehicle technologies and accessing new market segments.

Innovation and Flexibility Drive Future Success

Success in the European satellite launch vehicle market increasingly depends on companies' ability to offer flexible launch services while maintaining cost competitiveness. Incumbent players must focus on developing modular launch vehicle designs that can accommodate various payload sizes and orbit requirements while investing in reusable technology to reduce launch costs. Companies need to strengthen their position through vertical integration of critical technologies, development of proprietary launch systems, and establishment of robust supply chains to ensure operational reliability and market competitiveness.

For new entrants and challenger companies, success lies in identifying and exploiting niche market segments, particularly in the small satellite launch sector. These companies must focus on developing innovative launch technologies, establishing strategic partnerships with satellite manufacturers and operators, and maintaining strong relationships with regulatory bodies. The ability to offer rapid launch capabilities, competitive pricing, and reliable services while navigating complex regulatory requirements will be crucial for gaining market share. Companies must also consider environmental sustainability and space debris mitigation in their launch vehicle designs to align with increasing regulatory focus on space environment protection.

Europe Satellite Launch Vehicle Industry Leaders

-

Ariane Group

-

Avio

-

China Aerospace Science and Technology Corporation (CASC)

-

Mitsubishi Heavy Industries

-

ROSCOSMOS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: ISRO launched 36 communication satellites of Oneweb aboarding its LVM3 rocket into LEO.

- April 2022: The Long March 3B rocket was launched from the Xichang launch base with the Chinasat 6D, or Zhongxing 6D, communications satellite.

- March 2022: Boeing and MT Aerospace AG, which is a subsidiary of OHB SE, have signed a contract to supply structural components for NASA's Space Launch System (SLS)

Europe Satellite Launch Vehicle Market Report Scope

GEO, LEO, MEO are covered as segments by Orbit Class. Heavy, Light, Medium are covered as segments by Launch Vehicle Mtow. Russia are covered as segments by Country.| GEO |

| LEO |

| MEO |

| Heavy |

| Light |

| Medium |

| Russia |

| Orbit Class | GEO |

| LEO | |

| MEO | |

| Launch Vehicle Mtow | Heavy |

| Light | |

| Medium | |

| Country | Russia |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.