| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.99 Billion |

| Market Size (2030) | USD 8.13 Billion |

| CAGR (2025 - 2030) | 15.30 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Precision Farming Market Analysis

The Europe Precision Farming Market size is estimated at USD 3.99 billion in 2025, and is expected to reach USD 8.13 billion by 2030, at a CAGR of 15.3% during the forecast period (2025-2030).

The European precision farming landscape is undergoing significant transformation driven by the integration of advanced technologies and policy reforms. The new Common Agricultural Policy (CAP) reform post-2022 has opened doors for public funding to support precision farming adoption through various interventions, including rural development investments in machinery, farm advisory services, and eco-scheme payments. This policy framework aligns with the European Green Deal and Farm-to-Fork strategy, positioning Europe as a frontrunner in transforming the global food industry by setting aspirational goals for fair, healthy, and environmentally friendly food systems. The strategic focus on modernizing agriculture through precision farming is reflected in the National CAP Strategic Plans 2023-2027, which are being developed to ensure sustainable agricultural practices across the region.

The integration of digital agriculture and farm modernization has become increasingly prominent across European farms. ICT-AGRI, a European Research Area Network (ERA-NET), is actively coordinating research in ICT and robotics to create a common approach and shared priorities for agricultural technology implementation. This coordination has led to the development of innovative projects testing viable alternatives to harmful pesticides and herbicides, including non-chemical weed control in vineyards and precision farming techniques for more precise weed control. These initiatives demonstrate the region's commitment to combining traditional methods with advanced technologies to enhance agricultural productivity while maintaining environmental sustainability.

The emergence of smart farming technologies has revolutionized traditional agricultural practices in Europe. Precision farming technologies are being increasingly deployed for various applications, from soil monitoring and crop scouting to variable rate application of inputs. The adoption of these technologies is particularly evident in high-value crops, plantation crops, and forestry plantations, where large areas and irregular terrains make conventional farming methods challenging. The integration of soil monitoring systems with the EU Soil Observatory (EUSO) program has enabled better capture of soil functions through modern measuring techniques like proximal sensing and novel data processing tools.

The European agricultural sector is witnessing a significant shift towards automation and data-driven decision-making. The implementation of precision farming techniques has enabled farmers to optimize crop yields while reducing input costs through more efficient resource utilization. Various EU policy initiatives, including the EU Green Deal and its Farm-to-Fork strategy, are designing long-term solutions to achieve healthier food production and more sustainable agriculture. These initiatives are complemented by the Biodiversity Strategy, which aims to tackle plant health threats while promoting environmentally conscious farming practices. The integration of these policies with precision agriculture technologies is creating a more resilient and sustainable agricultural sector in Europe.

Europe Precision Farming Market Trends

Increasing Use of IoT in Agricultural Sector

The agricultural sector in Europe is experiencing a significant transformation through the integration of Internet of Things (IoT) technologies, particularly in precision farming applications. Agricultural IoT solutions are being increasingly deployed across various aspects, including smart farming, agricultural robotics, RFID sensors and tracking, field sensors, livestock monitoring, equipment sensors, and agricultural drone-based crop monitoring. These technologies are helping farmers make data-driven decisions, improve operational efficiency, and achieve better returns on investment while ensuring overall site security. The implementation of IoT has become particularly crucial as farmers seek sustainable solutions to long-standing challenges in crop and cattle management.

Various EU policy initiatives, including the EU Green Deal, Farm-to-Fork strategy, and the Biodiversity Strategy, are actively promoting the adoption of agricultural IoT-based solutions in agriculture. These initiatives are designed to achieve healthier food production, more sustainable agriculture, and better plant health protection. Several innovative projects across Europe demonstrate this trend, including an Italian Operational Group testing non-chemical weed control in vineyards, an Austrian group developing tailored flower mixtures to attract natural aphid predators, and a German initiative combining traditional methods with precision farming techniques for more precise weed control. These projects showcase how IoT integration is enabling farmers to protect their crops while reducing dependency on harmful pesticides and herbicides.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Focus on Sustainability and Food Security

The growing emphasis on sustainability and food security is becoming a primary driver for precision farming adoption across Europe. With global population projections indicating over 9.5 billion people by 2050, there is an urgent need to increase agricultural output by 70-100% while simultaneously reducing land usage, optimizing yields, and lowering greenhouse gas emissions. The European Green Deal and Farm to Fork Strategy have positioned Europe as a frontrunner in transforming the global food industry by establishing ambitious goals for creating a fair, healthy, and environmentally friendly food system. These initiatives are compelling farmers to adopt digital tools and smart, sustainable farming practices to optimize crop yields and protect soil health while reducing their carbon footprint.

The concepts of precision farming and sustainability are becoming increasingly interconnected, with precision farming technologies enabling more environmentally conscious crop production management. Through site-specific knowledge integration, farmers can target rates of fertilizer, seed, and chemicals based on soil conditions and other environmental factors. The European Union has taken significant steps in this direction, making precision farming one of the pillars of the Common Agricultural Policy with substantial R&D investments. The policy framework emphasizes four key sustainability pillars: social sustainability, economic sustainability, environmental sustainability, and agricultural modernization, all of which are supported by precision farming technologies and practices.

Rising Labor Shortages in Europe

The European agricultural sector is facing significant challenges due to increasing labor shortages, particularly in the fruit and vegetable sector, which heavily relies on seasonal workers. The sector's labor-intensive nature, requiring high numbers of agricultural workers for activities such as tending, harvesting, and packaging, has traditionally been managed by farmers themselves. However, the ongoing consolidation in EU agriculture has resulted in fewer but larger farms, creating a greater dependence on hired workers for farm operations. This structural change, combined with the challenges in securing reliable seasonal labor, is driving the adoption of farm automation technologies that can automate various agricultural tasks.

The situation is further complicated by the nature of seasonal work contracts and the role of private employment agencies. According to the Migration Policy Institute, these agencies often act as both recruiters and employers, serving as intermediaries between clients and workers in the agricultural sector. The complexity of this arrangement, coupled with issues such as limited job security and social security coverage for seasonal workers, has created additional challenges in maintaining a stable agricultural workforce. This labor market instability has become a pivotal factor pushing the European agriculture sector toward adopting less labor-intensive farm automation technologies. The trend is particularly evident in countries like Germany, where precision farming is being implemented in agricultural operations covering more than 500 hectares of arable land, with a notable 69% of farmers adopting technologies such as agricultural drones for agribusiness operations.

Segment Analysis: Technology

Guidance System Segment in Europe Precision Farming Market

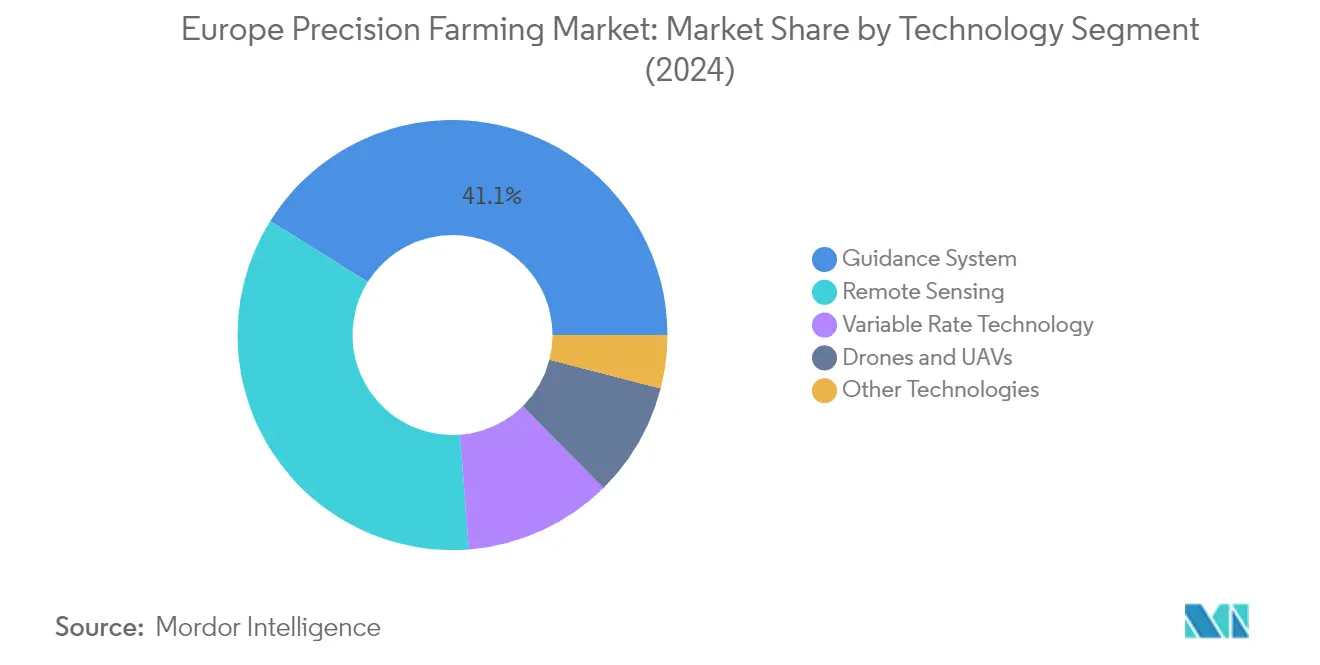

The Guidance System segment continues to dominate the European precision farming technology landscape, holding approximately 41% market share in 2024. This segment's prominence is driven by the increasing adoption of GPS/GNSS and GIS technologies that enable farmers to achieve superior accuracy in field operations. The technology helps improve field efficiency by providing hands-free steering capabilities, reducing overlaps, and maximizing the utilization of agricultural inputs. Modern guidance systems are becoming increasingly sophisticated, offering features like automatic calibration, real-time kinematic corrections, and integration with other precision farming tools, making them indispensable for large-scale farming operations across Europe.

Drones and UAVs Segment in Europe Precision Farming Market

The Drones and UAVs segment is emerging as the most dynamic sector in the European precision farming technology market, projected to grow at approximately 20% annually from 2024 to 2029. This remarkable growth is fueled by the increasing application of drone technology in crop monitoring, precision spraying, and field mapping activities. The adoption of drones is revolutionizing farming practices by providing real-time aerial imagery, enabling precise crop health assessment, and facilitating targeted interventions. The integration of artificial intelligence and machine learning capabilities with drone technology is further enhancing their utility in agricultural operations, making them an increasingly essential tool for modern farming practices.

Remaining Segments in Technology

The other significant segments in the European precision farming technology market include Remote Sensing, Variable Rate Technology, and Other Technologies. Remote Sensing technologies are crucial for collecting field data and monitoring crop conditions through various sensors and imaging systems. Variable Rate Technology enables precise application of inputs like fertilizers, seeds, and pesticides based on field variability. The Other Technologies segment encompasses emerging solutions such as IoT sensors, automated irrigation systems, and smart machinery interfaces. These segments collectively contribute to the comprehensive technological ecosystem that is transforming traditional farming practices into data-driven, efficient operations across Europe.

Segment Analysis: Components

Services Segment in Europe Precision Farming Market

The services segment dominates the Europe precision farming market, accounting for approximately 55% market share in 2024. This segment encompasses various critical services including signal subscription, yield monitor calibrations, mapping, seed and fertilizer recommendations, remote services, equipment installation, soil sampling, and in-season technology support. The major sector within services is signal subscription, with RTK signals helping increase accuracy to centimeter-level precision. The growing digital farming services sector has seen many companies focusing on providing innovative services, with products like SMS Basic, SMS Advanced, SMS Mobile, AgFiniti, and APEX being widely adopted. Additionally, this segment is experiencing the fastest growth rate of around 17% for the forecast period 2024-2029, driven by the launch of new crop monitoring services that have enhanced the ease of application of various crop monitoring technologies in digital farming.

Hardware and Software Segments in Europe Precision Farming Market

The hardware and software segments play crucial complementary roles in the precision farming ecosystem. The hardware segment includes various agricultural sensors installed in farms for monitoring moisture, temperature, water, and nutrients, along with communication devices capable of transmitting analog or digital signals. Flow and automatic control devices ensure steady distribution of fertilizers, pesticides, and other products by automatically adjusting the flow. The software segment focuses on digital agriculture management and the need for handling temporal and spatial variability of fields. Farm management software is particularly applicable for large agriculture and livestock farms, while various tools and software in agriculture aim at reducing uncertainties in decision-making processes. Both segments continue to evolve with technological advancements and increasing integration capabilities.

Segment Analysis: By Application

Yield Monitoring Segment in Europe Precision Farming Market

Yield monitoring continues to dominate the Europe precision farming market, holding approximately 43% market share in 2024. This segment's prominence is driven by the increasing concern about enhancing crop yields and the growing adoption of IoT-based monitoring systems. The integration of sensor-based monitoring systems and Decision Support Systems (DSS) in Europe delivers farmers and stakeholders comprehensive information and early warning capabilities based on crop status, pest attacks, and disease infestation. Advanced yield data collection through dense point data sets and high-resolution satellite imagery supports nutrient intake optimization and plant density management, particularly in cereal fields. The technology's ability to provide real-time monitoring and data-driven insights has made it an essential tool for modern farming operations seeking to maximize productivity and efficiency.

Variable Rate Application Segment in Europe Precision Farming Market

The Variable Rate Application (VRA) segment is projected to experience the fastest growth in the Europe precision farming market, with an estimated growth rate of around 16% during 2024-2029. This rapid growth is attributed to the increasing utilization of fertilizers and other chemical ingredients in limited arable land throughout the region. VRA technology focuses on diverse areas in farming activities including fertilization, lime application, weed control, irrigation, and seeding. The system develops site-specific maps of soil nutrient properties and utilizes sophisticated algorithms for precise fertilizer prescription and application control. The adoption of advanced technologies such as GPS for mapping and georeferencing of land, coupled with NIR technology for optimizing soil fertility, is driving the segment's growth. The technology's ability to reduce input costs while maximizing efficiency has made it particularly attractive to modern farmers seeking sustainable agricultural practices.

Remaining Segments in Application Market Segmentation

The other significant segments in the Europe precision farming market include Field Mapping, Soil Monitoring, Crop Scouting, and Other Applications. Field mapping technology has become crucial for collecting geospatial information regarding plant and soil properties using advanced tools like GPS and GIS systems. Soil monitoring applications have gained importance due to increasing concerns about soil moisture deficiency and excessive nutrient inputs, while crop scouting leverages advanced technologies like drones and GPS for pest management and crop health monitoring. These segments collectively contribute to the comprehensive precision farming ecosystem, enabling farmers to make data-driven decisions across various aspects of agricultural operations. The integration of these technologies has become particularly important as European agriculture moves towards more sustainable and efficient farming practices.

Europe Precision Farming Market Geography Segment Analysis

Precision Farming Market in Germany

Germany leads the European precision farming landscape with approximately 26% market share in the region. The country's agricultural sector has witnessed widespread adoption of modern farming techniques, particularly in data collection methods like agricultural GPS-based area measurement and soil sampling. German farmers, especially those managing large agricultural contractor services exceeding 500 hectares, have embraced precision farming technologies for comprehensive monitoring of soil health, plant growth, and overall farm management. The increasing awareness and implementation of agricultural drone applications in modular precision farming technology have significantly enhanced farming efficiency. The eastern federal states of Germany demonstrate a notably high proportion of educated farmers, contributing to better technology adoption and implementation. The combination of advanced education, substantial landholdings, and progressive farming practices has positioned Germany as a pioneer in smart farming innovation. The country's commitment to sustainable agriculture and technological advancement continues to drive the evolution of digital farming practices, making it a benchmark for other European nations in agricultural modernization.

Precision Farming Market in Italy

Italy's precision farming market is projected to grow at approximately 16% CAGR from 2024 to 2029, marking it as one of the most dynamic markets in Europe. The country has made significant strides in implementing real-time monitoring systems through innovative IT platforms integrated with field sensors. Italian farmers are increasingly adopting precision farming tools based on socioeconomic, financial, and contingent factors. The market has seen particular success in regions like the Plain of Tarquinia, where farmers are actively embracing various technology features. The adoption pattern shows a clear correlation with labor intensity, with precision farming adopters reporting higher efficiency in operations exceeding 50 days per hectare. Italian agricultural stakeholders have demonstrated strong interest in telematics applications, automated systems, and data-driven decision-making tools. The country's focus on optimizing nutrient management and reducing environmental impact through precision technologies has created a robust ecosystem for continued market expansion. The integration of advanced monitoring systems and smart farming practices has positioned Italy as a key growth market in European precision farming.

Precision Farming Market in France

France has established itself as a pivotal market in European precision farming, leveraging its position as the leading agricultural country in the European region. The country's precision farming landscape is characterized by strong adoption of digital farming modules, particularly in farm cooperatives and agricultural extension services. French farmers have shown particular interest in computer-controlled variable rate applications and agricultural mapping technologies. The Digital Agriculture Adoption Observatory has documented significant progress in remote sensing implementation, with 85% of remote sensing captured by satellite and 15% by drones or other UAV hardware, primarily in field crops and grape vineyards. The country's agricultural sector has witnessed substantial transformation through precision spraying tools and advanced monitoring systems. French farmers' increasing focus on environmental sustainability and efficient resource utilization has driven the adoption of precision farming technologies, particularly in cereal and vegetable crops. The integration of these technologies has significantly enhanced productivity while promoting sustainable farming practices across the nation.

Precision Farming Market in United Kingdom

The United Kingdom has emerged as a significant player in the precision farming sector, driven by the need to optimize agricultural productivity within limited arable land. British farmers have shown particular enthusiasm for map-based variable rate technology, especially in fertilizer application. The country's agricultural sector has witnessed significant technological transformation, particularly in developing variable seed rate maps using canopy sensing information. The implementation of advanced algorithms for predicting optimum seed rates in cereal crops has revolutionized farming practices in regions like East Yorkshire. The UK's approach to precision farming emphasizes the integration of modern technologies with traditional farming methods, creating a balanced and efficient agricultural system. The government's support through various schemes and initiatives has further accelerated the adoption of precision farming technologies. The focus on modernizing equipment and improving crop productivity has created a robust ecosystem for precision farming development, making the UK a key market for agricultural innovation.

Precision Farming Market in Other Countries

Other European countries, including Spain, Sweden, and Poland, have shown remarkable progress in adopting precision farming technologies. These markets are characterized by increasing utilization of soil testing, satellite imagery, and variable rate applications to enhance crop yields and minimize pest infestation. Spain has made significant strides in precision viticulture, while Poland has focused on robotics integration in farming operations. Sweden has demonstrated particular interest in drone services and advanced image algorithms for vegetable growing operations. The agricultural sectors in these countries are increasingly embracing innovative technologies to optimize production processes and improve resource efficiency. The diverse approaches to precision farming adoption across these nations reflect the adaptability and versatility of these technologies in different agricultural contexts. The continued evolution of precision farming practices in these markets suggests a promising future for agricultural technology adoption across Europe.

Get Analysis on Important Geographic Markets

Download PDF

Europe Precision Farming Industry Overview

Top Companies in Europe Precision Farming Market

The European precision farming landscape is characterized by intense innovation and strategic developments from major players like Deere & Company, Bayer CropScience, Trimble Inc., and AGCO Corporation. Companies are heavily investing in research and development to launch advanced autonomous farming solutions, GPS-guided equipment, and integrated software platforms. The industry has witnessed a strong focus on developing AI and machine learning capabilities, with companies establishing dedicated innovation centers and research facilities across Europe. Strategic partnerships, particularly between equipment manufacturers and technology providers, have become increasingly common to enhance product offerings and market reach. Companies are also expanding their presence through acquisitions of regional players and technology startups, especially those specializing in agricultural robotics and automation solutions. The market demonstrates a clear trend towards developing comprehensive end-to-end farm automation solutions rather than standalone products, with major players investing in cloud-based platforms and agricultural data analytics capabilities.

Consolidated Market Led By Global Players

The European precision farming market exhibits a relatively consolidated structure dominated by large multinational corporations with diverse agricultural technology portfolios. These industry leaders leverage their extensive research capabilities, established distribution networks, and strong financial positions to maintain their market dominance. The market has seen significant merger and acquisition activity, particularly involving the acquisition of innovative startups by established players to enhance their technological capabilities and expand their solution offerings. Regional players, while present in specific market segments, often struggle to compete with the comprehensive solutions offered by global leaders.

The competitive dynamics are shaped by the presence of both pure-play precision farming companies and diversified agtech conglomerates. Global players benefit from their ability to offer integrated solutions across the farming value chain, while specialized companies focus on developing niche technologies and applications. The market has witnessed increased collaboration between traditional equipment manufacturers and technology companies, creating new competitive dynamics and driving innovation in areas such as autonomous farming systems and precision application technologies.

Innovation and Integration Drive Market Success

Success in the European smart farming market increasingly depends on companies' ability to develop integrated solutions that address the complete farming lifecycle while ensuring data security and interoperability. Market leaders are focusing on developing user-friendly interfaces and providing comprehensive training and support services to overcome adoption barriers. Companies are also investing in building strong relationships with agricultural cooperatives and farming communities to enhance their market penetration and establish brand loyalty. The ability to provide localized solutions while leveraging global technological capabilities has become a crucial differentiator for market success.

For new entrants and smaller players, success lies in identifying and serving underserved market segments or developing specialized solutions for specific farming applications. The market presents opportunities for companies that can effectively address farmers' concerns regarding data privacy, system complexity, and return on investment. Regulatory support for sustainable farming practices and an increasing focus on food security create opportunities for companies offering solutions that enhance farming efficiency while reducing environmental impact. The relatively low bargaining power of buyers and moderate threat of substitutes provide established players with pricing power, while creating entry barriers for new competitors through high initial investment requirements and the need for specialized expertise.

Europe Precision Farming Market Leaders

-

John Deere

-

Bayer

-

AGCO Corporation

-

CLAAS KGaA mbH (365FarmNet)

-

Corteva (Granular Inc.)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Precision Farming Market News

- April 2024: AGCO Corporation has established a joint venture with Trimble, creating a new company named PTx Trimble. Trimble's established presence in multiple European countries brings significant experience and market reach to this collaboration, enhancing efforts to promote precision farming technologies across the region.

- December 2023: NIK, a Bulgarian precision farming technology company, has collaborated with Bayer to introduce the FieldView Spray Kit. This new tool aims to enhance farming operations by optimizing processes, reducing expenses, and improving sustainability. The kit achieves these goals through real-time monitoring capabilities, precise calibration features, and advanced data analytics.

- April 2023: AGCO Corporation partnered with Bosch BASF Smart Farming to introduce and promote Smart Spraying technology on Fendt Rogator sprayers. The collaboration also involves joint efforts to develop new innovative features.

Europe Precision Farming Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Government Support and Subsidies

- 4.2.2 Technological Advancements

- 4.2.3 Increasing Demand for Sustainable Agriculture

-

4.3 Market Restraints

- 4.3.1 Regulatory and Standardization Challenges

- 4.3.2 High Initial Cost

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power Of Suppliers

- 4.4.2 Bargaining Power Of Buyers

- 4.4.3 Threat Of New Entrants

- 4.4.4 Threat Of Substitute Products And Services

- 4.4.5 Degree Of Competition

5. MARKET SEGMENTATION

-

5.1 Technology

- 5.1.1 Guidance System

- 5.1.1.1 Global Positioning System (GPS)/ Global Satellite Navigation System (GNSS)

- 5.1.1.2 Global Information System (GIS)

- 5.1.2 Remote Sensing

- 5.1.3 Variable Rate Technology

- 5.1.3.1 Variable Rate Fertilizer

- 5.1.3.2 Variable Rate Seeding

- 5.1.3.3 Variable Rate Pesticide

- 5.1.4 Drones and UAVs

- 5.1.5 Other Technologies

-

5.2 Components

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

-

5.3 Application

- 5.3.1 Yield Monitoring

- 5.3.2 Variable Rate Application

- 5.3.3 Field Mapping

- 5.3.4 Soil Monitoring

- 5.3.5 Crop Scouting

- 5.3.6 Other Application

-

5.4 Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 United Kingdom

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 AGCO Corporation

- 6.3.2 TopCon Corporation

- 6.3.3 Corteva (Granular Inc.)

- 6.3.4 CNH Industrial N.V. (Raven)

- 6.3.5 Deere & Company

- 6.3.6 Teejet Technologies

- 6.3.7 CLAAS KGaA mbH (365FarmNet)

- 6.3.8 AG Leader Technology Inc.

- 6.3.9 Pottinger Landtechnik Gmbh group (MaterMacc)

- 6.3.10 Bayer Cropscience AG

- 6.3.11

- 6.3.12

- 6.3.13

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Precision Farming Industry Segmentation

Precision farming is the adoption of a highly precise set of practices that uses technology to cater to the needs of individual plots and crops. It is a farming management concept based on observing, measuring, and responding to inter and intra-field variability in crops.

The market is segmented by Technology(Guidance systems, Remote sensing, Variable Rate Technology, Drones and UAVs, and Other technologies), Components(Hardware, Software, and Services), Application(Yield monitoring, Variable Rate Application, Field Mapping, Soil Monitoring, Crop Scouting, Other Application), and Geography (Germany, United Kingdom, Italy, France, and the Rest of Europe). The market size and estimation will be provided in terms of value (USD) for the above-mentioned segments.

| Technology | Guidance System | Global Positioning System (GPS)/ Global Satellite Navigation System (GNSS) | |

| Global Information System (GIS) | |||

| Remote Sensing | |||

| Variable Rate Technology | Variable Rate Fertilizer | ||

| Variable Rate Seeding | |||

| Variable Rate Pesticide | |||

| Drones and UAVs | |||

| Other Technologies | |||

| Components | Hardware | ||

| Software | |||

| Services | |||

| Application | Yield Monitoring | ||

| Variable Rate Application | |||

| Field Mapping | |||

| Soil Monitoring | |||

| Crop Scouting | |||

| Other Application | |||

| Geography | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

Need A Different Region or Segment?

Customize Now

Europe Precision Farming Market Research Faqs

How big is the Europe Precision Farming Market?

The Europe Precision Farming Market size is expected to reach USD 3.99 billion in 2025 and grow at a CAGR of 15.30% to reach USD 8.13 billion by 2030.

What is the current Europe Precision Farming Market size?

In 2025, the Europe Precision Farming Market size is expected to reach USD 3.99 billion.

Who are the key players in Europe Precision Farming Market?

John Deere, Bayer, AGCO Corporation, CLAAS KGaA mbH (365FarmNet) and Corteva (Granular Inc.) are the major companies operating in the Europe Precision Farming Market.

What years does this Europe Precision Farming Market cover, and what was the market size in 2024?

In 2024, the Europe Precision Farming Market size was estimated at USD 3.38 billion. The report covers the Europe Precision Farming Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Precision Farming Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Precision Farming Market Research

Mordor Intelligence provides a comprehensive analysis of the precision farming industry. We leverage extensive expertise in agricultural technology and digital agriculture research. Our detailed examination covers emerging trends in smart farming, agricultural robotics, and agricultural IoT applications across Europe. The report offers in-depth insights into the usage of agricultural drones, smart irrigation systems, and controlled environment agriculture. It is available in an easy-to-read report PDF format for download.

Our analysis includes agricultural mapping techniques, agricultural GPS implementations, and the deployment of advanced agricultural sensors. The report provides stakeholders with valuable insights into precision agriculture developments. It includes information on crop monitoring systems, soil monitoring technologies, and yield monitoring solutions. We thoroughly examine trends in farm automation, agricultural data analytics, and variable rate technology applications.

The research also covers innovations in digital farming, smart agriculture practices, and satellite farming methodologies. Additionally, it evaluates the implementation of farm management software. This comprehensive analysis enables agricultural businesses, technology providers, and investors to make informed decisions. They can rely on detailed AgTech market intelligence and industry forecasts.