Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

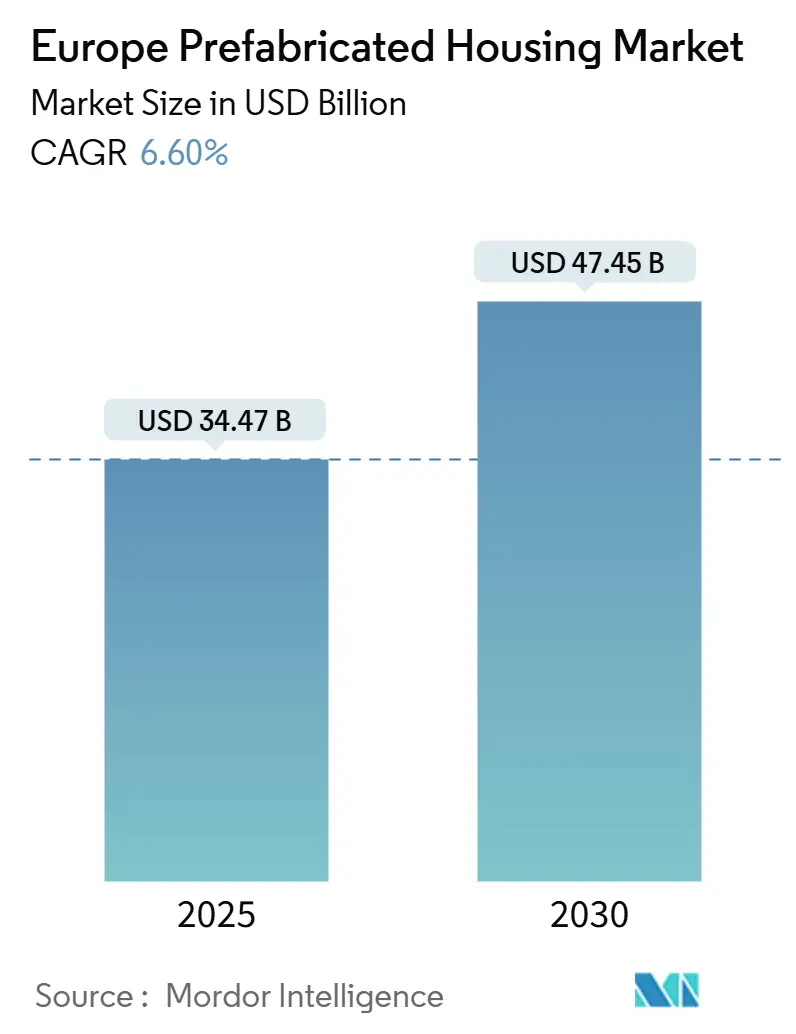

| Market Size (2025) | USD 34.47 Billion |

| Market Size (2030) | USD 47.45 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Prefabricated Housing Market Analysis by Mordor Intelligence

The Europe prefabricated housing market is estimated at USD 34.47 billion in 2025 and is expected to reach USD 47.45 billion by 2030, at a CAGR of 6.60% during the forecast period (2025-2030). This trajectory underscores the segment’s transition from a niche construction method to a mainstream residential solution across the continent. Mounting zero-emission mandates, persistent housing shortages, and rapid advances in off-site manufacturing are converging to accelerate adoption. Energy-performance regulation now rewards factory-built envelopes that embed renewable systems, while robotics and BIM-enabled production slash build times by up to 50% and project costs by 20%.[1]IFR International Federation of Robotics, “KR QUANTEC prints 3D facades for Belgian construction group,” ifr.org

As investors direct record sums into sustainable real-estate funds, the Europe prefabricated housing market is poised to capture a larger share of new-build activity, particularly in countries that link green-finance incentives to carbon-negative materials such as timber. Competitive intensity is rising as incumbents integrate vertically from design to installation and as technology start-ups introduce automated micro-factories that de-risk labor shortages.

Key Report Takeaways

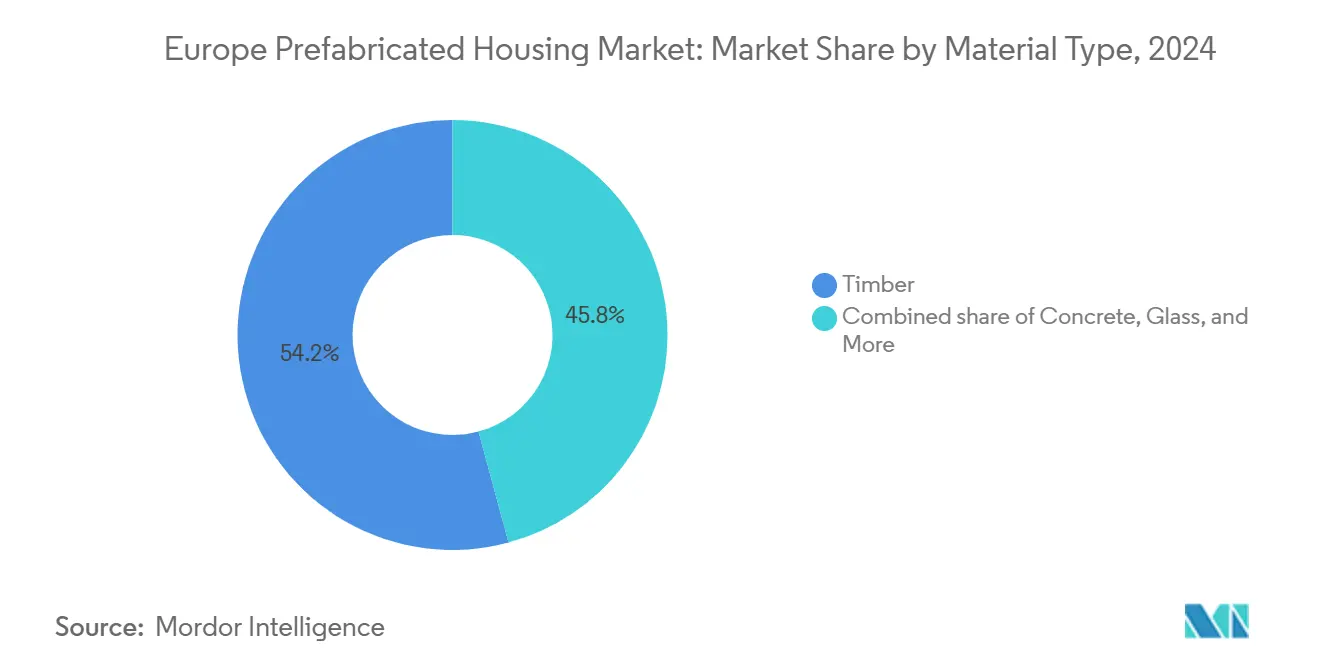

- By material, timber led with 54.20% of the Europe prefabricated housing market share in 2024.

- By housing type, single-family formats held a 71.00% share of the European prefabricated housing market size in 2024.

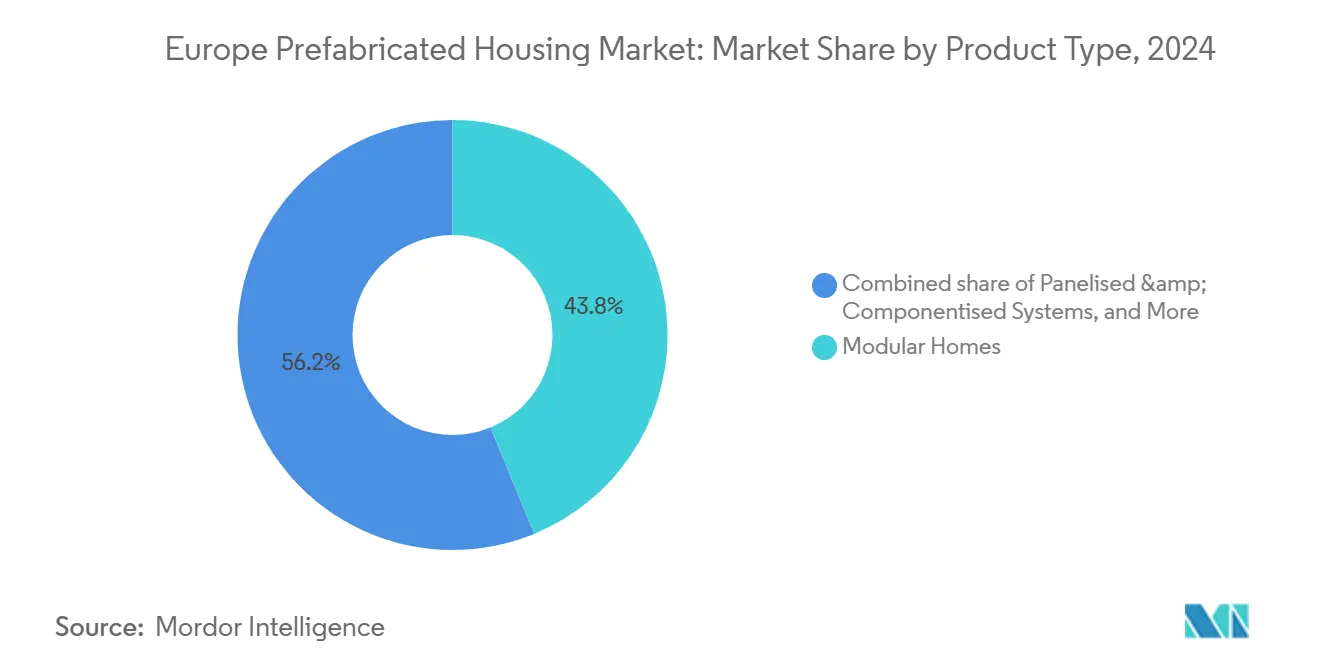

- By product type, modular homes commanded 43.80% of the Europe prefabricated housing market size in 2024 and are advancing at a 7.19% CAGR through 2030.

- By country, Germany accounted for 27.40% of the Europe prefabricated housing market size in 2024, while Sweden is projected to expand at a 7.39% CAGR to 2030.

Europe Prefabricated Housing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave & EPBD mandates fuel energy-efficient prefab retrofits | +1.2% | EU-wide; strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| 2 million-unit affordable-housing gap drives serial-construction tenders | +1.8% | Germany, France, UK; spillover to Eastern Europe | Long term (≥ 4 years) |

| Factory automation & robotics offset skilled-labor shortages | +1.1% | Nordic bloc, Germany, Netherlands | Medium term (2-4 years) |

| Green-finance taxonomies lower mortgage rates for timber modules | +0.9% | Core EU markets with mature green-finance regimes | Short term (≤ 2 years) |

| NATO & civil-protection contracts spur rapid-deploy volumetric units | +0.3% | Border and disaster-prone regions | Short term (≤ 2 years) |

| BIM-integrated 3-D printing shortens foundation lead times by 25% | +0.7% | Germany, Sweden, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Renovation Wave & EPBD Mandates Fuel Energy-Efficient Prefab Retrofits

Revisions to the Energy Performance of Buildings Directive require Member States to retrofit the lowest-performing 16% of non-residential stock by 2030 and to achieve zero on-site emissions in all new buildings that year. Governments are therefore promoting standardized, factory-produced wall, roof and façade modules that deliver predictable thermal performance and minimal waste. Germany’s implementation blueprint emphasizes off-site assembly as a pathway to halve construction time lines and demonstrate verifiable carbon savings under ISO 14001 management systems.[2]European Parliament, “Revision of the Energy Performance of Buildings Directive,” europarl.europa.eu Green-mortgage programs further amplify demand, trimming interest margins for households that opt for certified prefab envelopes, while public bodies accelerate school and hospital retrofits through serial contracting frameworks.

2 Million-Unit Affordable-Housing Gap Drives Serial-Construction Tenders

Eurostat estimates reveal a continent-wide deficit of roughly 2 million affordable dwellings, prompting authorities to bundle procurement lots that specify repeatable volumetric or panelized designs. Berlin’s Gewobag utility recently executed a 1,500-unit social-housing order in under 18 months at a unit cost 50% below average inner-city delivery, thanks to modular tender rules. The United Kingdom’s Pan-London Accommodation Collaborative Enterprise deployed a GBP 75 million framework for relocatable homes, demonstrating political commitment to precision manufacturing that meets both social and energy targets. As serial contracting migrates eastward, suppliers that standardize building systems for cross-border codes are best positioned to scale.

Factory Automation & Robotics Offset Skilled-Labor Shortages

Nearly 20% of Europe’s construction workforce will reach retirement age by 2030, intensifying reliance on automated production lines that fabricate floor cassettes, wall panels and volumetric pods around the clock. Robotics suppliers report 30% labor-cost savings and 80% logistics reductions when micro-factories are sited close to demand clusters. Corporate alliances—such as Wienerberger’s prefabricated wall initiative and Lindbäcks’ fully automated Swedish plant—illustrate how industrial methods translate into 3,500 turnkey units per year with tolerances measured in millimeters.

Green-Finance Taxonomies Lower Mortgage Rates for Timber Modules

The EU Taxonomy channels capital toward activities aligned with net-zero targets and has unlocked EUR 249 billion for qualifying construction practices. Over half of large European banks now embed Taxonomy scoring in mortgage underwriting, shaving lending costs for households purchasing timber-based homes that outperform energy baselines. Builders responding to the taxonomy combine carbon-storing mass-timber frames with phase-change insulation and rooftop photovoltaics, enabling life-cycle emission cuts of 35% compared with masonry equivalents. As lenders market “green-plus” mortgages, the Europe prefabricated housing market captures incremental demand that conventional on-site building cannot satisfy.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-digit input-cost inflation erodes prefab price advantage | -1.4% | EU-wide, particularly affecting material-intensive markets | Short term (≤ 2 years) |

| Fragmented national building codes & warranty rules delay approvals | -0.8% | Cross-border operations, standardization-dependent markets | Medium term (2-4 years) |

| Road-escort & width limits raise logistics cost for oversized modules | -0.6% | Continental Europe, cross-border transport corridors | Medium term (2-4 years) |

| "Catalogue-house" stigma depresses demand in dense urban cores | -0.4% | Major metropolitan areas: London, Paris, Berlin, Amsterdam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Double-Digit Input-Cost Inflation Erodes Prefab Price Advantage

The EU construction-cost index reached 117.00 points in December 2024, reflecting a 27.5% year-on-year rise in cement prices and a 42% jump in structural steel. Prefabrication, once 15% cheaper than in-situ methods, now risks parity for cost-sensitive projects, especially in affordable housing. Timber supply is tightening as sustainable-forestry quotas cap hardwood harvests, inflating saw-log prices and shrinking margins for module producers. Firms locked into fixed-price public contracts face pronounced margin pressure and must increasingly hedge raw-material exposure through forward purchasing agreements.

Fragmented National Building Codes & Warranty Rules Delay Approvals

Despite EU efforts at harmonization, variations persist among Member States on seismic design, fire classification and transport dimensions. Germany’s regional codes differ on allowable module heights, while France employs a hybrid public-private certification model that extends project vetting. Cross-border shippers confront inconsistent escort rules for oversized loads, even under Directive 96/53/EC. Warranty requirements also vary, creating insurance complexity that raises transaction costs and slows market entry.[3]CFPA Europe, “National Regulations,” cfpa-e.eu

Segment Analysis

By Material Type: Timber Dominates Green Transition

Timber captured 54.20% of Europe prefabricated housing market share in 2024, owing to carbon-sequestration benefits that align with Taxonomy-linked financing. The segment is projected to clock a 7.26% CAGR through 2030, outpacing steel and concrete. Sweden has introduced building-code amendments that prioritize mass-timber structures in public projects, accelerating demand for cross-laminated components. Hybrid wood-steel frames developed by KLEUSBERG extend timber’s application to mid-rise urban infill while preserving structural rigidity[4]KLEUSBERG, “Modulare Holzhybridbauweise,” kleusberg.de. Concrete remains essential for podiums and foundations, but its share is progressively eroded by printed masonry alternatives that cut embodied carbon by integrating recycled aggregates.

Second-tier materials, including glass and advanced composites, fulfill performance niches such as high-spec façade systems with integrated photovoltaic cells. Steel maintains relevance in volumetric pods requiring long spans, yet higher import prices are pushing suppliers to adopt lighter-gauge alloys and modular connection details that reduce tonnage. EU circular-economy policies favor materials with established recycling loops, a criterion that benefits aluminum curtain-wall systems now entering prefabrication supply chains.

Note: Segment shares of all individual segments available upon report purchase

By Type: Multi-Family Gains Momentum

Single-family homes accounted for 71.00% of Europe's prefabricated housing market share in 2024, yet multi-family formats are expanding faster at a 6.93% CAGR to 2030. Urban densification policies and land-use constraints drive municipalities to favor apartment blocks that maximize floor-area ratios. The Juf Nienke project in Amsterdam delivered 61 prefabricated timber flats, half earmarked for essential workers, demonstrating how modular design meets affordability and zoning targets. Developers such as Skanska’s BoKlok platform replicate Scandinavian prototypes across Western Europe, delivering units competitively priced for households earning EUR 15,000–30,000 per year.

Economies of scale make multi-family schemes ideal for serial manufacturing, as repetitive floor plans permit high line-speed operation and warrant batch procurement. Centralized energy systems allow building owners to exceed EPBD performance thresholds cost-effectively, an advantage that single-family sites lack.

By Product Type: Modular Homes Lead Innovation

Modular units represented 43.80% of Europe prefabricated housing market size in 2024 and will post a 7.19% CAGR by 2030. Factory completion of 3-D volumes—including MEP, finishes, and fixtures—minimizes weather exposure and ensures repeatable quality. Panelized systems retain relevance where design freedom or site-access limits preclude volumetric delivery. Manufactured-home formats occupy a niche in regulated estate-park segments that rely on standardized transportable chassis.

Building information modeling drives product convergence by enabling clash-free detailing and digital-twin asset management. Concrete-printing technologies extend modular logic outdoors by producing integrated stair cores and façade panels that bolt directly to timber or steel cassettes, trimming erection schedules by an additional week per floor.

Geography Analysis

Germany Leads, Sweden Accelerates

Germany held 27.40% of Europe prefabricated housing market size in 2024, leveraging its mature off-site supply chains and reputable brands such as HUF Haus and WeberHaus. Federal affordable-housing initiatives now allow municipalities to fulfill up to 30% of demand via factory-made components, a policy expected to widen adoption beyond Bavaria and Baden-Württemberg. Bien-Zenker earned “Company of the Year 2025” honors for customer satisfaction in price, transparency and sustainability, underscoring consumer acceptance.

Sweden registers the fastest national CAGR at 7.39% through 2030, propelled by industrialized timber construction and full BIM adoption within municipal planning. The Nordic bloc benefits from liberal transport allowances for 34.5-meter modular carriers, enabling cross-border shipping efficiencies. The United Kingdom, France, Spain and Italy follow as sizable but policy-diverse markets, each experimenting with design catalogs and skills-training centers to foster modern-methods uptake.

Competitive Landscape

The Europe prefabricated housing market is moderately fragmented, with regional champions holding entrenched positions while new entrants leverage automation to gain share. German manufacturers typically integrate design, production and site assembly, delivering turnkey packages that minimize subcontract interface risk. Nordic suppliers differentiate through climate-positive timber systems and proprietary BIM libraries.

Strategic moves in 2024-2025 include Norvestor and MG Link’s acquisition of PCS Modulsystem to create a pan-Nordic group specializing in wood-based public buildings. Automated Architecture secured GBP 2.6 million to scale robot-assembled timber dwellings, signaling venture-capital appetite for micro-factory business models that promise 30% lower labor overheads. Established contractors such as Skanska have absorbed impairment charges in conventional property portfolios but continue to expand BoKlok prefabricated output under joint branding with IKEA.

Product innovation centers on digital twins, 3-D printing and circular-material sourcing. GOLDBECK’s Blue Buildings road map targets 35% CO₂ reduction per square meter by 2030, integrating photovoltaic façades with smart-energy grids. Suppliers with proprietary software stacks for design-for-manufacture-and-assembly (DfMA) maintain a compelling cost-quality proposition as codes lean toward embodied-carbon disclosure.

Europe Prefabricated Housing Industry Leaders

-

SchwörerHaus KG

-

Hanse Haus GmbH

-

WeberHaus GmbH & Co.

-

Bien-Zenker GmbH

-

ScanHaus Marlow GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Norvestor and MG Link completed acquisition of 100% of PCS Modulsystem AB, consolidating Nordic modular capacity.

- March 2025: Automated Architecture raised GBP 2.6 million to deploy robotic micro-factories in Belgium and the U.S.

- March 2025: Skanska recorded SEK 2.0 billion impairment, including SEK 0.5 billion in European residential development.

- November 2024: Laing O’Rourke opened the United Kingdom’s first modern-method training facility.

Europe Prefabricated Housing Market Report Scope

Prefabrication is the method of construction where components of a building structure are assembled either in a manufacturing or production site, transporting complete or partial assemblies to the site where the structure should be present. This work is carried out in two stages: manufacturing components in a place other than the final location and their erection in position.

The report covers a complete background analysis of the European prefabricated housing market. It includes the economic assessment and contribution of economic sectors, market overview, market size estimation for key segments, emerging market segments, market dynamics, geographical trends, and the impact of the COVID-19 pandemic.

The European prefabricated housing market is segmented by type (single-family and multi-family) and country (Germany, United Kingdom, France, and Rest of Europe). The report offers the European prefabricated housing market size and forecasts in value (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Housing Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelized & Componentized Systems |

| Manufactured Homes |

| Other Prefab Types |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Sweden |

| Denmark |

| Norway |

| Rest of Europe |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Housing Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelized & Componentized Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe prefabricated housing market?

The market is valued at USD 34.47 billion in 2025 and is set to reach USD 47.45 billion by 2030.

How fast is prefabricated housing growing across Europe?

The sector is forecast to post a 6.60% CAGR between 2025 and 2030, led by regulatory zero-emission mandates and automation gains.

Which material dominates factory-built homes in Europe?

Timber leads with 54.20% share, buoyed by EU green-finance incentives and carbon-sequestration benefits.

Why are modular homes gaining favor over other prefab types?

Modular units arrive on site 95% complete, cutting build times by roughly half and delivering consistent quality under factory conditions.

Which European country holds the largest share of prefab adoption?

Germany leads with 27.40% of regional value, backed by strong industrial capacity and buyer acceptance of sustainably certified homes.

Page last updated on: