Europe Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

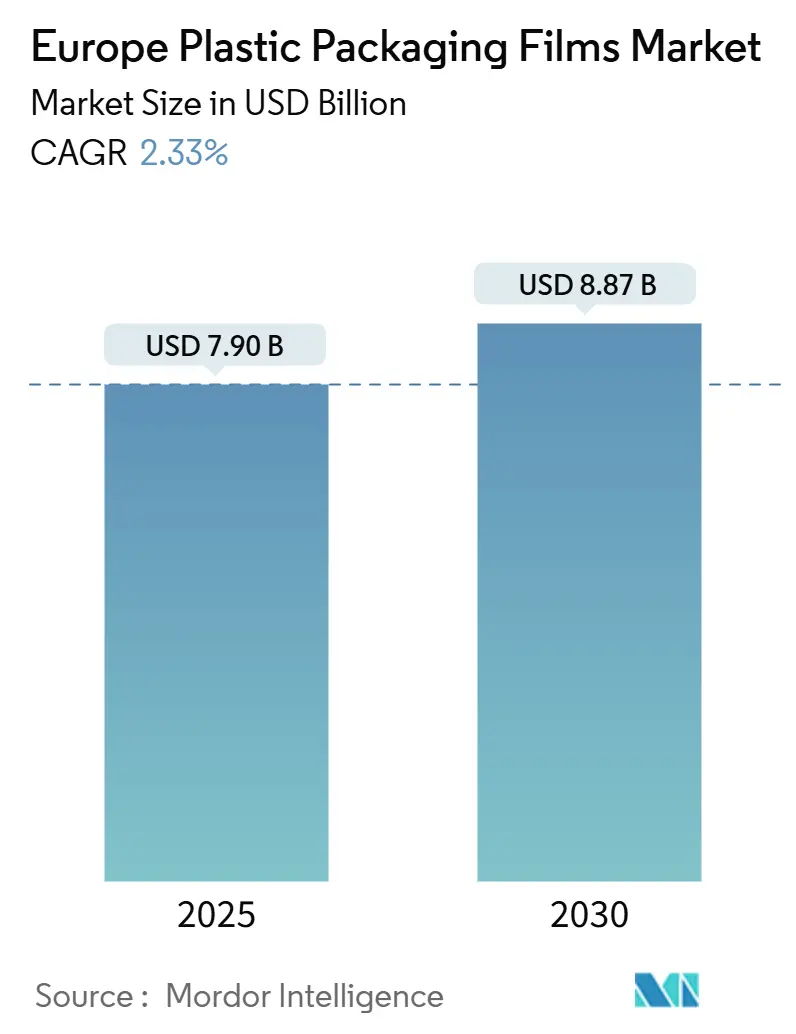

| Market Size (2025) | USD 7.90 Billion |

| Market Size (2030) | USD 8.87 Billion |

| Growth Rate (2025 - 2030) | 2.33% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Plastic Packaging Films Market Analysis by Mordor Intelligence

The Europe plastic packaging films market size stands at USD 7.90 billion in 2025 and is forecast to reach USD 8.87 billion by 2030, registering a 2.33% CAGR. Demand growth stems from regulatory shifts that favor lightweight recyclable constructions, rising adoption of post-consumer recycled (PCR) content and steady expansion of e-commerce and cold-chain logistics. However, higher energy prices and polymer feedstock volatility have tempered margin expansion, prompting converters to accelerate investments in mono-material barrier technologies and in-house recycling capacity. Manufacturers that validate PPWR-compliant film solutions and secure dependable PCR supply chains are poised to capture outsized share of upcoming procurement cycles, especially among multinational brand owners seeking documented sustainability gains.

Key Report Takeaways

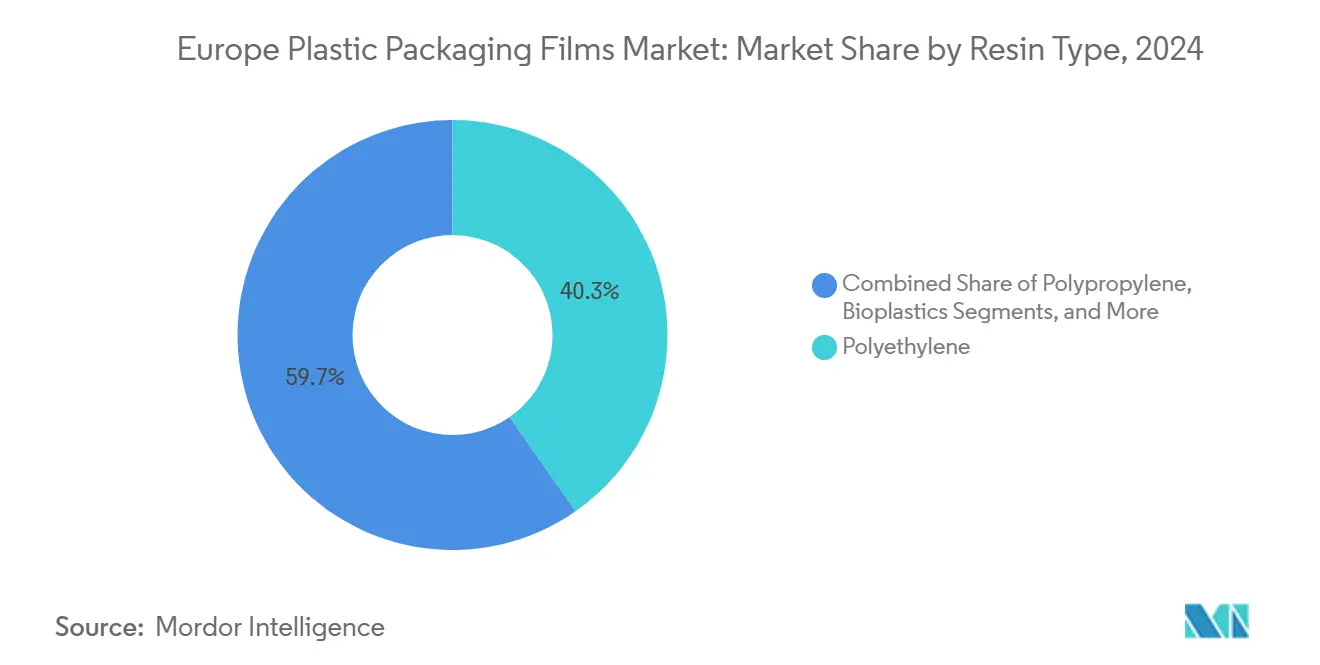

- By resin type, polyethylene commanded 40.31% share of the Europe plastic packaging films market size in 2024, while Bioplastics are on track for a 3.43% CAGR between 2025-2030.

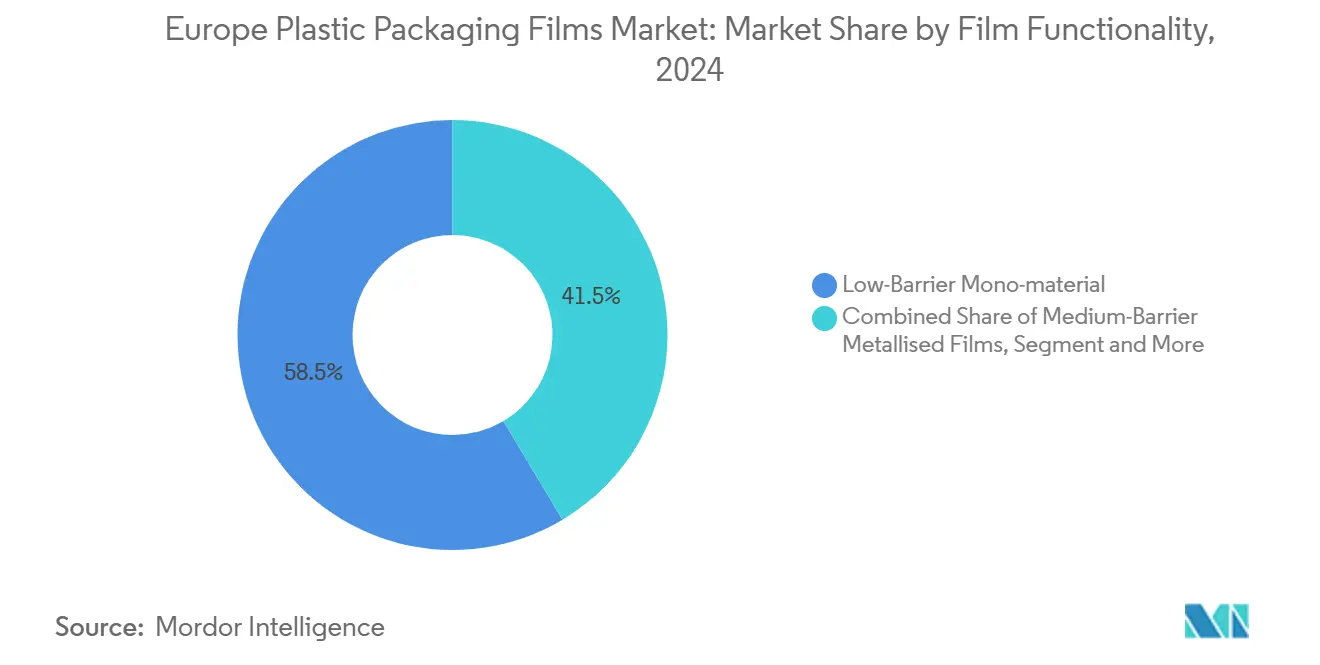

- By film functionality, pouches held 48.54% revenue share in 2024, while wraps and overwraps are advancing at a 3.85% CAGR, whereas low-barrier mono-material films captured 58.54% of functionality share in 2024.

- By end-user industry, food accounted for 32.43% of the Europe plastic packaging films market share in 2024. However, healthcare and pharmaceuticals are set to grow at a 4.33% CAGR through 2030.

- By geography, Germany accounted for 21.32% of the Europe plastic packaging films market share in 2024, while Spain is projected to expand at a 5.64% CAGR through 2030.

Europe Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting and material-efficiency mandates | +0.4% | EU-wide, early adoption in Germany and France | Medium term (2-4 years) |

| Mono-material, recycling-ready film demand | +0.6% | EU-wide, accelerated by PPWR | Short term (≤ 2 years) |

| E-commerce cold-chain and meal-kit deliveries | +0.5% | Germany, France, UK; expanding to Spain and Italy | Short term (≤ 2 years) |

| High-barrier films for food-waste reduction | +0.3% | EU-wide food-producing regions | Medium term (2-4 years) |

| EU-funded PCR capacity scale-up | +0.4% | Germany, France, Netherlands; spillover to Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting and Material-Efficiency Mandates Drive Innovation

Regulators now require minimized packaging mass by 2030, including strict empty-space ratios. Converters therefore pursue ultra-thin films that trim weight 15-20% yet keep oxygen and moisture barriers intact. [1]Anna Eriksson, “PPWR: Redefining Packaging and Its Waste,” Billerud, billerud.com Precision extrusion lines, plasma metallization and nano-coatings underpin this shift. Brand owners that document kilogram reductions per sales unit are prioritizing suppliers able to verify compliance, giving technologically advanced specialty film producers a pivotal edge as the Europe plastic packaging films market evolves.

Surge in Mono-Material, Recycling-Ready Film Specifications

PPWR stipulates that all packaging sold in the bloc be recyclable by 2030 and actually recycled at scale by 2035. Multi-layer PE/PP blends struggle to pass recyclability tests, accelerating R&D into single-polymer barriers that match EVOH or nylon performance. Players first to commercialize printable, heat-resistant mono-PE or mono-PP barrier films are already securing multi-year supply contracts with global food groups racing toward the 2030 compliance deadline.

Boom in E-Commerce Cold-Chain and Meal-Kit Deliveries

Remote grocery shopping generated 941 million plastic delivery bags in the UK during 2024, a figure heading toward 7 billion by 2030. Growth in meal-kit services fuels demand for insulated pouches containing PCR resin that can enter curbside collection streams. Converters delivering light, recyclable ice-gel liners and zip-reclosable pouches capture rising wallet share across Germany, France and the UK as the Europe plastic packaging films market continues scaling with digital-commerce volumes.

High-Barrier Films for Extended Shelf-Life and Food-Waste Cuts

The EU Farm-to-Fork strategy sets ambitious food-waste reduction targets, prompting retailers to favor packaging that extends shelf life. [2]Helena Garcia, “EU Packaging and Packaging Waste Regulation (PPWR) 2025,” Acquis Compliance, acquiscompliance.com EVOH-based multilayers still dominate oxygen-sensitive protein packs, yet recyclability concerns propel investments in coated mono-PE architectures. Emerging active films embed antimicrobial agents or oxygen absorbers, balancing PPWR rules with strict food-safety regulations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taxes on non-recyclable multilayer laminates | -0.3% | EU-wide, varying by member state | Short term (≤ 2 years) |

| Volatile polymer feedstock and energy costs | -0.4% | EU-wide, energy-intensive clusters | Short term (≤ 2 years) |

| Retail bans on hard-to-recycle black films | -0.2% | UK, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter EU Taxes on Non-Recyclable Multilayer Laminates

Extended Producer Responsibility (EPR) fees now escalate steeply when recyclability grades fall below 70%. [3]Andrew Almack, “PPWR 2025: How the EU's Packaging Waste Regulation Is Reshaping Sustainable Packaging,” Plastics For Change, plasticsforchange.org Laminated snack webs incur surcharges that erode margins, forcing converters to retrofit lines toward mono-material output more quickly than originally planned.

Volatile Polymer Feedstock and Energy Costs Squeezing Margins

Polypropylene spot quotes in Northwest Europe jumped EUR 70-100/tonne during February 2025 following Middle-East outages. Concurrent power price spikes amplified cost stress, particularly for extrusion coating plants with limited hedging. Smaller players in the Europe plastic packaging films market with thin balance sheets face the greatest liquidity risk.

Segment Analysis

By Resin Type: Bioplastics Gain Momentum Despite PE Dominance

Polyethylene preserved 40.31% share of the Europe plastic packaging films market in 2024 thanks to its versatility, favorable mechanical profile and established recycling loops. Bioplastics, however, represent the fastest-growing family at a 3.43% CAGR, powered by consumer demand for renewable materials and PPWR recycled-content quotas that encourage bio-based blends. PLA prices advanced sharply across Germany during 2025, reflecting capacity tightness. [4]Emilia Jackson, “Polylactic Acid Prices Surge in Europe amid Sustainability Push,” ChemAnalyst, chemanalyst.com

Investments in PCR-PE extruders proliferate as brand owners require 10% food-contact recycled content by 2030. Polypropylene’s mid-density form offers seal-integrity advantages for retort pouches but faces margin squeeze from feedstock price uncertainty. Specialty copolyesters and PVdC substitutes gain uptake in premium applications where odor or UV barriers matter. The Europe plastic packaging films market size for eco-designed bioplastic blends is projected to touch USD 0.41 billion by 2030, signaling a clear trajectory toward renewable inputs while retaining performance parity.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Format: E-Commerce Drives Pouch Innovation

Pouches delivered 48.54% of 2024 revenue thanks to their lightweight profile and growing role as a default ship-ready format for dry groceries and pet food. Wraps and overwraps are projected to post the fastest 3.85% CAGR, propelled by fresh-produce flow-wrap lines and pallet-unitization films optimized for downgauging. Eco Flexibles’ December 2024 installation of a second Swiss KS-SUP-400-D pouch system illustrates how converters are scaling recyclable mono-PE stand-ups that meet top-load tests while entering established PE recycling streams.

Transport shrink films see moderate gains as regulators push for reusable totes in closed loops, trimming primary demand yet opening refurbishment niches. The Europe plastic packaging films market size allocated to digitally printed pouches surged after inkjet systems like Fujifilm FP790 enabled variable designs without solvent VOCs, aligning with corporate net-zero targets.

By Film Functionality: Mono-Material Solutions Lead Transition

Low-barrier mono-material constructions captured 58.54% share in 2024 and remain the compliance standard for dry goods, tissues and secondary wraps. High-barrier multilayer films, though constrained by recyclability debate, are still projected for a 4.12% CAGR because meat, cheese and pharma blister packs cannot compromise on oxygen ingress limits. Metallized PP structures lose ground to aluminum-free coatings that provide similar water vapor resistance while entering mechanical recycling.

Research initiatives under CEFLEX demonstrate PE-based films achieving <1 cc/m²/day OTR through proprietary EVOH-free blends, narrowing the performance gap without layering dissimilar polymers. Hence, the Europe plastic packaging films industry is witnessing rapid technology crossover between food and medical sub-segments, with active films containing antimicrobial herbs and fungi-based agents gaining traction in hospital nutrition packs.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Accelerates Amid Food Dominance

Food filled 32.43% of demand in 2024, anchored by chilled meat, dairy and baked goods. Yet healthcare is slated for the fastest 4.33% CAGR to 2030, lifted by aging demographics and stricter sterility norms in drug distribution. Amcor’s 2025 blister-pack guide underscores rising calls for ethylene-oxide-sterilizable films that also satisfy PPWR recyclability bands.

Beverage sleeves and labels convert to thinner BOPE or BOPP shrink films compatible with bottle recycling. Personal-care pouches face substitution from refillable rigid packs, nudging converters toward recycle-ready sachets with high tear resistance. Industrial segments advance steadily as manufacturers recognize lightweight film hoods reduce freight emissions and deliver measurable Scope 3 gains. Collectively, end-use diversity cushions the Europe plastic packaging films market against cyclical swings in any single vertical.

Geography Analysis

Germany maintained a dominant 21.32% slice of the Europe plastic packaging films market in 2024, reflecting an unparalleled manufacturing base and early adoption of circular-economy guidelines. Local suppliers leverage proximity to automotive and engineering customers that demand industrial wraps capable of recycled-content disclosure. Federal grants covering 40% of line-retrofit costs for recyclate integration have accelerated domestic output of PCR-rich films.

Spain is emerging as the region’s growth engine, projected for a 5.64% CAGR through 2030. Fresh-produce exports, vibrant tourism and resurgent confectionery manufacturing are spurring conversions from rigid PET to lightweight flow-wraps that cut shipping costs while satisfying retailer carbon labeling rules. Record-high packaging industry turnover in 2024 funded multiple pouch and shrink-film line expansions across Valencia and Catalonia.

France and Italy remain sizable due to premium charcuterie, wine and luxury cosmetics that require elegant yet recyclable flexible solutions. Recent tax credits for bio-based content manufacture have catalyzed pilot trials of compostable cellulose-based flow wraps, though industrial scale remains limited. The UK post-Brexit scenario presents dual compliance tracks: domestic legislation borrows heavily from PPWR, yet divergence in labeling rules adds complexity for cross-channel suppliers. Nonetheless, capital deployments such as Eco Flexibles’ digital press installations attest to continued innovation momentum.

Rest-of-Europe markets in the Baltics, Balkans and Eastern bloc now align swiftly with EU directives, using cohesion-fund grants to erect high-performance recycling facilities. This infrastructure foundation is essential to keep pace with escalating PCR-content targets and supports broader volume growth across the Europe plastic packaging films market.

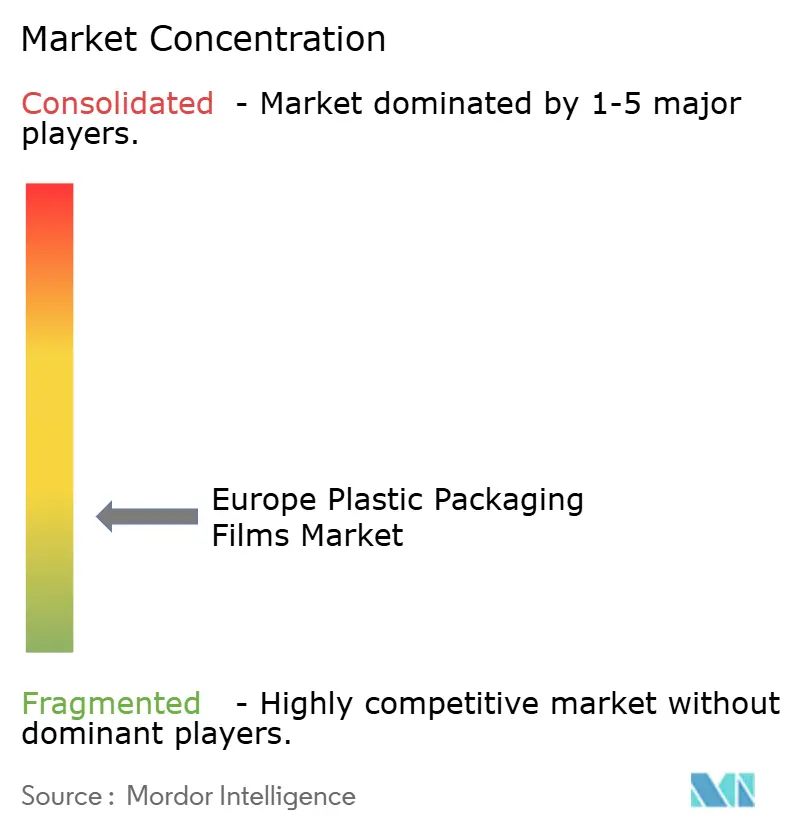

Competitive Landscape

Market concentration is fragmented. Mondi and Amcor collectively hold a sizeable share thanks to continent-wide plant footprints, in-house resin compounding, and proprietary coating formulations. These leaders are channeling capex into closed-loop programs-Mondi’s Germany-based recycling hub now converts 40 kt/yr of PCR LDPE pellets for brand-new “RetortPouch Recyclable” lines, while Amcor’s UK innovation center focuses on mono-PET medical films.

Second-tier groups such as Constantia Flexibles, Huhtamaki, and Schur Flexibles pursue niche specializations-aluminum-free coffee webs, high-clarity retortable pouches, and thin-gauge shrink hooders, respectively. Patent filings show a spike in nanoscale silica barrier layers and compatibilizer chemistries that allow EVOH-containing waste to enter PE recycling flows.

M&A activity remains lively. Fedrigoni’s March 2025 minority stake in Papkot accelerates fiber-based substitute development for single-use sachets. DS Smith’s EUR 34.4 million (USD 40.36 million) Hungarian upgrade diversifies production into flexibles alongside corrugated, illustrating convergence between segments. Smaller converters lacking scale for PCR upgrades risk consolidation or niche repositioning.

Long-term competitiveness hinges on PCR supply contracts, design-for-recycling credentials and the capacity to validate film performance at 25-30 microns without compromising machinability. Firms meeting those benchmarks are positioned to deepen partnerships with Carrefour, Tesco and Aldi as retailer scorecards tighten under PPWR.

Europe Plastic Packaging Films Industry Leaders

-

Taghleef Industries LLC

-

Innovia Films Ltd (CCL Industries Inc.)

-

Jindal Films Europe Virton S.A.

-

Mondi plc

-

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: JYSK optimized curtain packs, cutting 78 tonnes of plastic per year across European stores.

- March 2025: Fedrigoni bought a minority share in start-up Papkot to hasten fiber-based flexible substitution.

- March 2025: Smurfit Kappa allocated EUR 20 million (USD 21.3 million) to boost converting capacity across its European network, extending support operations for film-based packaging lines.

- February 2025: EU Packaging and Packaging Waste Regulation formally entered into force, setting binding recyclability thresholds and PCR quotas.

Europe Plastic Packaging Films Market Report Scope

Plastic films are versatile, serving to wrap products, overwrap various packaging types (from individual packs to palletized loads), create sachets, bags, and pouches, and are often part of laminates, where they are combined with other plastics and materials for packaging. The report also delves into the demand for these converted packaging films, analyzing them across essential resin and application categories. This broad scope mirrors the diverse needs of the market and the shifting preferences of consumers and businesses.

The European plastic packaging films market is segmented by type (polypropylene {biaxially oriented polypropylene [BOPP] and cast polypropylene [CPP]}, polyethylene {low-density polyethylene [LDPE] and linear low-density polyethylene [LLDPE]}, polyethylene terephthalate {biaxially oriented polyethylene terephthalate [BOPET]}, polystyrene, bio-based, and PVC, EVOH, PETG, and other film types), end-user industry (food [candy and confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products [seasonings and spices, spreadables, sauces, condiments, etc. ]), healthcare, personal care and home care, industrial packaging, and other end-user industries), and country (France, Germany, Italy, United Kingdom, Spain, Poland, Nordic, and Rest of Europe). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene-terephthalate (BOPET) |

| Polystyrene (OPS) |

| Bioplastics |

| Other Material Types |

| Wraps and Overwraps |

| Bags and Linings |

| Pouches |

| Other Packging Formats |

| Low-Barrier Mono-material Films |

| Medium-Barrier Metallised Films |

| High-Barrier Multilayer Films |

| Specialty Active and Antimicrobial Films |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Food Products | |

| Beverages | |

| Healthcare and Pharmaceutical | |

| Personal Care and Home Care | |

| Industrial Packaging | |

| Other End-use Industries |

| France |

| Germany |

| Italy |

| United Kingdom |

| Spain |

| Rest of Europe |

| By Resin Type | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polyethylene-terephthalate (BOPET) | ||

| Polystyrene (OPS) | ||

| Bioplastics | ||

| Other Material Types | ||

| By Packaging Format | Wraps and Overwraps | |

| Bags and Linings | ||

| Pouches | ||

| Other Packging Formats | ||

| By Film Functionality | Low-Barrier Mono-material Films | |

| Medium-Barrier Metallised Films | ||

| High-Barrier Multilayer Films | ||

| Specialty Active and Antimicrobial Films | ||

| By End-use Industry | Food | Candy and Confectionery |

| Frozen Foods | ||

| Fresh Produce | ||

| Dairy Products | ||

| Meat, Poultry and Seafood | ||

| Pet Food | ||

| Other Food Products | ||

| Beverages | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Home Care | ||

| Industrial Packaging | ||

| Other End-use Industries | ||

| By Country | France | |

| Germany | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe plastic packaging films market in 2025?

It is valued at USD 7.90 billion in 2025 with a forecast 2.33% CAGR to 2030.

Which country leads demand for flexible plastic films in Europe?

Germany holds the largest 21.32% share due to its industrial packaging requirements and early adoption of circular-economy practices.

What film functionality segment is growing fastest?

High-barrier multilayer films are advancing at a 4.12% CAGR because they deliver extended shelf life for meat, dairy and pharmaceuticals.

Why are mono-material films gaining popularity?

PPWR requires packaging to be recyclable by 2030, pushing converters toward single-polymer structures that can enter established PE or PP recycling streams.

Which end-use vertical shows the highest growth rate?

Healthcare and pharmaceuticals packaging is projected for a 4.33% CAGR through 2030 as sterile and antimicrobial requirements intensify.

What main risk threatens film producers’ margins?

Volatile polypropylene and LDPE feedstock prices coupled with elevated energy costs can compress margins, especially for smaller converters unable to hedge.

Page last updated on: