Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

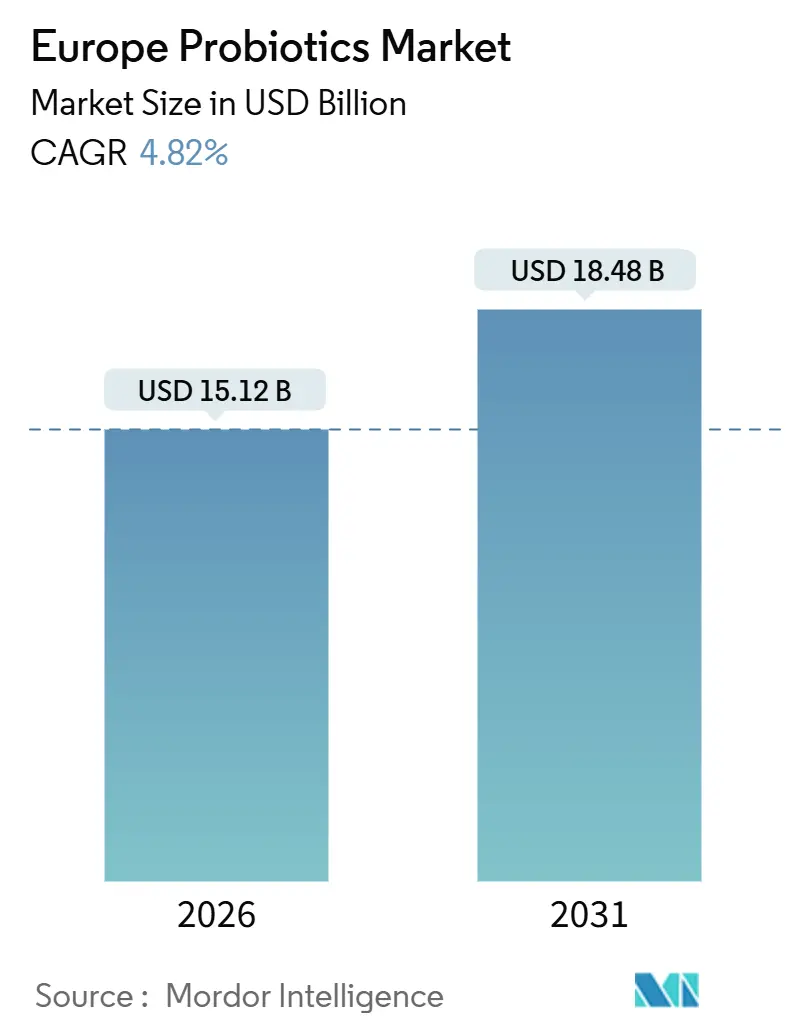

| Market Size (2026) | USD 15.12 Billion |

| Market Size (2031) | USD 18.48 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

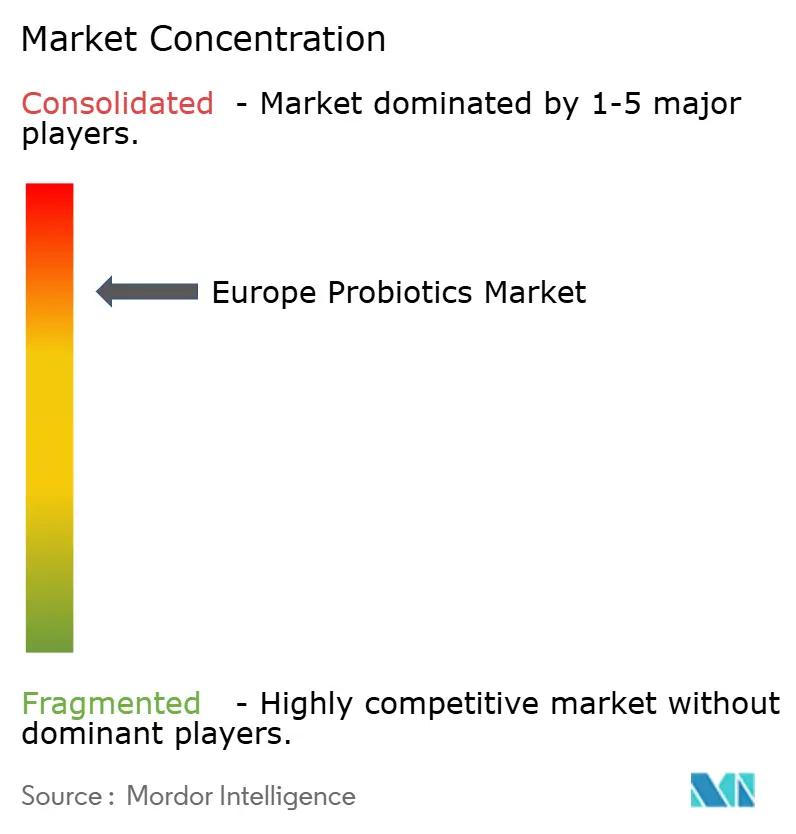

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Probiotics Market Analysis by Mordor Intelligence

The Europe food probiotics market stood at USD 15.12 billion in 2026 and is projected to reach USD 18.48 billion by 2031, expanding at a 4.82% CAGR. This mature category now relies on science-backed strain selection, stricter safety dossiers, and sharper consumer communication rather than broad-brush promotions. Demand remains anchored in traditional fermented dairy, yet purposeful innovation in supplements and ambient-stable foods is widening penetration across age groups and usage occasions. Major suppliers leverage consolidated strain libraries and deep regulatory know-how to retain licensing power, while retailers adopt private-label strategies to protect margins. Online channels, pharmacist advice, and rising preventive-health awareness together sustain steady volume gains and encourage premium formats that promise clinically documented outcomes.

Key Report Takeaways

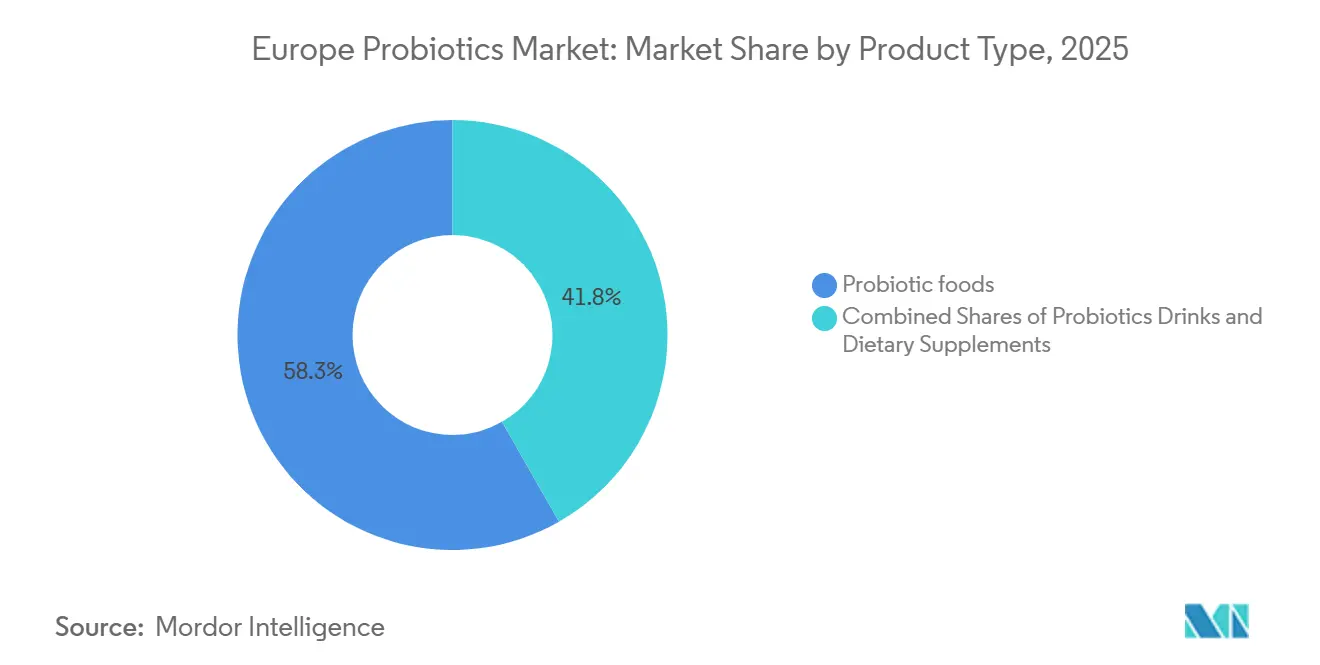

- By product type, probiotic foods contributed 58.25% of revenue in 2025, while dietary supplements are advancing at a 6.28% CAGR through 2031.

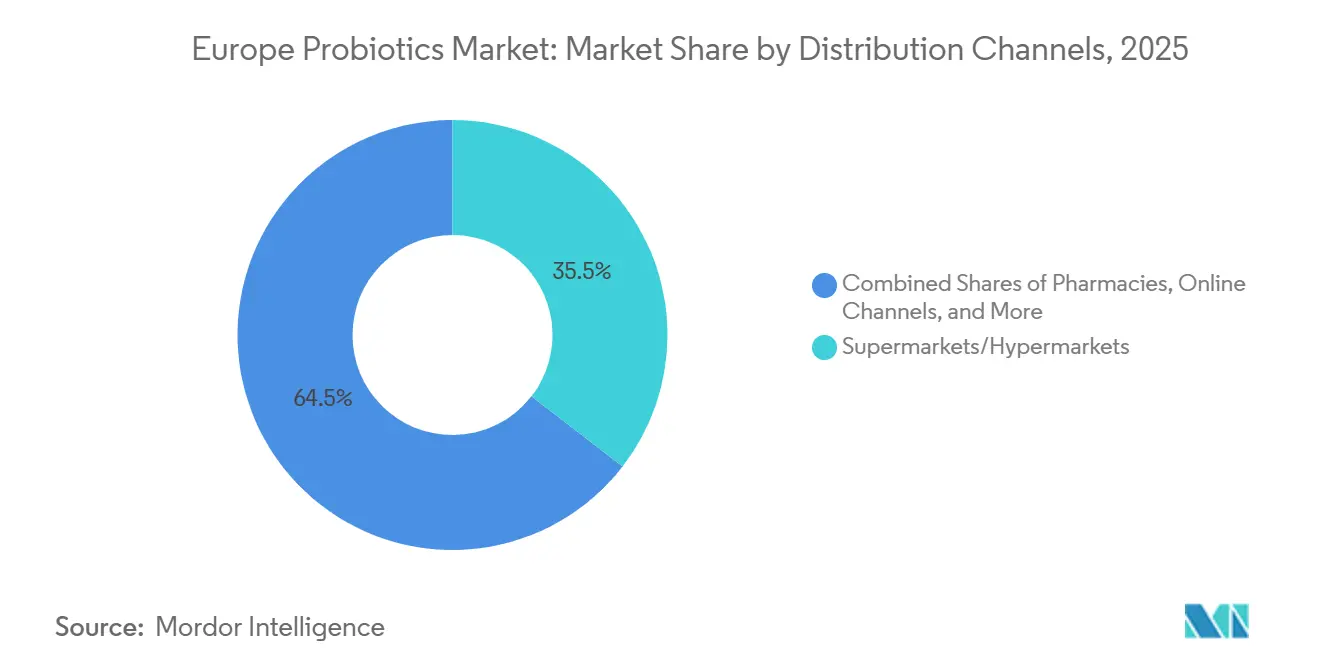

- By distribution channel, supermarkets and hypermarkets led with 35.48% of sales in 2025; pharmacies and drug stores are forecast to register the fastest 5.68% CAGR.

- By geography, the United Kingdom accounted for 52.31% revenue in 2025, whereas Germany is set to grow at a 6.38% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Probiotics Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on gut microbiota for immunity, digestion, and mental wellness | +1.2% | Global, with strongest uptake in UK, Germany, Netherlands | Medium term (2-4 years) |

| High consumption of dairy-based probiotics | +0.9% | France, Italy, Spain, Germany (fermented dairy traditions) | Long term (≥ 4 years) |

| Shift toward functional foods and beverages | +0.8% | UK, Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Increasing prevalence of lifestyle diseases like obesity and digestive disorders | +0.7% | Global, with elevated incidence in UK, Germany, Spain | Long term (≥ 4 years) |

| Strong retail infrastructure, including supermarkets and e-commerce | +0.6% | UK, Germany, France, Netherlands (mature retail networks) | Short term (≤ 2 years) |

| Cultural affinity for fermented foods | +0.5% | France, Italy, Spain, Greece (Mediterranean diet regions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Focus on Gut Microbiota for Immunity, Digestion, and Mental Wellness

Research on the gut-brain axis has redefined probiotics, elevating them from digestive aids to interventions with multi-system benefits. Peer-reviewed studies have associated specific probiotic strains with reduced anxiety, improved cognitive performance, and strengthened immune function. A 2024 meta-analysis in Nutrients revealed that Lactobacillus and Bifidobacterium strains influence cytokine production and short-chain fatty acid synthesis. These mechanisms are essential for mucosal immunity and neurotransmitter precursor availability. This growing body of evidence is shaping consumer behavior: 25% of UK adults now consume probiotic drinks regularly, with this figure rising to 39% among individuals aged 55 and older, a demographic focused on preventive health strategies, as per YouGov UK 2025. The convergence of mental wellness and immune health narratives—fueled by increased health awareness in the post-pandemic era—positions gut microbiota optimization as a key growth driver. This trend is particularly prominent in markets where healthcare systems encourage preventive nutrition. However, the absence of EFSA-approved claims for psychobiotic or immunomodulatory effects restricts marketing language. Consequently, brands rely on indirect messaging and third-party clinical summaries rather than direct on-pack claims.

High Consumption of Dairy-Based Probiotics

Fermented dairy products hold a significant place in European diets, combining tradition with functional benefits that existed long before modern probiotic science. According to longitudinal data from the European Prospective Investigation into Cancer and Nutrition, yogurt consumption in Mediterranean populations is linked to a 24% reduction in hip fracture risk, with each 200-gram serving associated with a 10-15% decrease in fracture incidence. Italian participants in the highest yogurt consumption group—approximately 85-98 grams per day—showed a 35% lower risk of colorectal cancer. Researchers credit this benefit to the combined effects of calcium, protein, and live cultures rather than probiotics alone. These epidemiological insights strengthen consumer trust in dairy-based products, even as plant-based alternatives gain momentum. France, Italy, and Spain collectively dominate the fermented dairy market, driven by the retail success of branded yogurts and fresh cheeses, both of which are perceived as inherently healthy. However, manufacturers face the challenge of converting this cultural preference into premium-priced functional products without alienating cost-conscious consumers who view yogurt as an everyday staple rather than a premium supplement.

Shift Toward Functional Foods and Beverages

European consumers are showing a growing willingness to pay more for foods that provide health benefits beyond basic nutrition. A YouGov survey conducted in 2025 indicated that 58% of UK respondents prioritize natural or organic ingredients when purchasing food and beverages. This preference also includes everyday products like breakfast cereals, snack bars, and kombucha that incorporate probiotics. Consequently, probiotic suppliers are expanding their offerings from traditional refrigerated dairy products to ambient-stable categories. They are utilizing microencapsulation technologies to protect live cultures during baking and extend shelf life. In Germany and the Netherlands, probiotic-enriched bakery items and breakfast cereals are gaining traction, driven by consumers' acceptance of scientifically-supported functional claims. The functional-beverage market, which includes dairy-based drinks like kefir and non-dairy alternatives such as oat-based probiotic smoothies, is attracting venture capital investments and fostering private-label innovation. Retailers are increasingly viewing this segment as a profitable growth area. However, the growth of functional foods is limited by the European Food Safety Authority's (EFSA) restrictive claim approvals[1]Source: EFSA, “Health Claims Regulation and Probiotic Submissions,” EFSA Journal, efsa.onlinelibrary.wiley.com. These limitations prevent brands from emphasizing specific benefits, making it harder to differentiate their products from conventional offerings.

Increasing Prevalence of Lifestyle Diseases Like Obesity and Digestive Disorders

As type 2 diabetes, inflammatory bowel disease, and obesity-related conditions become more prevalent, both clinicians and public health officials are turning to dietary interventions aimed at reshaping gut microbiota. Numerous meta-analyses have established a connection between regular yogurt consumption and a reduced risk of developing type 2 diabetes. Furthermore, mechanistic studies, as highlighted in BMC Medicine, indicate that certain probiotic strains can enhance insulin sensitivity and diminish systemic inflammation. In June 2025, 22% of adults in the UK voiced concerns over food affordability, highlighting the clash between health goals and financial realities. This scenario has spurred a demand for budget-friendly probiotic options. These include fortified yogurts and store-brand supplements that offer health benefits without the hefty price tag. In Germany, the pharmacy sector generated approximately USD 173 million from probiotic sales targeting digestive issues. This underscores a broader healthcare trend where over-the-counter probiotics are routinely recommended for conditions like irritable bowel syndrome and diarrhea linked to antibiotics, as noted by the Federal Office of Consumer Protection and Food Safety. The push for probiotics is especially pronounced among aging populations, where the challenges of multiple medications and their gastrointestinal side effects make them more receptive to scientifically-backed probiotic solutions.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of research and development | -0.8% | Global, with acute pressure on small-to-midsize ingredient suppliers | Long term (≥ 4 years) |

| Competition from alternative health products | -0.6% | UK, Germany, Netherlands (mature supplement markets) | Medium term (2-4 years) |

| Lack of consumer awareness in some regions | -0.5% | Poland, Russia, Rest of Europe (Eastern and peripheral markets) | Medium term (2-4 years) |

| Regulatory challenges and product claims restrictions | -0.7% | EU-wide, governed by EFSA; fragmented national enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Research and Development

Introducing a new probiotic strain to the European market requires significant multi-year investments in strain characterization, safety documentation, and randomized controlled trials that comply with EFSA's stringent standards. This regulatory process gives an advantage to multinational ingredient suppliers, such as Novonesis and DSM-Firmenich, who can distribute R&D costs across their global operations and utilize their existing strain libraries. On the other hand, smaller players face a difficult decision: either license established strains, which reduces margins due to royalty fees, or invest in proprietary strain development, a high-risk endeavor with uncertain returns. The November 2024 merger of Chr. Hansen and Novozymes into Novonesis highlights the industry's emphasis on scale. As a result of this consolidation, Novonesis now holds the largest strain catalog and the most comprehensive regulatory expertise in the industry. Brands targeting niche markets, such as pediatric probiotics or psychobiotics, face additional challenges. Without the ability to make direct claims, they must depend on indirect marketing and third-party endorsements, which significantly increase customer acquisition costs.

Competition from Alternative Health Products

Prebiotics, postbiotics, and synbiotics are gaining recognition as scientifically validated alternatives that address some of the regulatory and formulation challenges associated with live probiotics. Prebiotics, which are non-digestible fibers that selectively promote beneficial gut bacteria, have EFSA-approved claims for digestive health. They eliminate the need for refrigeration or viability testing, simplifying supply-chain processes and extending shelf life. Postbiotics, consisting of metabolites and cell fragments from probiotic fermentation, are emerging as a stable, heat-resistant option for functional foods. Early clinical studies suggest their immune-modulating effects are comparable to those of live cultures. Synbiotics, which combine prebiotics and probiotics in a single formulation, attract consumers seeking comprehensive gut-health solutions but face the same claim limitations as standalone probiotics. This competitive dynamic is evident in retail assortments, where the range of digestive-health products has expanded to include various mechanisms, reducing the visibility and trial rates of traditional probiotic SKUs. To justify premium pricing over prebiotic or postbiotic alternatives, brands must emphasize strain-specific clinical outcomes and innovate with formats such as chewable gummies or effervescent tablets.

Segment Analysis

By Product Type: Supplements Outpace Traditional Dairy

In 2025, Probiotic Foods Europe held a 58.25% market share, primarily driven by the widespread availability of yogurt, fermented dairy, and fortified breakfast cereals in retail outlets. Yogurt remains the leading subcategory, supported by years of consumer trust and an exclusive EFSA-approved claim linking its cultures to improved lactose digestion. In Germany and the Netherlands, bakery products and breakfast cereals enriched with probiotics are expanding their presence. Microencapsulation technologies enable these products to maintain ambient stability, withstand baking temperatures, and achieve longer shelf lives. Infant formulas and baby foods containing probiotic strains like Bifidobacterium lactis undergo rigorous EFSA safety evaluations, requiring manufacturers to provide strain-specific safety data for vulnerable populations. While this regulatory process slows innovation, it also creates a significant barrier to entry for approved products. Snacks and confections, such as probiotic gummies and chocolate, are gaining traction among younger consumers and driving trials, though their health claims remain limited due to the absence of approved assertions.

Dietary Supplements are the fastest-growing segment, with a 6.28% CAGR projected through 2031. This growth is supported by Germany's pharmacy-focused distribution model and increasing consumer interest in targeted gut-health solutions. In 2025, probiotic supplements aimed at digestive health generated USD 173 million in sales, representing approximately 8% of the pharmacy supplement market and growing at 7% annually, according to the Federal Office of Consumer Protection and Food Safety[2]Source: Federal Office of Consumer Protection and Food Safety, “Food Supplements Market Data Germany,” bvl.bund.de. Innovations in formats—such as delayed-release capsules, effervescent tablets, and high-CFU single-strain formulations—are enabling brands to command premium pricing and differentiate themselves with clinical evidence. Probiotic Drinks, which include dairy-based options like kefir and non-dairy alternatives such as oat and coconut beverages, occupy a niche position. Non-dairy options are gaining popularity among lactose-intolerant and vegan consumers but still account for a smaller share of the overall volume. The shift toward supplements reflects a broader trend of consumers increasingly viewing gut health as a proactive therapeutic focus, favoring pharmacist-recommended capsules over traditional refrigerated dairy products.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channels: Pharmacy Gains Ground

In 2025, supermarkets and hypermarkets are expected to account for 35.48% of the market value, driven by their extensive footfall and frequent promotional activities. However, tight margin thresholds and intense competition from private labels restrict their overall growth. Conversely, pharmacies and drug stores provide credibility and personalized counseling, which appeal to consumers dealing with sensitive issues like digestive or immunity concerns. This channel leads with a 5.68% CAGR through 2031 and already represents a significant portion of Germany's supplement turnover.

Pharmacists play a crucial role by validating strain selections, recommending dosages, and advising on usage periods. Their expertise effectively bridges the gap left by EFSA, which has yet to authorize explicit benefit claims. At the same time, online platforms are capitalizing on this advisory gap by offering tele-pharmacist consultations, subscription-based replenishments, and detailed trial summaries to enhance consumer confidence. As supermarket chains streamline their SKUs and shift toward lower-cost private-label products, high-margin therapeutic-grade probiotics are increasingly moving to professional channels. This transition not only boosts the share of pharmacies in Europe's food probiotics market but also strengthens their influence over brand formulation strategies.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, the United Kingdom accounted for 52.31% of the regional revenue, supported by well-established brands like Yakult, Actimel, and Biomel. These brands have built decades of consumer loyalty through consistent messaging and broad retail availability. A YouGov survey conducted in 2025 revealed that 25% of UK adults regularly consume probiotic drinks, with this figure increasing to 39% among individuals aged 55 and above, a demographic that prioritizes digestive health and immune support. However, the UK market faces economic challenges: In June 2025, 22% of adults expressed concerns about food affordability, which could limit the adoption of premium-priced probiotic products. Trust in the Food Standards Agency (FSA) remains high, ranging between 64-66%, providing a regulatory foundation for future health-claim approvals[3]Source: Food Standards Agency, “Consumer Trust and Food Safety Perceptions 2025,” food.gov.uk. Nonetheless, the FSA's alignment with EFSA standards restricts the scope for claim innovation.

With 65% supermarket penetration and 18% online sales, the UK's mature retail infrastructure serves as an ideal testing ground for innovations such as ambient-stable probiotic snacks and subscription-based supplement services. Germany is projected to achieve the highest growth rate among major geographies, with a CAGR of 6.38% through 2031. This growth is driven by a pharmacy-focused distribution model and a cultural preference for evidence-based supplementation. In 2019, Germany's food-supplement market reached EUR 2.6 billion, with pharmacies contributing over 84% of the revenue. Digestive-tract probiotics alone generated EUR 163 million in sales. The dominance of pharmacies provides an implicit clinical endorsement and supports premium pricing, as consumers perceive pharmacist-recommended products as more reliable than supermarket alternatives.

Germany's regulatory framework, managed by the Federal Office of Consumer Protection and Food Safety, enforces strict quality standards. These standards raise barriers to entry but also enhance consumer trust. France, Italy, and Spain collectively hold a significant share of fermented dairy consumption. For example, yogurt consumption in Italy is associated with a 35% lower risk of colorectal cancer, reinforcing the category's health benefits. In contrast, Russia, the Netherlands, and Poland exhibit lower per-capita probiotic consumption due to limited awareness and price sensitivity. However, increasing interest in preventive health and a growing retail infrastructure indicate potential for medium-term growth. The "Rest of Europe" category includes diverse markets with varying regulatory environments and levels of consumer awareness. These differences require localized strategies that balance clinical messaging with affordability.

Competitive Landscape

The market demonstrates significant dominance by leading suppliers, who collectively control over 80% of the market share. In 2024, Novonesis emerged as a result of the merger between Chr. Hansen and Novozymes, combining Chr. Hansen’s extensive clinical expertise with Novozymes’ advanced fermentation capabilities. This collaboration has created a strain repository that is unmatched in its breadth and depth. Similarly, DSM-Firmenich, established in 2023, is capitalizing on its ability to integrate fragrance-driven consumer insights with fermentation efficiency, enabling the company to accelerate its market entry and achieve economies of scale.

Mid-sized players are contributing to the competitive landscape with their unique strategies. BioGaia experienced a 15% increase in sales during Q3 2024, reaching SEK 281.8 million (USD 27 million). This growth was driven by strong prescriber trust in its Lactobacillus reuteri product, particularly for addressing pediatric colic. In contrast, Probi faced a 19% decline in revenue during the same quarter, which exposed its over-reliance on a limited customer base and highlighted the risks associated with shelf rotation. Emerging brands such as OptiBac and Winclove are navigating around mass-retail barriers by adopting direct-to-consumer models, promoting niche strain benefits, and forming strategic alliances with healthcare practitioners.

Technological advancements, including microencapsulation, genomics-guided discovery, and AI-enabled strain selection, are now pivotal in determining which companies can command premium royalties. However, despite the push for innovation, the European Food Safety Authority’s (EFSA) conservative stance on claim approvals continues to limit overt marketing efforts. This regulatory environment favors companies that can invest in multi-year clinical trials and maintain harmonized European dossiers. The ability to balance ambitious innovation with regulatory compliance has become a defining factor for competitive success in the European food probiotics market.

Europe Probiotics Industry Leaders

Danone S.A.

Bio-K Plus International Inc.

PepsiCo Inc. (KeVita )

Nestlé S.A.

Yakult Honsha Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Arla Foods has introduced its Arla Cultura range in the UK, featuring lactose-free gut health dairy products enriched with probiotics, vitamin D, calcium, protein, and fiber. The debut lineup includes three 500ml milk drinks (Original, Raspberry, Blueberry).

- May 2025: Lab4 Probiotics officially launched its proprietary probiotic blends to the global market at Vitafoods Europe 2025 in Barcelona. Lab4 family includes Lab4B for infant benefits, Lab4P for metabolic/immune effects like weight loss, and Lab4S combining Lab4 with Saccharomyces boulardii for antibiotic support.

- February 2025: Karma Water has expanded into the booming stick pack category with new Probiotic and Energy variants, targeting on-the-go consumers. Probiotic Stick Packs deliver 2 billion BC30 cultures (10x typical yogurt), plus 100% DV of vitamins A, E, B3, B5, B6, B12 in Berry Cherry, Blueberry Lemonade, Strawberry Lemonade flavors.

Europe Probiotics Market Report Scope

Probiotics are live microbes that can be added to a variety of goods, such as foods, medications, and nutritional supplements, with the goal of improving health when ingested or applied topically.

The European probiotics market is segmented on the basis of product type, distribution channel, and geography. Based on product type, the market is segmented into functional food and beverage, dietary supplement, and animal feed. The food and beverage segment is further bifurcated into dairy products, fermented products, non-alcoholic beverages, dietary supplements, and others. Based on the distribution channel, the market is segmented into supermarkets/ hypermarkets, pharmacies/health stores, convenience stores, and others. Based on geography, the market is segmented into Germany, the United Kingdom, France, Russia, Italy, Spain, and the Rest of the European countries.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Probiotic Foods | Yogurt |

| Bakery & Breakfast Cereals | |

| Infant Formula & Baby Foods | |

| Snacks & Confectionery | |

| Others | |

| Probiotic Drinks | Dairy-based |

| Non-dairy | |

| Dietary Supplements |

By Distribution Channels

| Supermarket/Hypermarkets |

| Pharmacies and Drug Stores |

| Convinience/Grocery Stores |

| Online Stores |

| Others |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Rest of Europe |

| By Product Type | Probiotic Foods | Yogurt |

| Bakery & Breakfast Cereals | ||

| Infant Formula & Baby Foods | ||

| Snacks & Confectionery | ||

| Others | ||

| Probiotic Drinks | Dairy-based | |

| Non-dairy | ||

| Dietary Supplements | ||

| By Distribution Channels | Supermarket/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Convinience/Grocery Stores | ||

| Online Stores | ||

| Others | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value and forecast growth rate for the Europe food probiotics market?

The market reached USD 15.12 billion in 2026 and is projected to expand to USD 18.48 billion by 2031 at a 4.82% CAGR.

Which product category is growing fastest across Europe?

Dietary supplements record the highest momentum at a 6.28% CAGR, benefiting from pharmacy endorsements and targeted health positioning.

Why do pharmacies outperform other channels in probiotic sales growth?

Pharmacists offer strain-specific guidance that substitutes for restricted on-pack claims, allowing premium pricing and higher consumer trust.

What emerging formats are broadening consumer reach?

Ambient-stable cereals, snack bars, and shelf-stable postbiotic products leverage encapsulation and fermentation advances to extend probiotics beyond the dairy aisle.