Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

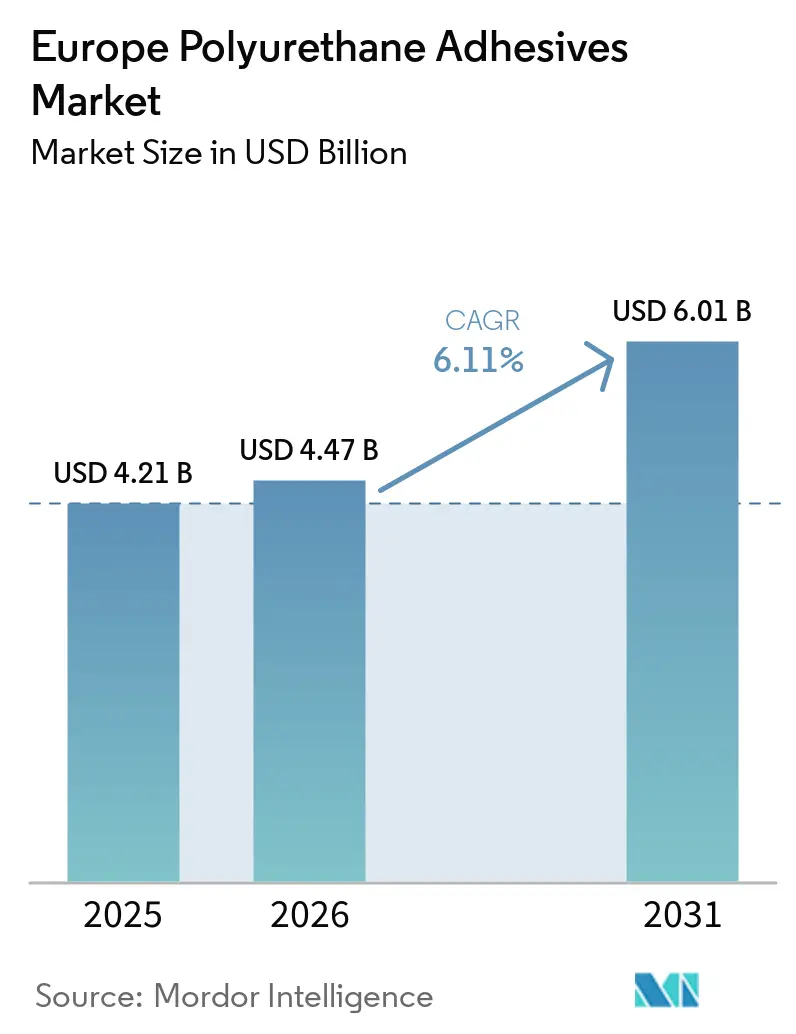

| Base Year Market Size (2025) | USD 4.21 Billion |

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polyurethane Adhesives Market Analysis by Mordor Intelligence

The Europe Polyurethane Adhesives Market size was valued at USD 4.21 billion in 2025 and is estimated to grow from USD 4.47 billion in 2026 to reach USD 6.01 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). Ongoing regulatory pressure to cut volatile organic compounds, surging structural bonding demand in electric-vehicle battery packs, and renovation subsidies under the Energy Performance of Buildings Directive are driving a fundamental shift toward solvent-free and ultra-low monomer reactive formulations. Suppliers are racing to scale water-borne dispersions and alpha-silane-terminated hybrids that align with the European Green Deal’s digital product passport requirements, even as elevated diisocyanate price volatility compresses margins. Competition centers on technical differentiation rather than sheer scale, with Henkel’s January 2026 purchase of Advanced Technical Products underscoring a pivot toward niche ISO 10993-certified grades for medical devices.

Key Report Takeaways

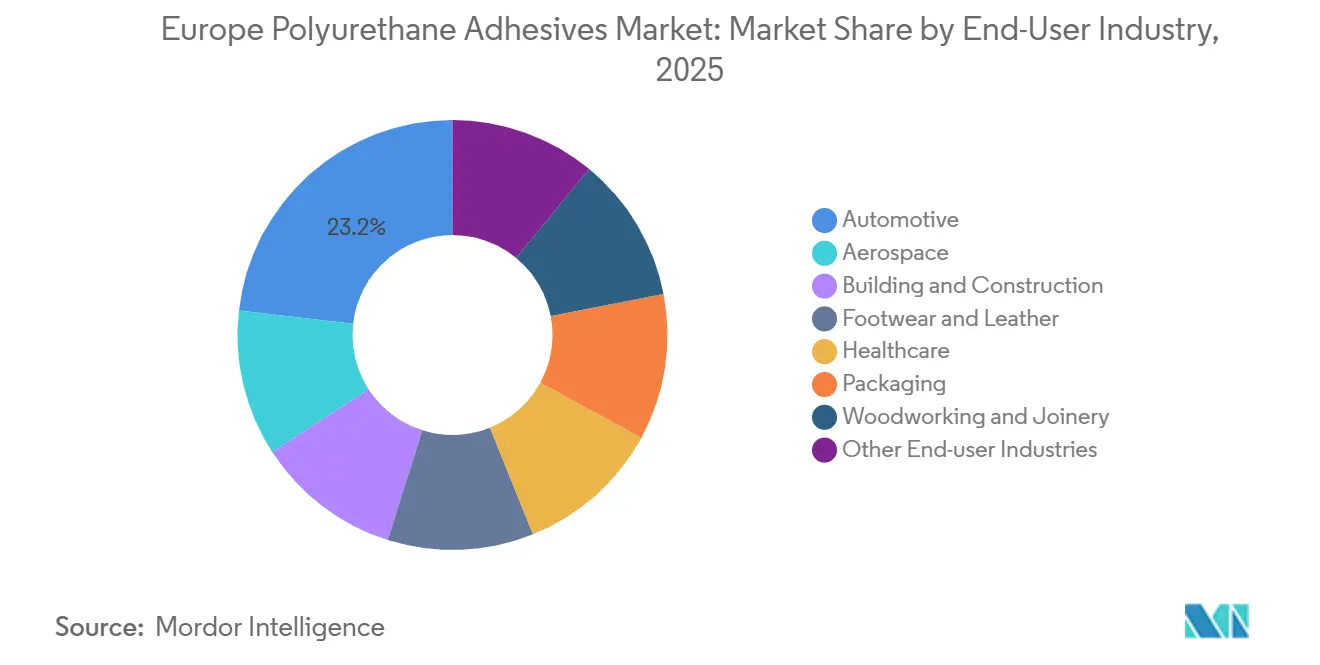

- By end-user industry, automotive applications led with 23.18% of the Europe Polyurethane Adhesives market size in 2025, and electrical and electronics registered the quickest expansion at 6.58% CAGR between 2026 and 2031.

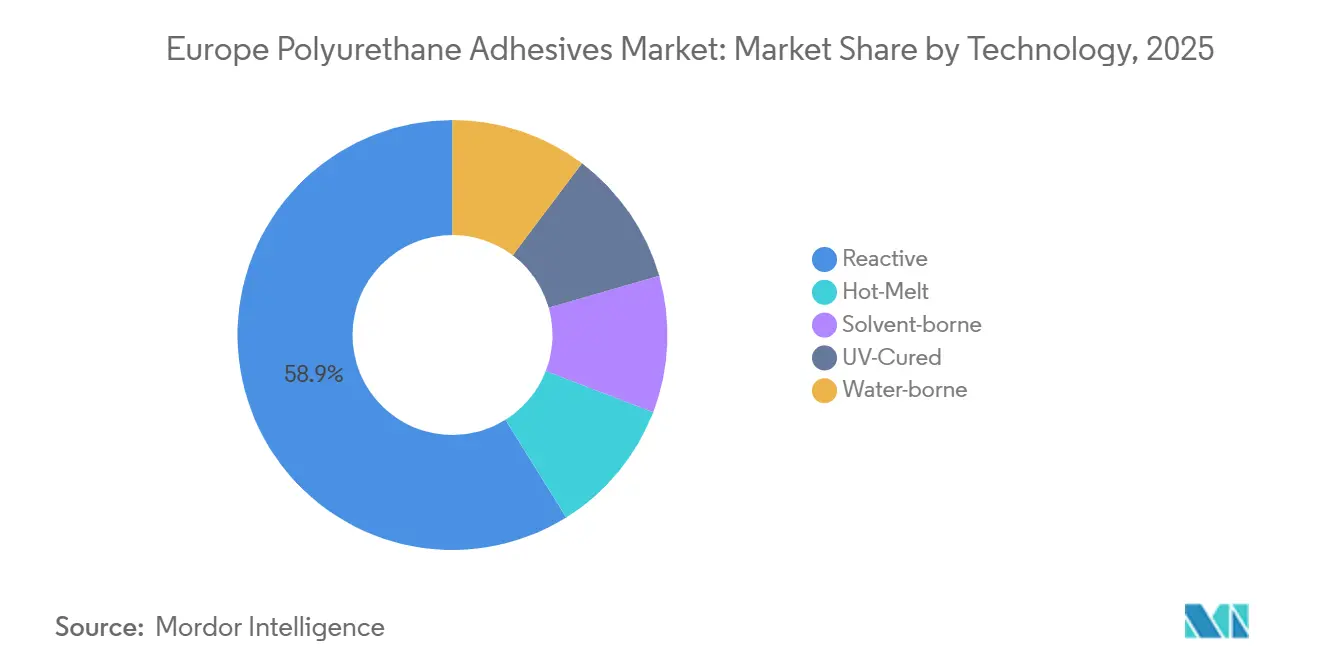

- By technology, reactive polyurethane systems held 58.87% of the European Polyurethane Adhesives market share in 2025, and are projected to advance at an 6.47% CAGR between 2026 and 2031.

- By geography, Germany commanded 23.12% of the Europe Polyurethane Adhesives market in 2025 and is set to post the fastest 6.35% annual growth rate between 2026 and 2031, supported by its integrated automotive supply chain and retrofit subsidies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Polyurethane Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting and structural bonding boom | +1.80% | Germany, France, Spain, Italy, Central Europe | Medium term (2-4 years) |

| Energy-efficient building insulation mandates | +1.50% | Germany, France, the Nordic countries, Benelux | Long term (≥ 4 years) |

| EU Green Deal push for low- volatile organic compound (VOC), solvent-free systems | +1.20% | EU-wide, strongest in Germany, the Netherlands, Nordic countries | Short term (≤ 2 years) |

| Modular timber construction adoption | +0.90% | Nordic countries, Germany, Austria, Switzerland, the UK, and France | Medium term (2-4 years) |

| Reactive polyurethanes in European medical-device assembly | +0.70% | Germany, Switzerland, Ireland, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting and Structural Bonding Boom

Europe has seen significant growth in battery electric vehicle (BEV) production, with a notable increase compared to the previous year. Each BEV now uses significantly more structural adhesive than internal-combustion vehicles. As gigafactories in Germany, France, and Spain expand their output, the demand for reactive polyurethane in traction-battery bonding is expected to grow at a faster pace than overall automotive production in the coming years. Electric-vehicle battery pack assembly increasingly relies on advanced polyurethane systems. These systems provide structural strength and thermal conductivity while replacing traditional mechanical fasteners, resulting in a notable reduction in pack weight. SikaForce-7888 L30 has gained approval for its effectiveness in aluminum-to-composite joints and is now specified by several major car manufacturers in Germany and France. Additionally, Evonik's ambient-cure potting compounds offer high dielectric strength, addressing both electrical isolation and vibration damping, highlighting the critical role of modern polyurethane systems in the evolving automotive industry.

Energy-Efficient Building Insulation Mandates

The Energy Performance of Buildings Directive mandates zero-emission new constructions and requires member states to renovate the least energy-efficient portion of non-residential buildings[2]European Commission, “Energy Performance of Buildings Directive,” europa.eu. In façade retrofits, polyurethane adhesives are used to secure rigid foam panels, but these formulations must comply with the EU Decopaint Directive, which limits volatile organic compounds (VOCs). Incentives in Germany have significantly increased demand for insulated façades, driving notable growth in adhesive consumption. Despite being priced higher, Henkel’s solvent-free Pattex PL Premium has gained a significant share of the German DIY market shortly after its launch, highlighting consumers' willingness to invest in low-emission products. Nordic building codes enforce strict U-value requirements, and Finland's adhesive usage per square meter of building envelope exceeds the European average, indicating potential consumption trends for Western Europe.

EU Green Deal Push for Low- Volatile Organic Compound (VOC), Solvent-Free Systems

The introduction of digital product passports requires manufacturers to disclose their products' embodied carbon and volatile organic compound (VOC) emissions. This initiative is driving the industry's transition away from solvent-borne chemistries. Water-borne polyurethane dispersions are growing at a faster pace compared to the overall European polyurethane adhesives market. Covestro's EU Ecolabel Dispercoll U 53 has gained widespread adoption in European footwear lines, contributing to a significant reduction in VOC emissions[1]Source: Covestro, “Dispercoll U,” covestro.com. BASF's expansion in Tarragona is expected to enhance dispersion capacity. Additionally, the company has achieved a meaningful reduction in Scope 1 and 2 emissions by integrating renewable energy. While water-borne systems are linked to longer open times and lower green strength, regulatory trends indicate a declining share for solvent-borne volumes in the market.

Reactive Polyurethanes in European Medical-Device Assembly

Stricter EU Medical Device Regulation requires full ISO 10993 biocompatibility, driving demand for reactive polyurethanes that cure without residual monomer. Henkel’s Loctite AA 3952 bonds polycarbonate housings in insulin pumps and cures in seconds under LED light without generating cytotoxic by-products. Loctite SI 5057, a two-part polyurethane-silicone hybrid, pots electronics in cardiac monitors while avoiding acetic-acid evolution, protecting sensitive circuitry. Germany, Switzerland, Ireland, and the Netherlands host most of Europe’s MedTech manufacturing, and qualification cycles that run 24-30 months create high entry barriers. Volumes remain modest, yet double-digit growth rates and premium pricing ensure outsized profit contribution for suppliers able to meet stringent extractables thresholds.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diisocyanate price and supply volatility | -1.40% | EU-wide, acute in Germany, France, Italy, and Spain | Short term (≤ 2 years) |

| Tightening REACH limits on free NCO content | -0.80% | EU-wide, strictest in Germany, the Netherlands, Nordic countries | Medium term (2-4 years) |

| Bio-based adhesive substitutes are gaining share | -0.60% | Germany, Austria, the Nordic countries, France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Diisocyanate Price and Supply Volatility

Force-majeure outages in Asia and Red Sea shipping delays lifted toluene diisocyanate spot prices by double digits in Q1 2025, raising European converters’ input costs by up to 18% quarter-on-quarter. Contract methylene-diphenyl diisocyanate prices moved in tandem, and Dow passed through broad polymer dispersion hikes in early 2026 to counter feedstock inflation amid geopolitical unrest. Wacker Chemie’s capacity ramp-up of alpha-silane hybrids at Nünchritz provides a hedge against aromatic-isocyanate dependency, but higher unit costs limit adoption to premium uses. Smaller formulators lack the capital to integrate upstream, leaving them exposed to merchant-supply shocks and squeezing working capital when spot prices spike.

Tightening REACH Limits on Free NCO Content

The European Chemicals Agency (ECHA) proposed reducing the free-isocyanate threshold from 0.1% to 0.05% w/w within a specified timeline. This change could necessitate the reformulation of a significant portion of reactive polyurethane grades currently sold across Europe. Achieving levels below 0.05% requires the use of higher-purity feedstocks and scavengers, such as caprolactam, which can increase manufacturing costs and potentially slow cure speeds. Germany has reported a notable rise in occupational-asthma cases linked to isocyanates, reinforcing the public health rationale for stricter regulations. In preparation for these changes, Henkel has invested in continuous reactors for ultra-low monomer prepolymers at its Bopfingen facility. This proactive approach may lead smaller competitors to exit the market or pursue consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Automotive Leads, Electronics Accelerates

The automotive segment accounted for 23.18% of the Europe Polyurethane Adhesives market size in 2025, as battery pack, structural, and interior applications all require reactive systems. The bonding of electric vehicle batteries required a significant amount of adhesive, with Dow’s VORATRON and SikaForce platforms winning most new specifications. Electrical and electronics remain smaller but post the fastest 6.58% CAGR between 2026 and 2031 as power-semiconductor modules benefit from polyurethane potting compounds, which shield them from heat cycling and vibrations. The building and construction sector, responding to the Energy Performance of Buildings Directive (EPBD) recast, represents a significant share of the volume under mandated retrofits. In Europe, footwear manufacturers in Italy and Spain are increasingly adopting water-borne dispersions with low volatile organic compound (VOC) emissions, showing steady annual growth. While healthcare occupies a niche segment, it commands premium margins, especially for ISO 10993-certified grades like Loctite AA 3952, prominently used in insulin pumps. The demand landscape is further diversified by packaging, woodworking, and aerospace sectors, with woodworking expected to see notable consumption of moisture-cure one-component formulations in the coming years.

By Technology: Reactive Systems Dominate, Water-Borne Gains

Reactive polyurethane systems captured 58.87% of the European polyurethane adhesives market share in 2025 and are projected to grow at 6.47% through 2026 to 2031,These materials exhibit exceptional bond strength and thermal stability, making them highly suitable for structural applications. Two-component grades provide varying pot lives, optimizing their use in automated mixing processes for battery packs. One-component moisture-cure products accommodate significant substrate gaps, making them effective for façade panel applications. Water-borne dispersions are experiencing a significant growth, driven by favorable regulatory conditions. Hot-melts achieve rapid cycle times in automotive interiors but experience a reduction in strength at elevated temperatures, limiting their application in under-hood components. Solvent-borne products have seen a decline in demand and are expected to decrease further due to volatile organic compound (VOC) regulations, including levies in certain European countries. Ultraviolet (UV)-cured polyurethane-acrylate hybrids maintain a modest market share but command premium pricing in specialized sectors such as micro-electronics and implantable devices. Wacker’s GENIOSIL STP-E grades address the gap between reactive polyurethane and silane-modified polymers, eliminating the need for organotin catalysts and expanding their applicability in parquet flooring adhesives.

Geography Analysis

Germany led with 23.12% of the Europe Polyurethane Adhesives market in 2025 and is forecast to grow 6.35% annually between 2026 and 2031. Producing millions of vehicles annually, including a significant share of battery electric units, the company also subsidizes deep-energy retrofits through KfW 40 Plus grants. Investments like Henkel's ultra-low monomer reactor and Dow's chlor-alkali asset closure highlight the pressing need for local capacity in the face of fluctuating feedstock supplies. France, buoyed by strong demand for Airbus composites and a surge in timber construction, ranks among the top markets. However, its tax on volatile organic compounds (VOCs) is accelerating a shift towards water-borne and reactive systems. The United Kingdom, Italy, and Spain together account for a notable portion of the regional demand. Notably, Italy's footwear hubs in Veneto and Tuscany are making a significant shift towards dispersions, while Spain's wind-blade plants are opting for two-component structural grades for spar-cap bonding. Nordic countries, holding a considerable market share, have per-capita adhesive usage significantly above the regional average. This heightened consumption is driven by a deep penetration of timber construction and stringent Swan-label requirements. Eastern Europe's growth, largely fueled by automotive component exports, faces challenges due to cold-chain gaps limiting the distribution of two-component products.

Competitive Landscape

The Europe Polyurethane Adhesives Market is moderately consolidated. Strategic focus now shifts to circular-feedstock and tin-free systems that meet Construction Products Regulation digital-passport rules and upcoming REACH free-NCO limits. Wacker’s alpha-silane hybrids and BASF’s bio-polyols from waste cooking oil exemplify pivots toward feedstock diversification and lower carbon intensity.

Europe Polyurethane Adhesives Industry Leaders

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

3M

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Huntsman International LLC has bolstered its Performance Products facility in Hungary, boosting its polyurethane capacity and emphasizing sustainability and innovation. This move is set to invigorate the growth of Europe's polyurethane adhesives market.

- May 2025: Evonik Industries AG transitioned its polyurethane (PU) additive production to green electricity as part of its sustainability strategy. The company aims to reduce scope 1 and 2 emissions by 25% by 2030 and achieve climate neutrality by 2050.

Europe Polyurethane Adhesives Market Report Scope

Polyurethane adhesives are versatile bonding agents formed from polymer resins containing urethane linkages. They provide strong, flexible, and durable bonds across diverse materials such as wood, plastics, metals, glass, and concrete. Resistant to moisture, chemicals, and temperature variations, they are widely used in construction, automotive, packaging, and footwear industries. Their elasticity and toughness make them ideal for applications requiring both strength and adaptability in demanding environments.

The Europe Polyurethane Adhesives Market is segmented by end-user industry, technology, and country. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. By technology, the market is segmented into hot-melt, reactive, solvent-borne, UV-cured, and water-borne. The report also covers the market size and forecasts for the Europe Polyurethane Adhesives Market in 6 countries across Europe. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

Technology

| Hot-Melt |

| Reactive |

| Solvent-borne |

| UV-Cured |

| Water-borne |

Geography

| Germany |

| France |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| NORDIC Countries |

| Rest of Europe |

| End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| Technology | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| UV-Cured | |

| Water-borne | |

| Geography | Germany |

| France | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| NORDIC Countries | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the polyurethane adhesives market.

- Product - All polyurethane adhesive products are considered in the market studied

- Resin - Under the scope of the study, thermoset and thermoplastic based polyurethanes are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms