Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

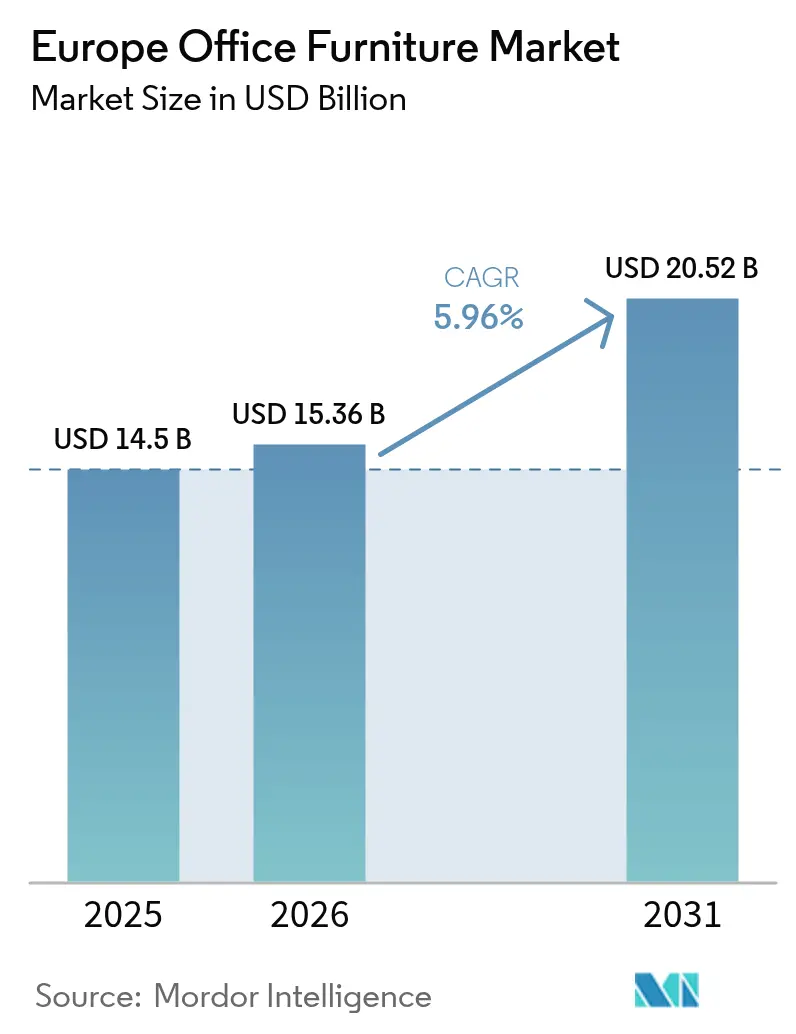

| Base Year Market Size (2025) | USD 14.50 Billion |

| Market Size (2026) | USD 15.36 Billion |

| Market Size (2031) | USD 20.52 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Office Furniture Market Analysis by Mordor Intelligence

The Europe office furniture market size is expected to grow from USD 14.50 billion in 2025 to USD 15.36 billion in 2026 and is forecast to reach USD 20.52 billion by 2031 at 5.96% CAGR over 2026-2031. Current growth is fuelled by organizations that are redesigning spaces to support hybrid work, mandating more ergonomic seating, and favouring modular configurations that can be re-used or re-sold to meet circularity targets. Companies are also responding to environmental, social, and governance benchmarks by insisting on in-house take-back programs and guaranteed recycled content, while EU ergonomics standards are pushing seating upgrades across every major geography. Supply-chain resilience has become another priority because spot prices for timber rose 30% and steel 25% in 2024, prompting firms with diversified sourcing to outperform those relying on single suppliers. Competitive advantages now revolve around full-service lifecycle offerings, sensor-enabled products that track utilization, and premium aesthetics that help employers stand out in tight labour markets. The Europe office furniture market consequently remains a bellwether for how corporate real-estate strategies, regulatory requirements, and sustainability goals converge in physical workspace investments.

Key Report Takeaways

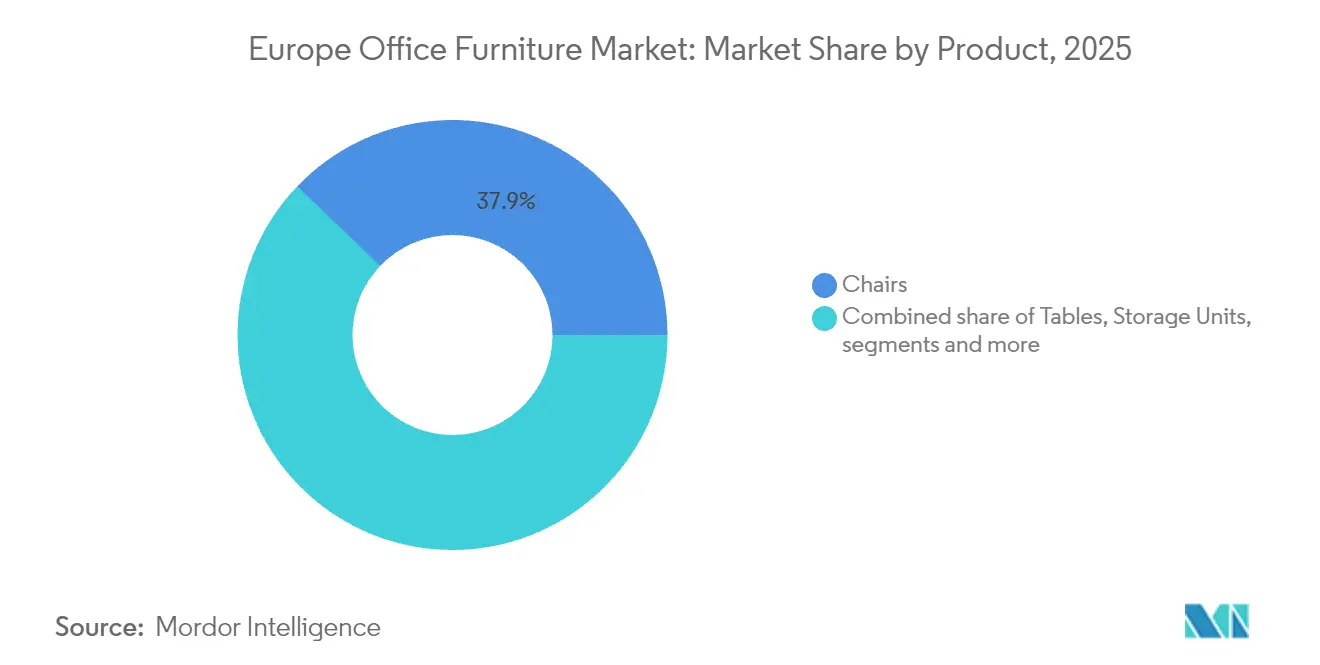

- By product, chairs accounted for 37.85% of the Europe office furniture market share in 2025, while booths and office dividers are projected to post the fastest 6.55% CAGR through 2031.

- By material, wood captured 45.20% of the Europe office furniture market size in 2025; plastics and polymers will expand at a 6.39% CAGR through 2031 as recycled content gains traction.

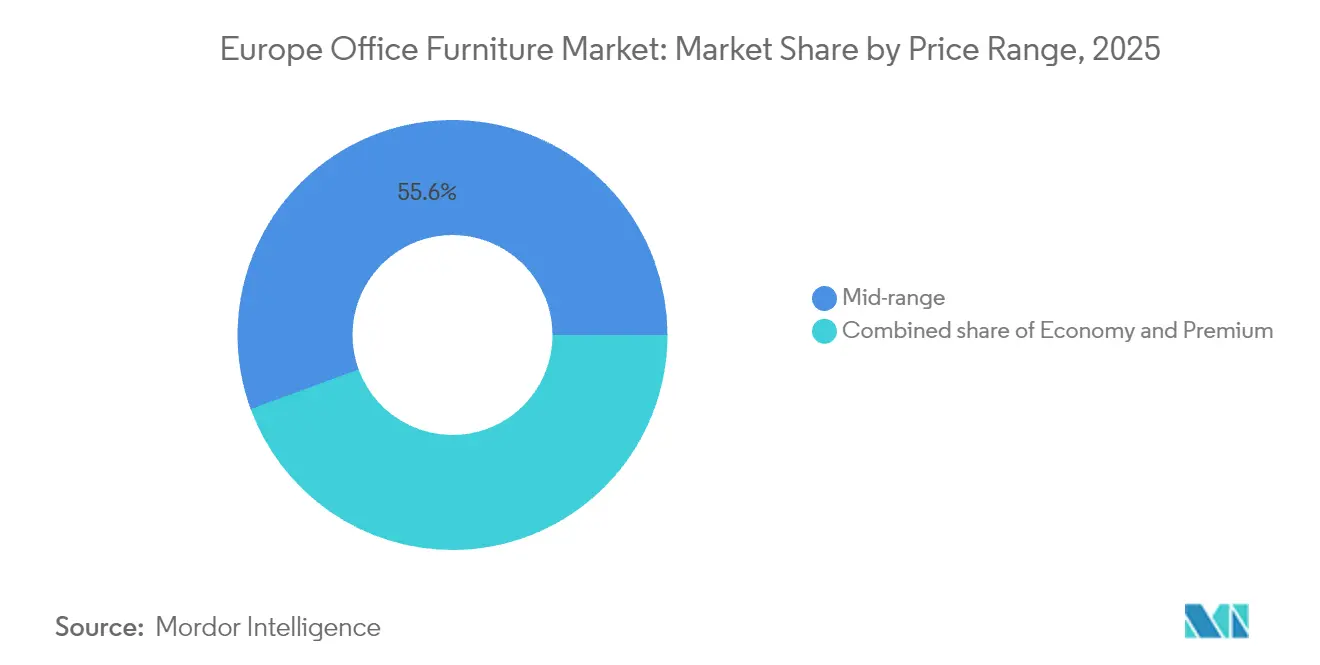

- By price range, mid-range captured 55.60% of the Europe office furniture market size in 2025, but the premium tier is slated to grow 6.81% per year and surpass the market average as employers prioritize higher-spec solutions.

- By end-user, corporate offices held 61.35% of the Europe office furniture market size in 2025, whereas healthcare offices will advance at a 7.24% CAGR on the back of modernization and infection-control requirements.

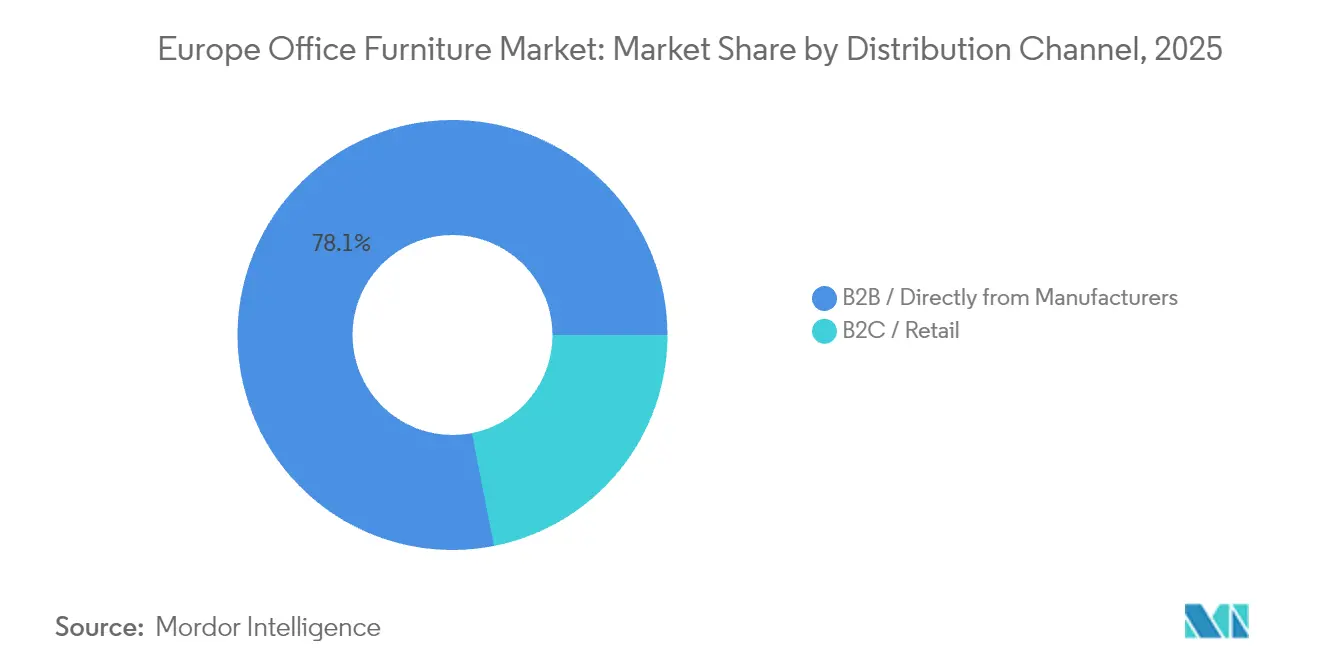

- By distribution channel, B2B direct sales commanded 78.10% of the Europe office furniture market size in 2025 and will accelerate at a 7.55% CAGR because manufacturers use the channel to capture margin and deepen client relationships.

- By geography, Germany maintained a 20.30% of the Europe office furniture market size in 2025, yet Spain is projected to log a 7.73% CAGR to 2031 due to robust construction and professional-services expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic hybrid-work boom sustaining replacement cycle | +1.2% | Global, with strongest impact in Germany, the United Kingdom, France | Medium term (2-4 years) |

| Corporate ESG mandates fuelling demand for circular & recycled furniture | +0.8% | EU-wide, particularly Nordic and Benelux regions | Long term (≥ 4 years) |

| Stricter EU ergonomics directives (EN 1335-1:2020) accelerating ergonomic seating adoption | +0.7% | EU-wide regulatory compliance requirement | Short term (≤ 2 years) |

| Premiumisation of workspace aesthetics to attract talent in tight labour markets | +0.9% | Major European business centres, strongest in Germany, the United Kingdom | Medium term (2-4 years) |

| AI-driven mass-custom design platforms reducing lead-times & inventory risk | +0.4% | Technology-forward markets: Germany, Netherlands, Nordic | Long term (≥ 4 years) |

| Smart-sensor-embedded desks & chairs enabling workplace analytics spend | +0.3% | Early adopters in Germany, the United Kingdom, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic hybrid-work boom sustaining replacement cycle

Corporate shifts to flexible attendance models have lengthened daily seat-rotation patterns and reduced total fixed desks, yet the same shift is prolonging replacement cycles for modular furniture that accommodates more users per seat[1]K2 Space, “Office Design Trends 2024,” k2space.co.uk. . Companies are introducing height-adjustable desks, mobile cabinets, and tool-free reconfiguration systems to align seating density with fluctuating occupancy. Utilization metrics already show collaborative zones at 32% occupancy versus 26% for assigned workstations, steering investment toward multi-purpose furniture that helps facilities teams redeploy square footage rapidly. The Europe office furniture market benefits because such modular lines require frequent add-ons and accessories, lifting average ticket value when leases renew. Furniture manufacturers now capture recurring revenue through subscription models that allow clients to swap out pieces on demand, drastically reducing unused stock and landfill waste. Real-estate teams also value the data captured by sensor-enabled desks and chairs that feed utilization dashboards in real time, guiding proactive maintenance schedules that extend product lifespans.

Corporate ESG mandates fuelling demand for circular and recycled furniture

Procurement departments across Europe now treat carbon reduction as a formal purchasing criterion, accelerating the push for remanufactured tables, chair refurbishments, and as-a-service subscriptions. Providers such as NORNORM report 50% yearly growth in leased square meters while claiming up to 70% lower CO₂ impact compared with first-sale purchases[2]NORNORM, “Santander CIB Financing for Circular Expansion,” nornorm.com.. Circular offerings often include guaranteed take-back, refurbishment, and transparent end-of-life reporting, helping corporate clients meet scope-three emission targets. The strategy confers a sales advantage because buyers can now avoid upfront capital expenditure and pay from operating budgets, an approach that realigns financial planning with sustainability goals. Manufacturers simultaneously integrate ocean-bound plastics and post-consumer PET felt into panelling and seating shells, prompting plastics to emerge as the fastest material segment by 2030. The circular trend is further propelled by EU policy proposals that would extend eco-design rules to furniture and force detailed life-cycle disclosure on every item sold.

Stricter EU ergonomics directives accelerating ergonomic seating adoption

The EN 1335-1:2020 standard updates anthropometric ranges to cover 95% of European citizens, prompting companies to replace aging chairs with models offering adjustable seat depth, synchronized mechanisms, and calibrated lumbar support[3]British Standards Institution, “BS EN 1335,” bsigroup.com.. Facilities managers face compliance audits that may trigger workers’-compensation penalties if standards are not met, driving a wave of proactive chair replacements even inside organizations with otherwise restricted budgets. Seating suppliers differentiate through certifications that verify both dimensional and durability criteria, creating a market moat for well-capitalized brands. Healthcare and education verticals are moving first because occupational-health specialists have new levers to mandate upgrades across their estates. In hybrid offices, multi-user seating settings benefit from quick-adjust levers and QR-code tutorials that help each new occupant calibrate posture in seconds. Manufacturers capitalize on the standard by bundling digital ergonomics coaching apps with every chair, generating ancillary subscription revenue that improves loyalty.

Premiumization of workspace aesthetics to attract talent in tight labour markets

Tight European labour pools translate into elevated human-capital costs, compelling employers to enhance physical surroundings as a competitive differentiator. Recruiters increasingly highlight hotel-inspired lobbies, artisanal wood finishes, and curated artwork when courting candidates, making premium furniture a tangible symbol of organizational culture. Emerging design guidelines now emphasize biophilic materials, varied textures, and muted colour palettes that support mental well-being, with studies indicating productivity uplifts of 6% and creativity gains of 15% after fit-out. Premium vendors exploit these preferences by partnering with renowned designers and offering limited-edition collections that double as brand storytelling devices in social media campaigns. Although premium solutions carry higher capital outlays, finance departments accept the spend because the return comes in lower turnover and higher employee engagement metrics. Acoustic pods, statement seating, and modular lounge systems embody the premium push, each commanding margins that outstrip commodity desks by several multiples.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven capex deferrals by corporates | -1.1% | EU-wide, strongest impact in Germany, Italy | Short term (≤ 2 years) |

| Volatile timber & steel prices squeezing OEM margins | -0.8% | Manufacturing-heavy regions: Germany, Italy, Poland | Medium term (2-4 years) |

| Shrinking office-space footprints due to remote work | -0.6% | Major metropolitan areas across Europe | Long term (≥ 4 years) |

| EU Waste-from-Electricals (WEEE-style) take-back obligations adding cost | -0.3% | EU-wide regulatory compliance requirement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-driven capex deferrals by corporates

Persistent consumer-price inflation across Europe is pushing finance teams to freeze non-essential capital outlays, which directly impedes furniture refresh cycles. German furniture revenue dipped 7.40% to USD 17.8 billion (EUR 16.4 billion) in 2024, and office sub-categories contracted 4% as companies diverted cash to technology and working-capital cushions. Instead of purchasing new chairs, facilities teams engage refurbishment vendors that deliver 30-50% savings while still meeting ergonomic guidelines. Deferred makeover budgets skew mid-range volumes downward even as premium lines survive, because executives seek “statement” areas that communicate stability amid economic turbulence. The slowdown induces backlog in the Europe office furniture market but also creates latent demand that could surface in a spending sprint once macroeconomic uncertainty subsides.

Volatile timber and steel prices squeezing OEM margins

Manufacturers across Europe expect raw-material inputs to stay elevated after pandemic-related spikes, with survey data indicating potential 30% and 25% price increases for wood and steel respectively in 2025. These costs compress margins and force either price hikes or specification downgrades, each with its own demand risk. Some vendors are substituting bamboo, engineered composite boards, or recycled metals to cap exposure, but re-certification for structural integrity can delay product launches. Smaller factories without hedging facilities or diversified supply chains risk insolvency, leading to acquisition targets for larger groups seeking volume leverage. The price pressure also slows innovation because R&D budgets get reallocated to mitigate commodity shocks, lengthening refresh cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chairs Lead While Acoustic Solutions Accelerate

Chairs retained 37.85% of 2025 revenue because every workstation still requires an ergonomically compliant seat, making chairs the single indispensable product line in the Europe office furniture market share. Mandatory EN 1335 re-certifications plus corporate wellness programs extend chair lifecycles to roughly five years, triggering predictable replacement orders that stabilize factory output. Height-adjustable desks and large conference tables remain mainstays in medium to large offices, yet the post-pandemic emphasis on collaboration spurs a pivot toward lounge-style seating zones that mix sofas, stools, and coffee tables. Open-plan floorplates, however, suffer from noise fatigue, which propels booths and privacy pods to a 6.55% forecast CAGR through 2031, the fastest of any category.

Booths and divider systems thrive due to lightweight composite cores, magnetized assembly kits, and built-in ventilation fans that meet fire-safety and air-quality codes. Start-ups deploy pods immediately after signing lease agreements because the modules bypass landlord fit-out approval, shaving weeks from move-in timelines. Multinational enterprises integrate pods with booking software that tracks occupancy, optimizing seating density as return-to-office rates fluctuate. Chairs, meanwhile, remain critical for compliance but are diversifying quickly into multipurpose hybrids think perch stools that tilt to boost posture or soft task chairs that double as visitor seating.

By Material: Wood Dominates While Plastics Drive Innovation

Wood maintained a 45.20% Europe office furniture market share in 2025, sustained by client preference for natural textures that signal warmth and biophilia. Chain-of-custody certifications such as FSC and PEFC give wood an environmental edge, allowing manufacturers to charge premiums in ESG-oriented tenders. Oak, ash, and walnut finishes remain popular for executive conference tables and reception counters, though veneer sheets over particleboard cores help reduce weight and cost. Metal sub-frames add structural integrity to sit-stand desks, yet soaring steel prices pressure bill-of-materials budgets, prompting the sector to investigate alternative alloys. Simultaneously, recycled polymer formulations register the highest 6.39% CAGR because they fit circular procurement mandates and enable complex geometries in one-piece molds.

Innovative polymers embed cable-management channels, NFC tags, and antimicrobial additives during molding, supporting new hygiene and tech-integration requirements without secondary assembly. This capability shortens production times and reduces part counts, lowering warranty risk while boosting design freedom. Furniture made from recycled PET felt also gains traction as acoustic baffles behind monitor arms, providing sound absorption and colour customization at scale.

By Price Range: Premium Segment Outpaces Market Growth

Mid-range furniture generated 55.60% of 2025 sales because it balances cost pressures with feature sets that satisfy most procurement checklists. Three-tier price architecture economy, mid, premium remains standard practice, yet inflation pushes some clients either to refurbish existing stock or to trade up for visibly superior items that justify spending. Economy products still win small business orders and public-sector frameworks constrained by austerity, but warranty claims and durability concerns limit long-term viability in enterprise accounts. Premium purchases, currently at a 6.81% CAGR, include stitched leather executive seating, solid wood desks with concealed power hubs, and privacy booths lined with wool felt for better acoustics.

Moreover, premium pieces integrate sensor arrays and app-powered height presets that feed wellness analytics, a feature set aligned with data-driven HR programs. CFOs green light these buys when analysis shows lower depreciation curves and higher residual values, effectively shrinking total cost of ownership. Vendors capitalize on this dynamic by offering in-house reupholstery and refurbishment services, retaining brand equity across multiple ownership cycles. Premium therefore operates both as a product and a service category, further insulating suppliers from commodity price swings. As hybrid work mints new flagship hubs intended to showcase corporate culture, the Europe office furniture market size allocated to premium will keep expanding.

By End-user: Healthcare Offices Accelerate Growth

Corporate offices still represent 61.35% of total turnover because centralized spaces remain essential for collaboration, branding, and regulatory oversight. Despite desk densities declining, the need for flexible collaboration sets drives spending on team tables, mobile storage, and lounge seating. Educational campuses maintain a steady share, modernizing libraries and innovation hubs with agile furnishings that cater to varied learning modalities. Government agencies procure based on multi-year framework agreements, which helps manufacturers forecast volumes and invest in localized support teams.

Healthcare offices deliver standout momentum with a 7.24% CAGR, reflecting hospital expansions and specialized administrative wings that demand antimicrobial coatings, sealed seams, and wipe-clean surfaces. These settings require ergonomic seating built for long shifts at nurse stations and reception counters that double as triage desks, pushing suppliers to certify materials for stringent infection-control protocols. The environment also encourages furniture designed around patient comfort for example, adjustable visitor chairs in consultation rooms creating niche product lines that command premium pricing. As outpatient clinics proliferate across suburban Europe, localized fit-outs present new volume pockets.

By Distribution Channel: Direct Sales Dominate and Accelerate

B2B direct sales reached 78.10% in 2025 because manufacturers prefer holding client relationships rather than sharing margin with intermediaries. Direct channels allow bundled services space planning, financing, and after-sales maintenance making them attractive for organizations that lack internal facility teams. Digitally enabled configurators let clients design workstations online and receive instantaneous quotes, cutting lead times and errors. National dealership networks still exist but increasingly serve as installation partners rather than prime contractors, reversing traditional roles.

Online portals now target small-office and home-office customers who crave commercial-grade pieces shipped at residential parcel rates, a cohort that exploded during pandemic lockdowns. Augmented-reality apps help users visualize desks at actual scale in living rooms, bridging the gap between retail and contract furnishings. Specialty showrooms retain value for prototyping, allowing corporate buyers to test acoustic pods and sit-stand desks before signing six-figure orders. Hybrid models digital first, physical confirmation second are likely to keep directing wallet share to brands that manage omnichannel touchpoints seamlessly.

Geography Analysis

Germany held 20.30% of 2025 revenues, anchored by Europe’s largest manufacturing base and stringent regulatory frameworks that heighten demand for certified ergonomics. The nation’s export-led economy invests heavily in showcase headquarters where design-forward furniture underscores brand prestige, ensuring a stable core for the Europe office furniture market size. Nevertheless, macroeconomic uncertainty caused many German corporates to delay upgrades in 2024, impacting new-build fit-outs and driving higher refurbishment rates.

Spain, by contrast, will post the region’s quickest 7.73% CAGR through 2031 as real-estate and ICT sectors expand employment rosters and office footprints. Madrid and Barcelona lead greenfield builds that prioritize WELL and LEED certifications, requiring ultra-low-VOC materials and sensor-enhanced sit-stand desks. The Spanish market, once dominated by small carpentry workshops, now attracts multinational vendors eager to localize production and shorten supply chains. Declining financing costs encourage developers to spec premium communal areas cafeterias, co-working lounges, rooftop meeting pods that rely on durable outdoor-rated furniture varieties.

Elsewhere, the Nordics couple high purchasing power with circular procurement mandates, producing healthy demand for remanufactured chairs and resource-positive materials. Benelux nations, with their dense financial and logistics clusters, favor high-end modular systems that can relocate across leased floors every three years. Italy remains a design powerhouse exporting premium collections but experiences domestic softness due to slower GDP growth. France shows steady mid-range spend as Paris accelerates office redevelopment ahead of the 2024 Olympic legacy phase. The collective rest-of-Europe segment benefits from EU recovery funds channelled into digital infrastructure, which in turn attracts tech tenants needing agile workstations.

Regulatory Landscape

Regulation in Europe is tightening around product safety, ergonomics, and sustainability disclosure. The EU Ecodesign for Sustainable Products Regulation (ESPR) (Regulation (EU) 2024/1781), effective from July 2024, sets the direction for forthcoming furniture-specific requirements around durability, repairability, and resource efficiency. Furniture is also prioritized in the EU Ecodesign and Energy Labelling Working Plan 2025-2030, which signals an industry shift toward documented circularity attributes such as recycled content and take-back readiness.

Near-term compliance focus also includes chemical emissions and general safety obligations. From 6 August 2026, the EU restriction on formaldehyde release (Regulation (EU) 2023/1464, REACH Annex XVII entry 77) limits formaldehyde emissions from furniture placed on the EU market. This pushes manufacturers to verify wood-based panels, adhesives, and finishes earlier in the product development cycle. In parallel, the General Product Safety Regulation (EU) 2023/988 sets overarching safety duties, supported by harmonized furniture safety standards referenced under Commission Implementing Decision (EU) 2019/1698, reinforcing the need for documented conformity across seating, tables, and modular systems used in offices.

Value Chain Analysis

The Europe office furniture value chain begins with upstream inputs such as timber and wood-based panels, metals (steel and aluminum), plastics and polymers (including recycled streams), textiles, foam, fasteners, coatings, and adhesives, then moves through design and engineering, component fabrication, final assembly, and quality and certification processes. The sector remains shaped by a large SME base (about 1 million employees across around 130,000 enterprises), with clusters specializing by capability (woodworking, metal frames, upholstery) and feeding contract and project-led demand for chairs, desks, storage, and acoustic solutions.

Downstream, manufacturers sell through B2B direct sales, dealers and integrators, and project specifiers such as architects and workplace consultants, with installation, maintenance, refurbishment, and take-back increasingly bundled as lifecycle services. Supply-chain volatility and maritime disruption during 2024 reinforced the role of multi-sourcing and near-shoring for components, while ESPR-related preparations add a new data layer to the chain, including design-for-disassembly, traceability, and Digital Product Passport readiness. Industry platforms such as the GO Furniture Meta-Cluster (formed after the 2021-2024 Furniture Go International project) are being used to connect SMEs to cross-border innovation and sustainability programs, helping align smaller producers with new compliance and service expectations.

Competitive Landscape

The Europe office furniture market is moderately concentrated, with the top five players together controlling a significant portion of sales. This scale gives them an advantage while still leaving plenty of room for regional specialists. Steelcase leads the market, using its global R&D capabilities to introduce sensor-integrated desks that provide occupancy analytics dashboards. Herman Miller stands out with its iconic designs and a strong focus on sustainable materials, such as ocean-bound plastics used in its Aeron Remastered chair. Haworth’s position is built on modular walls and private-office suites that combine acoustical privacy with quick reconfiguration, catering to the needs of hybrid work environments.

European stalwarts Kinnarps and Vitra contribute a notable combined share through their focus on Nordic minimalism and Swiss precision, respectively, each emphasizing strong commitments to circular supply chains. Strategic moves include Flokk’s 2024 acquisition of Stylex, boosting North American exposure and broadening the portfolio with healthcare-grade seating. Also noteworthy is Watson Furniture’s 2025 partnership with Sedus to cross-sell German-engineered tables into U.S. markets, reflecting outbound ambitions amid saturated European demand.

Competitive fronts now extend to digital platforms where AI-powered configurators slash quoting time, appealing to large corporates with compressed relocation schedules. Vendors build analytics ecosystems that monetize desk-usage data, selling anonymized insights back to clients for space-optimization plans. Sustainability remains another wedge; companies unable to certify cradle-to-cradle loops risk exclusion from Nordic tenders. Finally, volatile input prices encourage suppliers to hedge materials through long-term contracts or to invest directly in sawmills, creating barriers for smaller entrants. These dynamics demonstrate that while headline concentration metrics show moderate dominance, the market rewards agility and niche specialization.

Europe Office Furniture Industry Leaders

Steelcase Inc.

Herman Miller Inc.

Haworth Inc.

Kinnarps AB

Vitra International AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circular procurement and lifecycle service models create whitespace for manufacturers and integrators that can operationalize take-back, refurbishment, and reporting at scale, especially as ESG-driven buying criteria and ESPR preparations pull sustainability data into tender requirements. Leasing and subscription models already show traction, for example NORNORM reports rapid growth in leased area and positions its model around materially lower CO2 impact versus first-sale purchases, which supports demand for standardized, modular product architectures that can be redeployed and remanufactured across client sites.

Compliance-driven product redesign also opens opportunities around materials and documentation. The 6 August 2026 formaldehyde emission restriction in the EU increases the value of low-emission boards, certified adhesives and finishes, and verified test documentation for office systems built with wood-based components. At the same time, industry bodies and trade notes point to active investment attention on European furniture districts. FederlegnoArredo, for instance, reported the Italian wood-furniture supply chain at EUR 52.2 billion production turnover at the close of 2025, which supports supplier development in engineered panels, recycled polymers, and component standardization aligned with modular workstations, acoustic booths, and direct-to-business configuration workflows.

Recent Industry Developments

- June 2026: Herman Miller introduced updates to the Aeron Chair, adding new color options and advancing materials with an emphasis on recycled and bio-based inputs. The change reinforces premiumization in task seating while aligning flagship products with corporate circularity and carbon-accounting requirements in European tenders.

- December 2025: HNI Corporation completed its acquisition of Steelcase Inc., combining two major office furniture portfolios and distribution footprints. The consolidation reshapes competitive dynamics for large enterprise and public-sector bids by expanding bundled offerings across seating, systems furniture, and workplace services.

- July 2024: NORNORM secured a debt facility from Santander CIB that was guaranteed by the European Investment Fund to scale its furniture-subscription model across key European hubs. The financing strengthened the economics of circular office fit-outs by expanding access to asset-backed leasing and refurbishment capacity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of office furniture sold across Europe for use in professional workspaces, including core items like seating, desks, tables, and storage, counted at the point of sale to end users through direct and indirect channels.

Scope exclusions: We exclude residential-only furniture and home decor items that are not designed or marketed for office use.

Segmentation Overview

- By Product

- Chairs

- Employee Chairs

- Meeting Chairs

- Guest Chairs

- Tables

- Conference Tables

- Desks

- Other Tables

- Storage Units

- Filing Cabinets

- Bookcases & Shelving

- Sofas/Soft Seating

- Booths and Office Dividers

- Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others)

- Chairs

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-range

- Premium

- By End-user

- Corporate Offices

- Healthcare Offices

- Educational Institutions

- Government & Public Offices

- Hospitality & Retail Back-office

- Others

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B / Directly from Manufacturers

- B2C / Retail

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Benelux

- Nordics

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base that keeps the model realistic, especially on furniture production, trade flows, and building activity that links to office fit-outs. We typically refer to public data series and reference documents such as Eurostat manufacturing and trade statistics, UN Comtrade trade tables, and national statistical offices for construction and business demography.

To sharpen the Europe view, we also cross-check with sources such as European Commission policy pages (for circularity and product compliance direction), customs and port releases where available, and peer-reviewed journals that cover ergonomics and workplace design adoption. Company annual reports, filings, and investor presentations help confirm revenue mix and channel emphasis, while reputed press and association websites are used to validate event-driven demand swings. Where needed, paid company financials and a shipment-level import/export database were used to validate directional shares and unit pricing logic. This desk source list is illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how demand is formed in Europe, which is usually shaped by office refurbishments, hybrid-work layouts, and procurement cycles in large enterprises and public bodies. We spoke with manufacturers, distributors, large buyers, and industry experts across major European countries so gaps in desk inputs, such as channel splits and price movements, could be closed before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 48% | Functional/Unit leaders: 43% | |

| Smaller Players: 16% | Managers: 44% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where production and trade data are used to reconstruct the addressable office furniture consumption pool across Europe, and it is then aligned to observable demand signals from workspace projects. To keep the totals grounded, we corroborate them with selective bottom-up approximations, such as sampled price points by product type multiplied by expected unit demand from refurbishment activity, and then we adjust where the two views disagree.

Inputs used in the model include office employment levels, office construction and renovation trends, procurement activity from corporate and public buyers, import intensity by furniture category, and average selling price movements by material and product mix. Because hybrid work is still changing buying patterns, we also track indicators like seat-to-desk ratios in new layouts and the share of flexible collaboration zones in fit-out plans, which shifts the split between seating, tables, and storage. Forecasting is done using scenario analysis supported by simple multivariate regression where demand drivers like renovation spend and office headcount explain a large share of historical movement, and assumptions are refined using what interviewees expect for lead times and pricing.

When bottom-up checks are incomplete for smaller countries or niche product lines, gaps are handled through proportional allocation using trade and employment weights, followed by a reasonableness check against per-employee spend and replacement cycle norms.

Data Validation & Update Cycle

Outputs are validated by comparing the final market totals with independent signals such as Europe-wide furniture trade balances, major country construction cycles, and disclosed revenue direction from relevant suppliers. Outliers are reviewed, and if a variance cannot be explained by a clear driver, such as currency movement or one-time project timing, we re-check assumptions and, when required, re-contact participants for clarification.

Before sign-off, the model goes through multi-step analyst reviews where calculations, unit conversions, and year mapping are verified, followed by a final consistency pass across countries and channels. Reports are refreshed annually, with interim updates triggered by material events like sharp raw material price swings, trade disruptions, or policy changes that alter compliance costs. A final review is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Europe Office Furniture Market Estimate Compared With Other Published Estimates

Published market sizes for Europe office furniture can appear far apart even when they claim to measure the same underlying category, because the scope and measurement point can shift. Differences most often come from whether values represent consumption versus revenue, which countries are included in Europe, and how direct versus retail sales are treated.

The benchmark table shows a noticeable spread across the latest published numbers, and in Mordor Intelligence's model the total is tied to office-specific furniture categories sold into professional workplaces through both direct and indirect channels, rather than broader furniture groupings or narrower consumption-only cuts. The gap is also widened when some publishers time pricing using different exchange-rate windows, or when their forecast path assumes either a rapid hybrid-work refresh cycle or a slower replacement cycle without checking what procurement teams are actually budgeting for.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.36 B (2026) | |

| Industry Publisher A | USD 18.23 B (2024) | Uses a different base year and may reflect a broader revenue view for Europe office furniture, which can include adjacent categories and a different country basket, and it is less transparent on how channel markups and currency timing are treated. |

| Trade Journal B | USD 10.48 B (2024) | Reported as Europe office furniture consumption in EUR, which is typically narrower than sell-in revenue and can exclude parts of the value chain, and the conversion to USD can shift the headline depending on the exchange-rate period used. |

Taken together, the differences are mainly explained by what is being counted (revenue versus consumption), which geographies are grouped into Europe, and how pricing and currency are handled for the stated year. By keeping the model anchored to clear demand drivers like office renovations and procurement cycles, and then cross-checking totals using trade and pricing signals, the estimate stays traceable to practical inputs that can be repeated and updated each year.

Key Questions Answered in the Report

What is the forecast value of the Europe office furniture market in 2031?

The market is projected to reach USD 20.52 billion by 2031, growing at a 5.96% CAGR.

Which product category will grow fastest in European offices?

Booths and office dividers are expected to post a 6.55% CAGR through 2031, driven by demand for acoustic privacy in hybrid workplaces.

Why are plastics gaining share in office furniture materials?

Recycled polymers meet circular procurement goals and enable complex, lightweight designs, leading the material segment with a 6.39% CAGR.

Which European country shows the strongest growth momentum?

Spain is forecast to record a 7.73% CAGR due to rising construction and professional-services activity.

Page last updated on: