Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

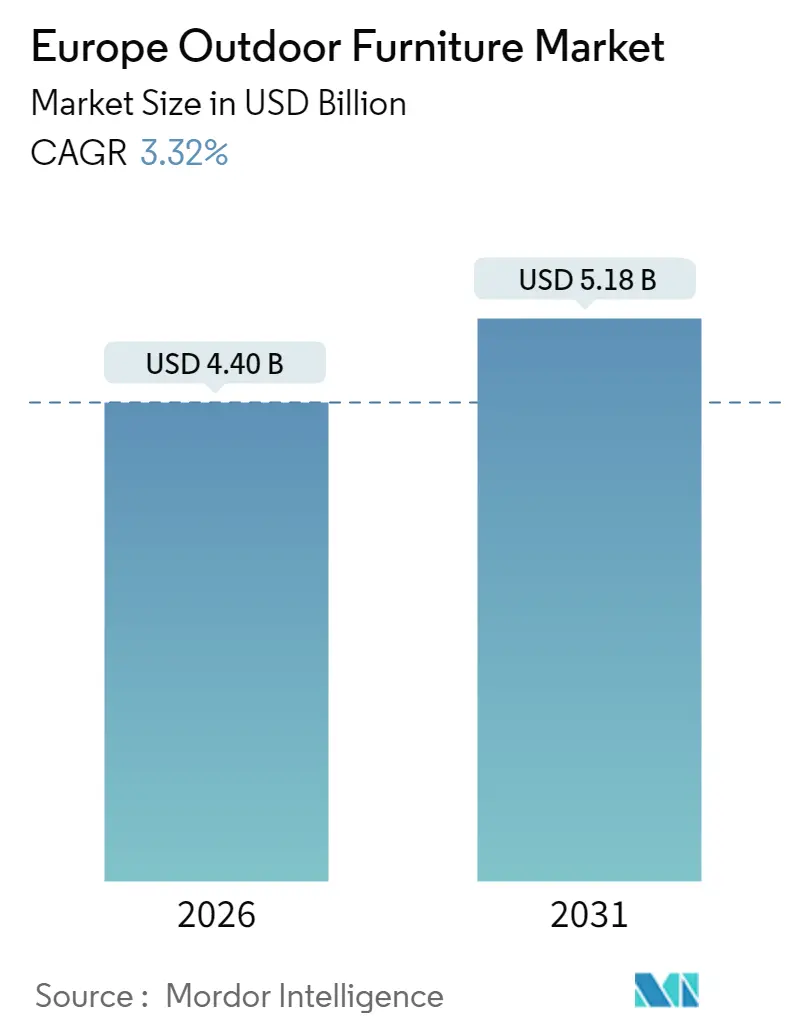

| Market Size (2026) | USD 4.4 Billion |

| Market Size (2031) | USD 5.18 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Outdoor Furniture Market Analysis by Mordor Intelligence

Europe outdoor furniture market size in 2026 is estimated at USD 4.4 billion, growing from 2025 value of USD 4.26 billion with 2031 projections showing USD 5.18 billion, growing at 3.32% CAGR over 2026-2031. Demand momentum is rooted in sustained hospitality refurbishment programs, growing residential investments in balcony and patio upgrades, and the region-wide regulatory pivot toward circular design. Producers have adapted to macroeconomic headwinds by moderating prices and widening sustainable product lines, which has helped the Europe outdoor furniture market maintain positive volume traction. Strategic production ramp-ups—including IKEA’s price rollback and factory additions—signal continuing confidence in mid-term demand fundamentals [1]Inter IKEA Group, “FY24 Price Investment Statement,” about.ikea.com. . At the same time, raw-material cost swings and seasonal buying patterns remain structural challenges that suppliers must manage through agile sourcing and inventory practices.

Key Report Takeaways

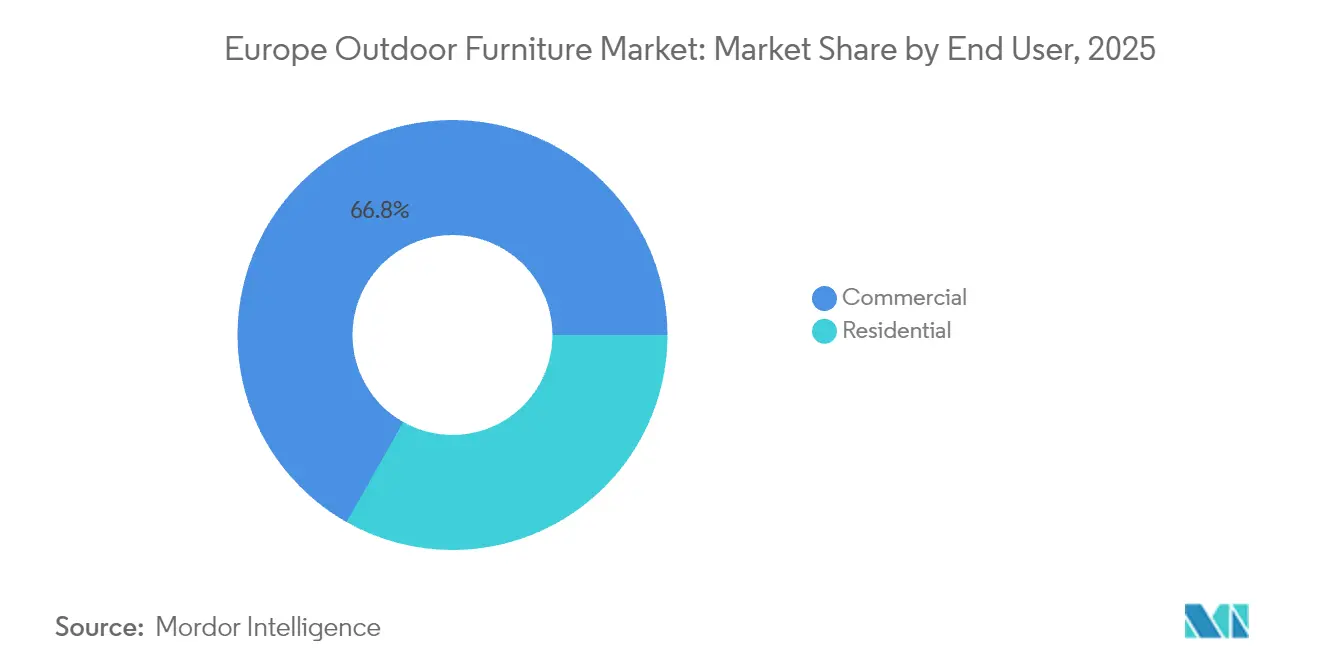

- By end user, commercial applications led with 66.80% share of the European outdoor furniture market in 2025, while the residential segment is forecast to expand at a 5.17% CAGR through 2031.

- By material, wood captured 40.30% of the European outdoor furniture market share in 2025; recycled plastic offerings are growing at a 4.72% CAGR to 2031.

- By distribution channel, B2B contractors accounted for a 57.80% share of the European outdoor furniture market size in 2025, whereas B2C e-commerce is set to rise at a 4.01% CAGR.

- By geography, Germany held 16.85% revenue share in 2025, and France is advancing at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Outdoor Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in hospitality & tourism contract demand | +0.8% | Germany, France, Spain, Italy | Medium term (2-4 years) |

| Rising consumer spend on outdoor living spaces | +0.6% | NORDICS, BENELUX, UK | Long term (≥ 4 years) |

| Expansion of e-commerce furniture retail | +0.5% | Germany, UK, France | Short term (≤ 2 years) |

| EU green public-procurement sustainability push | +0.4% | EU-wide, strongest in Germany, NORDICS | Long term (≥ 4 years) |

| Hybrid-work demand for balcony & patio furnishing | +0.3% | Urban centers across Europe | Medium term (2-4 years) |

| Emergence of smart, multifunctional outdoor furniture designs | +0.2% | Germany, NORDICS, BENELUX | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Hospitality & Tourism Contract Demand

Hotel, restaurant, and leisure operators are refurbishing terraces and poolside zones to meet travelers’ preference for open-air experiences, which drives bulk furniture procurements and fuels commercial segment dominance. Compagnie des Alpes recorded more than 10 million visitors in its most recent fiscal year and earmarked fresh capex for outdoor capacity upgrades, highlighting steady contract pipelines [2]Compagnie des Alpes, “2023 Investor Presentation,” compagniedesalpes.com. . Mediterranean destinations enjoy extended high-season windows that amplify furniture turnover, while mountain and northern resorts invest in weather-resistant fixtures to lengthen operating days. Sustainability specifications are becoming standard in tenders, favoring certified timber and recycled plastic constructions. This driver’s medium-term impact reflects the hospitality sector’s phased renovation cycles and macro-tourism recovery.

Rising Consumer Spend on Outdoor Living Spaces

Hybrid work patterns have prompted European households to view balconies, patios, and gardens as functional extensions of interior rooms. The residential slice of the Europe outdoor furniture market is therefore growing faster than the commercial slice as consumers channel discretionary budgets toward lounge sets, daybeds, and ergonomic chairs. IKEA accelerated this shift by trimming average price points 10% during FY 2024 to catalyze volume gains without sacrificing design quality. Nordic consumers, who prize nature immersion and long daylight hours, lead per-capita spending on premium sets that marry aesthetics with durability. The long-term horizon of this driver rests on generational lifestyle preferences that consistently emphasize well-equipped outdoor zones.

Expansion of E-commerce Furniture Retail

Online channels now enable shoppers to compare materials, view configurators, and schedule white-glove delivery for bulky items once confined to brick-and-mortar showrooms. In Switzerland and Austria, furniture already claims roughly 10% of total e-commerce receipts, illustrating headroom for wider regional diffusion. XXXLutz, for example, amassed USD 281 million in digital sales during 2023, validating scalability in virtual storefronts. Consumers appreciate transparent sustainability data online, which allows recycled plastic and certified-wood brands to spotlight lifecycle merits alongside price. Improved last-mile logistics and the spread of frictionless payment apps reinforce the short-term impetus.

EU Green Public-Procurement Sustainability Push

Public agencies across Europe must follow the European Commission’s Green Public Procurement criteria for furniture, effectively steering demand toward low-emission and repairable products [3]European Commission, “Green Public Procurement Criteria for Furniture,” environment.ec.europa.eu. . Because public bodies wield large purchasing budgets, their specifications shape broader market expectations, including in private resort developments and corporate campuses. The Nordic Council advances this agenda through Product-Service-System pilots that extend the service life of contract furniture from 6 years to as many as 30 years [4]Nordic Council of Ministers, “Product-Service Systems in the Nordic Furniture Sector,” norden.org. . Manufacturers that carry environmental labels such as Blue Angel or FSC thus enjoy higher tender win rates. The long-term nature of regulatory rollouts solidifies this demand driver for the decade ahead.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -0.7% | EU-wide, particularly Germany, NORDICS | Short term (≤ 2 years) |

| Seasonal sales cyclicality | -0.4% | Northern Europe, NORDICS | Medium term (2-4 years) |

| EU extended-producer-responsibility (EPR) costs | -0.3% | EU-wide, strongest in Germany, France | Medium term (2-4 years) |

| Rise of rental/subscription furniture models | -0.2% | Urban centers, NORDICS, BENELUX | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Cost Volatility

European lumber prices have seesawed since 2022, when Swedish softwood exports to the continent fell 5%, tightening regional supply and inflating input costs. Wood-based products, which account for 40.7% of the Europe outdoor furniture market, bear the brunt of this turbulence. Manufacturers attempt to hedge by sourcing from alternate geographies, yet freight surcharges and certification inconsistencies raise landed costs. Passing hikes through to consumers remains difficult because price sensitivity rises during economic uncertainty. Metal and recycled-plastic feedstocks also encounter energy-linked price swings, compressing margins in the short run.

Seasonal Sales Cyclicality

Outdoor furniture demand peaks from April to August, leaving northern suppliers with excess capacity and inventory risk during colder months. Retailers mark down unsold stock late in the season, compelling factories to realign production schedules and financing strategies. While Mediterranean markets offer longer buying windows, they do not fully offset northern troughs. Some brands introduce weather-resistant indoor-outdoor hybrids to stretch usage, yet consumer acceptance is still nascent. Consequently, the market’s medium-term upside is dampened by entrenched seasonal rhythms.

Segment Analysis

By Product Type: Chairs Dominate Volume While Loungers Propel Premium Growth

Chairs held 41.10% of the Europe outdoor furniture market in 2025 on account of their ubiquity across dining, cafe, and event venues. The Europe outdoor furniture market size for chairs benefits from high replacement frequency because casual seating weathers faster than tables. Loungers and daybeds are forecast to post a 5.62% CAGR through 2031 as wellness trends boost demand for relaxation-oriented layouts. Manufacturers differentiate these premium items through adjustable backrests, quick-dry foams, and smartphone docking features that extend stay times for hospitality patrons. Multifunctional sets that combine modular ottomans with storage compartments resonate in urban apartments where space is scarce.

Demand for tables and full dining sets remains steady because families prioritize coordinated aesthetics and durable surfaces for alfresco meals. Smart integrations, including solar charging spots, are moving from novelty to value-added option, especially in lounge furniture. HAHN Kunststoffe leverages recycled polymer slats to produce maintenance-free seating that satisfies Blue Angel criteria while lowering lifecycle costs. Commercial tenders increasingly mandate stackability and rapid cleaning features to streamline operations. The long-tail “other” category, embracing benches, planters, and umbrellas, delivers steady incremental revenue that rounds out assortments.

Note: Segment shares of all individual segments available upon report purchase

By Material: Wood Retains Leadership Yet Recycled Plastic Gains Momentum

Wood accounted for 40.30% of the Europe outdoor furniture market in 2025, buoyed by its natural feel and consumers’ perception of premium craftsmanship. Raw-material headwinds and forestry certification expenses, however, expose profitability to volatility. Conversely, plastic—especially post-consumer recycled grades—will register the quickest gains, expanding at a 4.72% CAGR as municipal recycling targets push buyers toward circular alternatives. The Europe outdoor furniture market size for recycled-plastic seating is projected to widen further once supply chains mature and colorfastness improves. Metal frames thrive in modern bistro concepts, providing slim profiles and durability against wind loads.

Composite materials blend natural fibers with high-density polyethylene, offering wood-like aesthetics without splintering, and earn growing interest from public-space specifiers seeking vandal-resistant surfaces. EU EPR policies reward designs with mono-material construction that simplifies end-of-life processing, thereby favoring plastics and metals over multi-layered wood-plastic hybrids. VAT incentives for repaired or refurbished furniture in several member states additionally nudge buyers away from virgin hardwoods. Certification logos such as FSC and Blue Angel have become must-have badges during procurement, guiding both commercial and residential decisions. Suppliers that align material science innovations with compliance regimes stand to capture outsized share gains.

By End User: Commercial Bulk Orders Prevail While Residential Demand Accelerates

Commercial venues represented 66.80% of 2025 shipments, cementing their weight in the Europe outdoor furniture market thanks to large-scale hotel, restaurant, and resort orders. Operators focus on gross-margin payback by selecting robust pieces that endure frequent relocation and intensive cleaning cycles. Many also copy residential aesthetics to deliver “home-away-from-home” ambience that encourages longer guest dwell times. The residential slice, though smaller, will chart a quicker trajectory because stay-at-home preferences spur patio makeovers, pushing the Europe outdoor furniture market share of the segment upward. Higher disposable incomes in Scandinavia and the Netherlands foster demand for premium loungers with built-in heating pads that extend usage into cooler evenings.

Some commercial buyers now explore rental programs that refresh aesthetics annually without capital outlays, creating hybrid revenue streams for suppliers. Residential customers mimic professional spaces by opting for contract-grade finishes that promise longer warranties. Cross-segmentation is further evident as boutique hotels adopt artisan wood benches sourced from local carpenters to signal authenticity. Conversely, co-living complexes equip communal rooftops with modular sets that mirror private-home trends, blurring traditional market boundaries. This convergence obliges brands to carry versatile catalogues that satisfy both specification grids and lifestyle aspirations.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Contractor Networks Rule but Digital Direct-to-Consumer Grows Swiftly

Contractor-led B2B networks commanded 57.80% of 2025 transactions because hospitality and public-sector renovations often bundle furniture within turnkey packages. Specifiers rely on trusted supply chains to meet tight construction timelines, reinforcing repeat volumes for incumbent vendors. Yet the Europe outdoor furniture market is witnessing fast B2C gains, with online platforms fueling a 4.01% CAGR thanks to expanded product visualization and doorstep assembly services. The Europe outdoor furniture market size attributable to e-commerce will deepen as virtual reality tools let buyers preview sets in precise balcony dimensions. Specialty showrooms still matter for tactile assessment in premium price brackets, though many now operate click-and-collect formats to merge physical and digital journeys.

Home-center chains cater to budget shoppers seeking immediate pick-up, while pop-up summer stores in tourist hubs capture seasonal spikes. Logistics innovation—such as flat-pack kits and recyclable pallet returns—reduces last-mile frictions and lowers damage claims. Mobile wallets like TWINT ease checkout in Switzerland and inspire similar wallet launches elsewhere, shrinking cart abandonment. Manufacturers also pilot subscription drop-offs, enabling consumers to swap styles each season, which cushions demand dips linked to weather variability. The channel mix will therefore diversify, compelling firms to refine price ladders and after-sales service levels.

Geography Analysis

Germany captured 16.85% of 2025 revenue, reflecting its status as Europe’s largest consumer economy and an engineering base that supports value-adding automation. Builders and municipal bodies there specify recycled plastic benches from HAHN Kunststoffe, which processes 90,000 tons of waste annually under Blue Angel oversight. Energy price spikes and softer residential construction temper near-term growth, yet sustainability preferences and premium garden culture sustain steady replacement cycles. Regional clustering of suppliers in Bavaria and North Rhine-Westphalia shortens lead times for central European buyers. Government incentives for circular design further reinforce domestic sourcing.

France is forecast to log the swiftest expansion at a 4.88% CAGR as consumers upscale terraces and cafés refresh curbside seating to serve growing tourist arrivals. Parisian apartments with compact balconies drive need space-saving loungers and foldable tables that maximize utility without crowding walkways. Provence and Côte d’Azur resorts extend outdoor seasons into late autumn, widening commercial replenishment windows. French producers benefit from the country’s advanced woodworking heritage, yet they must still counter Asian import competition on entry-level SKUs. National EPR furniture rules encourage a pivot toward mono-material plastics that ease downstream recycling.

The United Kingdom sustains mid-single-digit momentum amid economic challenges thanks to entrenched garden culture and strong do-it-yourself retail channels. Online research rates are high, leading to rapid adoption of configurator tools for customized patio sets. Spain and Italy leverage long tourist seasons to maintain healthy commercial refurbishment pipelines, yet cyclical employment and credit conditions create occasional demand lulls. Nordic markets, though hampered by shorter summers, compensate through higher average selling prices because consumers invest in hardier, design-led lines suited to harsh weather. BENELUX nations, with dense urban living and affluent households, demonstrate appetite for modular, multifunctional pieces that support flexible social gatherings.

Competitive Landscape

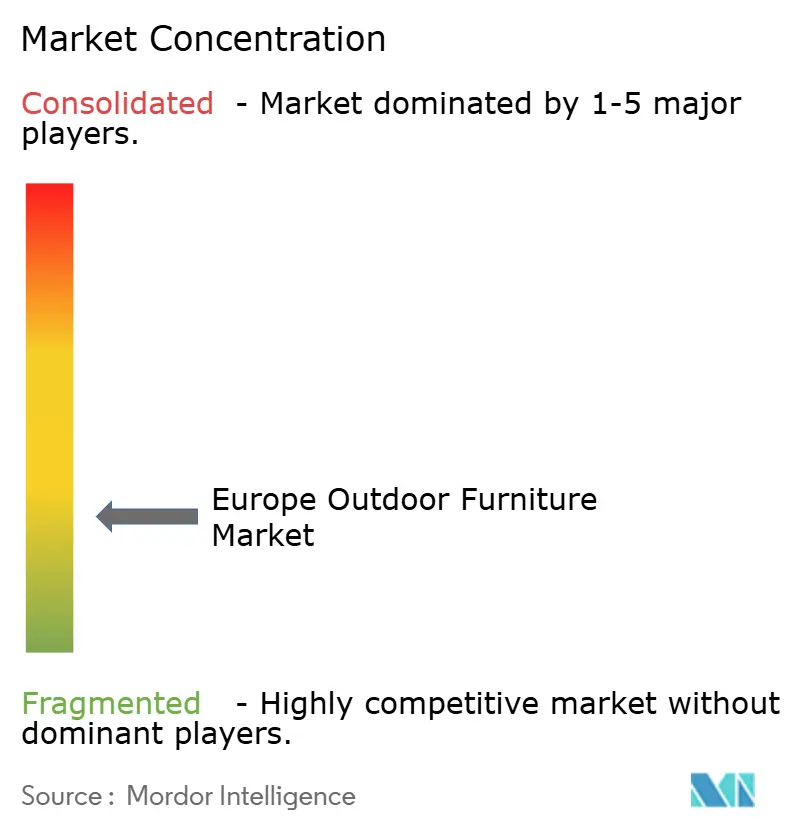

The Europe outdoor furniture market is moderately fragmented, with competition extending beyond the top five companies. IKEA anchors the high-volume tier, having earmarked EUR 2.2 billion for new eco-efficient factories in Slovakia and Sweden that expand automated throughput and reduce carbon footprints. HAHN Kunststoffe carves out a sustainability niche by transforming post-consumer polymers into low-maintenance benches and tables, securing contracts from municipalities keen on circular procurement. Royal Botania targets the luxury pocket with artisanal teak and brushed-steel pieces, launching the Carés chair line in 2024 to reinforce design leadership.

Subscription pioneer NORNORM channels EUR 110 million (USD 128.0 million) of fresh capital into European expansion, challenging ownership norms by offering pay-as-you-go packages that lower upfront costs for startups and co-working hubs. Domestic mid-scale producers confront margin compression when competing against low-cost Asian imports, prompting many to emphasize quick-delivery programs and bespoke finishes. Digital transformation accelerates across the board as augmented-reality shopping apps and AI-driven style advisors gain mainstream traction, demanding IT investments that favor larger balance sheets. Brands also partner with architects to co-design signature collections that secure exclusive hospitality rollouts, thereby locking in volume visibility.

Compliance proficiency is no longer a differentiator but a ticket to play, given EU-wide EPR and eco-design statutes that standardize baseline performance. Firms enhance resilience by dual-sourcing non-wood inputs and pre-booking freight capacity ahead of peak season, lessons learned from recent supply chain snarls. Collaborative R&D consortia explore bio-based resins and 3D-printed recycled composites, eyeing long-term breakthroughs that decouple growth from virgin material constraints. Competitive intensity therefore hinges on a triad of cost stewardship, sustainability verification, and omnichannel reach, with laggards at risk of steady share erosion.

Europe Outdoor Furniture Industry Leaders

-

IKEA Group

-

Kettler

-

Hartman Outdoor Products

-

Fermob

-

Royal Botania

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Inter IKEA Group acquired its Baltic retail franchises to deepen direct customer engagement across Estonia, Latvia, and Lithuania.

- July 2024: Royal Botania introduced the Carés chair line, combining FSC-certified teak with recyclable aluminum frames to bolster sustainability appeal.

- March 2024: HAHN Kunststoffe GmbH expanded recycled-plastic capacity to 90,000 tons per year while retaining Blue Angel certification.

- January 2024: IKEA relaunched the Nytillverkad collection, reviving 1960s icons with updated materials and colors for global rollout.

Europe Outdoor Furniture Market Report Scope

The European outdoor furniture market is involved in the creation, distribution, and sale of furniture specifically designed for outdoor environments such as gardens, patios, balconies, and terraces. This market includes a broad array of products, including seating options (chairs, benches, loungers), dining sets, tables, and decorative items made from materials such as wood, metal, plastic, wicker, and textiles. It serves both residential and commercial segments, focusing on providing durable, weather-resistant, and visually appealing furniture for enhancing outdoor living spaces.

The European outdoor furniture market is segmented by material, product, end user, distribution channel, and country. By material, the market is segmented into wood, metal, plastic, and other materials. By product, the market is segmented into chairs, tables, seating sets, loungers and daybeds, dining sets, and other products. By end user, the market is segmented into commercial and residential. By distribution channel, the market is segmented into multi-brand stores, specialty stores, online platforms, and other distribution channels. By country, the market is segmented into Germany, the United Kingdom, France, Italy, and the Rest of Europe. The report provides market sizes and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Chairs |

| Tables |

| Seating Sets |

| Loungers and Daybeds |

| Dining Sets |

| Other Products |

By Material

| Wood |

| Metal |

| Plastic |

| Other Materials |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C Channels | Specialty Stores |

| Home Centers | |

| Online | |

| Other Distribution Channels | |

| B2B Channel/Contractors |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type | Chairs | |

| Tables | ||

| Seating Sets | ||

| Loungers and Daybeds | ||

| Dining Sets | ||

| Other Products | ||

| By Material | Wood | |

| Metal | ||

| Plastic | ||

| Other Materials | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C Channels | Specialty Stores |

| Home Centers | ||

| Online | ||

| Other Distribution Channels | ||

| B2B Channel/Contractors | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe outdoor furniture market?

The market is valued at USD 4.4 billion in 2026 and is projected to reach USD 5.18 billion by 2031.

How fast is demand growing for recycled plastic outdoor furniture in Europe?

Recycled plastic pieces are expanding at a 4.72% CAGR, the quickest among material categories.

Which end-user segment is growing faster, residential or commercial?

Which end-user segment is growing faster, residential or commercial?

Which end-user segment is growing faster, residential or commercial?

France combines outdoor lifestyle premiumization with a rebound in tourism, driving a 4.88% CAGR through 2031.

How are EU regulations affecting product design?

Extended Producer Responsibility and Green Public Procurement rules push manufacturers toward mono-material, recyclable designs and verified eco-labels.

Page last updated on: