Europe Rotor Blade Market Size

| Study Period | 2019-2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

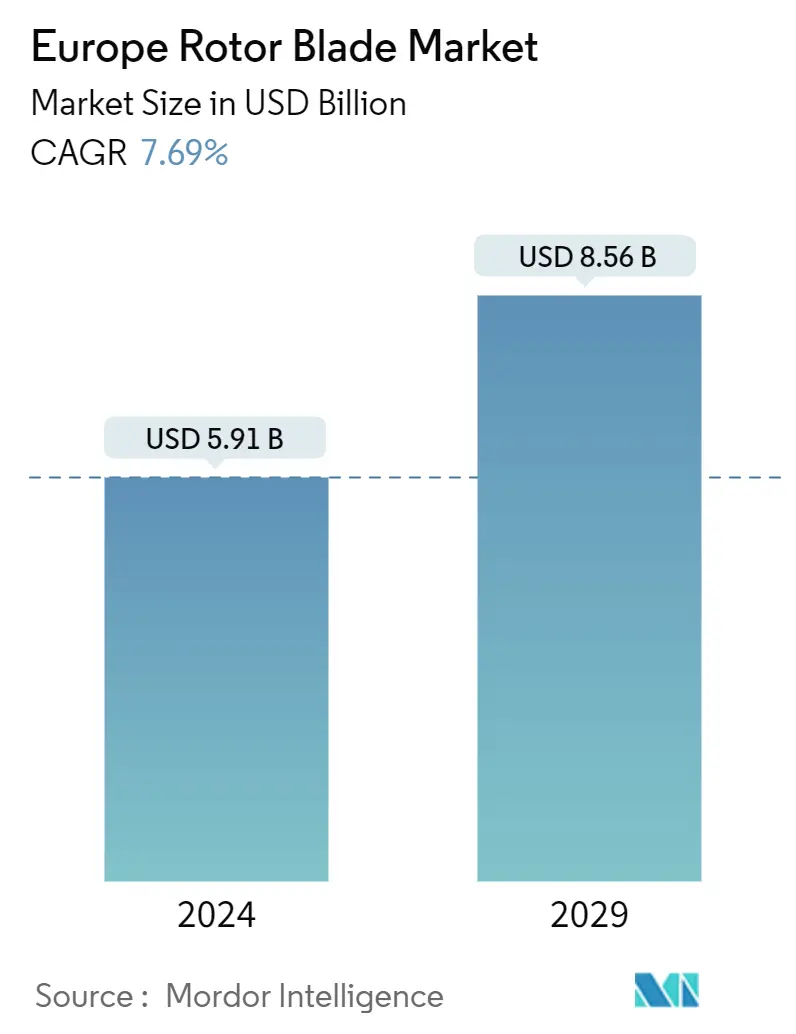

| Market Size (2024) | USD 5.91 Billion |

| Market Size (2029) | USD 8.56 Billion |

| CAGR (2024 - 2029) | 7.69 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Rotor Blade Market Analysis

The Europe Rotor Blade Market size is estimated at USD 5.91 billion in 2024, and is expected to reach USD 8.56 billion by 2029, growing at a CAGR of 7.69% during the forecast period (2024-2029).

- Over the medium term, factors such as the growing number of offshore and onshore wind energy installations, the declining cost of wind energy, and increasing investments in the wind power sector are anticipated to drive the Europe rotor blade market during the forecast period.

- On the other hand, factors such as the accompanying high cost of transportation and cost competitiveness of alternate clean power sources like solar power, hydropower, etc., can potentially restrain the market growth during the forecast period.

- Nevertheless, the wind power business has sought cost-effective solutions, and a highly efficient product has the ability to alter the industry's dynamics. There were instances where old turbines were replaced not owing to damage but because more effective blades were sold in the market. Thus, technological advancements eventually create a wonderful opportunity for the market of rotor blades.

Europe Rotor Blade Market Trends

Offshore Segment to Dominate the Market

- Europe accounted for 18.59 GW of new wind installed capacity in 2022. The electricity demand in Europe has increased after the departure of the pandemic, coupled with the commencement of industrial activities and rapid urbanization. The region has also witnessed a growing share of renewables to fulfill the increasing electricity demand.

- Europe is considered to have ample renewable energy resources to generate electricity, such as solar, wind, hydro, biomass, geothermal, etc. A good number of countries in Europe have become at the forefront of utilizing renewable energy globally. Factors such as decarbonization, sustainability of power systems, ambitious targets, and clean energy transition have driven the offsore wind energy market of Europe.

- In December 2022, the European Commission approved the 2023 Renewable Energy Sources Act, and the 2023 Offshore Wind Energy Act aims to improve the environment and focus on achieving a greenhouse gas-neutral electricity supply in the power market of Europe.

- Further, in May 2022, the European Commission published the REPowerEU plan, which contains a series of concrete measures designed to phase out Russian fossil fuels and boost the production of renewable energy in the EU. This plan would help further develop offshore wind energy in the region.

- With the REPowerEU announcement, the Esbjerg Declaration was formed to achieve the further expansion of offshore wind and decided to jointly develop The North Sea as a Green Power Plant of Europe, an offshore renewable energy system connecting Belgium, Denmark, Germany, and the Netherlands, and possibly other North Sea partners, including the members of the North Seas Energy Cooperation (NSEC) and set out a new target of 150 GW of offshore wind by 2050.

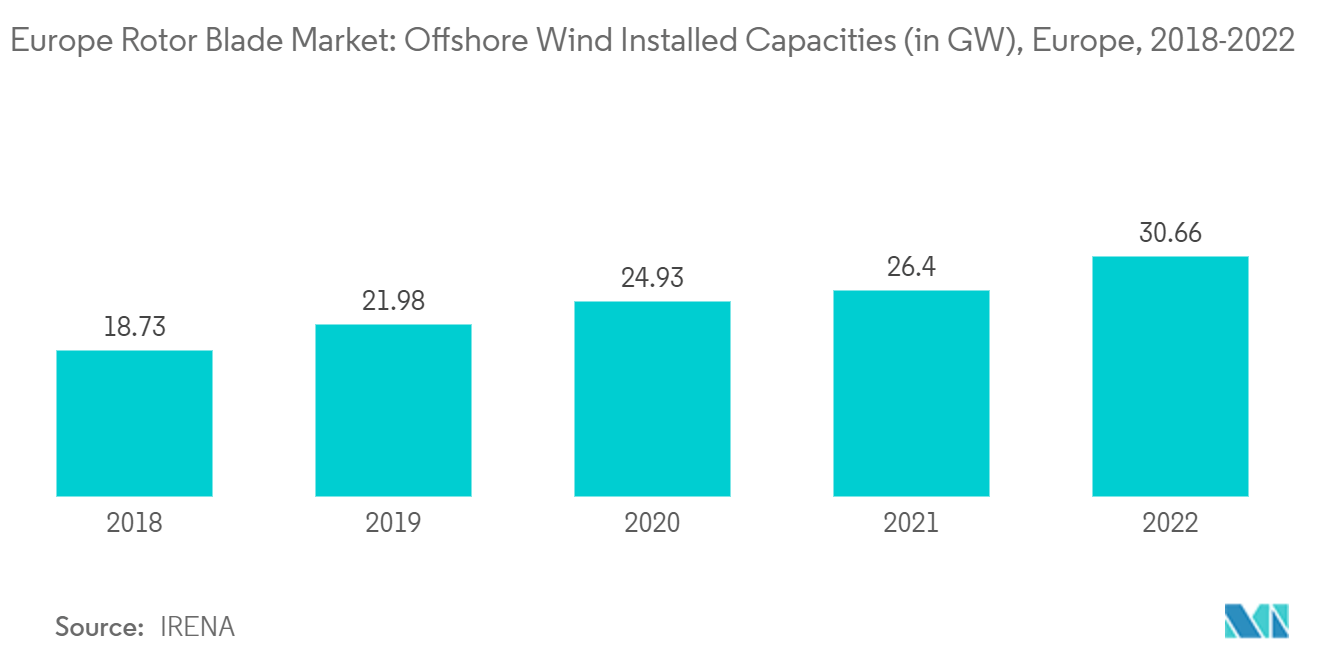

- According to International Renewable Energy Agency, Europe is among the leading regions in the global offshore wind power market. In 2022, it added 4,264 MW, reaching 30.66 GW. In March 2022, the French government entered into an offshore sector agreement with France's wind industry. The agreement recognizes that offshore wind is a significant and vital opportunity and commits to developing 40 GW of offshore wind by 2050 spread over 50 wind farms. This is expected to witness considerable development in offshore wind power.

- Also in June 2022, The Killybegs Fishermen’s Organization and Sinbad Marine Services have proposed a floating wind farm to be built offshore Donegal, Ireland, and have signed a Memorandum of Understanding with Swedish floating wind developer and technology provider, Hexicon.

- Therefore, owing to the above points, the offshore segment is anticipated to dominate the market during the forecast period.

United Kingdom to Dominate the Market

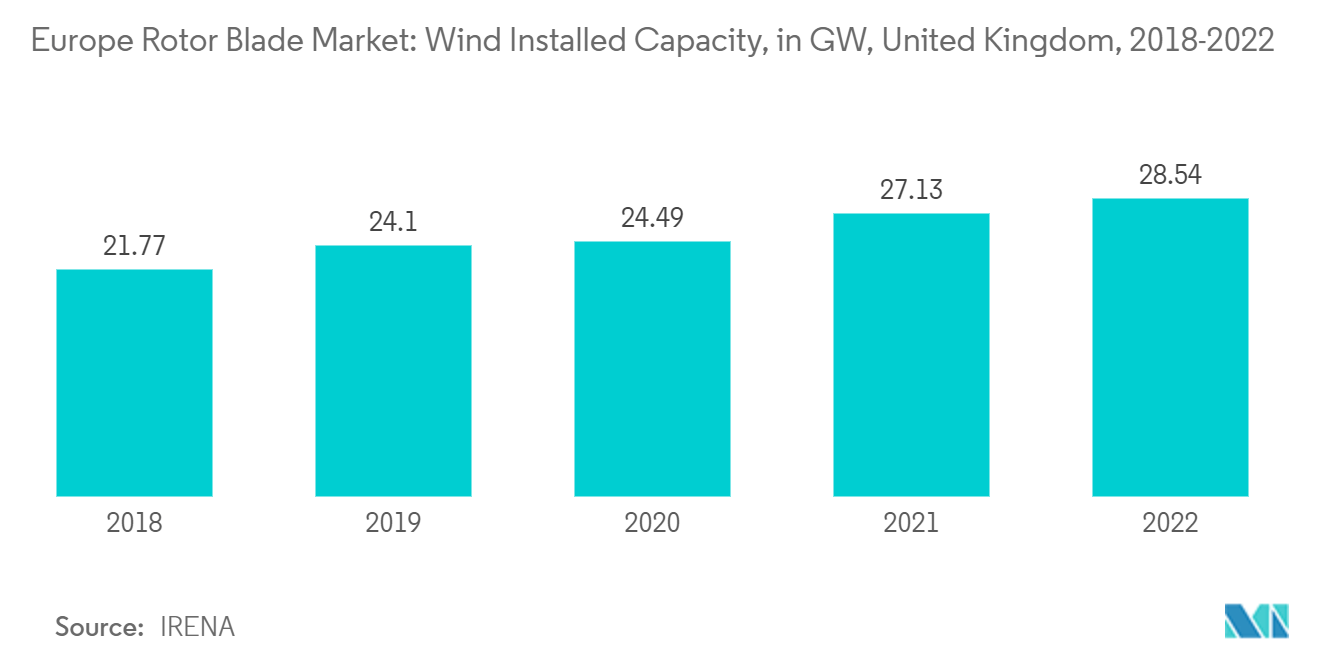

- The United Kingdom is one of the growing countries in wind energy generation. The country stands as the best location for wind power in Europe. By 2022, the United Kingdom installed a wind capacity of 28.54 GW.

- Moreover, the United Kingdom is not heavily affected by the Russia-Ukraine conflict compared to the other EU countries, Since the country is not dependent on the Russian gas supply. However, in April 2022, the former UK Prime Minister implemented an energy security strategy to lessen the war impact and boost renewable energy development within the country. This will, in turn, support the growth of the wind energy market and further aid the development of the wind rotor blade market.

- Since the country is one of the forerunners in offshore wind projects, between 2016 and 2021, nearly USD 25.79 billion was invested in offshore wind in the United Kingdom, witnessing a favorable investment environment in the offshore wind sector.

- Furthermore, in April 2022, the government announced a strategic plan to boost Britain's energy security, including an increased target of up to 50 GW of operating offshore wind capacity by 2030. The 50GW offshore wind target includes 5 GW of large-scale floating wind installations.

- Moreover, in January 2022, the UK government announced more than USD 82.5 million of public and private funding to advance research and development in floating offshore wind projects. The government plans to invest USD 41.9 million in 11 projects as part of the Floating Offshore Wind Demonstration Program.

- Therefore, owing to the above points, the United Kingdom is anticipated to dominate the market during the forecast period.

Europe Rotor Blade Industry Overview

The Europe rotor blade market is fragmented in nature. Some of the major players in the market (in no particular order) include Nordex SE, Siemens Gamesa Renewable Energy, SA, Vestas Wind Systems A/S, Suzlon Energy Limited, and LM Wind Power (a GE Renewable Energy business), among others.

In February 2022, Nordex announced that it would cease the production of rotor blades at the Rostock GVZ rotor blade site in Germany by the end of June 2022. The decision has been taken primarily due to a shift towards larger blades that are not manufactured at Rostock.

Europe Rotor Blade Market Leaders

-

Nordex SE

-

Siemens Gamesa Renewable Energy SA

-

Vestas Wind Systems A/S

-

Suzlon Energy Limited

-

LM Wind Power (a GE Renewable Energy business)

*Disclaimer: Major Players sorted in no particular order

Europe Rotor Blade Market News

- January 2024: Vestas announced its decision to establish a new blade factory in Szczecin region of Poland that is planned to produce blades for Vestas flagship offshore wind turbine, the V236-15.0 MW, and is expected to start operations in 2026.

- September 2023: Memmingham, a manufacturer of lifting equipment for the installation of wind turbine rotor blades, has launched a new generation of its popular RBC-D range of installation yoke: the RBC-D50.1.

Europe Rotor Blade Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing number of offshore and onshore wind energy installations

4.5.1.2 Declining cost of wind energy

4.5.2 Restraints

4.5.2.1 Increasing Competition from Alternate Renewable Energy Sources

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Location of Deployment

5.1.1 Onshore

5.1.2 Offshore

5.2 Blade Material

5.2.1 Carbon Fiber

5.2.2 Glass Fiber

5.2.3 Other Blade Materials

5.3 Geography

5.3.1 Germany

5.3.2 France

5.3.3 Spain

5.3.4 United Kingdom

5.3.5 Italy

5.3.6 NORDIC

5.3.7 Turkery

5.3.8 Russia

5.3.9 Rest of Europe

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Nordex SE

6.3.2 Siemens Gamesa Renewable Energy SA

6.3.3 Vestas Wind Systems A/S

6.3.4 Suzlon Energy Limited

6.3.5 Enercon GmbH

6.3.6 LM Wind Power (a GE Renewable Energy business)

6.3.7 BayWa R.E AG

- *List Not Exhaustive

6.4 Market Ranking/Share Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Development of High Efficiency and light weight wind turbines

Europe Rotor Blade Industry Segmentation

Rotor blades are the key components of wind turbines, as they are in direct contact with high-speed winds. Rotor blades convert the wind's kinetic energy into rotational energy, which is later converted into electrical energy.

Europe's rotor blade market is segmented by location of deployment, blade material, and geography. By location of deployment, the market is segmented into onshore and offshore. By blade material, the market is segmented by carbon fiber, glass fiber, and other blade materials. The report also covers the market size and forecasts for the rotor blade market across significant countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Location of Deployment | |

| Onshore | |

| Offshore |

| Blade Material | |

| Carbon Fiber | |

| Glass Fiber | |

| Other Blade Materials |

| Geography | |

| Germany | |

| France | |

| Spain | |

| United Kingdom | |

| Italy | |

| NORDIC | |

| Turkery | |

| Russia | |

| Rest of Europe |

Europe Rotor Blade Market Research Faqs

How big is the Europe Rotor Blade Market?

The Europe Rotor Blade Market size is expected to reach USD 5.91 billion in 2024 and grow at a CAGR of 7.69% to reach USD 8.56 billion by 2029.

What is the current Europe Rotor Blade Market size?

In 2024, the Europe Rotor Blade Market size is expected to reach USD 5.91 billion.

Who are the key players in Europe Rotor Blade Market?

Nordex SE, Siemens Gamesa Renewable Energy SA, Vestas Wind Systems A/S, Suzlon Energy Limited and LM Wind Power (a GE Renewable Energy business) are the major companies operating in the Europe Rotor Blade Market.

What years does this Europe Rotor Blade Market cover, and what was the market size in 2023?

In 2023, the Europe Rotor Blade Market size was estimated at USD 5.46 billion. The report covers the Europe Rotor Blade Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Europe Rotor Blade Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe Rotor Blade Industry Report

Statistics for the 2024 Europe Rotor Blade market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe Rotor Blade analysis includes a market forecast outlook to for 2024 to 2029) and historical overview. Get a sample of this industry analysis as a free report PDF download.

Europe Rotor Blade Market Report Snapshots