Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 75.28 Billion |

| Market Size (2031) | USD 85.91 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Organic Food And Beverages Market Analysis by Mordor Intelligence

The European organic food and beverages market size stands at USD 75.28 billion in 2026 and is projected to reach USD 85.91 billion by 2031, reflecting a 5.27% CAGR. Momentum comes from rising health awareness, premiumization of high-value categories, and the rapid scaling of digital commerce that lowers the friction of premium-price purchases. Multinationals are locking in certified supply through regenerative-agriculture contracts, while niche disruptors exploit functional innovation to secure urban millennial demand. Shelf-life-extending technologies, stronger EU organic regulations, and corporate Scope 3 decarbonization targets further reinforce demand resilience. Supply-side shocks from weather volatility and Brexit-related inspections are being absorbed through localized sourcing, nitrogen-flush canning, and retailer discounting strategies that conserve volume yet protect value growth.

Key Report Takeaways

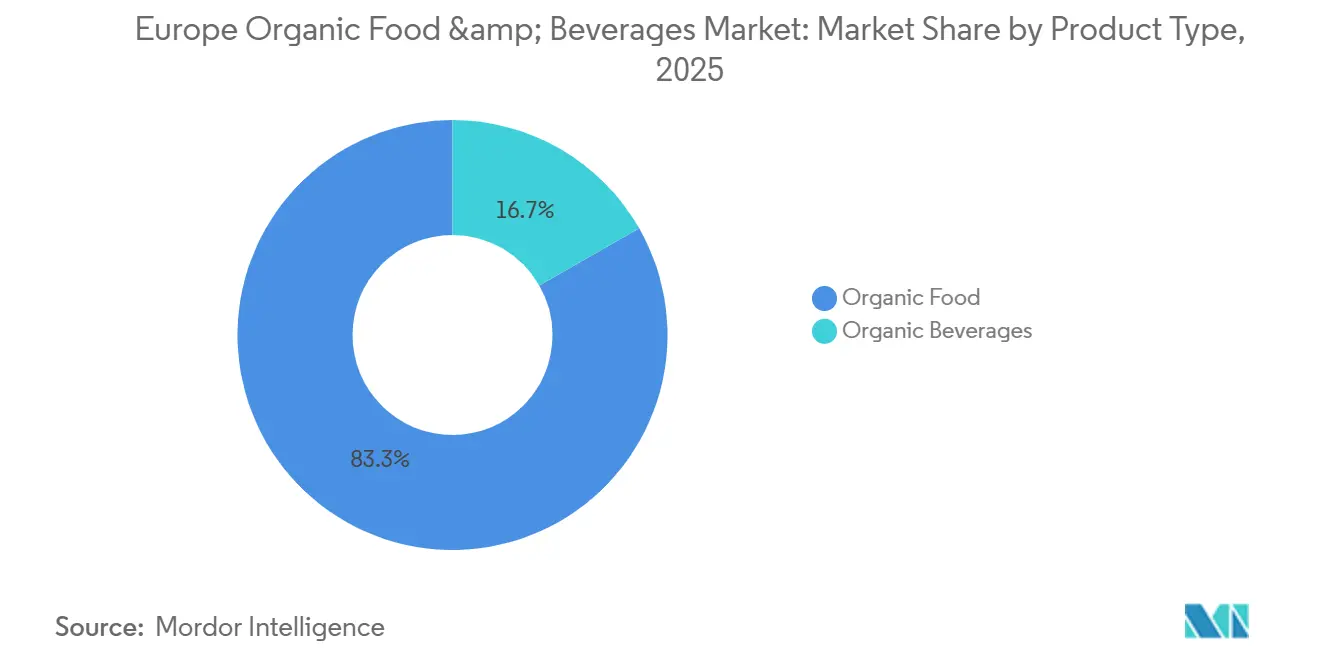

- By product type, Organic Food led with 83.26% revenue share in 2025, while Organic Beverages are forecast to advance at a 6.78% CAGR through 2031.

- By form, Fresh/Chilled products accounted for 67.75% of the European organic food and beverages market share in 2025, yet Canned formats are projected to expand at a 7.18% CAGR to 2031.

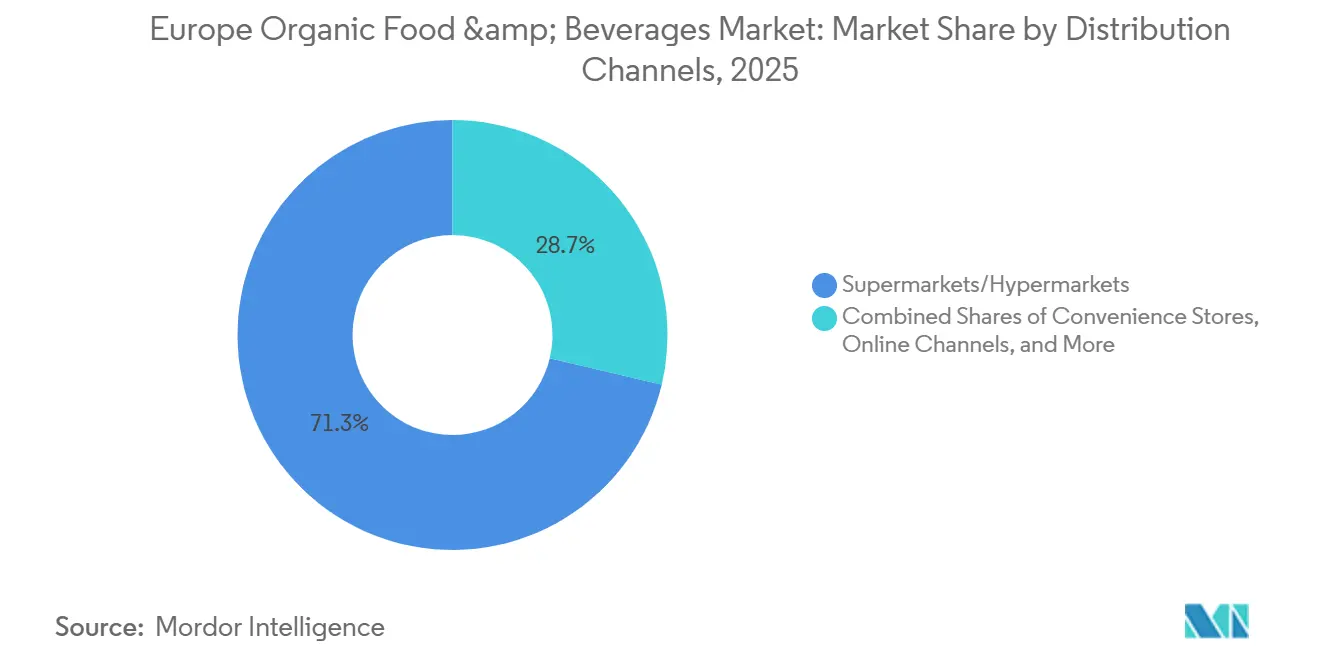

- By distribution channel, Supermarkets and Hypermarkets captured 71.28% of the 2025 value, while Online Channels are expected to post a 6.85% CAGR, the fastest among all channels.

- By geography, Germany held 35.31% of regional sales in 2025, whereas Poland is positioned for the quickest growth at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Organic Food And Beverages Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health awareness drives demand for clean-label products free from pesticides and additives | +1.2% | Global, with highest intensity in Germany, Netherlands, France | Medium term (2-4 years) |

| Plant-based trend fuels organic dairy alternatives and vegan beverages | +1.0% | Western Europe (Germany, UK, Netherlands), expanding to Poland, Spain | Short term (≤ 2 years) |

| Urban millennials prioritize organic for immunity and wellness | +0.8% | Metropolitan areas across Germany, France, UK, Netherlands, Belgium | Medium term (2-4 years) |

| Sustainability certifications align with Scope 3 emissions goals | +0.7% | Germany, France, Netherlands, UK (corporate procurement focus) | Long term (≥ 4 years) |

| Strong regulatory framework via EU Organic Regulation | +0.6% | EU-27 member states, with spillover to UK post-Brexit alignment discussions | Long term (≥ 4 years) |

| Premiumisation of high-penetration categories | +0.9% | Germany, France, UK, Netherlands (high disposable income markets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plant-Based Trend Fuels Organic Dairy Alternatives and Vegan Beverages

In 2024 and 2025, the demand for oat milk in Germany and the UK is expected to grow significantly, with sales projected to increase by double digits. This growth is driven by manufacturers improving formulations to achieve barista-grade foam stability and fortifying products with calcium and B12 to closely match the nutritional profile of dairy. Oatly's strategic decision in 2024 to source oats locally from British farms not only reduced logistics-related emissions by an estimated 15% but also mitigated risks associated with weather volatility in Eastern Europe. This move aligned well with the sustainability goals of UK retailers, particularly those focused on meeting Scope 3 carbon reduction targets. However, plant-based options continue to gain traction among flexitarian consumers, who often prioritize animal welfare considerations over carbon footprint alone. Additionally, the functional beverage segment is experiencing rapid innovation. Brands such as Minor Figures are introducing organic oat drinks infused with adaptogens and nootropics, targeting cognitive performance and mental well-being. These value-added products are positioned as premium offerings, enabling them to command price premiums of 40 to 60% compared to standard oat milk.

Urban Millennials Prioritize Organic for Immunity and Wellness

In Berlin, Paris, Amsterdam, and London, urban consumers are increasingly perceiving organic food as a proactive investment in their health rather than merely a lifestyle choice. According to survey data from 2025, 62% of urban millennials identify immunity support as their primary motivation for purchasing organic products, surpassing environmental concerns. This demographic shows a strong preference for organic produce with high ORAC scores—such as blueberries, kale, and turmeric—and demonstrates a willingness to pay a premium of 35 to 50% for cold-chain systems that maintain the phytonutrient content of these products. Retailers with robust last-mile logistics have significantly benefited from this behavior, as it aligns with consumer demand for quality and freshness. E-commerce platforms have effectively leveraged this trend by bundling organic staples with value-added services, including telehealth consultations and personalized nutrition plans. This approach has successfully converted one-time buyers into loyal subscription customers, who exhibit a lifetime value 70% higher than that of traditional walk-in shoppers.

Sustainability Certifications Align with Scope 3 Emissions Goals

Multinational food-service operators and retail chains are increasingly incorporating organic certification into their supplier scorecards. This strategic shift serves as a proxy for Scope 3 carbon reductions and is driving contract volumes toward farms that implement third-party-verified regenerative agricultural practices. Danone has announced a significant commitment of EUR 1.1 billion for the period between 2024 and 2030 to support regenerative agriculture initiatives. In partnership with Soil Capital, Danone plans to enroll 50,000 European dairy and crop farms in carbon-farming programs. These programs reward farmers based on measurable carbon sequestration outcomes rather than solely focusing on compliance with input standards. This approach is gaining traction among private-equity firms, which view certified organic supply chains as resilient assets. These supply chains are considered inflation-hedged and capable of maintaining stable premiums, even during periods of economic uncertainty. Additionally, in 2024, the European Investment Bank provided USD 20 million in funding to Heura Foods, a Spanish company specializing in plant-based protein production. This investment aims to enhance organic soy sourcing from EU-based farms, reducing dependency on South American imports and shortening supply chains by an average of 4,000 kilometers, thereby improving efficiency and sustainability[1]Source: European Investment Bank, “Heura Foods Financing 2024,” eib.org.

Premiumisation of High-Penetration Categories

Parents are increasingly viewing organic infant formula and baby food as essential investments in their children's health. This trend of premiumization is evident, with Hipp's carbon-neutral production facilities in Germany allowing the brand to charge a 25% premium over conventional counterparts, all while securing a 40% market share in Central Europe. Alnatura, boasting over 220 specialty stores throughout Germany, achieved a notable USD 1.4 billion in revenue for the fiscal year 2023/2024. Their success is attributed to private-label organic products, which are priced 15 to 20% lower than those of multinational brands, yet still command a 30% premium over conventional supermarket offerings. This strategic pricing effectively attracts middle-income households looking to upgrade from discount chains. Meanwhile, cold-pressed organic juices are transitioning from niche health-food outlets to mainstream supermarkets. Brands are employing high-pressure processing (HPP) to extend shelf life to 45 days without resorting to thermal pasteurization. This method not only preserves enzyme activity but also justifies the USD 6 to USD 8 per liter price tag. In the realm of beverages, organic wine and craft beer are gaining traction as premium products. In countries like France, Italy, and Belgium, the combination of appellations, brewery heritage, and organic certification allows these drinks to command a 40 to 70% premium over their conventional counterparts.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply shortages from weather events and limited farmland | -0.8% | Southern Europe (Spain, Italy, France), Eastern Europe (Poland, Romania) | Short term (≤ 2 years) |

| Higher prices limit low-income consumer access | -0.6% | Southern and Eastern Europe (Spain, Italy, Poland, Romania, Bulgaria) | Medium term (2-4 years) |

| Short shelf life of fresh organics | -0.4% | Pan-European, with acute impact in regions with fragmented cold-chain infrastructure | Medium term (2-4 years) |

| Post-Brexit UK trade barriers | -0.3% | UK and EU-27 cross-border trade corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Shortages from Weather Events and Limited Farmland

In 2024, extreme rainfall wreaked havoc on wheat and vegetable harvests in France, Germany, and Poland. This led to a year-over-year 12% drop in organic cereal availability, compelling processors to resort to non-US imports to fulfill their contracted volumes. In Western Europe, the conversion rates for organic farmland have hit a plateau. The prime parcels have already made the switch, leaving only marginal lands that yield less and incur higher input costs. This scenario deters new entrants, especially in the absence of direct subsidies. Thanks to co-financing from the US's Common Agricultural Policy, Poland saw an 8% increase in organic acreage in 2024. However, due to first-year yield penalties and knowledge gaps among newly converted farmers, the total output only rose by 4%. In 2024, a shortage of organic livestock feed drove up costs by 15 to 20%. This surge in expenses squeezed margins for organic dairy and meat producers, who found it challenging to pass the full cost increase onto their price-sensitive consumers in Southern and Eastern Europe, according to the European Trade data[2]Source: European Commission, “Trade Data 2024,” agriculture.ec.europa.eu.

Higher Prices Limit Low-Income Consumer Access

Organic products typically carry a premium of 30 to 50% compared to conventional alternatives in most European markets. This price disparity limits accessibility for households in the bottom two income quintiles, particularly in Spain, Italy, Poland, and Romania, where disposable incomes are lower than Western European averages. Inflation in 2024 and 2025 reduced real wages across Southern and Eastern Europe. Consequently, 28% of surveyed consumers either shifted from organic to conventional products or decreased their purchase frequency. This trend was especially evident in the fresh produce and dairy categories. Discount retailers Aldi and Lidl addressed this issue by introducing organic private labels priced 10 to 15% lower than branded options. However, these private labels still cost 20 to 30% more than conventional store brands, maintaining an affordability gap for low-income consumers. In 2024, government subsidy programs in France and Germany, designed to provide vouchers for organic produce to low-income families, reached only 12% of eligible households. Limited awareness and bureaucratic obstacles hindered the effectiveness of these programs, leaving structural demand challenges unresolved, according to the French Ministry of Agriculture[3]Source: French Ministry of Agriculture, “Organic Agriculture Programs,” agriculture.gouv.fr.

Segment Analysis

By Product Type: Functional Beverages Propel Faster Value Creation

Organic Beverages recorded a 6.78% CAGR outlook, well above the European organic food and beverages market average. Venture-backed players deploy probiotics and adaptogens that allow 40–60% mark-ups, and profitability gains appear as Oatly lowered per-liter costs 18% via regional oat sourcing. Direct-trade coffee and tea models pay farmers 20–30% premiums over Fair-Trade minima, aligning with ethically minded consumers and accelerating specialty-cafe demand. Within Organic Food, fruit and vegetables dominate volumes because of strong pesticide-avoidance associations, while meat, fish, and poultry remain niche at under 10% of sales due to limited certified capacity and steep premiums.

Value creation continues as dairy bifurcates. Organic milk volumes ease in core Western markets where plant alternatives capture younger cohorts, yet cheese and yogurt upgrade through probiotic credentials. Frozen and processed foods, aided by blast-freezing and retort solutions, extend reach to regions lacking sophisticated cold chains. Snack lines such as organic chocolate bars priced at USD 4–6 per 100 g reflect mid-single-digit growth yet demonstrate consumer acceptance of higher unit economics. Consequently, the Europe organic food and beverages market size expansion remains anchored by a diversified product pipeline.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Ambient-Stable Solutions Cut Waste And Boost Reach

Canned products are on track for a 7.18% CAGR, the fastest among form factors, because nitrogen-flush and retort sterilization push shelf life to 36 months without preservatives. Organic canned tomatoes and legumes win shelf space in discount chains that prize convenience and price stability. Frozen formats notch mid-single-digit gains as blast-freezing preserves nutrient content, serving food-service channels hungry for year-round consistency.

Fresh/Chilled organics still hold 67.75% of the European organic food and beverages market share, but 5–8-day shelf lives drive 30–40% retail waste. Supermarkets deploy dynamic pricing to clear near-expiry goods, protecting value though margin compression persists. Modified-atmosphere packaging adds two or three days of sell-through yet costs EUR 0.15-0.25 per pack, squeezing mid-tier labels. Subscription produce boxes boast 95% sell-through by synchronizing harvests with deliveries, but remain under 5% of Fresh/Chilled volume.

By Distribution Channel: Digital Commerce Accelerates Premium Recapture

Online Channels are set for a 6.85% CAGR as predictive inventory and same-day delivery facilitate premium-price purchases and furnish brands with first-party data. Amazon Fresh and Ocado added 25% more organic SKUs in 2024-2025, achieving sub-two-hour fulfillment in top urban ZIP codes. Direct-to-consumer models secure 40–50% gross margins, though EUR 30-50 acquisition costs per subscriber temper profitability.

Supermarkets and Hypermarkets still command 71.28% of the 2025 value, leveraging scale to undercut specialty stores by 10–15% on price, yet losing share to online and discount formats. Aldi and Lidl boosted organic SKU counts 30% and attracted 22% more category shoppers, albeit at gross margins 500–700 bps below branded equivalents. Convenience stores contribute less than 5% due to limited shelf space and high throughput requirements. Specialty stores maintain a 12–15% share by coupling deep assortments with staff expertise, even as rent pressure limits platform extension.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany’s 35.31% 2025 share underscores deep “Bio” culture, dense specialty networks, and purchasing power. Alnatura generated USD 1.3 billion in revenue in fiscal 2023-2024 at 25–30% gross margins, confirming specialty viability. Discount leaders extended private-label organics 30%, democratizing access yet compressing supplier margins. Growth moderates to low single digits as penetration tops 6.8% of food sales, but premiumization in infant formula and cold-pressed juice sustains value expansion. The UK diverged after Brexit as Certificate of Inspection protocols added three to five days to EU shipments, spurring domestic sourcing despite 10–15% cost premiums, which paradoxically strengthened local farm economics while fragmenting cross-border logistics.

Poland leads growth at a 7.11% CAGR, fueled by CAP subsidies and middle-class upgrades. Biedronka and Lidl raised organic SKU depth 25% in Warsaw and Krakow, turning certification into a health and status marker. Acreage expanded 8% in 2024, yet yield drag held output growth to 4%, creating pricing tension that nonetheless sustains farmer economics. France, Italy, and Spain collectively command nearly 30% share thanks to Mediterranean crop suitability, yet affordability headwinds triggered partial consumer trade-down during the 2024-2025 inflation spike.

Netherlands and Belgium outperform on per-capita spend because Rotterdam enables efficient re-exports and public institutions mandate 30% organic content in school meals, respectively. Russia lags at under 1% penetration due to sparse certification infrastructure, though affluent Moscow households provide niche demand. Rest of Europe, including Scandinavia and the Balkans, grows 6–8% as accession candidates mirror EU standards to unlock subsidy flows.

Competitive Landscape

High concentration defines the Europe organic food and beverages market, rated 8/10 on the concentration scale. Danone, Nestlé, and Arla Foods leverage regenerative farming contracts that secure volumes and open carbon-credit monetization. Danone targeted 50,000 farms for outcome-based programs by 2030, creating a durable feedstock hedge DANONE.COM. Nestlé deploys blockchain for traceability in organic baby food and plant-based lines, allowing 30–40% premiums.

Oatly and Veganz exploit direct-to-consumer channels, functional claims, and regionally sourced inputs to resonate with millennials, with Oatly reaching profitability after an 18% cost reduction. Private-equity shops chase mid-tier brands with USD 50-200 million in revenue, treating certified supply chains as inflation-proof assets. Aldi and Lidl disrupt from below with private-label organics at mid-tier conventional prices, compressing supplier margins by 3–5 points.

Specialty retailers defend share through curated ranges and staff storytelling, yet online giants erode traffic by matching assortment and adding delivery convenience. Innovation focuses on traceability tech, with 40% of surveyed brands deploying IoT sensors and blockchain for cold-chain proof points. White-space frontiers include organic aquaculture, insect protein, and cellular agriculture, areas still nascent in regulation and ripe for early movers.

Europe Organic Food And Beverages Industry Leaders

General Mills, Inc.

Nestlé S.A.

Danone S.A.

Amy's Kitchen, Inc.

The Hain Celestial Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Better Nature debuted Peri Peri Tempeh in Tesco stores, targeting meat-eaters with a high-protein plant-based chicken alternative. The product claims to be organic and delivers 44 g of protein.

- May 2025: Rude Health debuted the UK's first organic, dairy-free iced coffee range, featuring Oat Latte Iced Coffee and Mocha Iced Coffee, which are now available at Waitrose and Ocado. Made with cold-brew organic Arabica beans from Latin American farms, organic oat milk (Oat Latte), and coconut milk/cacao.

- March 2025: Yeo Valley Organic, the UK's largest organic brand known for dairy, launched its first meat product—100% British free-range organic grass-fed beef burgers in 362 Tesco stores. The products are made from grass-fed beef for superior taste and nutrition.

Europe Organic Food And Beverages Market Report Scope

Europe's organic food & beverages market is segmented by product type, distribution channel, and geography. Based on product type, the market has been segmented by organic food and organic beverages. The organic food segment is further classified into organic fruit & vegetables, organic meat, fish & poultry, organic dairy products, organic frozen & processed foods, and others. The organic beverage segment is further classified into alcoholic and non-alcoholic beverages. Based on the distribution channel, the market has been segmented into supermarkets/hypermarkets, convenience stores, specialist stores, online retailing, and other distribution channels. Based on geography, the report offers a detailed regional analysis, which includes the United Kingdom, France, Germany, Italy, Russia, Spain, and the Rest of Europe. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

Product Type

| Organic Food | Fruit and Vegetables |

| Meat, Fish and Poultry | |

| Dairy Products | |

| Frozen and Processed Foods | |

| Other Foods | |

| Organic Beverages | Fruit and Vegetable Juices |

| Dairy-based | |

| Coffee | |

| Tea | |

| Other Beverages |

By Form

| Fresh/Chilled |

| Canned |

| Frozen |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Belgium |

| Poland |

| Rest of Europe |

| Product Type | Organic Food | Fruit and Vegetables |

| Meat, Fish and Poultry | ||

| Dairy Products | ||

| Frozen and Processed Foods | ||

| Other Foods | ||

| Organic Beverages | Fruit and Vegetable Juices | |

| Dairy-based | ||

| Coffee | ||

| Tea | ||

| Other Beverages | ||

| By Form | Fresh/Chilled | |

| Canned | ||

| Frozen | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe organic food and beverages market?

The market is valued at USD 75.28 billion in 2026 and is forecast to reach USD 85.91 billion by 2031.

Which product category is growing faster, Organic Food or Organic Beverages?

Organic Beverages are projected to grow at a 6.78% CAGR through 2031, outpacing Organic Food.

Which form factor is expanding most rapidly?

Canned organics are forecast to rise at a 7.18% CAGR as shelf-life technologies improve.

Which country leads regional sales and which is the fastest growing?

Germany leads with 35.31% of 2025 value, while Poland is the fastest expanding at a 7.11% CAGR to 2031.