| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.67 Billion |

| Market Size (2030) | USD 3.07 Billion |

| CAGR (2025 - 2030) | 2.80 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe PCB Market Analysis

The Europe PCB Market size is estimated at USD 2.67 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 2.8% during the forecast period (2025-2030).

The European PCB industry is experiencing significant technological transformation driven by the increasing integration of advanced electronics across various sectors. The widespread adoption of connected devices and smart technologies has fundamentally altered the PCB manufacturing landscape, with Germany leading the digital adoption curve as evidenced by 98.1% of German households owning cell phones in 2022. This digital transformation is further accelerated by the expansion of 5G infrastructure, with the United Kingdom alone seeing its mobile base stations providing 5G services double to over 6,500 locations by 2021, enabling more sophisticated PCB applications in telecommunications and IoT devices.

The industry is witnessing substantial investments in manufacturing capabilities and technological advancements across the region. A notable example is Unimicron Germany's EUR 12 million investment in September 2022 for a new facility and advanced high-tech printed circuit board production processes, representing one of Europe's most modern manufacturing facilities. This trend is further exemplified by Infineon Technologies' opening of a new manufacturing facility in Hungary in October 2022, with an investment of EUR 100 million, specifically aimed at meeting the growing demand for power semiconductor modules in vehicle electrification.

The European printed circuit board market is increasingly focusing on sustainable and advanced manufacturing processes, with companies developing innovative solutions for environmental compliance. The industry is witnessing a shift toward recyclable and biodegradable PCB components, addressing the growing environmental concerns while maintaining high performance standards. This evolution is supported by significant institutional backing, as evidenced by the European Union's EUR 6 billion investment announced in November 2022 for developing a satellite internet system, which is expected to drive innovation in PCB manufacturing for space and communication applications.

The market is experiencing considerable consolidation through strategic acquisitions and partnerships, aimed at strengthening technological capabilities and market presence. This trend is illustrated by NCAB Group's acquisition of PreventPCB in Italy, which integrated sales of approximately USD 29.59 million. According to industry projections, the Internet of Things (IoT) sector is poised for substantial growth, with the UK market alone expected to exceed 150 million connected devices by 2024, primarily driven by white goods and consumer wearables which account for over 40% of all IoT connections, creating new opportunities for circuit board manufacturing in these emerging applications.

Europe PCB Market Trends

Rising Demand for Miniaturization of Technology and Growth in Diversity and Density of PCBs

The miniaturization of electronic components has revolutionized the development of portable and handheld computing devices, driving significant demand for increasingly sophisticated PCBs. Today's electronics industry is characterized by a strong trend toward miniaturization, with components shrinking in size and placing new demands on PCB design. For instance, Ball Grid Array (BGA) components now require extremely short conductor widths and minimal board clearance for implementations that are even denser than traditional HDI PCB circuit boards. These boards have evolved to feature dielectric thicknesses and isolation clearances of up to 50 μm, enabling the creation of more compact and powerful electronic devices.

The advent of IoT has substantially impacted PCB design and size requirements, particularly in smart homes, offices, wearables, and remote monitoring applications. HDI PCB technology enables IoT circuit boards to be remarkably compact while increasing the effective performance of IoT devices. According to recent industry data, 98.1% of German households owned at least one cell phone in 2022, highlighting the widespread adoption of miniaturized electronic devices. The market for one-millimeter-thick printed circuit boards is expanding significantly, especially in microelectronics, medical technology, and automobile electronics applications, particularly in high-performance LED headlights. These ultra-thin PCBs are increasingly preferred in applications requiring constrained installation spaces, weight savings, or cooling optimization.

Understand The Key Trends Shaping This Market

Download PDF

Increasing R&D and Investments in PCB Manufacturing in Europe

The European PCB manufacturing sector has witnessed substantial investments in technological advancements and capacity expansions. A notable example is Unimicron Germany's EUR 12 million investment in 2022 for a new facility and advanced high-tech PCB production processes. The investment aims to enhance the company's technological leadership in printed circuit board technology and sustainability. Similarly, the European Union announced a new satellite internet system development backed by EUR 6 billion in funding, with plans to have the system operational by 2027, demonstrating the region's commitment to advanced technology infrastructure.

The government initiatives toward semiconductor production are creating a ripple effect in PCB manufacturing. The European Union and German federal government are allocating additional funds under the European Chips Act to establish a robust environment for the European microelectronics industry. Companies like Bosch have announced significant investments, with EUR 3 billion allocated to its semiconductor sector by 2026 as part of the Important Project of Common European Interest (IPCEI) on Microelectronics and Communications Technologies. These investments are primarily intended to promote research and innovation, creating new opportunities for PCB manufacturers to develop more advanced and sophisticated products.

Increasing Adoption of Flexible and Flex-Rigid PCBs (Wearable Electronics, Flexible Displays and Medical Applications)

The medical sector is experiencing a significant shift toward flexible PCBs and flex-rigid PCBs, driven by the need for more sophisticated and portable medical devices. According to the European Heart Network, cardiovascular disease causes 3.9 million deaths in Europe annually, accounting for 45% of all deaths, which has led to increased demand for medical devices like pacemakers and heart monitors that utilize flexible PCBs. These applications require greater flexibility and portability while devices become smaller and more complex, particularly in blood glucose monitors, heart monitors, and intravenous treatment infusion pumps where space constraints are critical.

The automotive industry has embraced rigid-flex PCBs due to their high stress-absorbing capability and space-saving properties. Tesla's new factory in Grünheide, Germany, with its planned capacity of 500,000 cars annually, exemplifies the growing demand for advanced PCBs in electric vehicles. These PCBs demonstrate superior reliability even under harsh environments and are extensively used in control modules, LCD screens, entertainment systems, and various automotive applications. The combination of rigid and flexible sections in these PCBs provides optimal solutions for complex electronic systems while maintaining durability and performance in demanding automotive environments.

Increasing Complexity Due to Miniaturization of Components

The continuous drive toward miniaturization in electronic devices has created significant challenges in PCB manufacturing and assembly processes. When it comes to layout design, shrinking PCBs requires innovative approaches as components need specific keep-out areas for positioning on the board. PCB designers and layout engineers must challenge traditional IPC specifications and manipulate the assembly keep-outs of components to accommodate the maximum number of components while maintaining signal integrity in high-speed circuits.

The complexity extends to the assembly stage, where challenges increase inversely with component size. Current package sizes of passive components can be as small as 008004 (8 mils X 4 mils), making rework extremely difficult and significantly impacting production yields. The integration of various component packages like ball grid array, quad flat no-leads, bare die, and surface mount technology on a single board presents additional manufacturing challenges. These hybrid assemblies, combining surface mount technology with micro-e technology like wire bond, bare die, BGA, and QFN placement, require sophisticated equipment and precise manufacturing processes to ensure reliable production.

Strict Requirements to Comply with Legislations

Environmental regulations have become increasingly stringent in Europe, particularly concerning the use of hazardous materials in electronic and electrical products. The Restriction of Hazardous Substances (RoHS) compliance, originally developed in the European Union, has become a mandatory requirement for OEMs manufacturing and selling electronic products or components to European clients. The directive has restricted the use of six critical materials in PCBs, including lead, mercury, cadmium, polybrominated diphenyl ethers, hexavalent chromium, and polybrominated biphenyls, along with specific phthalates.

The implementation of these regulations has led to significant changes in manufacturing processes and material selection. The removal of lead has presented the most significant challenge for electronics manufacturers due to various factors such as higher melting temperatures, mixed processes, and supply chain complexities. However, these challenges are balanced by the benefits of RoHS-compliant PCBs, including reduced metal poisoning, improved product safety, and enhanced thermal properties. Manufacturers must continuously adapt their processes and materials to meet these environmental standards while maintaining product quality and performance, driving innovation in eco-friendly PCB manufacturing techniques.

Segment Analysis: By Category

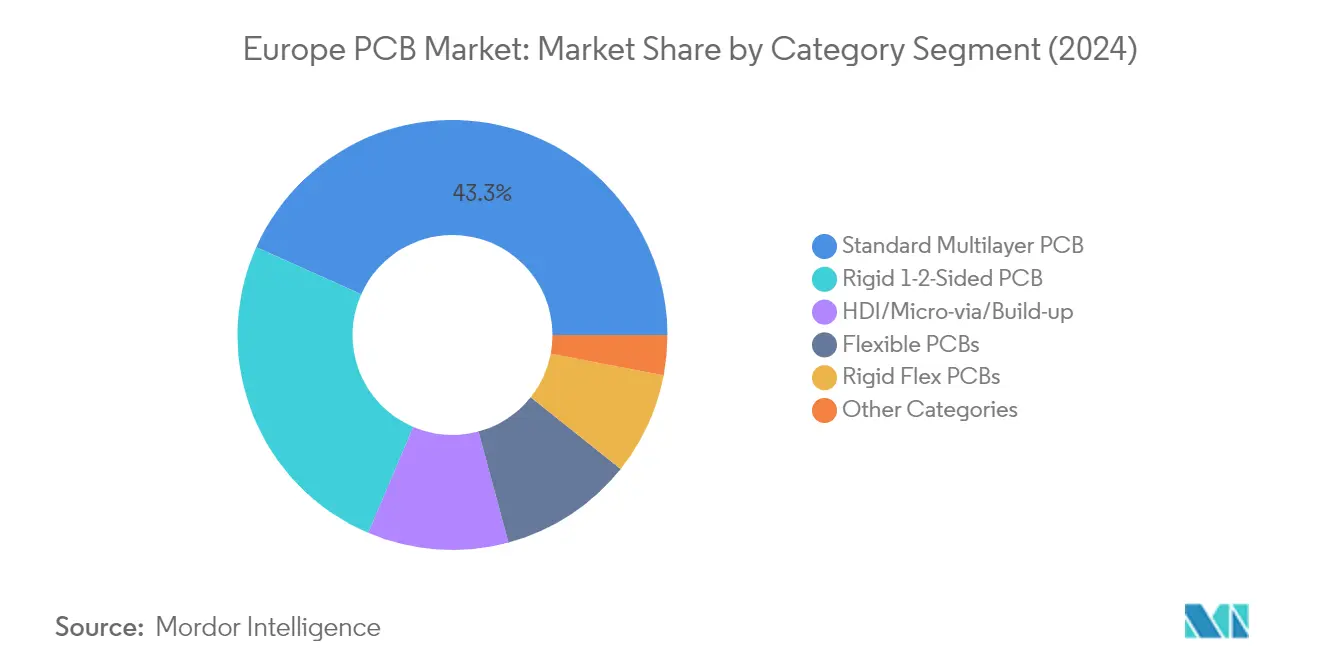

Standard Multilayer PCB Segment in Europe PCB Market

Standard multilayer PCBs continue to dominate the European PCB market, holding approximately 43% market share in 2024. This segment's prominence is driven by its widespread adoption across various industries, including computers, medical equipment, in-car systems, GPS, and satellite systems. The technology's ability to solve electrical performance issues while saving space, including EMI shielding and signal thermal integrity control, has made it indispensable in modern electronics. Multilayer PCBs are particularly favored in the medical industry for their lightweight, small size, and impressive functionality compared to single-layer alternatives, leading to their extensive use in modern X-ray equipment, heart monitors, CAT scan equipment, and medical testing devices.

Flexible PCBs Segment in Europe PCB Market

The flexible PCBs segment is emerging as the fastest-growing category in the European PCB market, with an expected growth rate of approximately 4% during 2024-2029. This growth is primarily driven by the increasing adoption in wearable technology, LED lighting, and medical instrumentation. The segment's expansion is further supported by its ability to reduce the space and weight of conventional wiring by up to 75% while offering greater resistance to vibration and shock. The technology's versatility in applications ranging from smart socks and belts to wristbands and sports helmets, along with its essential role in flexible displays and medical devices, continues to drive its rapid adoption across various industries.

Remaining Segments in PCB Category Market

The remaining segments in the European PCB market include rigid 1-2-sided PCBs, HDI/micro-via/build-up, rigid flex PCBs, and other categories, each serving specific market needs. Rigid 1-2-sided PCBs remain crucial for basic electronic applications and LED lighting systems. The HDI/micro-via/build-up segment is gaining importance in applications requiring higher density and miniaturization. Rigid flex PCBs combine the benefits of both rigid and flexible circuits, finding applications in aerospace, automotive, and medical sectors. These segments collectively contribute to the market's diversity and cater to varying technological requirements across different industries.

Segment Analysis: By End-User Vertical

Industrial Electronics Segment in Europe PCB Market

The Industrial Electronics segment continues to dominate the European PCB market, commanding approximately 35% market share in 2024, with a valuation of USD 912.3 million. This significant market position is primarily driven by the widespread adoption of Industry 4.0 technologies across European manufacturing facilities, including the implementation of advanced automation systems, industrial IoT devices, and smart manufacturing solutions. The segment's growth is further supported by increasing investments in industrial automation, particularly in countries like Germany, France, and the UK, where manufacturing digitalization initiatives are gaining momentum. The deployment of PCB components in industrial control systems, SCADA applications, and various sensor-based monitoring systems has created substantial demand within this segment.

Automotive Segment in Europe PCB Market

The Automotive segment has emerged as the fastest-growing sector in the European PCB market, projected to grow at approximately 5% during 2024-2029. This remarkable growth is primarily attributed to the increasing integration of electronic components in modern vehicles, particularly in electric and autonomous vehicles. The segment's expansion is driven by the rising demand for advanced driver assistance systems (ADAS), in-vehicle infotainment systems, and electric vehicle control units. European automotive manufacturers' commitment to vehicle electrification and the implementation of stringent safety regulations requiring advanced electronic systems have further accelerated the adoption of PCBs in this sector. The trend toward connected vehicles and smart mobility solutions continues to create new opportunities for PCB manufacturers in the automotive industry.

Remaining Segments in End-User Vertical

The other segments in the European PCB market, including Aerospace & Defense, Consumer Electronics, Communications, Medical, and Other End-users, collectively represent diverse applications and opportunities. The Aerospace & Defense segment benefits from increasing defense modernization programs and satellite communication systems development. Consumer Electronics continues to drive innovation in flexible and high-density PCBs, while the Communications segment is experiencing growth due to 5G infrastructure deployment. The Medical segment shows promising growth potential due to the increasing adoption of advanced medical devices and diagnostic equipment. Each of these segments contributes uniquely to the market's overall dynamics, with varying requirements for PCB technology and specifications.

Europe PCB Market Geography Segment Analysis

PCB Market in Germany

Germany stands as the powerhouse of Europe's PCB industry, commanding approximately 44% of the regional market share in 2024. The country's dominance is underpinned by its robust automotive sector, where major manufacturers are increasingly incorporating advanced electronic systems and autonomous driving technologies. The presence of innovation clusters and cutting-edge manufacturing facilities has positioned Germany as a hub for printed circuit board production, particularly in high-density interconnect (HDI) and multilayer PCB segments. The country's commitment to Industry 4.0 initiatives has driven substantial investments in smart manufacturing technologies, fostering the development of sophisticated PCB solutions. German manufacturers have particularly excelled in producing automotive PCBs for electric vehicles, with companies focusing on developing boards that can handle higher power requirements and thermal management challenges. The country's strong focus on research and development, coupled with its established industrial infrastructure, continues to attract both domestic and international investments in PCB manufacturing capabilities.

PCB Market in United Kingdom

The United Kingdom's PCB market is projected to grow at approximately 4% CAGR from 2024 to 2029, marking it as the fastest-growing PCB market in Europe. The country's growth is primarily driven by its strong focus on aerospace and defense applications, where PCB demand remains consistently high. The UK government's initiatives to promote domestic electronic manufacturing capabilities have created a favorable environment for printed circuit board manufacturers. The country has developed particular expertise in high-reliability PCBs for critical applications, supported by stringent quality standards and certification requirements. British manufacturers have carved out a niche in specialized PCB solutions, particularly for medical PCBs and industrial automation applications. The presence of leading research institutions and technology companies has fostered innovation in PCB design and manufacturing processes. The UK's emphasis on sustainable manufacturing practices has also led to developments in environmentally friendly PCB production methods.

PCB Market in Italy

Italy's PCB market has established itself as a significant player in Europe's electronics manufacturing landscape, particularly excelling in industrial automation and machinery applications. The country's strength lies in its specialized manufacturing capabilities, especially in producing high-performance PCBs for industrial equipment and automotive applications. Italian manufacturers have developed expertise in complex multilayer PCBs, serving both domestic and international markets. The country's PCB industry benefits from strong integration with its manufacturing sector, particularly in industrial automation and machinery production. Recent investments in modernizing production facilities have enhanced the capability to produce more sophisticated PCB designs. The government's support for digital transformation through initiatives like Industria 4.0 has created new opportunities for PCB manufacturers. Italy's focus on quality and precision has made it a preferred supplier for high-reliability PCB applications.

PCB Market in France

France's PCB market has carved out a strong position in Europe's electronics manufacturing landscape, particularly in aerospace and defense applications. The country's PCB industry benefits from its strong aerospace sector, with manufacturers specializing in high-reliability boards for critical applications. French PCB manufacturers have developed particular expertise in flexible and rigid-flex PCBs, serving both domestic and international markets. The country's focus on technological innovation has led to advancements in PCB manufacturing processes and capabilities. Strong collaboration between industry and research institutions has fostered innovation in PCB design and manufacturing techniques. The French government's support for industrial modernization has encouraged investments in advanced manufacturing capabilities. The country's PCB industry has also benefited from its strong position in medical device manufacturing, requiring specialized PCB solutions.

PCB Market in Other Countries

The PCB market in other European countries, including Spain, the Netherlands, Belgium, Ireland, Norway, Sweden, and other nations, demonstrates diverse specializations and growth patterns. These markets are characterized by their focus on specific industry verticals, with some countries excelling in automotive electronics while others specialize in industrial automation or consumer electronics. The presence of specialized manufacturing clusters in these countries has fostered innovation in specific PCB applications. Many of these markets have developed unique competencies in niche segments, such as high-frequency PCBs or specialized flexible circuits. The increasing adoption of Industry 4.0 technologies across these countries has created new opportunities for PCB manufacturers. Regional cooperation and technology sharing have strengthened the overall competitiveness of these markets. These countries continue to invest in modernizing their manufacturing capabilities and developing expertise in emerging PCB technologies.

Get Analysis on Important Geographic Markets

Download PDF

Europe PCB Industry Overview

Top Companies in Europe PCB Market

The European PCB market features established players like Würth Elektronik Group, KSG GmbH, Aspocomp Group, LeitOn GmbH, and Becker & Müller Schaltungsdruck GmbH leading the competitive landscape. Companies are increasingly focusing on developing advanced PCB technologies, particularly in high-density interconnects (HDI) and flexible circuits, to meet the growing demands of the automotive and telecommunications sectors. The industry witnesses continuous investment in research and development activities, with manufacturers expanding their capabilities in areas like microvia technology and multi-layer PCBs. Operational excellence is being achieved through automation and Industry 4.0 integration, while strategic partnerships with technology providers and material suppliers strengthen the value chain. Companies are also expanding their geographical presence through acquisitions and new facility establishments, particularly in key markets like Germany and the United Kingdom, while simultaneously developing environmentally sustainable manufacturing processes.

Market Structure Shows Regional Leadership Dominance

The European PCB market exhibits a fragmented structure with a mix of global conglomerates and regional specialists, where German manufacturers hold significant market share due to their strong presence in the automotive and industrial electronics sectors. The market is characterized by the presence of both vertically integrated manufacturers offering end-to-end solutions and specialized players focusing on niche segments like high-frequency PCBs or flex-rigid boards. The competitive dynamics are shaped by established domestic manufacturers with strong local customer relationships competing against global players who bring advanced technologies and economies of scale.

The industry has witnessed considerable consolidation through mergers and acquisitions, particularly as companies seek to expand their technological capabilities and geographic reach. Notable trends include larger companies acquiring specialized manufacturers to enhance their product portfolios and enter new market segments. Cross-border acquisitions have become increasingly common as companies aim to strengthen their presence across different European regions and gain access to new customer bases, while also investing in manufacturing facilities to maintain competitive advantages in terms of quality and delivery times.

Innovation and Adaptability Drive Future Success

Success in the European PCB market increasingly depends on companies' ability to adapt to rapidly evolving technological requirements and maintain strong relationships with key customers in the automotive, telecommunications, and industrial sectors. Market leaders are investing heavily in advanced PCB manufacturing capabilities and quality management systems to meet stringent industry standards and regulatory requirements. Companies are also focusing on developing specialized solutions for emerging applications in electric vehicles, 5G infrastructure, and medical devices, while maintaining flexibility in their production processes to accommodate both high-mix, low-volume and low-mix, high-volume orders.

The competitive landscape is further shaped by the need to address environmental regulations and sustainability requirements, with successful companies implementing eco-friendly manufacturing processes and developing recyclable printed circuit board solutions. Market participants are increasingly focusing on building robust supply chains to mitigate risks and ensure consistent delivery capabilities, while also investing in digital transformation initiatives to improve operational efficiency. The ability to provide value-added services such as design support, prototyping, and testing capabilities is becoming crucial for maintaining competitive advantage, as is the development of strong technical expertise in emerging technologies like embedded components and high-frequency applications.

Europe PCB Market Leaders

-

Jabil Inc.

-

Aspocomp Group PLC

-

KSG GmbH

-

Benchmark Electronics Inc.

-

Wurth Elektronik Group (Wurth Group)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe PCB Market News

- December 2022 - ICAPE Group announced the acquisition of 100% of the shares in MMAB Group, a Swedish PCB manufacturer and distributor. MMAB Group's addition confirms the company's external growth target for 2022, securing USD 35 million in additional revenue. With its proven ability to make acquisitions, the company intends to pursue this offensive strategy in the short and medium term while maintaining a policy of optimizing organization and solid organic growth.

- November 2022 - UnimicronGermany, headquartered in Geldern, North Rhine-Westphalia, committed to investing an additional EUR 12 million (USD 12.89 million) in new infrastructure, equipment, and buildings in 2022.

Europe PCB Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Degree of Competition

-

4.3 Industry Value Chain Analysis

- 4.3.1 Typical PCB Manufacturing Workflow

- 4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rising demand for miniaturization of technology and growth in diversity and density of PCBs

- 5.1.2 Increasing R&D and investments in PCB manufacturing in Europe

- 5.1.3 Increasing adoption of flexible and flex-rigid PCBs (Wearable electronics, Flexible displays and Medical applications)

-

5.2 Market Restraints

- 5.2.1 Increasing complexity due to miniaturization of components

- 5.2.2 Strict requirements to comply with legislations

6. MARKET SEGMENTATION

-

6.1 By Category

- 6.1.1 Standard Multilayer PCBs

- 6.1.2 Rigid 1-2-sided PCBs

- 6.1.3 HDI/Micro-via/Build-up

- 6.1.4 Flexible PCBs

- 6.1.5 Rigid Flex PCBs

- 6.1.6 Other Categories

-

6.2 By End-user Vertical

- 6.2.1 Industrial Electronics

- 6.2.2 Aerospace and Defense

- 6.2.3 Consumer Electronics

- 6.2.4 Communications

- 6.2.5 Automotive

- 6.2.6 Medical

- 6.2.7 Other End-user Verticals

-

6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Rest of Europe

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Jabil Inc.

- 7.1.2 Aspocomp Group PLC

- 7.1.3 KSG GmbH

- 7.1.4 Benchmark Electronics Inc.

- 7.1.5 Wurth Elektronik Group (Wurth Group)

- 7.1.6 LeitOn GmbH

- 7.1.7 MicroCirtec Micro Circuit Technology GmbH

- 7.1.8 Becker & Muller Schaltungsdruck GmbH

- 7.1.9 AT&S Austria Technologies & Systemtechnik AG

- 7.1.10 MEKTEC Europe GmbH (Nippon Mektron Ltd)

- 7.1.11 Unimicron Technology Corporation

- 7.1.12 Sumitomo Electric Industries Ltd (Sumitomo Corporation)

- 7.1.13 ICAPE Group

- 7.1.14 Elvia PCB Group

- 7.1.15 Fujikura Ltd

- 7.1.16 Multek Corporation

- 7.1.17 NCAB Group

- 7.1.18 Exception PCB Limited

- 7.1.19 Lab Circuits

- 7.1.20 Eurocircuits

- 7.1.21 TTM Technologies Inc.

- *List Not Exhaustive

8. MARKET OUTLOOK

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe PCB Industry Segmentation

A printed circuit board, or PCB, helps mechanically and electrically connect electronic components utilizing conductive pathways, tracks, or signal traces engraved from copper sheets laminated onto a non-conductive substrate. PCBs dominate electronic devices and can be easily identified as green-colored boards.

The Europe Printed Circuit Board Market is segmented by Category (Standard Multilayer PCBs, Rigid 1-2-sided PCBs, HDI/Micro-via/Build-up, Flexible PCBs, Rigid-flex PCBs, and other categories), End-user Vertical (Industrial Electronics, Aerospace & Defense, Consumer Electronics, Communications, Automotive, Medical, and other end-user verticals), Country (United Kingdom, Germany, France, Italy, Spain, and rest of Europe). The report offers market forecasts and size in volume (million units) and value (USD million) for all the above segments.

| By Category | Standard Multilayer PCBs |

| Rigid 1-2-sided PCBs | |

| HDI/Micro-via/Build-up | |

| Flexible PCBs | |

| Rigid Flex PCBs | |

| Other Categories | |

| By End-user Vertical | Industrial Electronics |

| Aerospace and Defense | |

| Consumer Electronics | |

| Communications | |

| Automotive | |

| Medical | |

| Other End-user Verticals | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe PCB Market Research FAQs

How big is the Europe PCB Market?

The Europe PCB Market size is expected to reach USD 2.67 billion in 2025 and grow at a CAGR of 2.80% to reach USD 3.07 billion by 2030.

What is the current Europe PCB Market size?

In 2025, the Europe PCB Market size is expected to reach USD 2.67 billion.

Who are the key players in Europe PCB Market?

Jabil Inc., Aspocomp Group PLC, KSG GmbH, Benchmark Electronics Inc. and Wurth Elektronik Group (Wurth Group) are the major companies operating in the Europe PCB Market.

What years does this Europe PCB Market cover, and what was the market size in 2024?

In 2024, the Europe PCB Market size was estimated at USD 2.60 billion. The report covers the Europe PCB Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe PCB Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe PCB Market Research

Mordor Intelligence offers a comprehensive analysis of the printed circuit board industry. We leverage extensive expertise in PCB and PCBA technologies. Our research covers the complete spectrum of circuit board manufacturing, from PCB design to PCB assembly processes. The report provides detailed insights into various technologies, including surface mount technology, flexible PCB, HDI PCB, and multilayer PCB solutions. Additionally, it offers a thorough analysis of PCB materials and PCB components.

Stakeholders across industries benefit from our detailed examination of electronic circuit board applications. These include automotive PCB, medical PCB, aerospace PCB, and PCBs for consumer electronics sectors. The report, available as an easy-to-download PDF, covers industrial PCB implementations, embedded PCB solutions, and rigid PCB technologies. Our analysis includes PCB manufacturing trends, PCB prototype development, and the evolution of printed wiring board (PWB) technologies. It provides valuable insights for manufacturers, suppliers, and industry professionals seeking to understand the European PCB landscape.