Market Size of Europe Plastic Bottles Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

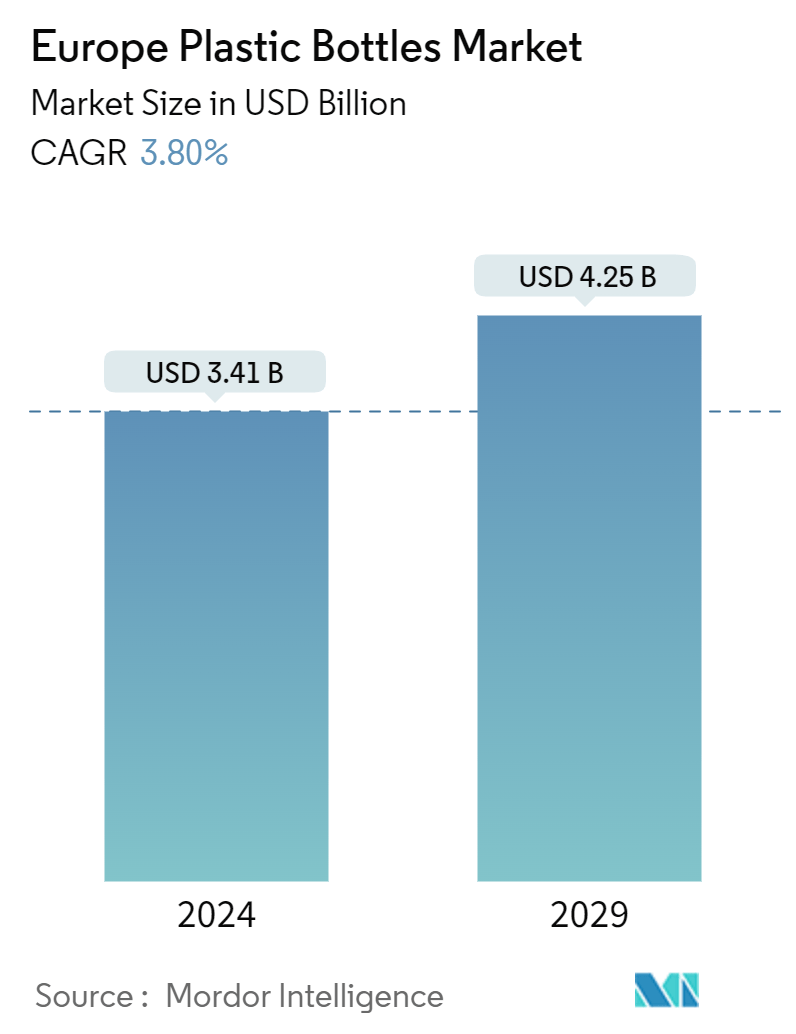

| Market Size (2024) | USD 3.41 Billion |

| Market Size (2029) | USD 4.25 Billion |

| CAGR (2024 - 2029) | 3.80 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe Plastic Bottles Market Analysis

The Europe Plastic Bottles Market size is estimated at USD 3.41 billion in 2024, and is expected to reach USD 4.25 billion by 2029, growing at a CAGR of 3.80% during the forecast period (2024-2029). In terms of production volume, the market is expected to grow from 3.78 million tonnes in 2024 to 4.5 million tonnes by 2029, at a CAGR of 3.55% during the forecast period (2024-2029).

- The plastic bottles market in Europe is characterized by products primarily made from polyethylene terephthalate, polypropylene, and polyethylene. These materials dominate the packaging landscape due to their lightweight and durable nature and cost-effectiveness, making them a preferred choice for manufacturers. Given the global reliance on packaged foods and beverages, these factors set the stage for a significant impact on the European plastic bottles market in the coming years.

- The rising adoption of plastic is closely linked to its lightweight properties. This advantage not only conserves energy during transportation but also curtails emissions. The weight benefit of plastic becomes even more pronounced when compared with heavier alternatives like glass, which demand more transportation trips.

- Among the various materials used to craft plastic bottles, polyethylene terephthalate (PET) is favored for its durability, versatility, and cost-efficiency. As Europe's food, beverage, and pharmaceutical industries expand and innovate, the demand for plastic packaging, especially PET bottles, rises in tandem. Moreover, the industry's trend of introducing new beverages in diverse flavors and packaging styles further bolsters the demand for rigid plastic bottles.

- The beverage segment, particularly, is heavily reliant on plastic bottles, driven by the consistent demand for bottled water and non-alcoholic drinks. Consumers gravitate toward bottled water for its perceived purity, often avoiding potentially contaminated tap water, and they appreciate the convenience and portability it offers.

- Addressing environmental concerns, a study by the European Commission highlighted the prevalence of PET bottles and their lids in ocean debris. In response, the European Council implemented stringent regulations aiming to reduce the use of single-use plastics and set ambitious recycling targets.

- The foundational pillars for material circularity include removal, redesign, reuse, and alternative models. The overarching goal is to minimize material use, eliminate surplus, and incorporate recyclable components. While there is ongoing innovation for alternative packaging solutions, a crucial focus remains on ensuring existing materials can be effectively collected, recycled, and/or refilled, thereby promoting a circular packaging economy.

- One increasingly favored strategy in this endeavor is the rise of deposit return systems (DRS). When effectively designed, Deposit Refund Systems (DRS) can significantly boost collection rates of beverage packaging in the non-alcoholic beverages industry. Thus, the expansion of efficient DRS across Europe becomes paramount, a feat achievable only with backing from the European Commission. This urgency was underscored by a joint press release from UNESDA, in collaboration with Zero Waste Europe and Natural Mineral Waters Europe (NMWE), in October 2021. They urged the European Commission to establish minimum standards for new Deposit Refund Systems (DRS) in the revision of the EU Packaging and Packaging Waste Directive.

- In a testament to this trend, Europe's Brookfield Drinks unveiled a 100% Prevented Ocean Plastic bottle in March 2024. Part of the company’s NEO WTR range, this bottle was set to hit the shelves in 250 Tesco superstores. Brookfield Drinks' initiative is a notable achievement, surpassing major soft drink brands by launching a new spring water range in the industry's first fully recycled ocean-bound plastic bottle, complete with a recyclable cap and label.