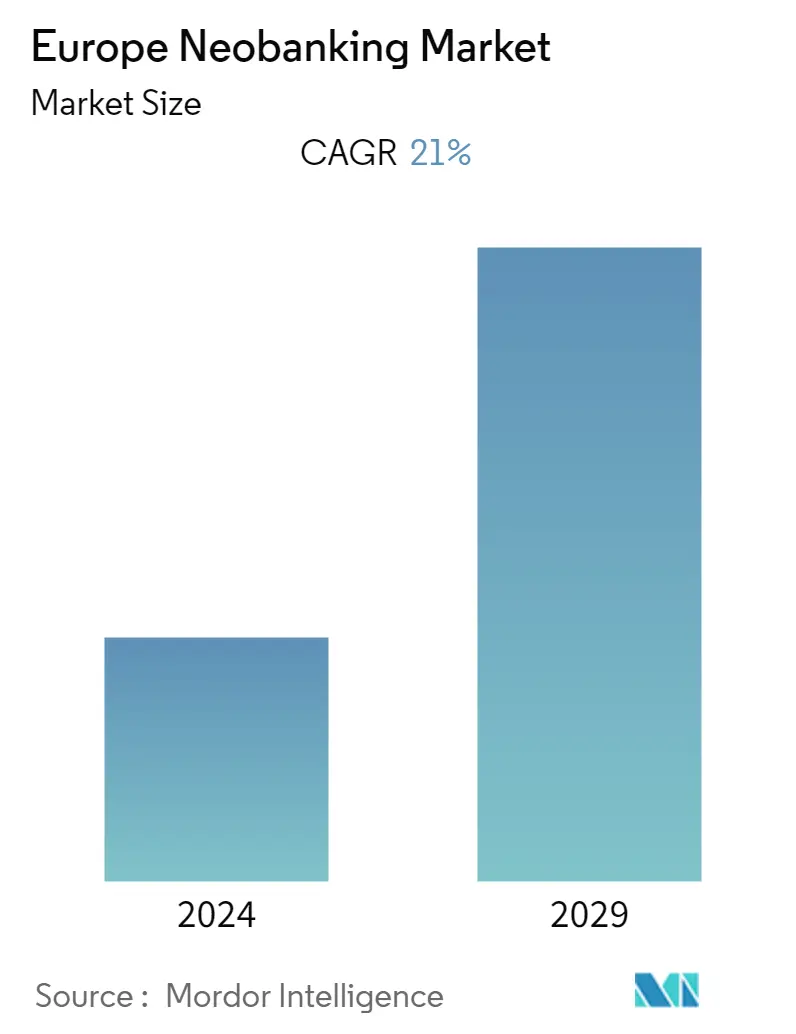

Market Size of Europe Neobanking Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | 21.00 % |

| Market Concentration | Medium |

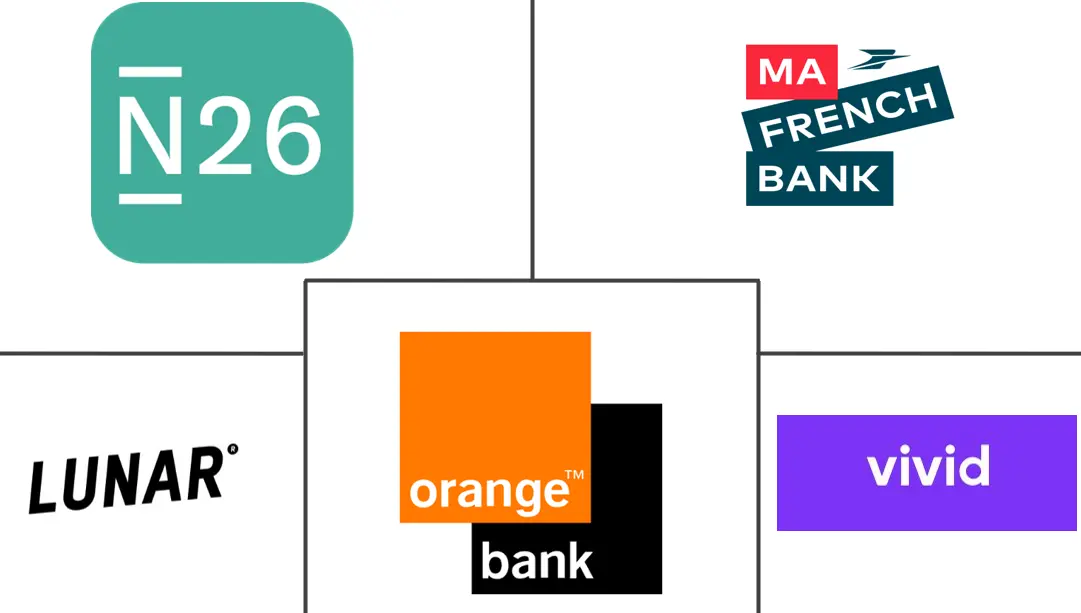

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Neobanking Market Analysis

Europe's Neobanking Market is estimated to have generated 2100 billion worth of transaction value in the current year and is poised to achieve a CAGR of 21% for the forecast period.

Neobanking is a novel banking technology that provides complete online banking solutions from opening an account to other services, without the need to go to a bank for its customers. Neobanking differs from traditional banks, as they have no physical offices & branches.

Europe holds the biggest market share in the Neobanking Market and accounts for over 30% share of the global revenue due to the establishment of multiple technology start-ups & the growing adoption of technology. The growing adoption of internet services and the increased use of smartphones are expected to accelerate market growth.

During the period of Covid-19 in 2020, Germany was having the highest user number in Digital Commerce with an average transaction value Digital commerce per user stood at a level of 2,084 US$ which stands at the second highest level after the United States. Higher and Middle-income level people contribute the most to an increase in the adoption of the Neobanking Market with restrictions made during covid for offline transactions.

Some banks are more vulnerable than others to the fallout from the COVID-19 crisis due to a weaker solvency position or individual business model characteristics. More than 2,000 small and medium-sized banks are directly supervised by national authorities. The ECB has taken measures to drastically mitigate banks funding risk, by providing new long-term central bank funding and making it easier to access this funding.

Europe Neobanking Industry Segmentation

The Europe Neobanking market is segmented by account type (Business account, Savings account), by services (Mobile-banking, Payments and money transfers, savings, Loans, Others), and By Country (Germany, Spain, Italy, Russia, France, United Kingdom, and Rest of Europe), various trends, opportunities, and company profiles. The report offers Market size and forecasts for the Europe Neobanking Market in value (USD Billion) for all the above segments.

| By Account Type | |

| Business Account | |

| Savings Account |

| By Services | |

| Mobile Banking | |

| Payments and Money Transfers | |

| Savings Account | |

| Loans | |

| Other Sevices |

| By Country | |

| Germany | |

| France | |

| United Kingdom | |

| Russia | |

| Italy | |

| Spain | |

| Rest of Europe |

Europe Neobanking Market Size Summary

The European neobanking market is experiencing significant growth, driven by the increasing adoption of digital banking solutions that offer comprehensive online services without the need for physical bank branches. This market is the largest globally, accounting for a substantial portion of the worldwide revenue, thanks to the proliferation of technology startups and the widespread use of smartphones and internet services. The COVID-19 pandemic accelerated the shift towards neobanking, as restrictions on offline transactions prompted higher and middle-income individuals to embrace these digital solutions. The regulatory environment, particularly the Payment Services Directive, has further facilitated this growth by allowing fintech firms direct access to customer data, previously reserved for traditional banks.

Neobanks are particularly appealing to younger demographics, with the highest penetration among 18 to 24-year-olds, due to their low-cost models and minimal fees for banking services. The market's expansion is supported by advancements in AI, Big Data, and Cloud Computing, which enhance service delivery and operational efficiency. Major players like N26, Vivid, and Lunar dominate the market, but technological advancements and service innovations continue to attract new entrants. The market's competitive landscape is marked by significant funding activities, such as Lunar's recent capital raise and N26's landmark funding round, which underscore the sector's dynamic nature and potential for further growth.

Europe Neobanking Market Size - Table of Contents

-

1. MARKET INSIGHTS AND DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Insights on Technological innovation in the Neobanking Industry

-

1.5 Porters 5 Force Analysis

-

1.5.1 Threat of New Entrants

-

1.5.2 Bargaining Power of Buyers/Consumers

-

1.5.3 Bargaining Power of Suppliers

-

1.5.4 Threat of Substitute Products

-

1.5.5 Intensity of Competitive Rivalry

-

-

1.6 Insights on Government Regulations Landscape in the Neobanking Industry

-

1.7 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Account Type

-

2.1.1 Business Account

-

2.1.2 Savings Account

-

-

2.2 By Services

-

2.2.1 Mobile Banking

-

2.2.2 Payments and Money Transfers

-

2.2.3 Savings Account

-

2.2.4 Loans

-

2.2.5 Other Sevices

-

-

2.3 By Country

-

2.3.1 Germany

-

2.3.2 France

-

2.3.3 United Kingdom

-

2.3.4 Russia

-

2.3.5 Italy

-

2.3.6 Spain

-

2.3.7 Rest of Europe

-

-

Europe Neobanking Market Size FAQs

What is the current Europe Neobanking Market size?

The Europe Neobanking Market is projected to register a CAGR of 21% during the forecast period (2024-2029)

Who are the key players in Europe Neobanking Market?

https://n26.com/en, https://vivid.money/en-eu, https://www.mafrenchbank.fr, https://www.orangebank.fr and https://www.lunar.app are the major companies operating in the Europe Neobanking Market.