Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

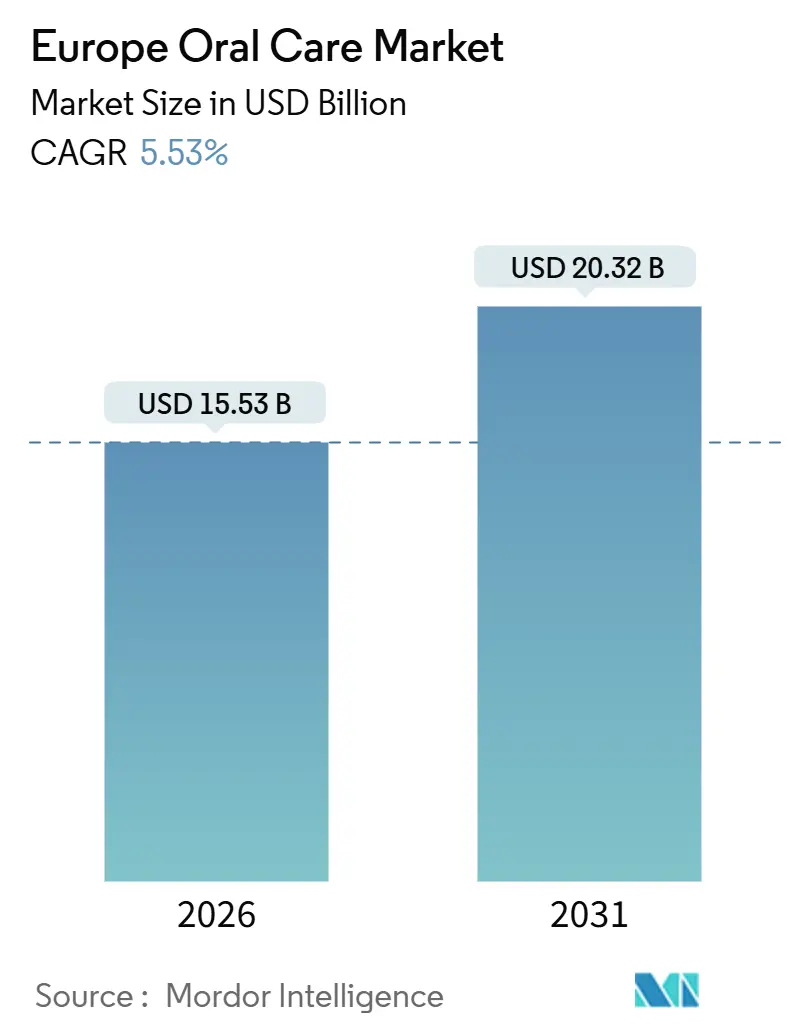

| Market Size (2026) | USD 15.53 Billion |

| Market Size (2031) | USD 20.32 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

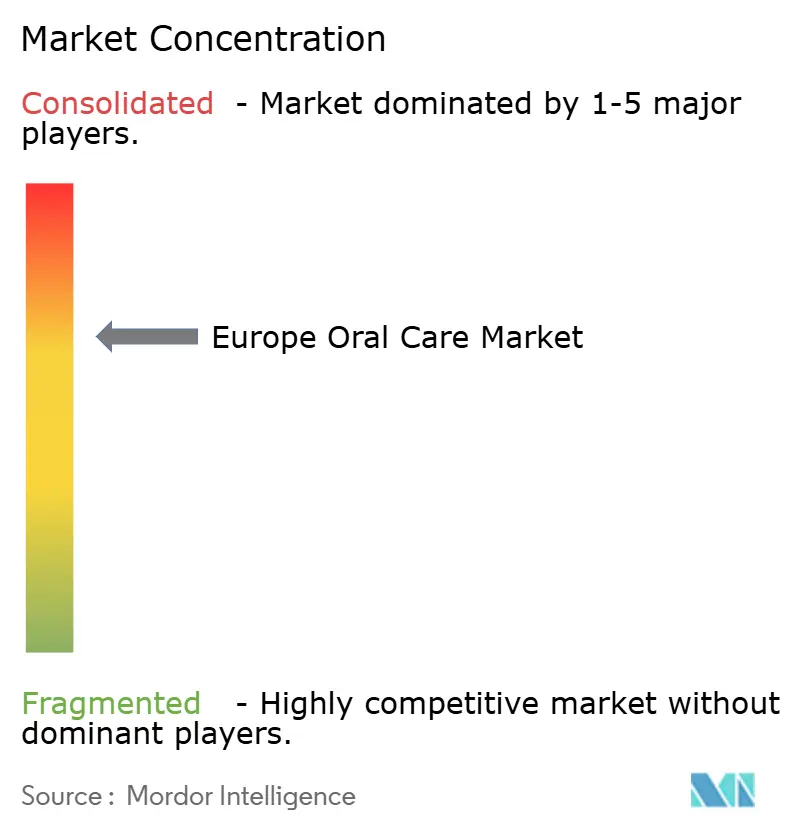

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Oral Care Market Analysis by Mordor Intelligence

The Europe oral care market size is estimated at USD 15.53 billion in 2026, and is expected to reach USD 20.32 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). This trajectory reflects a confluence of demographic shifts, regulatory momentum, and technology-led product innovation that distinguishes Europe from other mature markets. The region's aging profile, with individuals aged 65 and above comprising 21.6% of the EU population in 2024 and projected to climb to 32.5% by 2100, creates sustained demand for specialized dental care formulations addressing gum recession, sensitivity, and restorative needs. Concurrently, national health systems are embedding preventive oral hygiene into primary care protocols, a strategic pivot that elevates routine product usage beyond cosmetic concerns. Clean-label reformulations, such as titanium-dioxide-free pastes and bamboo-based brushes, are expanding shelf space as retailers tighten sustainability scorecards. At the same time, anti-dumping tariffs on Chinese erythritol and stricter counterfeit enforcement raise cost and compliance hurdles that favor companies with diversified supply chains.

Key Report Takeaways

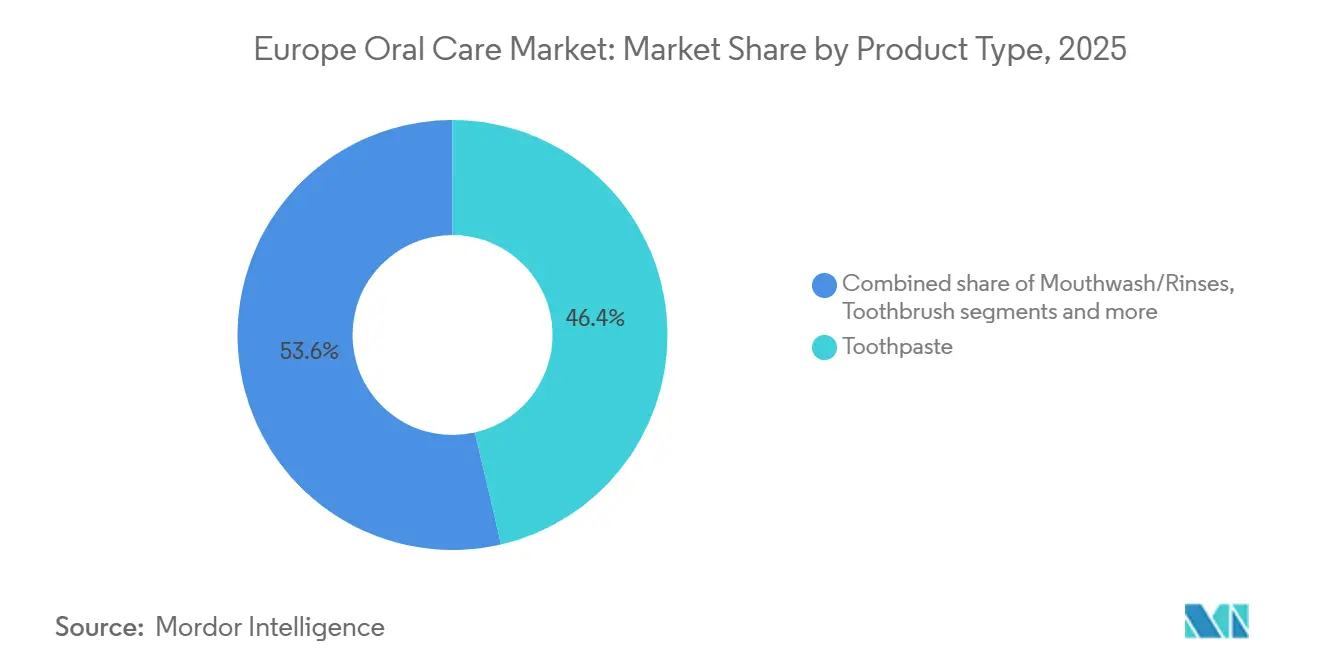

- By product type, toothpaste led with 46.38% of oral care market share in 2025, while mouthwash/rinses are forecast to expand at a 5.97% CAGR through 2031.

- By category, conventional and synthetic lines accounted for 89.47% of revenue in 2025; natural and organic products represent the fastest trajectory at a 6.35% CAGR to 2031.

- By end-user, adults dominated with 93.71% volume in 2025, yet the kids segment is pacing ahead at a 7.36% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 36.59% value in 2025, whereas online stores are advancing at a 6.87% CAGR to 2031.

- By geography, Germany contributed 16.81% of the 2025 value; Spain is projected to post the highest national growth at a 7.66% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Oral Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and organic toothpaste | +0.9% | Western Europe, particularly Germany, United Kingdom, France | Medium term (3-4 years) |

| Increase consumer focus on oral hygiene | +1.2% | Pan-European, with stronger impact in Northern Europe | Long term (≥ 5 years) |

| Integration of smart technologies in electric toothbrush | +0.7% | Western and Northern Europe | Medium term (3-4 years) |

| Favorable government initiatives on oral-hygiene | +0.8% | United Kingdom, France, Nordic countries, Eastern Europe | Long term (≥ 5 years) |

| Aging population and dental health needs | +1.1% | Pan-European, with highest impact in Germany, Italy, Nordic countries | Long term (≥ 5 years) |

| Rising disposable income and healthcare spending | +0.8% | Eastern Europe, Southern Europe | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural and Organic Toothpaste

Clean-label formulations free from synthetic surfactants, artificial sweeteners, and microplastics are reshaping procurement strategies across European retail chains. Conventional sodium lauryl sulfate is yielding to coconut-derived surfactants, while titanium dioxide, banned in food applications under EU Regulation 2022/63, faces voluntary phase-outs in oral care despite remaining legally permissible. The Humble Co. expanded its bamboo toothbrush and natural toothpaste tablet range in 2024, securing listings in Carrefour and Tesco that previously reserved shelf space for multinational brands. Denttabs introduced fluoride-infused toothpaste tablets in 2024, addressing a long-standing criticism that tablet formats compromised caries prevention, and the product achieved ISO 11609 compliance for abrasivity, signaling readiness for clinical endorsement. This shift is not purely consumer-driven; procurement officers at hospital trusts and care homes are embedding sustainability criteria into tender specifications, favoring suppliers with Cradle to Cradle or EU Ecolabel certifications that verify biodegradable packaging and ethically sourced actives.

Increase Consumer Focus on Oral Hygiene

European consumers are actively prioritizing oral hygiene, which drives growth in the oral care market. They recognize that good oral health directly affects cardiovascular health, diabetes management, and respiratory well-being. This understanding has transformed oral care from a simple daily routine into a crucial health practice. Older adults, who experience more dental problems, actively seek advanced oral care products and follow thorough hygiene routines. According to the OECD, the population aged 65 and older will grow from 21% in 2023 to 30% by 2050 [1]Source: Organisation for Economic Co-operation and Development (OECD), "Health at a Glance: Europe 2024", oecd.org. This aging population actively shapes the oral care market by demanding specific products. They need specialized items like dry mouth toothpaste, anti-gum disease mouthwashes, and denture care solutions. Their requirements for targeted oral health products drive companies to develop new solutions and expand the specialized oral care market.

Integration of Smart Technologies in Electric Toothbrush

AI-guided brushing feedback and pressure sensors are transitioning electric toothbrushes from convenience tools to diagnostic devices. Philips launched the Sonicare 9900 Prestige in 2024, featuring SenseIQ technology that adjusts intensity in real time based on gum sensitivity and plaque density, and the companion app generates personalized brushing maps that users can share with dental professionals during telemedicine consultations. Procter & Gamble's Oral-B iO Series 10, introduced in 2024, incorporates a color touchscreen and magnetic charging that reduces cord clutter, addressing a friction point in bathroom ergonomics, while its AI algorithm tracks 16 zones of the mouth and flags areas of chronic neglect, creating a feedback loop that improves technique adherence by 34% according to a 2024 clinical trial published in the Journal of Clinical Dentistry. Oclean, a challenger brand, entered European markets in 2024 with a subscription model priced 40% below incumbents, bundling brush heads and toothpaste refills with cloud-stored brushing analytics, a strategy that appeals to cost-conscious millennials who prioritize data portability over brand heritage. These innovations are converging with dental insurance telematics pilots in the Netherlands and Sweden, where insurers offer premium discounts to policyholders who share brushing data, mirroring usage-based models in auto insurance.

Favorable Government Initiatives on Oral Hygiene

European governments actively transform their oral healthcare programs by moving beyond basic awareness campaigns to create comprehensive healthcare policies. The United Kingdom actively implemented the NHS Dental Recovery Plan since February 2024, which focuses on prevention through the 'Smile for Life' program and strategically places dental professionals in schools across underserved regions [2]Source: National Health Service (NHS), "SMILE4LIFE", england.nhs.uk. Additionally, Romania takes action through its 'National Oral Health Improvement Campaign (2025-2030)' to actively address and reduce gaps in oral healthcare access. The World Health Organization's global oral health assembly in November 2024 actively drives the agenda for universal oral healthcare coverage by 2030, which motivates European countries to develop detailed implementation strategies. These policy changes actively create new opportunities in the market for educational materials and specialized products that support public health initiatives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of traditional way of tooth cleaning | -0.6% | Eastern Europe, Rural areas across Europe | Short term (≤ 2 years) |

| Counterfeit products affecting brand reputation | -0.8% | Eastern Europe, Online channels | Medium term (3-4 years) |

| Raw material price fluctuations | -0.5% | Pan-European, with higher impact on cost-sensitive segments | Short term (≤ 2 years) |

| Regulatory compliance requirements | -0.4% | Pan-European, particularly affecting smaller manufacturers | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Traditional Way of Tooth Cleaning

European consumers largely stick to traditional oral care methods, which restricts the growth of advanced oral care products in the region. Many people continue to use manual toothbrushes and basic toothpaste due to cost concerns, lack of awareness about newer products, and limited access to dental education. This behavior is especially common among the elderly and rural populations. Most consumers treat oral care as a simple daily task and believe brushing twice a day with manual tools meets their needs, even when dentists recommend modern alternatives. Lower-income regions in Central and Eastern Europe show minimal adoption of electric toothbrushes, interdental cleaning tools, and therapeutic products. This low adoption directly impacts sales of innovative oral hygiene products.

Counterfeit Products Affecting Brand Reputation

The European Union Intellectual Property Office documented EUR 3 billion in lost sales across cosmetics and personal care in 2024, translating to 32,000 displaced jobs and EUR 1.2 billion in foregone tax revenue. Counterfeit Colgate toothpaste seized at Rotterdam port in 2024 contained diethylene glycol, a toxic adulterant linked to renal failure, prompting the European Commission to mandate serialized QR codes on all oral care products sold through online marketplaces by January 2026. This enforcement gap is widening as third-party sellers on Amazon and eBay exploit jurisdictional ambiguities, listing products with authentic branding but fulfilling orders from non-EU warehouses that evade customs inspections. Brand owners are deploying blockchain-based provenance tracking and consumer-facing authentication apps, yet adoption remains below 15% among target demographics, limiting the deterrent effect. The reputational damage extends beyond immediate health risks; a 2024 survey by the European Consumer Organisation found that 28% of respondents who unknowingly purchased counterfeit oral care products subsequently switched to private-label alternatives, perceiving branded goods as overpriced and inadequately protected.

Segment Analysis

By Product Type: Mouthwash Gains as Therapeutic Formulations Mature

Toothpaste held a 46.38% share in 2025, reflecting its entrenched position as the primary vehicle for fluoride delivery and daily plaque control, yet mouthwash and rinses are expanding at a 5.97% CAGR through 2031, the fastest pace among product categories. This acceleration stems from the commercialization of alcohol-free, microbiome-preserving formulations that address growing consumer and clinical concerns about antimicrobial resistance and oral dysbiosis. Haleon introduced Parodontax Active Gum Health mouthwash in 2024, incorporating stannous fluoride and cetylpyridinium chloride to target bleeding gums, a formulation that secured reimbursement approval under Germany's statutory health insurance for patients with diagnosed periodontitis. Toothbrushes, encompassing both manual and electric variants, are growing at a moderate pace as smart features command premium pricing but remain confined to affluent urban segments. Other product types, interdental brushes, tongue scrapers, and dental floss, serve niche roles yet collectively contribute incremental volume as dentists prescribe them for post-surgical care and orthodontic maintenance.

Mouthwash's trajectory is further amplified by its compatibility with telemedicine workflows; remote consultations during the COVID-19 pandemic normalized virtual prescriptions for therapeutic rinses, a practice that persists as health systems seek to reduce in-person visit loads. Toothpaste innovation is shifting toward delivery mechanisms, microencapsulated whitening agents, and enzyme-enhanced biofilm disruption that extend efficacy beyond the 2-minute brushing window, yet regulatory inertia slows commercialization as the EU Cosmetics Regulation requires manufacturers to demonstrate safety and efficacy for novel actives through multi-year clinical trials. Toothbrushes are bifurcating into ultra-low-cost manual variants for public procurement and high-tech electric models that integrate with smartphone apps, leaving mid-priced manual brushes in a margin squeeze. The segment's evolution underscores a broader pattern: products that enable measurable health outcomes and align with digital health ecosystems are capturing disproportionate growth, while undifferentiated commodity offerings face pricing pressure from private-label competition.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Natural and Organic Formulations Disrupt Conventional Dominance

Conventional and synthetic products commanded an 89.47% share in 2025, sustained by their cost efficiency, established clinical evidence, and compatibility with mass-production infrastructure, yet natural and organic alternatives are accelerating at a 6.35% CAGR through 2031, driven by regulatory tailwinds and shifting procurement criteria. The EU's ban on titanium dioxide in food applications, codified in Regulation 2022/63, created a halo effect that pressured oral care brands to voluntarily reformulate despite the ingredient's continued legality in cosmetics, with Unilever's Zendium Complete Protection, launched in 2024, eliminating synthetic colorants and preservatives in favor of natural enzymes, amyloglucosidase, glucose oxidase, lactoperoxidase, that mimic saliva's antimicrobial properties.

The European Medicines Agency has approved multiple naturally derived active ingredients for therapeutic oral care products, enabling natural formulations with validated health claims. The WHO's 2024 report on environmental determinants of health emphasizes reducing chemical exposure through personal care products, including oral care, and providing policy support for natural alternatives. The sales value of organic health and beauty products, including oral care, in the United Kingdom increased in 2023, according to the Soil Association [3]Source: Soil Association, “The Organic Beauty and Wellbeing Market 2024”, soilassociation.org. The demand for natural and organic oral care products has grown, driven by scientific research validation and regulatory compliance. Consumers are prioritizing oral care products that combine effectiveness with safety and environmental sustainability.

By Distribution Channel: Digital Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets captured 36.59% of distribution in 2025, leveraging their ubiquity, impulse-purchase dynamics, and ability to cross-promote oral care with adjacent categories such as cosmetics and over-the-counter pharmaceuticals, yet online stores are expanding at 6.87% CAGR through 2031, driven by subscription models and direct-to-consumer strategies that bypass traditional retail mark-ups. Philips launched a subscription service for Sonicare brush heads and toothpaste in 2024, offering 20% discounts and free shipping for quarterly deliveries, a model that locks in recurring revenue and reduces customer acquisition costs by 35% compared to transactional sales. Drug stores and pharmacies retain advantages in therapeutic segments where pharmacists recommend prescription-strength formulations and insurance reimbursement requires point-of-sale verification, yet their share is eroding as telemedicine platforms enable remote prescriptions that patients fulfill via online pharmacies.

Other distribution channels, dental clinics, direct sales, and vending machines, serve niche roles yet collectively contribute incremental volume. Dental clinics in Germany and the Netherlands stock professional-grade products that patients purchase post-consultation, a channel that generates high-margin sales yet remains capacity-constrained by appointment availability. E-commerce's ascent is not without friction; counterfeit products proliferate on third-party marketplaces, prompting the European Commission to mandate serialized QR codes by January 2026, and last-mile delivery costs inflate prices for low-value items such as toothpaste, limiting online shopping's appeal for price-sensitive shoppers. The channel's evolution is also shaped by retailer consolidation; Carrefour's acquisition of Cora's French hypermarkets in 2024 concentrated buying power, enabling the chain to negotiate exclusive SKUs and promotional windows that smaller competitors cannot match, a dynamic that favors multinational brands with the scale to support customized product runs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Adult Segment Dominates While Children's Market Accelerates

Adults represented 93.71% of end-user volume in 2025, reflecting their higher per-capita consumption and willingness to pay for premium formulations addressing sensitivity, whitening, and gum health, yet the kids and children segment is expanding at 7.36% CAGR through 2031, propelled by gamified digital tools and fluoride-optimized formulations that convert parental compliance into habitual behavior. Adults demonstrate increased awareness of oral health's connection to overall health and invest in specialized oral hygiene products, including therapeutic toothpaste, electric toothbrushes, whitening systems, and mouthwashes. These products address specific concerns such as gum disease, enamel erosion, and tooth sensitivity. The segment's growth is further supported by lifestyle factors, including tobacco use, dietary habits, and stress, which necessitate consistent use of advanced oral care products.

The kids/children segment growth is driven by increased parental awareness about early oral hygiene habits, enhanced pediatric dental education, and public health initiatives across Europe. The market has responded with child-oriented products featuring attractive flavors, packaging, and designs, improving product adoption among children. Government initiatives further support this growth, as demonstrated by the United Kingdom's 'Smile for Life' program in 2024, which promotes oral health from infancy through school age through education, preventive care, and access to age-appropriate dental products.

Geography Analysis

Germany held a 16.81% share in 2025, underpinned by a dense network of 80,000 practicing dentists and a cultural norm where 60% of adults attend biannual check-ups, sustaining premium demand for sensitivity-relief and whitening formulations that dental professionals recommend during consultations. Spain is poised to grow at 7.66% CAGR through 2031, the fastest pace among major geographies, fueled by the Ministry of Health's 2024-2030 oral health strategy that allocated EUR 120 million to preventive care, including subsidized fluoride treatments for low-income children and mobile dental clinics for rural municipalities. France and Italy exhibit divergent dynamics: France's 100% Santé scheme expanded in 2024 to cover annual scaling and polishing for adults over 50, driving volume uptake of therapeutic mouthwashes, while Italy's fragmented regional health systems create procurement inefficiencies that favor local brands over multinational entrants.

The United Kingdom is navigating post-Brexit regulatory divergence as the Medicines and Healthcare products Regulatory Agency (MHRA) establishes independent approval pathways for novel actives, a shift that could accelerate time-to-market for innovative formulations yet requires manufacturers to duplicate clinical trials conducted under EU frameworks. Poland and Belgium are experiencing rapid growth as rising disposable incomes and EU4Health funding expand access to preventive care; Poland's Ministry of Health launched a school-based fluoride varnish program in 2024, mirroring Ireland's Smile agus Sláinte initiative, while Belgium's integration of oral health screenings into primary care is driving demand for pediatric formulations. The Rest of Europe category, encompassing smaller markets such as Austria, Denmark, and Portugal, collectively represents 15% to 18% of volume, with growth trajectories shaped by localized regulatory frameworks and varying levels of public health investment.

Regional variations in consumer preferences are pronounced; German consumers prioritize clinical efficacy and dentist endorsements, sustaining demand for therapeutic formulations, while Spanish and Italian shoppers exhibit a stronger affinity for natural and organic products, reflected in the rapid expansion of brands such as The Humble Co. and Denttabs in those markets. The UK's post-Brexit regulatory environment is creating arbitrage opportunities for manufacturers who can navigate dual approval pathways, yet the administrative burden is deterring smaller firms from launching in the market. Nordic countries are at the forefront of digital health integration, with Sweden's Folktandvården (public dental service) piloting AI-guided brushing apps that sync with patient records, a model that other EU member states are evaluating for adoption. Eastern European markets such as Poland are witnessing premiumization as middle-class expansion drives demand for electric toothbrushes and whitening formulations, yet price sensitivity remains acute, favoring value-oriented brands and private-label alternatives.

Competitive Landscape

The European oral care market demonstrates moderate consolidation, characterized by the dominant presence of multinational corporations including Colgate-Palmolive, Procter & Gamble, Haleon PLC, and Unilever. These corporations maintain significant market positions through established product portfolios and extensive distribution networks. The competitive environment has evolved with the emergence of specialized firms focusing on sustainability initiatives, which have successfully penetrated specific market segments. Large companies are acquiring innovative businesses to access new technologies and expand into emerging markets, while maintaining significant investment in internal research and development. This approach helps them remain competitive, develop new products, and grow their market share in expanding segments.

Strategic market opportunities predominantly exist at the convergence of technological innovation and natural formulation development, particularly in the advancement of personalized oral care solutions based on oral microbiome analysis. The competitive dynamics are increasingly influenced by artificial intelligence integration across product development and consumer engagement frameworks. Emerging disruptors are exploiting incumbents' sluggish response to sustainability mandates and digital health integration. The Humble Co. expanded its bamboo toothbrush and natural toothpaste tablet range into France and Spain in 2024, leveraging Cradle to Cradle certification to meet public procurement criteria in Paris and Barcelona, markets where multinational brands lack equivalent credentials. TePe introduced the TePe GOOD toothbrush in 2024, manufactured from bio-based plastics derived from Swedish pine resin, a formulation that secured endorsement from the Swedish Dental Association and is gaining traction in Nordic markets where environmental certifications influence purchasing decisions.

Technology deployment is bifurcating the market; high-income segments adopt AI-guided electric toothbrushes with subscription refills, while price-sensitive cohorts gravitate toward private-label manual brushes sold through discount retailers such as Lidl and Aldi. Consolidation is accelerating as mid-tier brands exit or accept acquisition offers; Haleon's 2022 spin-off from GSK and Kenvue's 2023 separation from Johnson & Johnson created standalone entities with dedicated oral care mandates, yet both face integration costs and portfolio rationalization that temporarily constrain innovation budgets. The competitive landscape is further shaped by the EU Cosmetics Regulation's reformulation mandates, which favor incumbents with in-house R&D capabilities and clinical trial infrastructure over smaller firms that rely on contract manufacturers.

Europe Oral Care Industry Leaders

-

Colgate-Palmolive Company

-

Procter & Gamble Company

-

Unilever PLC

-

Haleon PLC

-

Kenvue, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Oral-B introduced the iO Series 2 (iO2), expanding its iO technology product line. The company developed the Oral-B iO2 as an entry-level model, specifically targeting manual toothbrush users.

- June 2024: Corsodyl introduced its Gum Strength & Protect product line, comprising two toothpastes and a daily mouthwash, which demonstrated clinical efficacy in preventing gum problems.

- January 2024: Sensodyne introduced its premium Clinical White range, featuring advanced whitening technology. The product line is scientifically proven to whiten teeth by two shades while providing continuous protection for sensitive teeth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European oral care market as retail and professional sales of toothpaste, toothbrushes, mouthwashes/rinses, denture products, dental accessories (floss, picks, whitening strips, tongue cleaners), and related natural or medicated formulations purchased by households and dental offices across 27 EU members, the U.K., Norway, Switzerland, and Russia.

Scope Exclusions: products sold only to dental laboratories, injectable periodontal therapeutics, and purely aesthetic in-clinic procedures are outside this estimate.

Segmentation Overview

-

Product Type

- Toothpaste

- Mouthwash/Rinses

- Toothbrush

- Other Product Types

-

Category

- Natural/Organic

- Conventional/Synthetic

-

End-User

- Kids/Children

- Adult

-

Distribution Channel

- Supermarkets/Hypermarkets

- Drug Stores/Pharmacies

- Online Stores

- Other Distribution Channels

-

Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with dentists, hygienists, procurement heads at pharmacy chains, and e-commerce category managers across Germany, Spain, the U.K., and the Nordics refined channel splits, average selling prices, and likely adoption of smart brushes. Short consumer pulse surveys helped us align per-capita paste usage and flavor preferences with real-world behavior that desk work cannot expose.

Desk Research

We began with open datasets such as Eurostat trade codes for HS 3306 articles, WHO European Health Information Gateway on caries prevalence, OECD aging population series, and European Dental Association shipment surveys, which frame demand pools. Additional inputs came from company 10-Ks, retailer scans, patent abstracts via Questel, and news screening on Dow Jones Factiva that flags new launches and price shifts. Customs dashboards like Volza and regulation trackers from the European Chemicals Agency helped us validate cross-border flows and fluoride limits. The sources listed are illustrative; many more public and subscription channels were reviewed for corroboration and clarification.

Two Mordor analysts also tap paid repositories, D&B Hoovers for manufacturer revenues and Marklines for electric toothbrush component costs, to strengthen brand-level signals before modeling.

Market-Sizing & Forecasting

A top-down build begins with 2024 retail and professional sales reconstructed from production plus net imports, then reconciled to consumption through average price and usage checks. Selective supplier roll-ups and online channel audits provide a bottom-up cross-check. We feed multivariate regression models with six fingerprints: per-capita toothpaste consumption, 65+ population share, e-commerce penetration in fast-moving consumer goods, average fluoride limit changes, disposable income growth, and unit price of electric brush heads to forecast demand. Gaps where company disclosures are silent are bridged with channel mark-up benchmarks validated in expert calls.

Data Validation & Update Cycle

Outputs move through anomaly screens, senior-junior peer reviews, and variance checks against independent macro and shipment series. Reports refresh every twelve months, with interim updates triggered by material events such as VAT changes or a major recall, and each release undergoes a fresh analyst pass before client delivery.

Why Mordor's Europe Oral Care Baseline Commands Reliability

Published figures often diverge because firms choose different product baskets, country sets, and price assumptions.

Key gap drivers include: some studies exclude accessories, others sample only five core economies, and a few index prices on ex-factory values, while Mordor Intelligence models end-user spend and updates currencies quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.78 B (2025) | Mordor Intelligence | - |

| USD 7.63 B (2024) | Regional Consultancy A | Limited to toothpaste and toothbrush; five countries only |

| USD 11.57 B (2024) | Global Consultancy B | Uses ex-factory prices; accessories excluded |

| USD 10.00 B (2024) | Trade Journal C | Forecasts stop at 2034; smart-brush segment omitted |

These contrasts show that Mordor's disciplined scope, variable selection, and annual refresh cadence deliver a balanced, transparent baseline clients can replicate with clear steps and trusted inputs.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Europe’s oral care market in 2026 and what CAGR is expected through 2031?

The oral care market size was USD 15.53 billion in 2026 and is forecast to grow at a 5.53% CAGR, reaching USD 20.32 billion by 2031.

Which product type is expanding fastest in Europe?

Mouthwash and rinses lead growth with a 5.97% CAGR thanks to alcohol-free, microbiome-friendly formulas approved for therapeutic use.

Why is Spain projected to outpace other countries?

Spain’s oral health plan subsidizes fluoride treatments and mobile clinics, lifting access for children and rural residents and driving a 7.66% CAGR.

What is driving demand for natural and organic toothpaste?

Retail sustainability mandates and consumer avoidance of synthetic surfactants have moved clean-label pastes into mainstream channels, posting a 6.35% CAGR.