Europe Physical Security Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

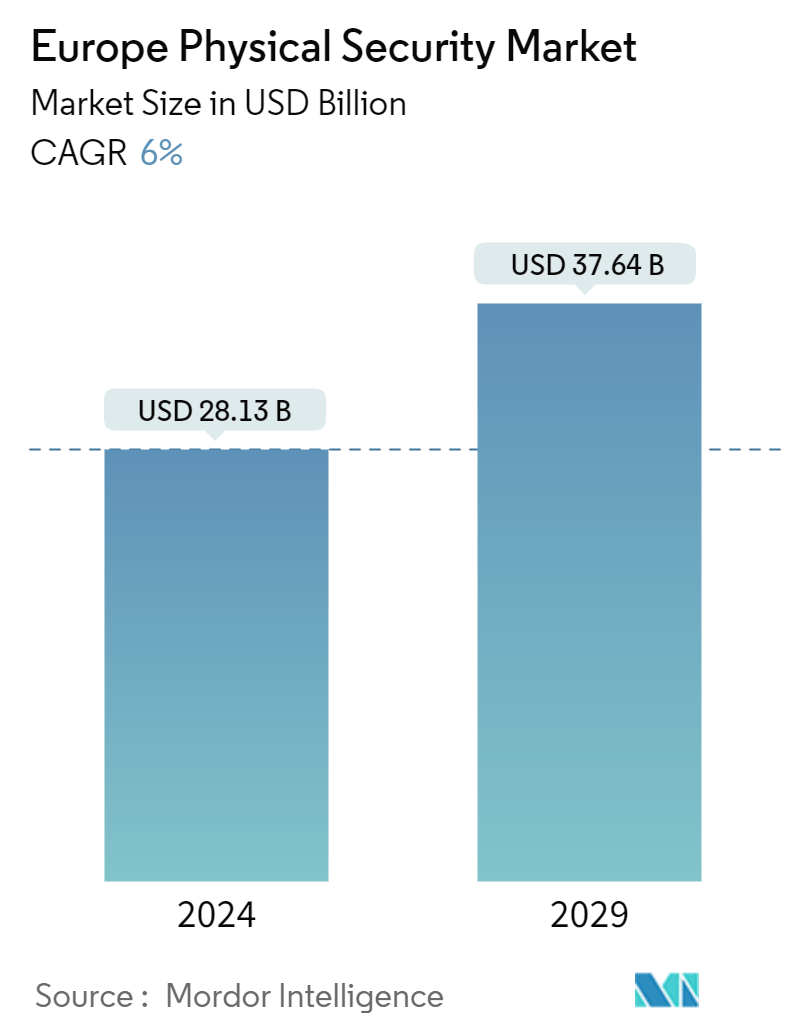

| Market Size (2024) | USD 28.13 Billion |

| Market Size (2029) | USD 37.64 Billion |

| CAGR (2024 - 2029) | 6.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Physical Security Market Analysis

The Europe Physical Security Market size is estimated at USD 28.13 billion in 2024, and is expected to reach USD 37.64 billion by 2029, growing at a CAGR of 6% during the forecast period (2024-2029).

- Physical security encompasses many aspects that must be addressed to guarantee an organization's safety. At its most fundamental, physical security encompasses security measures directly related to safeguarding individuals, assets, and infrastructure. Physical security systems like video surveillance cameras and cloud-based surveillance have significantly contributed to the European market's growth. The market is witnessing an increasing number of security cameras.

- The rapid advancements of artificial intelligence (AI) and machine learning (ML), incorporated into smart building technology in new construction and commercial refurbishment, have resulted in an increasing number of devices utilizing physical security systems. These factors, combined with the ever-evolving nature of cloud storage for many applications, necessitate architecture and technology updates that drive the growth of physical security systems.

- The physical security market's growth is augmented by integrating these systems with Internet of Things (IoT) devices, artificial intelligence, and cloud services. For instance, in August 2023, an artificial intelligence (AI) camera system was installed along a major road in England, United Kingdom, by the police. Within 72 hours, the system had captured nearly 300 drivers in breach of the law. After five days, the number had increased to a total of 1,000. The government is adopting such security measures to avoid accidents and enforce the rules and regulations better. AI-powered cameras have seen a rapid increase in demand and will likely boost the market's growth.

- Implementing advanced video analytics offers a wide range of capabilities, such as iris, fingerprint, facial, license plate recognition, crowd recognition, and tracking and counting people, driving the need for physical security solutions. In Germany, biometrics are being increasingly used in retail and hospitality settings to automate age estimation, payment processes, and more. Such adoption will generate more demand for physical systems across Germany.

- After the COVID-19 pandemic, the European market increased physical security business opportunities, with the potential to purchase more advanced products and systems. The physical security market is experiencing a steady increase in size and the adoption of security devices. Additionally, businesses and public areas have had to keep up with changing health requirements. Therefore, physical security systems now enable compliance with capacity restrictions, mask compliance, and hygiene regulations.

- However, organizations across Europe face significant challenges when implementing surveillance and analytics systems, as they are subject to operational issues, and accuracy is one of the primary barriers to adoption. Furthermore, video surveillance has become a contentious issue in the civil liberties community, as it is seen as a breach of privacy. There is a growing awareness of who is watching the video and the potential for misuse, as individuals anticipate that their data will only be used for legitimate and specified purposes, thus hindering the market's growth.

Europe Physical Security Market Trends

The Biometric System Segment is Expected to Hold a Significant Market Share

- Biometrics are primarily employed in security systems for secure environments susceptible to theft or essential physical security needs. These systems collect immutable data, such as fingerprints, voice, retinal, facial, and hand signals. Biometric solutions provide more security than other authentication methods, such as passwords or access cards. The utilization of biometric systems in physical security is in demand due to technological advancements and their increasing affordability and dependability.

- For instance, in August 2023, the French authorities ordered 544 kiosks and 250 tablets for the collection of face and fingerprint biometric data from ferry car passengers in response to concerns that queues could arise for UK passengers traveling to France when the European Union's EES (Entry/Exit System) system becomes operational. It also stated that the system could increase the time taken to complete border checks, as passengers must be scanned at digital kiosks to verify their travel documents.

- The government of the United Kingdom is continuing to implement secure biometric immigration control systems. In July 2023, the United Kingdom government implemented new penalties for non-compliance with biometric requirements for digital visas. This amendment ensures that the photographs included in the documents are not too advanced so that face biometrics can be accurately matched. Such adoption of Biometrics Systems will boost the demand for physical security across Europe.

- The utilization of biometrics technology is on the rise, with growing demand across various sectors. In particular, facial recognition is becoming increasingly popular for verifying user identity. For instance, in June 2023, the French Senate voted to approve a proposal for a law on the testing of facial recognition in public areas. This law enabled judicial authorities and intelligence agencies to utilize remote biometric identifiers in public places for three years.

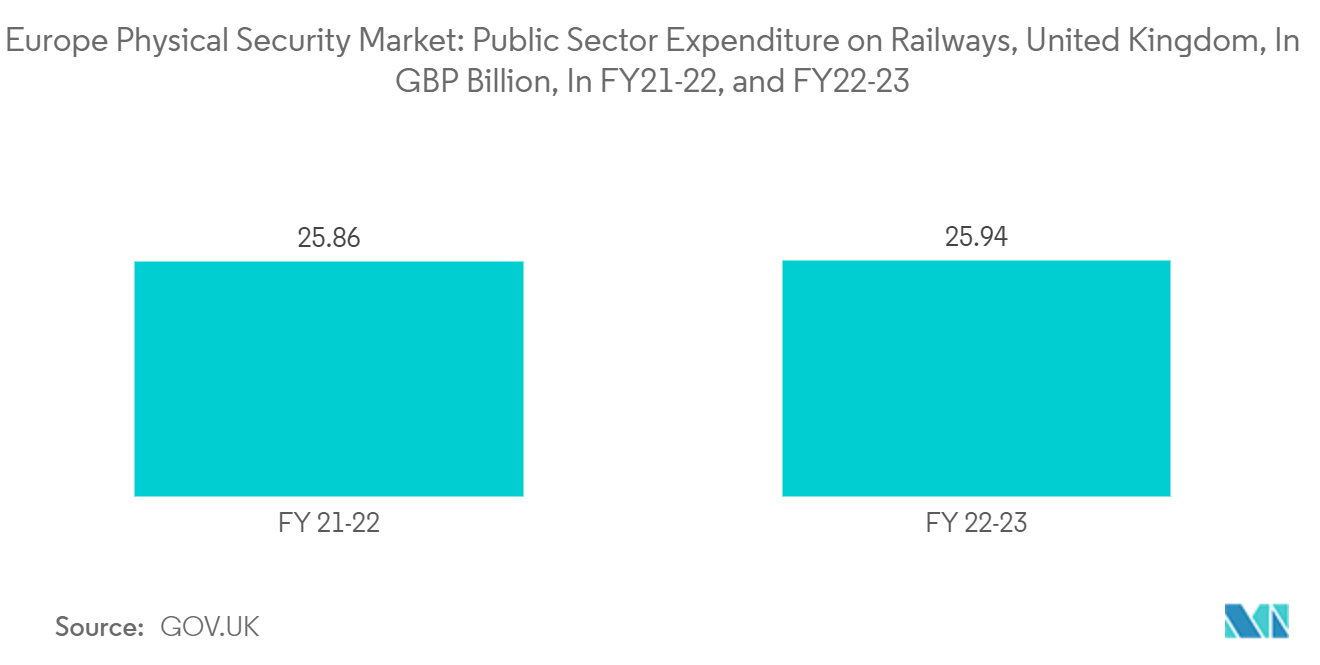

- Biometrics, such as fingerprints and iris recognition, can enhance railway safety by precision verifying the identity of passengers, staff, and contractors. Public expenditure on railways in the United Kingdom amounted to approximately GBP 25.9 billion (USD 31.64 billion) in FY 2022/23, compared to the previous year's GBP 25.8 billion (USD 31.52 billion). Such a rise in railway expenditure will increase the demand for biometrics systems adoption across railway stations in the United Kingdom. Also, it will boost the adoption of other physical security systems in public spaces across Europe.

- In July 2023, Eurostar Group implemented a biometric, contactless check-in system in London St Pancras, the SmartCheck system, which iProov provided. This fast-track service allows Eurostar's Business Premier and Cara Blanche passengers to bypass queues for ticketing and UK exit checks during connections between the United Kingdom and continental Europe.

Germany is Expected to Witness Significant Market Growth

- The demand for physical security systems like video surveillance cameras in Germany is increasing rapidly due to the proliferation of terrorism-related risks in public areas and increasing private sector initiatives to enhance the safety and health of personnel in the workplace. The German government has adopted several measures to strengthen security in the nation, and the implementation of modern surveillance technology has played a prominent role in these efforts.

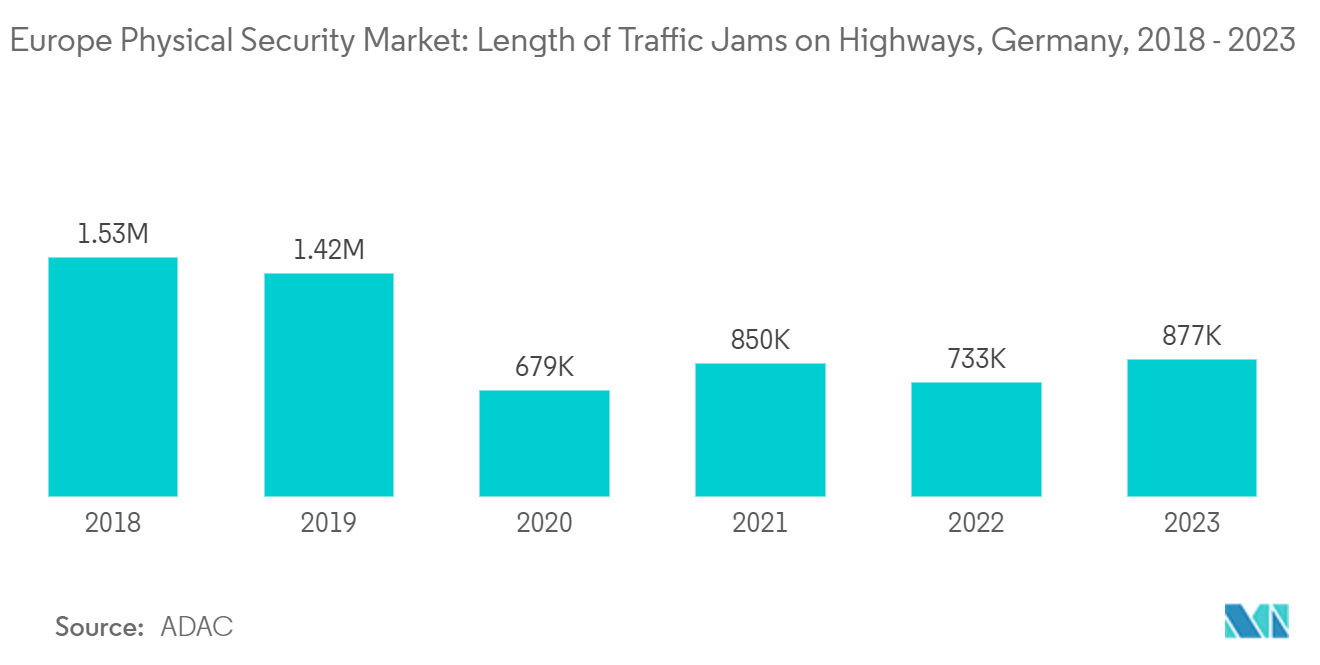

- The increased number of road traffic fatalities has increased the need for installing video surveillance cameras. Video surveillance cameras can monitor and document traffic incidents, allowing for a more comprehensive understanding of the causes and trends of accidents.

- According to the Statistische Bundesamt, there were 2,776 fatalities in Germany in 2022, an increase of 2,562 cases from the previous year. The increasing awareness of safety risks caused by accidents is prompting the need for more effective monitoring and prevention measures, which is leading to an increase in the utilization of video surveillance cameras.

- As technology advances and costs decrease, countries recognize the value of investing in AI surveillance cameras to improve their security and safety protocols. For instance, in April 2023, the Monocam, a video camera equipped with AI, was expected to be deployed in the Rhineland-Palatinate region. It can detect any unusual activity in the car; the recording is stored and transmitted to the relevant law enforcement authorities for investigation. The system was expected to be tested on two highway bridges in the Land of Rhineland Palatinate, Germany.

- Biometrics can improve airport security by accurately identifying staff and passengers, thus reducing the risk of identity theft and unauthorized access. For instance, in April 2022, Hamburg Airport passengers could access security and boarding checkpoints without needing a boarding pass and smartphone. This measure was due to the introduction of the Star Alliance Biometric Face Field Recognition system, which was implemented following a successful trial period. This innovation made Hamburg Airport the fourth airport to benefit from biometric access. Passengers who register for the system can access all participating airports.

Europe Physical Security Industry Overview

The European physical security market is fragemented, owing to the presence of several companies. The players adopt strategies like product innovation, new product launches, partnerships, collaborations, and mergers and acquisitions. Some of the major players include Siemens AG, Securitas AB, Secom Co. Ltd, Dahua Technology Co. Ltd, Hanwha Vision Co. Ltd, G4S Limited, Vanderbilt Industries, Bosch Security Systems GmbH, Teledyne FLIR LLC, Genetec Inc., Johnson Controls, Hangzhou Hikvision Digital Technology Co. Ltd, Schneider Electric, and Honeywell International Inc.

- August 2023: Hanwha Vision partnered with A2 Technology, a company that offers smart city solutions, to provide innovative video solutions. A2 primarily aims to protect communities and improve mobility through artificial intelligence (AI) and video analytics. Its solutions are deployed in more than 100 cities worldwide, with its most renowned solution being installed in 54 Tunnels and 300+ km on high-speed railroads.

- July 2023: Securitas entered into an extended five-year contract to provide security services for Microsoft data centers in 31 countries. The agreement outlined a comprehensive suite of services designed according to Microsoft's requirements. Securitas is dedicated to providing the highest level of security when and where it is required. Innovation and technology integration are vital priorities for Securitas to strike a balance between security measures and innovative solutions.

Europe Physical Security Market Leaders

-

Securitas AB

-

Bosch Security Systems GmbH

-

Dahua Technology Co., Ltd.

-

Hanwha Vision Co., Ltd.

-

Secom Co., Ltd.

*Disclaimer: Major Players sorted in no particular order

Europe Physical Security Market News

- June 2023: Hanwha Vision launched its new bi-spectrum AI camera range, offering visual and thermal imaging capabilities. The thermal lens allows the perimeter to be monitored for suspicious activity, even in dim lighting, inclement weather, or visual obstructions. The lens also provides identification details, identifying suspicious activity, such as an intruder. This expedited detection and identification process reduces the time and cost of installing the device.

- May 2023 - Secom, a security integration company, invested USD 192 million in two cloud video surveillance providers, the Eagle Eye and the Brivo. Eagle Eye offers a comprehensive cloud video surveillance solution, combining cyber security, cloud video, artificial intelligence (AI), and analytics to provide businesses with a more secure and efficient way to monitor their operations. Artificial intelligence (AI) is also utilized for more sophisticated video analytics, including smart video search and smart alarms, which can detect abnormal activity or particular occurrences in video recordings.

Europe Physical Security Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Corporate Risks and Physical Security Threats

5.1.2 Organizations' Access Control Requirements have Grown Due to the Prevalence of Remote and Hybrid Work

5.1.3 The Accelerated Incorporation of Machine Learning (ML) and Artificial Intelligence (AI)

5.2 Market Challenges

5.2.1 The Physical Security Systems Vulnerability to Cyber Attacks

5.2.2 Rapid Technological Progress Necessitates Frequent System Upgrades

6. MARKET SEGMENTATION

6.1 By System Type

6.1.1 Video Surveillance System

6.1.1.1 IP Surveillance

6.1.1.2 Analog Surveillance

6.1.1.3 Hybrid Surveillance

6.1.2 Physical Access Control System (PACS)

6.1.3 Biometric System

6.1.4 Perimeter Security

6.1.5 Intrusion Detection

6.2 By Service Type

6.2.1 Access Control as a Service (ACaaS)

6.2.2 Video Surveillance as a Service (VSaaS)

6.3 By Type of Deployment

6.3.1 On-Premises

6.3.2 Cloud

6.4 By Organization Size

6.4.1 SMEs

6.4.2 Large Enterprises

6.5 By End-user Industry

6.5.1 Government Services

6.5.2 Banking and Financial Services

6.5.3 IT and Telecommunications

6.5.4 Transportation and Logistics

6.5.5 Retail

6.5.6 Healthcare

6.5.7 Residential

6.5.8 Other End-user Industries

6.6 By Country***

6.6.1 United Kingdom

6.6.2 Germany

6.6.3 France

6.6.4 Spain

6.6.5 Italy

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Securitas AB

7.1.2 Bosch Security Systems GmbH

7.1.3 Secom Co. Ltd

7.1.4 Dahua Technology Co. Ltd

7.1.5 Hanwha Vision Co. Ltd

7.1.6 G4S Limited

7.1.7 Vanderbilt Industries

7.1.8 Siemens AG

7.1.9 Teledyne FLIR LLC

7.1.10 Genetec Inc.

7.1.11 Johnson Controls

7.1.12 Hangzhou Hikvision Digital Technology Co. Ltd

7.1.13 Schneider Electric SE

7.1.14 Honeywell International Inc.

7.1.15 Axis Communications AB

7.1.16 NEC Corporation

7.1.17 HID Global Corporation

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Europe Physical Security Industry Segmentation

Physical security refers to preventing unauthorized intruders from accessing controlled facilities. Physical security technologies have developed significantly recently, offering advanced protection at competitive prices. Physical security devices utilize cloud technology and AI for even more sophisticated real-time data processing. Various automated physical security components can perform multiple functions in a physical security system.

The European physical security market is segmented by system type (video surveillance system [IP surveillance, analog surveillance, and hybrid surveillance], physical access control system (PACS), biometric system, perimeter security, and intrusion detection), service type (Access Control-as-a-Service (ACaaS) and Video Surveillance-as-a-Service (VSaaS)), type of deployment (on-premises and cloud), organization size (SMEs and large enterprises), end-user industry (government services, banking and financial services, IT and telecommunications, transportation and logistics, retail, healthcare, residential, and other end-user industries), and country (the United Kingdom, Germany, France, and Rest of Europe). The report offers the market sizes and forecasts for all the above segments in terms of value (USD).

| By System Type | |||||

| |||||

| Physical Access Control System (PACS) | |||||

| Biometric System | |||||

| Perimeter Security | |||||

| Intrusion Detection |

| By Service Type | |

| Access Control as a Service (ACaaS) | |

| Video Surveillance as a Service (VSaaS) |

| By Type of Deployment | |

| On-Premises | |

| Cloud |

| By Organization Size | |

| SMEs | |

| Large Enterprises |

| By End-user Industry | |

| Government Services | |

| Banking and Financial Services | |

| IT and Telecommunications | |

| Transportation and Logistics | |

| Retail | |

| Healthcare | |

| Residential | |

| Other End-user Industries |

| By Country*** | |

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Italy |

Europe Physical Security Market Research FAQs

How big is the Europe Physical Security Market?

The Europe Physical Security Market size is expected to reach USD 28.13 billion in 2024 and grow at a CAGR of 6% to reach USD 37.64 billion by 2029.

What is the current Europe Physical Security Market size?

In 2024, the Europe Physical Security Market size is expected to reach USD 28.13 billion.

Who are the key players in Europe Physical Security Market?

Securitas AB, Bosch Security Systems GmbH, Dahua Technology Co., Ltd., Hanwha Vision Co., Ltd. and Secom Co., Ltd. are the major companies operating in the Europe Physical Security Market.

What years does this Europe Physical Security Market cover, and what was the market size in 2023?

In 2023, the Europe Physical Security Market size was estimated at USD 26.44 billion. The report covers the Europe Physical Security Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Europe Physical Security Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe Physical Security Industry Report

Statistics for the 2024 Europe Physical Security market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe Physical Security analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Europe Physical Security Market Report Snapshots