Europe Pharmaceutical Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

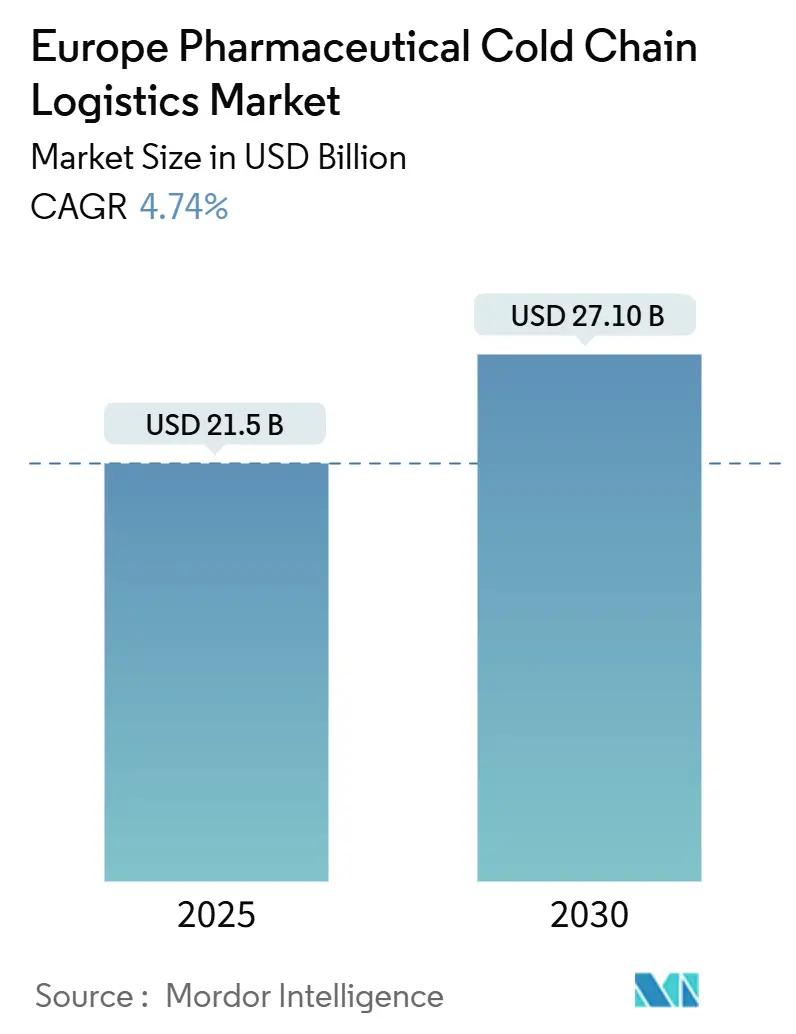

| Market Size (2025) | USD 21.5 Billion |

| Market Size (2030) | USD 27.10 Billion |

| Growth Rate (2025 - 2030) | 4.74% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Pharmaceutical Cold Chain Logistics Market Analysis by Mordor Intelligence

The Europe Pharmaceutical Cold Chain Logistics Market size is estimated at USD 21.5 billion in 2025, and is expected to reach USD 27.10 billion by 2030, at a CAGR of 4.74% during the forecast period (2025-2030).

Demand for ultra-low-temperature services—particularly below -120 °C for cell and gene therapies—remains the single most influential driver of this expansion, pressing logistics firms to deploy cryogenic freezers, dry-shippers, and redundant power systems that go far beyond conventional 2-8 °C solutions[1]J. Meneghel et al., “Ultra-low shipping temperatures for cell therapies,” Cytotherapy, isct-cytotherapy.org. The Europe pharmaceutical cold chain logistics market continues to benefit from sustained biologics uptake, stricter EU GDP and serialization mandates, and sizable pandemic-preparedness budgets under HERA that add long-term volume to national stockpiles. However, energy-price volatility, driver shortages, and GMP-skilled labor gaps have raised operating costs and accelerated automation investments across the Europe pharmaceutical cold chain logistics market. Competitive intensity has sharpened as global integrators such as UPS, DHL, and DSV spend aggressively on acquisitions and digital visibility tools that promise real-time, batch-level temperature assurance across borders.

Key Report Takeaways

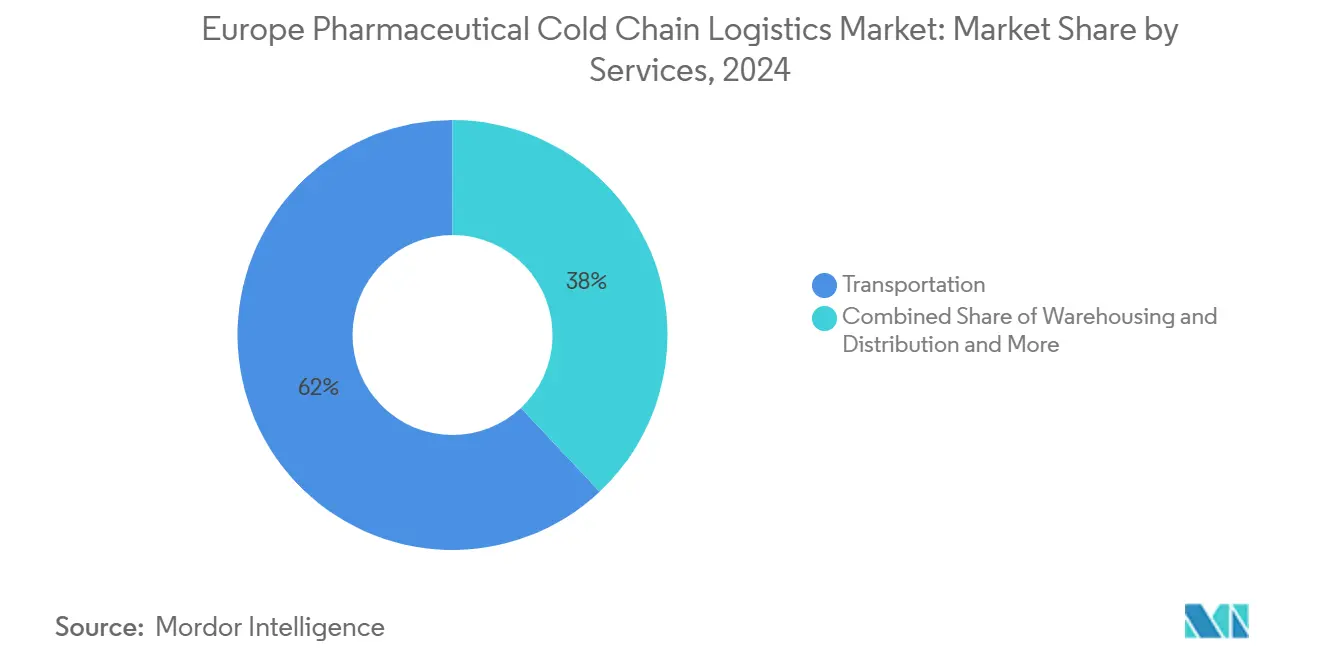

- By services, transportation led with 62% share in 2024 while value-added services are forecast to rise at a 4.10% CAGR through 2030.

- By temperature type, chilled products accounted for 41% of the Europe pharmaceutical cold chain logistics market size in 2024 and deep-frozen/ultra-low logistics is advancing at a 4.60% CAGR to 2030.

- By geography, Germany held 21% of Europe's pharmaceutical cold chain logistics market share in 2024; Poland is projected to expand at a 4.50% CAGR between 2025-2030.

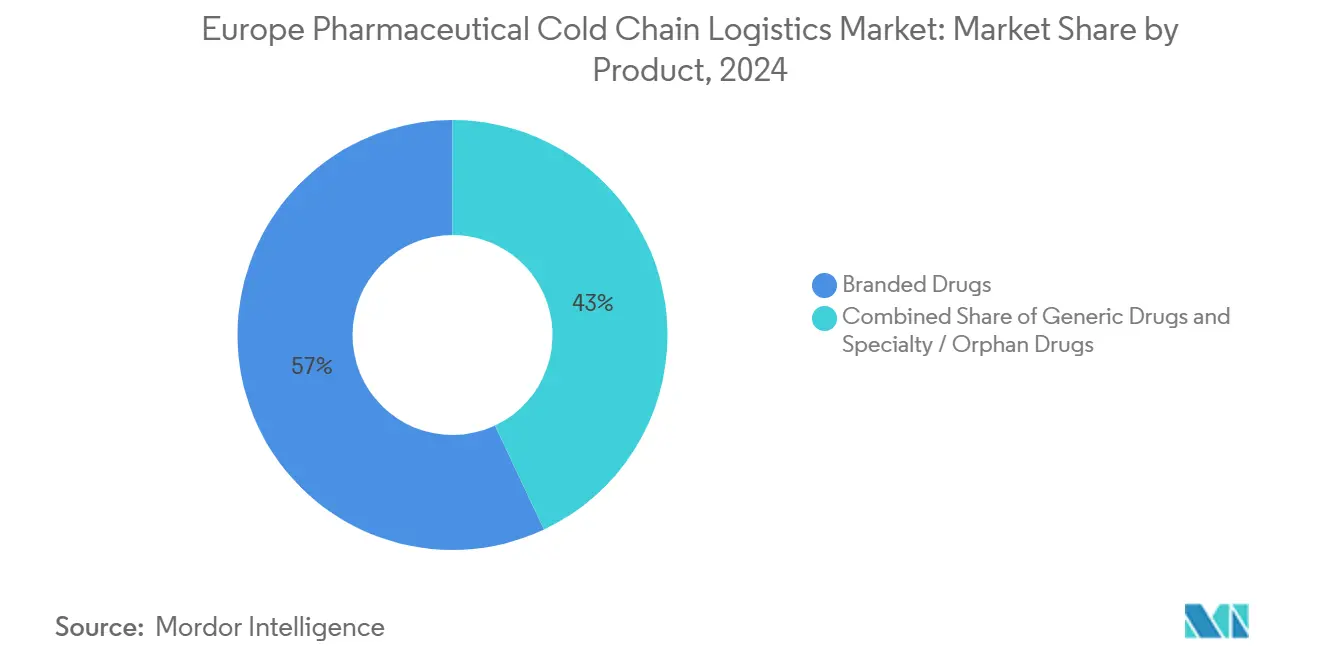

- By product, branded drugs captured 57% revenue share in 2024, while specialty/orphan drugs are poised for 5.20% CAGR growth through 2030.

- By end user, pharmaceutical manufacturers represented 41% share of the Europe pharmaceutical cold chain logistics market size in 2024, and biotech & biosimilar manufacturers show the highest expected CAGR at 5.44% during 2025-2030.

Europe Pharmaceutical Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in biologics & temperature-sensitive drugs demand | +1.2% | Germany, France, UK | Long term (≥ 4 years) |

| E-commerce & direct-to-patient last-mile growth | +0.8% | Nordic countries, Netherlands | Medium term (2-4 years) |

| Seasonal variant-adapted mRNA booster campaigns | +0.6% | EU/EEA | Short term (≤ 2 years) |

| HERA-driven pandemic stockpile purchases | +0.5% | EU-wide | Medium term (2-4 years) |

| EU GDP & serialization compliance tightening | +0.4% | Germany, France | Short term (≤ 2 years) |

| Commercialization boom in cell- & gene-therapy/ATMPs | +0.9% | Germany, UK, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Biologics & Temperature-Sensitive Drugs Demand

A growing pipeline of monoclonal antibodies, mRNA vaccines, and autologous cell products has pushed half of all new European drug approvals into cold-chain categories, many of which require controlled environments at 0-5 °C or down to -120 °C to preserve potency. The Europe pharmaceutical cold chain logistics market, therefore, sees sustained capital inflows into GDP-certified warehouses fitted with continuous power backups, liquid nitrogen chambers, and IoT sensors. Real-time lane qualification and end-to-end audit trails are now baseline expectations for sponsors submitting to EMA quality-risk assessments. Logistics providers that previously specialized in 2-8 °C vaccines now differentiate on their ability to host cryogenic fleets, digitally verify temperature excursions within ±2 °C, and generate 21 CFR Part 11-compliant data in seconds.

E-commerce & Direct-to-Patient Last-Mile Growth

Post-pandemic consumer behavior favors home delivery of prescription biologics, prompting pharmacies and tele-health platforms across the Nordics to integrate carrier-agnostic APIs that allocate shipments to couriers based on real-time temperature-validated capacity. This trend forces the Europe pharmaceutical cold chain logistics market to deploy smaller insulated parcel shippers with phase-change materials engineered for 24-hour autonomy while maintaining 2-8 °C stability, replacing bulk pallet moves to hospital warehouses. Providers must also reconcile diverse national GDP licensing rules for patient-level distribution, bringing digital labeling, photo proof-of-delivery, and automated return logistics into a single compliant workflow.

Seasonal Variant-Adapted mRNA Booster Campaigns

European vaccination strategies now incorporate semiannual COVID-19 boosters blended with influenza programs, creating two-month demand spikes for up to 150 million multi-dose vials that each require steady -50 °C conditions. Precision scheduling is critical: distribution cycles must synchronize with epidemiologic modeling that pinpoints peak transmission windows, compressing lead times and stressing the Europe pharmaceutical cold chain logistics market. Reverse-logistics flows for thawed or unused doses further compound complexity, necessitating validated lane reuse and stringent waste-documentation protocols[2]European Centre for Disease Prevention and Control, “COVID-19 Vaccination Coverage in the EU/EEA During the 2023-24 Season Campaigns,” ecdc.europa.eu.

HERA-Driven Pandemic Stockpile Purchases

The EUR 6 billion (USD 6.3 billion) HERA budget funds strategic inventories of antivirals, monoclonal antibodies, and diagnostics stored across multi-temperature nodes till 2027, effectively converting sporadic project work into multi-year service contracts. Public tenders increasingly stipulate dual-use facilities that can pivot from long-term warehousing to 48-hour national deployment. This requirement motivates new public-private partnerships in the Europe pharmaceutical cold chain logistics market and guarantees predictable capacity off-take for providers willing to co-invest in backup energy generation and 24/7 SOP-compliant staffing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy cost & infrastructure complexity | -0.9% | Germany, wider EU | Short term (≤ 2 years) |

| Counterfeiting risk & DSCSA/EU-FMD gaps | -0.3% | EU-wide | Medium term (2-4 years) |

| Declining generic-drug base-load volumes | -0.4% | EU-wide | Long term (≥ 4 years) |

| GMP-skilled labor shortages | -0.7% | Germany, Netherlands, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Cost & Infrastructure Complexity

Electricity tariffs remain 30-60% higher than pre-2022 averages across key industrial clusters, raising refrigeration OPEX and elongating ROI on new GDP facilities. Simultaneously, EU Green Deal mandates require carbon-footprint reporting, pushing operators to upgrade insulation panels, switch to low-GWP refrigerants, and install rooftop solar arrays. These capital-intensive retrofits compress margins in the Europe pharmaceutical cold chain logistics market even as compliance standards climb[3]DACHSER SE, “Chemical logistics is on the move – scenarios and outlook for Germany,” dachser.com.

GMP-Skilled Labor Shortages

The haulage sector projects a shortfall of 2 million professional drivers by 2026 and comparable deficits in GDP-qualified warehouse staff. Certification pathways take months, creating bottlenecks for lanes that demand dual-driver protocols during multi-country runs. Firms respond by automating temperature checks, deploying AMRs for case picking, and offering retention bonuses, but staffing still constrains capacity and raises service prices across the Europe pharmaceutical cold chain logistics market.

Segment Analysis

By Services: Transportation Holds Sway as Value-Added Capabilities Accelerate

Transportation accounted for 62% of Europe's pharmaceutical cold chain logistics market share in 2024, underpinned by the continent’s dense road network linking more than 200 cross-border corridors under a harmonized but stringently policed GDP umbrella. Road freight dominates because it supports pallet-level tracking, validated reefer units, and direct store delivery models that remove airport hand-offs. Airfreight remains indispensable for high-value, ultra-low shipments, yet yield management drives selective use to premium therapies with rigid stability profiles. In parallel, rail operators test refrigerated wagons between Spain and Germany, signaling modal diversification aimed at carbon reduction.

Value-added services posted the fastest growth at 4.10% CAGR, reflecting mounting demand for serialization, GDP auditing, and lane-qualification consulting. Pharma shippers now seek one-stop partners able to integrate SOP design, temperature-map packaging, and real-time dashboarding—capabilities that elevate barriers to entry and generate fee-based revenue streams within the Europe pharmaceutical cold chain logistics market. The segment also benefits from regulatory clauses that hold logistics providers jointly liable for data integrity, incentivizing investment in blockchain-ready platforms that can prove chain-of-custody compliance in seconds.

Note: Segment shares of all individual segments available upon report purchase

By Temperature Type: Chilled Leads While Deep-Frozen Surges

Chilled cargo (0-5 °C) represented 41% of the Europe pharmaceutical cold chain logistics market size in 2024, encompassing vaccines, insulins, and monoclonals whose volume streams stabilize warehouse utilization throughout the year. Operators adopt multi-chamber trucks capable of holding +15 °C, 2-8 °C, and -20 °C zones to consolidate deliveries, sharpening drop density and decreasing cost per kilometer.

Deep-frozen/ultra-low segments record the highest CAGR at 4.60% through 2030. Cell therapy sponsors bypass dry ice pallets in favor of liquid nitrogen dry-shippers that maintain -150 °C for 10 days without external power, enabling intercontinental autologous transfers. This niche compels logistics firms to invest in droplet-digital tracking that monitors internal pressure and tilt events, thereby enhancing risk mitigation across the Europe pharmaceutical cold chain logistics market.

By Product: Branded Dominance Amid Specialty Upswing

Branded drugs held a 57% share of the Europe pharmaceutical cold chain logistics market in 2024 as blockbuster biologics anchor predictable shipping calendars and justify premium logistics fees. As patents expire, generic output shifts to Asia, eroding baseline pallet flows and pressing European providers to win new-molecule programs.

Specialty and orphan therapies expand at a 5.20% CAGR to 2030. Many are produced in micro-batches tied to individual patients or ultra-narrow populations, dramatically shrinking shipment sizes while amplifying documentation complexity. Providers responding with dedicated “white-glove” teams and serialized insulated boxes lock in higher yields, signalling a structural shift toward quality-over-quantity economics in the Europe pharmaceutical cold chain logistics market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Manufacturers Rule, Biotech Rises

Pharmaceutical manufacturers generated 41% of 2024 revenue, leveraging entrenched networks and direct contracting power to specify lane audits and quality KPIs. Their multi-site production footprints continue to drive intra-EU pallet relocation, especially in Germany and Ireland.

Biotech and biosimilar firms, though smaller, register the fastest growth at 5.44% CAGR as new antibody and gene-editing platforms reach commercialization. Lacking in-house logistics units, these companies outsource cradle-to-patient supply chain orchestration, opening doorways for 4PL models inside the Europe pharmaceutical cold chain logistics market.

Geography Analysis

Germany controlled 21% of Europe's pharmaceutical cold chain logistics market share in 2024, thanks to its extensive biologics manufacturing clusters in Hessen, Baden-Württemberg, and Bavaria. Frankfurt’s airport pharma hub processed over 120,000 tons of temperature-controlled cargo in 2024, reinforcing Germany’s status as the central consolidation node for intra-EU biologics distribution. Yet rising power bills and labor scarcities spur automation programs, including refrigerated high-bay warehouses deploying shuttle robots and AI-assisted pick routing.

Poland posts the fastest 4.50% CAGR on the back of greenfield biologics plants near Łódź and Poznań, offering cost-effective fill-finish capacity for multinational companies. The Netherlands and Belgium exploit Rotterdam and Antwerp port assets, plus GDP-certified air hubs at Schiphol and Liège, to serve as European gateway nodes. Sweden and Denmark pilot direct-to-patient biologic delivery, experimenting with AI-optimized route plans that shorten lead times by 18% compared with 2023 benchmarks. Collectively, these dynamics keep the Europe pharmaceutical cold chain logistics market geographically diversified yet interlinked through stringent regulatory commonalities.

Competitive Landscape

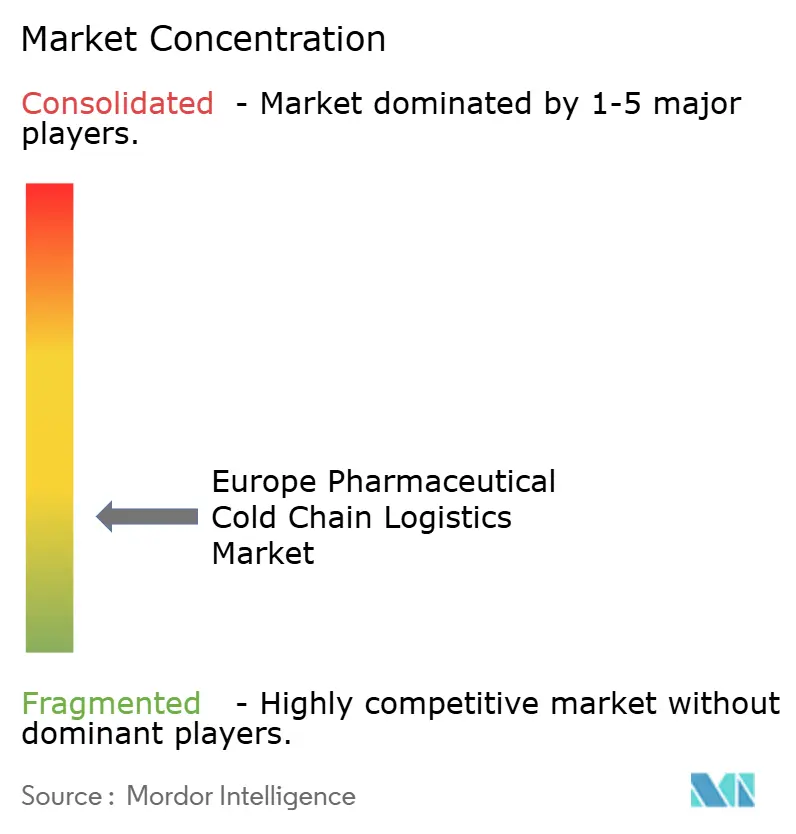

The Europe pharmaceutical cold chain logistics market is fragmented yet faces nimble specialists in ultra-cold and last-mile niches. DHL Supply Chain continues multiyear EUR 2 billion (USD 2.08 billion) deployment in GDP hubs and temperature-controlled vehicle fleets across Germany and Benelux, targeting double-digit growth via bundled warehousing-plus-transport contracts. Kuehne + Nagel expands its PharmaChain network by adding 25 GDP locations, incorporating real-time temperature telemetry into its KN Login platform to satisfy EMA data integrity audits.

UPS closed acquisitions of Frigo-Trans and BPL in January 2025, gaining four additional cryogenic warehouses and bolstering pan-European milk-run routes for 2-8 °C biologics[4]United Parcel Service, “UPS Completes Acquisitions of Healthcare Cold-Chain Logistics Providers Frigo-Trans and BPL,” ups.com. DSV finalized a EUR 14.3 billion (USD 14.9 billion) takeover of Schenker in April 2025, nearly doubling controlled-room-temperature pallet capacity and integrating Schenker’s GDP Center-of-Excellence into its existing LifeSci vertical. Regional specialists, such as Trans-o-flex and EuroTrans Pharma, defend share through dense domestic networks and guaranteed two-hour delivery windows for oncology injectables, differentiating against global integrators.

Technology constitutes the new battleground: blockchain pilots verify that refrigerated doors stayed sealed, AI models predict lane-specific excursion risk, and drones conduct yard checks on trailer power status. Logistics providers also expand consultative offerings—lane validation, risk mapping, and serialization data services—creating sticky relationships that elevate switching costs in the Europe pharmaceutical cold chain logistics market.

Europe Pharmaceutical Cold Chain Logistics Industry Leaders

-

DHL Supply Chain

-

Kuehne + Nagel International AG

-

United Parcel Service

-

DSV

-

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its EUR 14.3 billion (USD 14.9 billion) acquisition of Schenker, instantly enlarging refrigerated cross-dock capacity by 85,000 pallet positions across 18 European sites.

- April 2025: DHL Group earmarked EUR 2 billion (USD 2.08 billion) through 2030 for new GDP hubs and a 40% expansion in temperature-controlled vehicles under its Health Logistics program.

- January 2025: UPS closed purchases of Frigo-Trans and BPL, adding six multi-zone warehouses and 250 GDP-validated trucks to its European healthcare fleet.

- November 2024: CEVA Logistics launched a reusable packaging initiative aimed at lifting sustainable shipper adoption from 30% to 70% by 2030, targeting a 50,000-ton CO₂e reduction.

Europe Pharmaceutical Cold Chain Logistics Market Report Scope

Pharmaceutical logistics is related to the handling, transport, and chain management of multiple and varied products, the vast majority of which require specific conditions in their logistic treatment.

The European pharmaceutical cold chain logistics market is segmented by product (generic drugs, branded drugs), by application (bio-pharma, chemical pharma), by mode of transport (air shipping, rail shipping, road shipping, and sea shipping), by country (Germany, United Kingdom, Netherlands, France, Italy, Spain, Poland, Belgium, Sweden, and Rest of Europe).

The report offers the market sizes and forecasts for the European pharmaceutical cold chain logistics market in value (USD) for all the above segments.

| Transportation | Road |

| Air | |

| Sea | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Generic Drugs |

| Branded Drugs |

| Specialty / Orphan Drugs |

| Pharmaceutical Manufacturers |

| Biotech & Biosimilar Manufacturers |

| Hospitals & Retail Pharmacies |

| Healthcare Distributors & Wholesalers |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Poland |

| Sweden |

| Rest of Europe |

| By Services | Transportation | Road |

| Air | ||

| Sea | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Product | Generic Drugs | |

| Branded Drugs | ||

| Specialty / Orphan Drugs | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech & Biosimilar Manufacturers | ||

| Hospitals & Retail Pharmacies | ||

| Healthcare Distributors & Wholesalers | ||

| Others | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Sweden | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current valuation of the Europe pharmaceutical cold chain logistics market?

The market is valued at USD 21.50 billion in 2025 with a projected rise to USD 27.1 billion by 2030.

Which service segment holds the largest share in Europe?

Transportation commands 62% of revenue, driven by extensive road and multimodal networks.

Which temperature band is expanding the fastest?

Deep-frozen/ultra-low logistics (<-20 °C) is growing at a 4.60% CAGR owing to cell and gene therapy uptake.

Which country is the fastest-growing European market through 2030?

Poland leads with a 4.50% CAGR, propelled by new manufacturing investments and healthcare expansion.

What major acquisitions reshaped the competitive landscape in 2025?

UPS acquired Frigo-Trans and BPL, while DSV completed a EUR 14.3 billion takeover of Schenker, expanding cold-chain capacity.

Which end-user segment is expected to grow quickest?

Biotech and biosimilar manufacturers show the highest growth at a 5.44% CAGR through 2030.

Page last updated on: