Europe Rigid Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

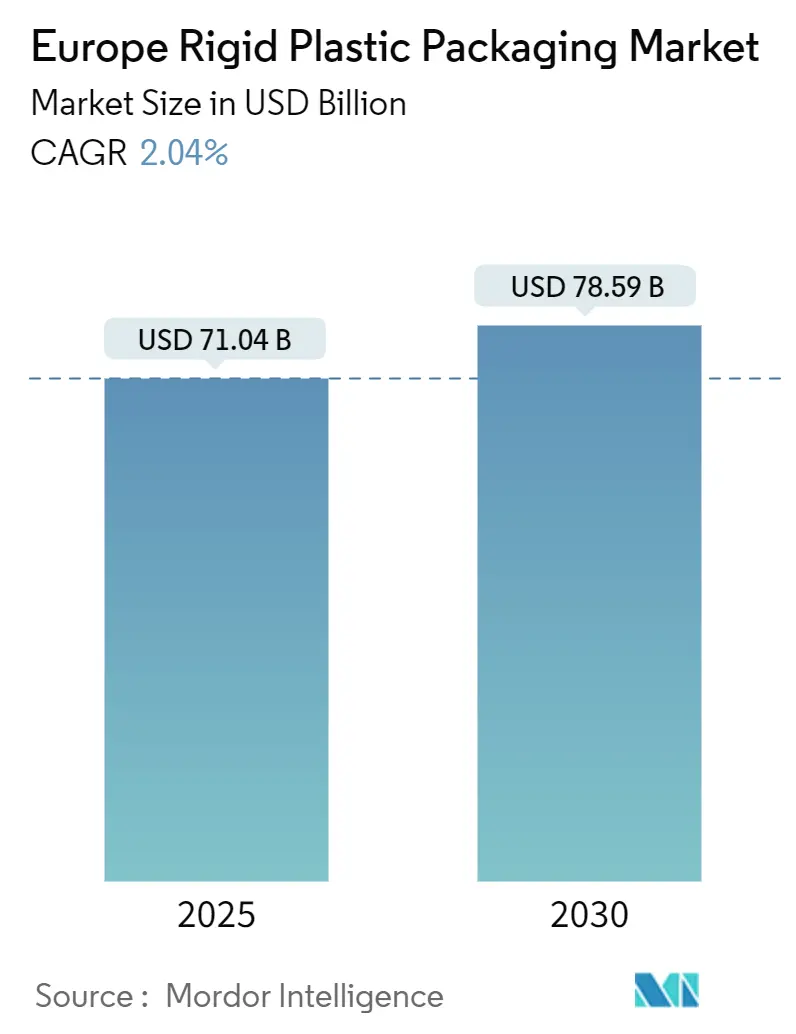

| Market Size (2025) | USD 71.04 Billion |

| Market Size (2030) | USD 78.59 Billion |

| Growth Rate (2025 - 2030) | 2.04% CAGR |

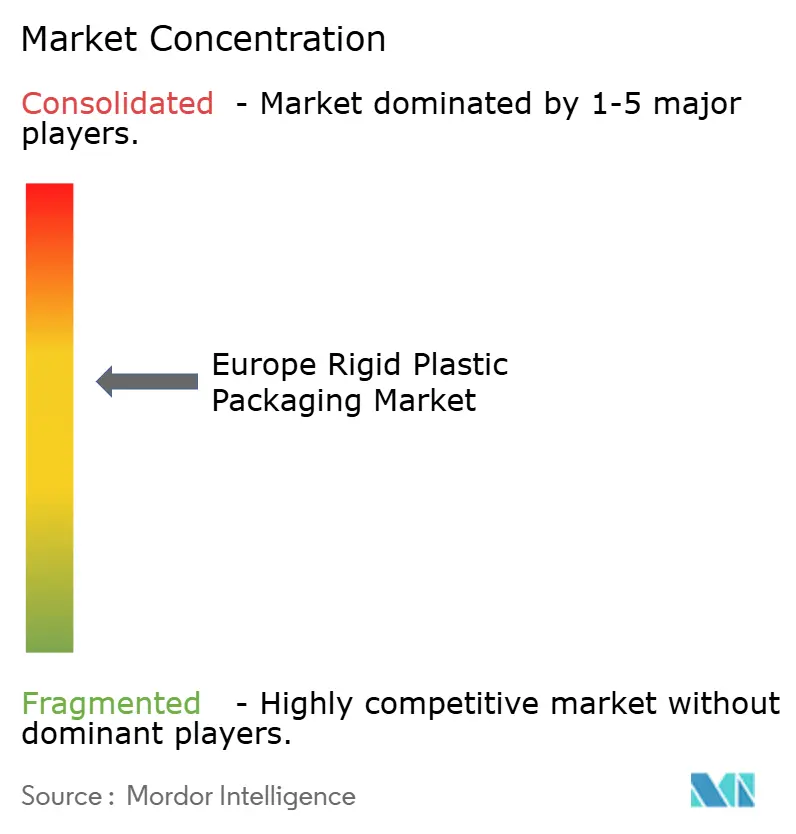

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The Europe rigid plastic packaging market size reached USD 71.04 billion in 2025 and is forecast to expand to USD 78.59 billion by 2030 at a 2.04% CAGR, reflecting the sector’s steady adaptation to ambitious EU circular-economy mandates. Stricter collection targets, minimum recycled-content thresholds, and material taxes are reshaping design choices, procurement strategies, and capital allocation. Deposit-return schemes (DRS) underpin rising recycled PET demand, while energy-price volatility and feedstock inflation accelerate operational efficiency programs. Large converters pursue mergers to pool compliance resources, and producers that invest early in closed-loop infrastructure secure commercial advantages with beverage, food, and healthcare brand owners. Material substitution pressures from fiber-based alternatives intensify competition, yet rigid formats retain defensible positions wherever high barrier, reusability, or impact resistance requirements outweigh lightweighting incentives.

Key Report Takeaways

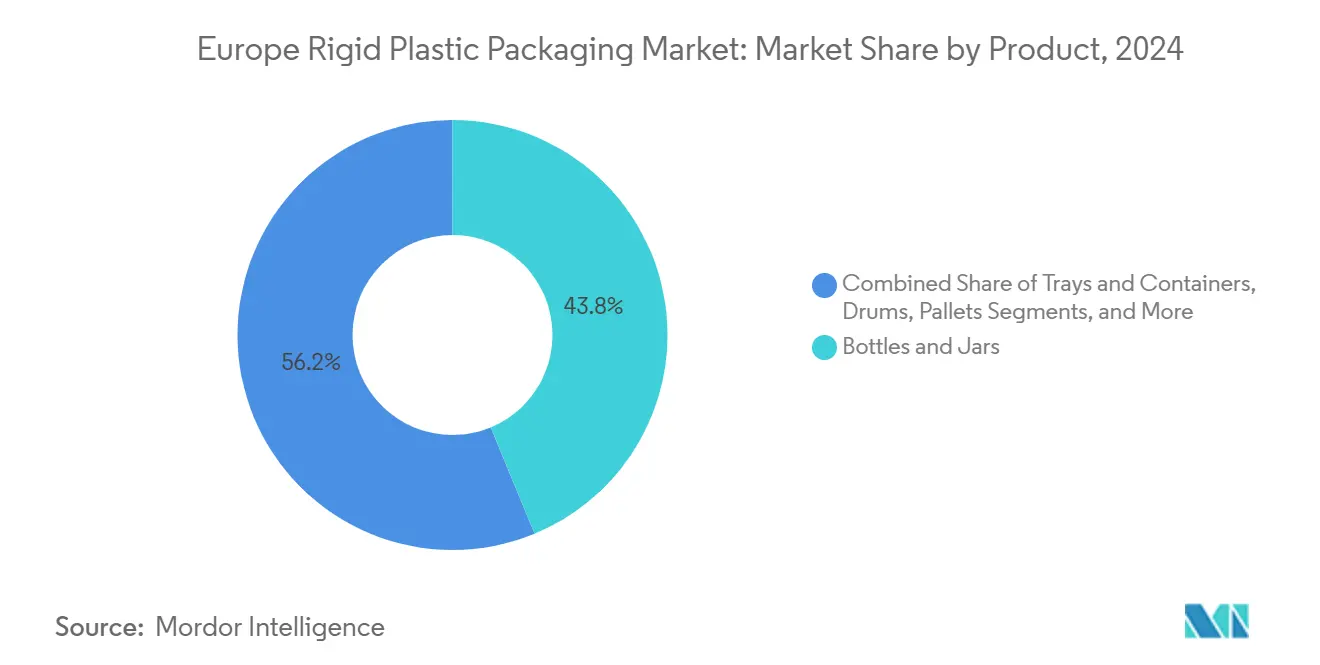

- By product type, bottles and jars commanded 43.76% of the European rigid plastic packaging market share in 2024 and are advancing at a 2.78% CAGR through 2030.

- By material, polyethylene delivered 35.33% revenue share in 2024, while polyethylene terephthalate is set to record the fastest 3.09% CAGR to 2030.

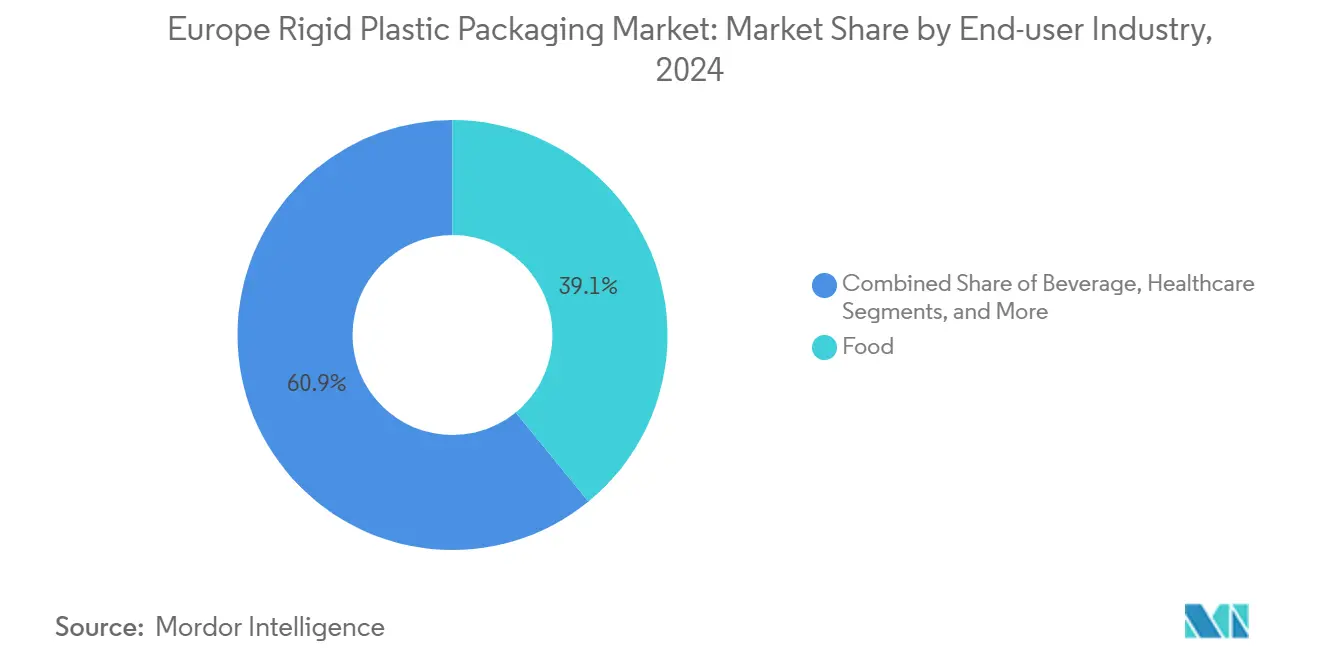

- By end-user industry, food packaging captured 39.11% of Europe's rigid plastic packaging market size in 2024; industrial applications are poised to grow at a 3.12% CAGR between 2025-2030.

- By geography, Germany held 20.73% revenue share in 2024, whereas France is projected to post the highest 3.31% CAGR over the same period.

Europe Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for recyclable rigid PET bottles in beverages | +1.40% | EU-wide, strongest in Germany, the Netherlands | Medium term (2-4 years) |

| Booming e-commerce is boosting protective rigid formats | +0.80% | Western Europe's core, expanding to CEE | Short term (≤ 2 years) |

| The growth of EU deposit-return schemes is accelerating the collection infrastructure | +0.60% | EU member states, phased implementation | Long term (≥ 4 years) |

| Refill-and-reuse store pilots driving HDPE bottle redesigns | +0.50% | Urban centers across the EU, pilot markets | Medium term (2-4 years) |

| Rapid scale-up of European bioplastics capacity | +0.30% | France, Netherlands, Germany | Long term (≥ 4 years) |

| Pharma cold-chain expansion needs high-barrier rigid packs | +0.20% | EU pharmaceutical hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Recyclable Rigid PET Bottles in Beverages

Deposit-return schemes already deliver collection rates above 90% in Germany and inspire similar adoption across the bloc, lifting demand for food-grade rPET feedstock. Portugal’s pilot proved technical viability with 1,281 packages captured per reverse-vending unit daily, and transparent blue PET accounted for most returns, underlining the power of color standardization to streamline sorting. The EU obligation for 25% recycled content in PET bottles by 2025 and 30% by 2030 creates an undersupplied secondary-material pool despite Europe’s 3 million-tonne washing and 1.4 million-tonne pellet capacity. Brand owners therefore lock in bilateral offtake agreements, stimulating retrofits of washing lines and extrusion reactors. As a result, PET bottles remain the fastest-growing rigid format and anchor more than half of the upcoming resin recycling investments[1]Plastics Recyclers Europe, “PET Market in Europe: State of Play,” unesda.eu.

Booming E-commerce Boosting Protective Rigid Formats

Online retail penetration exceeded 22% of total European goods sales in 2024, heightening the need for impact-resistant containers that survive multi-node fulfillment chains. Rigid drums, pails, and stackable tubs reduce breakage rates and warranty claims as parcels transit automated sorting hubs, and retailers accept marginal material increases when product-damage savings offset weight penalties. With packaging waste generation projected at 209 kg per capita by 2030, regulators now demand right-sizing evidence; nonetheless, protective rigid solutions often score favorably on life-cycle damage avoidance, sustaining a near-term boost for converters targeting e-commerce-ready designs[2]European Chemicals Agency, “Understanding the Packaging and Packaging Waste Regulation,” echa.europa.eu.

Growth of EU Deposit-Return Schemes Accelerating Collection Infrastructure

The Packaging and Packaging Waste Regulation compels all member states to hit 90% beverage-container recovery by 2029, triggering an unprecedented rollout of reverse-vending fleets, counting centers, and digitized clearing platforms. Engineering firms specializing in high-speed compaction and label-recognition systems receive multi-year order backlogs, while polymer producers fine-tune bottle geometry to ensure cross-border readability. Harmonized markings and color codification improve recycled-material quality, enabling larger rPET shares in rigid packaging grades and reinforcing the European rigid plastic packaging market’s transition to closed loops.

Rapid Scale-up of European Bioplastics Capacity

Consortium projects funded under the Circular Bio-based Europe Joint Undertaking (CBE JU) accelerate commercial pathways for polyethylene furanoate (PEF) bottle resins and polylactic acid blends, aiming to cut fossil-based feedstock dependence. Demonstrator lines in France and the Netherlands plan multi-kiloton outputs by 2027, offering converters drop-in options with superior barrier properties that suit carbonated drinks and sauce bottles[3]Circular Bio-based Europe JU, “CBE JU Boosting the EU’s Biotech and Biomanufacturing Sectors,” cbe.europa.eu. Although cost parity with PET remains elusive, sustainability scorecards and brand pledges create early-adopter premiums.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use plastic taxes and Extended Producer Responsibility fees | -0.70% | EU-wide implementation, varying rates by country | Short term (≤ 2 years) |

| Shift toward paper and flexible substitutes for lightweighting | -0.40% | Western Europe is leading, spreading eastward | Medium term (2-4 years) |

| Volatile rPET and rHDPE prices are squeezing converter margins | -0.30% | EU recycling markets, supply-demand imbalances | Short term (≤ 2 years) |

| Energy-price shocks raise extrusion and injection costs | -0.20% | Manufacturing-intensive regions, Germany, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Single-Use Plastic Taxes and Extended Producer Responsibility Fees

Eco-modulated fees, effective from 2025, penalize rigid packs with limited recyclability, inflating compliance outlays for legacy designs. Differential levies-EUR 800/ton (USD 866/ton) on polystyrene trays in Italy versus EUR 456/ton (USD 494/ton) on mono-material PET in France, drive format migration and prompt SKU rationalization. Large converters absorb charges via scale efficiencies, but small molders risk margin erosion or exit, accelerating sector consolidation.

Shift Toward Paper and Flexible Substitutes for Lightweighting

Fiber-based trays and molded-pulp cups displace small rigid containers in ready-meal, produce, and confectionery categories. Stora Enso’s USD 1 billion board line in Finland delivers 750,000 tons of annual capacity and showcases dry forming that lowers CO₂ by 75% against PS while meeting barrier specs. Brand owners use such transitions to hit public plastic-reduction pledges, trimming addressable volume for commodity resin suppliers.

Segment Analysis

By Product: Bottles and Jars Lead Market Evolution

Bottles and jars contributed USD 31.1 billion, equal to 43.76% of Europe's rigid plastic packaging market size in 2024, and will keep expanding fastest at a 2.78% CAGR to 2030. This momentum stems from beverage-sector reliance on DRS-compatible PET formats and pharma demand for sterilizable HDPE pill containers. Tray and container demand hold steady in chilled-food distribution, yet PFAS bans compel barrier-coating innovation. Caps and closures evolve toward tethered designs, mandated on all single-use beverage packs by July 2024, spurring tooling upgrades across closure suppliers.

Intermediate bulk containers and drums carved a resilient niche in chemical logistics; however, e-commerce parcel density has yet to justify the broad replacement of flexible liners. Pallets and other rigid accessories maintain incremental growth, driven by circular pool operators that refurbish high-density polyethylene decks. The product mix thus remains weighted toward bottles, ensuring that PET and HDPE dominate resin off-take in the European rigid plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Polyethylene Dominance Faces PET Challenge

Polyethylene generated 35.33% revenue in 2024, underpinned by blow-molded canisters and personal-care bottles. However, PET’s 3.09% CAGR will erode this margin, especially where mono-material recyclability and clarity enhance shelf appeal. Polypropylene retains value in hot-fill sauces and microwaveable trays; however, high-crystallinity PP faces stiff competition from barrier paperboard laminates.

Polystyrene usage declines as taxes bite and mechanical-recycling routes lag food-grade approval. PVC’s share shrinks further on upcoming additive-restriction rules. Emerging bio-based resins still command sub-2% of volume but draw premium pricing and brand endorsement, reinforcing Europe's rigid plastic packaging market share shifts toward next-generation materials.

By End-user Industry: Food Applications Drive Sustainability Innovation

Food packaging totaled USD 27.8 billion in 2024, representing 39.11% Europe rigid plastic packaging market share, and prompts intensive R&D into mono-material barrier layers that survive pasteurization. Mandatory PFAS removal by 2026 accelerates coating switches to EVOH or bio-PVDC alternatives. Beverage makers reshape procurement around closed-loop PET streams to de-risk recycled-content compliance, leveraging multi-year supply contracts with reclaimers.

Industrial uses, although smaller, post the highest 3.12% CAGR as e-commerce and chemicals processing raise demand for returnable rigid containers. Healthcare continues to expand on cold-chain biologics, offsetting stringent validation costs with supply-chain risk mitigation. Cosmetics move toward refillable HDPE jars, keeping volume but extending product lifespans inside the Europe rigid plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Germany’s proven 90% PET collection rate demonstrates circular-economy scalability and underpins converter confidence in supply continuity. Energy-efficiency retrofits and carbon contracts for differences mitigate escalating utility charges, keeping competitiveness intact. France combines policy ambition with industrial know-how as its bio-plastics ventures receive CBE JU backing and domestic brands pledge swift adoption of bio-based rigid packs. Italy sustains moderate growth through gourmet food exports that demand premium protective trays, while Spain leans on its beverage sector to expedite PET loop closure.

Poland posts above-average volume rises thanks to e-commerce warehousing and automotive component manufacturing that require durable bins and pallets. The Netherlands hosts Europe’s busiest polymer import/export terminals and pilots’ digital DRS clearinghouses, disseminating best practices across Benelux. Rest-of-Europe markets such as Romania, Bulgaria, and Croatia gain traction as the PPWR synchronizes regulatory expectations, encouraging multinationals to expand molding capacity eastward and shortening supply chains within the broader Europe rigid plastic packaging market.

Competitive Landscape

Sector consolidation accelerated when Amcor and Berry disclosed an all-stock merger forming a USD 24 billion packaging powerhouse, pooling R&D and procurement to meet PPWR deadlines. Faerch’s acquisition of PACCOR strengthened its position in circular dairy trays, demonstrating niche-focused buy-and-build strategies. Silgan broadened its closures reach via Weener Packaging, expanding precision-dispensing capability.

Technology differentiation centers on energy-smart equipment and advanced sorting compatibility. WITTMANN’s iMAGOxt platform cuts injection energy up to 20% and feeds real-time carbon dashboards to auditors. Resin suppliers such as Trinseo push cost-pass-through pricing to offset styrene volatility, but converters confront margin compression unless customer agreements feature raw-material indexation. Fiber-based insurgents like Stora Enso challenge smaller rigid SKUs by touting CO₂ reductions, forcing plastic converters to highlight reuse cycles and recycling efficacy. Brand owners increasingly score suppliers on traceable recycled content, accelerating capital toward mechanical and chemical recycling joint ventures inside the European rigid plastic packaging market.

Europe Rigid Plastic Packaging Industry Leaders

-

Alpla Werke Alwin Lehner GmbH & Co KG

-

Amcor plc

-

Greiner Packaging International GmbH

-

PACCOR Packaging GmbH (Faerch Group)

-

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor and Berry closed their merger, creating a USD 24 billion revenue entity with USD 650 million synergy targets.

- January 2025: EU Regulation 2025/40 entered force, mandating universal recyclability by 2030 and setting a 30% recycled-content minimum for PET food packaging.

- January 2025: Trinseo raised European polystyrene, ABS, and SAN prices by 45–55 EUR/t amid styrene cost inflation.

- November 2024: Silgan amended its senior secured facility after acquiring Weener Packaging, reporting USD 5.9 billion in net sales in 2024.

Europe Rigid Plastic Packaging Market Report Scope

The market study tracks the demand for rigid plastic packaging products catering to the demand in the food, foodservice, beverage, healthcare, personal care, and cosmetic industries, industrial, building and construction, automotive, and other end-user industries. Rigid plastics can be of different grades and different material combinations based on the type of product being packed, like polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, bioplastics, and other materials.

The European rigid plastic packaging market is segmented by product (bottles and jars, trays and containers, caps and closures, intermediate bulk containers (IBCS), drums, pallets, and other product types), material (polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), other rigid plastic packaging materials), end-user industry (food, beverage, healthcare, cosmetics and personal care, industrial, building and construction, automotive, other end-user industries), and country (the United Kingdom, Germany, France, Italy, Spain, Poland, Rest of Europe). The report offers market forecasts and size in value terms in USD for all the above segments.

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Pallets |

| Other Product Types |

| Polyethylene (PE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Polystyrene (PS) and Expanded PS (EPS) |

| Polyvinyl Chloride (PVC) |

| Other Rigid Plastic Materials |

| Food |

| Beverage |

| Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Building and Construction |

| Automotive |

| Other End-user Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Bottles and Jars |

| Trays and Containers | |

| Caps and Closures | |

| Intermediate Bulk Containers (IBCs) | |

| Drums | |

| Pallets | |

| Other Product Types | |

| By Material | Polyethylene (PE) |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP) | |

| Polystyrene (PS) and Expanded PS (EPS) | |

| Polyvinyl Chloride (PVC) | |

| Other Rigid Plastic Materials | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Building and Construction | |

| Automotive | |

| Other End-user Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe rigid plastic packaging market be in 2025?

The market stands at USD 71.04 billion in 2025 and is projected to reach USD 78.59 billion by 2030.

What CAGR is expected for Europe’s rigid plastic pack sector through 2030?

A measured 2.04% CAGR is forecast as regulatory compliance and circular-economy investments temper growth.

Which product category holds the biggest share of rigid plastic packs in Europe?

Bottles and jars account for 43.76% of 2024 revenue and remain the fastest-growing segment at 2.78% CAGR.

Why is France the fastest-growing market for rigid plastic packaging?

Aggressive biopolymer investments and strong EPR incentives propel France toward a 3.31% CAGR through 2030.

How are deposit-return schemes influencing material demand?

DRS mandates boost high-grade rPET availability and drive brand owners to secure recycled content contracts, supporting PET’s 3.09% CAGR.

What impact do single-use plastic taxes have on converters?

Eco-modulated fees raise costs for non-recyclable formats, squeezing margins and accelerating consolidation among smaller converters.

Page last updated on: