Market Size of europe pet diet Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

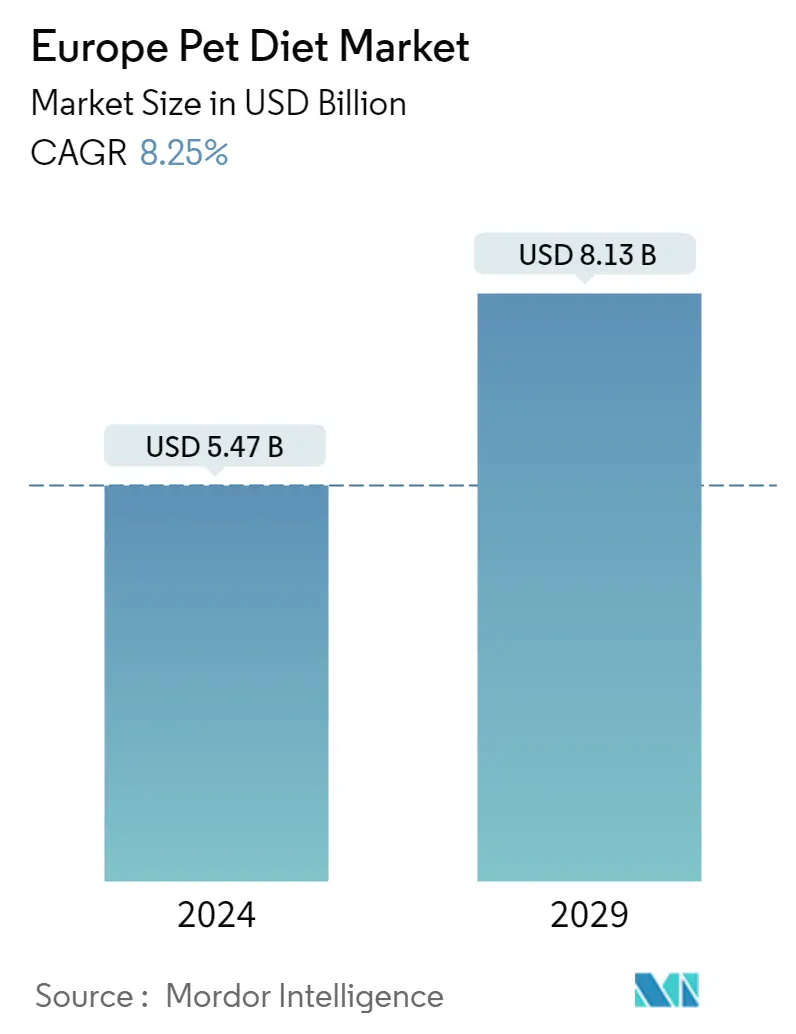

Market Size (2024) | USD 5.47 Billion |

|

|

Market Size (2029) | USD 8.13 Billion |

|

|

Largest Share by Pets | Dogs |

|

|

CAGR (2024 - 2029) | 8.25 % |

|

|

Largest Share by Country | United Kingdom |

|

|

Market Concentration | Low |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Europe Pet Diet Market Analysis

The Europe Pet Diet Market size is estimated at USD 5.47 billion in 2024, and is expected to reach USD 8.13 billion by 2029, growing at a CAGR of 8.25% during the forecast period (2024-2029).

5.47 Billion

Market Size in 2024 (USD)

8.13 Billion

Market Size in 2029 (USD)

7.83 %

CAGR (2017-2023)

8.25 %

CAGR (2024-2029)

Largest Market by Sub Product

23.11 %

value share, Digestive Sensitivity, 2022

The rising prevalence of digestive issues among pets is driving the segment, as these diets contain digestive enzymes that effectively support the healthy gut of pets.

Largest Market by Country

16.14 %

value share, United Kingdom, 2022

In the United Kingdom, the high pet population, strong consumer demand, and growing health concerns among pet owners regarding preventive pet healthcare have boosted the market growth.

Fastest-growing Market by Sub Product

9.42 %

Projected CAGR, Urinary tract disease, 2023-2029

The increasing prevalence of urinary tract infections among pets and the products' ability to reduce infections and promote pet health are expected to drive the segment during the forecast period.

Fastest-growing Market by Country

11.02 %

Projected CAGR, Poland, 2023-2029

In Poland, the rising pet ownership rates and increasing consumer spending on custom-made veterinary diets based on specific pets' health are some of the major factors driving the market growth.

Leading Market Player

15.16 %

market share, Mars Incorporated, 2022

Mars, Incorporated is the leading company as it has invested heavily in product launches that are focused on targeting multiple pet health issues, such as digestive and urinary tract diseases.

Dogs hold the largest share among pet animals, dominating the market due to the higher expenditure on them compared to other pet animals

- Veterinary diets are specialized pet food products developed to address specific health conditions in pets. In the European market, pet veterinary diets experienced a significant surge of 25.4% between 2017 and 2021. This growth could be attributed to advancements in pet nutrition science and research, leading to the innovation of more specialized diets capable of addressing a broader range of health issues in pets. Therefore, pet veterinary diets accounted for 9.6% of the European pet food market in 2022.

- Among animals in Europe, dogs dominated the market, accounting for 44.1% in 2022. This domination could be attributed to their large population in the region, accounting for 29.9% of the European pet population in the same year.

- Cats held a share of 36.3% of the pet population in 2022. Despite the larger pet cat population, they accounted for 41.9% of the market, relatively less compared to dogs. This difference could be attributed to greater dog humanization compared to cats in the region. Also, the average pet expenditure per dog was USD 4.9 thousand, whereas, for cats, it was USD 4.4 thousand in 2022. This resulted in a larger market share for dogs despite their smaller population compared to cats.

- Other pet animals accounted for 13.9% of the market value in 2022. There is potential for other pet animals in terms of veterinary diets, evidenced by the fact that these animals accounted for 33.8% of the pet population in 2022.

- The rising pet humanization and increasing incidence of diseases are anticipated to drive the European pet veterinary diet market during the forecast period.

The United Kingdom and Germany held the largest market share in the European pet veterinary diet market due to their high pet populations compared to other countries

- Pet veterinary diets play a vital role in treating specific diseases and infections in pets. They are used for both preventive and curative purposes. With the increasing awareness of pet health and well-being, veterinary diets have gained significant importance in the pet food market across the region. In 2022, veterinary diets accounted for 9.5% of the European pet food market.

- Between 2017 and 2022, the market experienced a steady growth of 44.6%, attributed to factors such as the rising pet adoption during the pandemic and the availability of a wider range of dietary options to meet pets' specific needs.

- Among European countries, the United Kingdom and Germany held the largest market shares in veterinary diets for pets, with market values of USD 750.3 million and USD 675.1 million, respectively, in 2022. This dominance in the regional market can be due to their high pet populations compared to other countries, well-established manufacturing facilities, and the growing trend of premiumization.

- Poland and Russia are expected to register the fastest growth, with CAGRs of 11.0% and 10.3%, respectively, during the forecast period due to the increasing penetration of these diets and the growing pet population in these countries.

- The availability of a diverse range of veterinary diets specifically formulated to address various pet infections and the pet owners' willingness to invest more in enhancing the health of their pets are the factors that are expected to drive the growth of the veterinary diet segment in Europe. The segment is anticipated to register a CAGR of 7% during the forecast period.

Europe Pet Diet Industry Segmentation

Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary tract disease are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. France, Germany, Italy, Netherlands, Poland, Russia, Spain, United Kingdom are covered as segments by Country.

- Veterinary diets are specialized pet food products developed to address specific health conditions in pets. In the European market, pet veterinary diets experienced a significant surge of 25.4% between 2017 and 2021. This growth could be attributed to advancements in pet nutrition science and research, leading to the innovation of more specialized diets capable of addressing a broader range of health issues in pets. Therefore, pet veterinary diets accounted for 9.6% of the European pet food market in 2022.

- Among animals in Europe, dogs dominated the market, accounting for 44.1% in 2022. This domination could be attributed to their large population in the region, accounting for 29.9% of the European pet population in the same year.

- Cats held a share of 36.3% of the pet population in 2022. Despite the larger pet cat population, they accounted for 41.9% of the market, relatively less compared to dogs. This difference could be attributed to greater dog humanization compared to cats in the region. Also, the average pet expenditure per dog was USD 4.9 thousand, whereas, for cats, it was USD 4.4 thousand in 2022. This resulted in a larger market share for dogs despite their smaller population compared to cats.

- Other pet animals accounted for 13.9% of the market value in 2022. There is potential for other pet animals in terms of veterinary diets, evidenced by the fact that these animals accounted for 33.8% of the pet population in 2022.

- The rising pet humanization and increasing incidence of diseases are anticipated to drive the European pet veterinary diet market during the forecast period.

| Sub Product | |

| Diabetes | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Renal | |

| Urinary tract disease | |

| Other Veterinary Diets |

| Pets | |

| Cats | |

| Dogs | |

| Other Pets |

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Country | |

| France | |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Europe Pet Diet Market Size Summary

The European pet diet market is experiencing robust growth, driven by increasing pet humanization and a rising awareness of pet health. Veterinary diets, which are specialized pet food products designed to address specific health conditions, have gained significant traction in the region. This growth is attributed to advancements in pet nutrition science, leading to the development of diets that cater to a broader range of health issues. Dogs dominate the market, largely due to their significant population and the higher expenditure on their care compared to cats. Despite cats being more numerous, the greater humanization of dogs contributes to their larger market share. Other pet animals also present a growing opportunity, with a notable portion of the pet population in Europe.

The market is characterized by a diverse range of veterinary diets and a trend towards premiumization, with pet owners willing to invest more in their pets' health. The COVID-19 pandemic has further accelerated the adoption of pets and the shift towards online sales channels, enhancing market accessibility. Key players in the market include Affinity Petcare SA, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle (Purina), and Virbac, who are actively expanding their presence and product offerings. The market's growth is supported by cultural factors, such as the affinity for cats in countries like Russia, and the increasing popularity of premium and medium-priced pet food options.

Europe Pet Diet Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Sub Product

-

1.1.1 Diabetes

-

1.1.2 Digestive Sensitivity

-

1.1.3 Oral Care Diets

-

1.1.4 Renal

-

1.1.5 Urinary tract disease

-

1.1.6 Other Veterinary Diets

-

-

1.2 Pets

-

1.2.1 Cats

-

1.2.2 Dogs

-

1.2.3 Other Pets

-

-

1.3 Distribution Channel

-

1.3.1 Convenience Stores

-

1.3.2 Online Channel

-

1.3.3 Specialty Stores

-

1.3.4 Supermarkets/Hypermarkets

-

1.3.5 Other Channels

-

-

1.4 Country

-

1.4.1 France

-

1.4.2 Germany

-

1.4.3 Italy

-

1.4.4 Netherlands

-

1.4.5 Poland

-

1.4.6 Russia

-

1.4.7 Spain

-

1.4.8 United Kingdom

-

1.4.9 Rest of Europe

-

-

Europe Pet Diet Market Size FAQs

How big is the Europe Pet Diet Market?

The Europe Pet Diet Market size is expected to reach USD 5.47 billion in 2024 and grow at a CAGR of 8.25% to reach USD 8.13 billion by 2029.

What is the current Europe Pet Diet Market size?

In 2024, the Europe Pet Diet Market size is expected to reach USD 5.47 billion.