Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

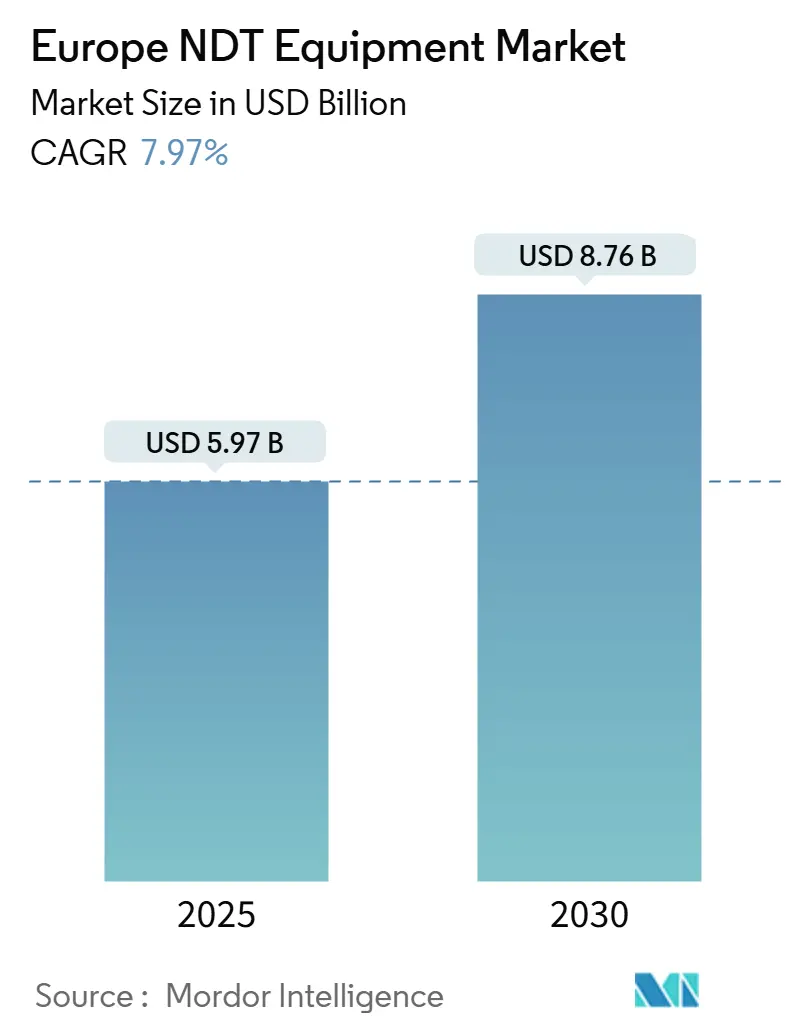

| Market Size (2025) | USD 5.97 Billion |

| Market Size (2030) | USD 8.76 Billion |

| Growth Rate (2025 - 2030) | 7.97% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe NDT Equipment Market Analysis by Mordor Intelligence

The Europe NDT Equipment market size stands at USD 5.97 billion in 2025 and is projected to climb to USD 8.76 billion by 2030, reflecting a 7.97% CAGR over the forecast period. This sustained advance demonstrates that asset-heavy sectors are transitioning from reactive maintenance to predictive integrity programs, anchored in digital twin workflows and micro-focused X-ray systems that meet the quality standards of additive manufacturing. Equipment still supplies a significant portion of the revenue base, but a pronounced shift toward outcome-based contracts is evident as operators outsource inspections to preserve capital, standardize data flows, and accelerate technology refreshes. Regulatory tightening, particularly under the EU Pressure Equipment Directive and revised IAEA safety standards, is reducing inspection intervals and compelling plants to adopt phased-array ultrasonic, computed tomography, and infrared thermography systems that provide volumetric coverage in fewer passes. Germany, France, and the United Kingdom remain the highest-value pockets of the Europe NDT Equipment market thanks to aerospace, nuclear, and automotive quality mandates, yet Spain, Poland, and Romania are recording the fastest momentum as renewable energy projects attract EU cohesion funds. Competitive strategy is shifting toward hybrid leasing and managed-service offerings in which equipment vendors bundle calibration, software, and training, thereby blurring the traditional line between hardware and services.[1]European Commission, “Horizon Euratom 2024 – Nuclear Research and Training,” europa.eu

Key Report Takeaways

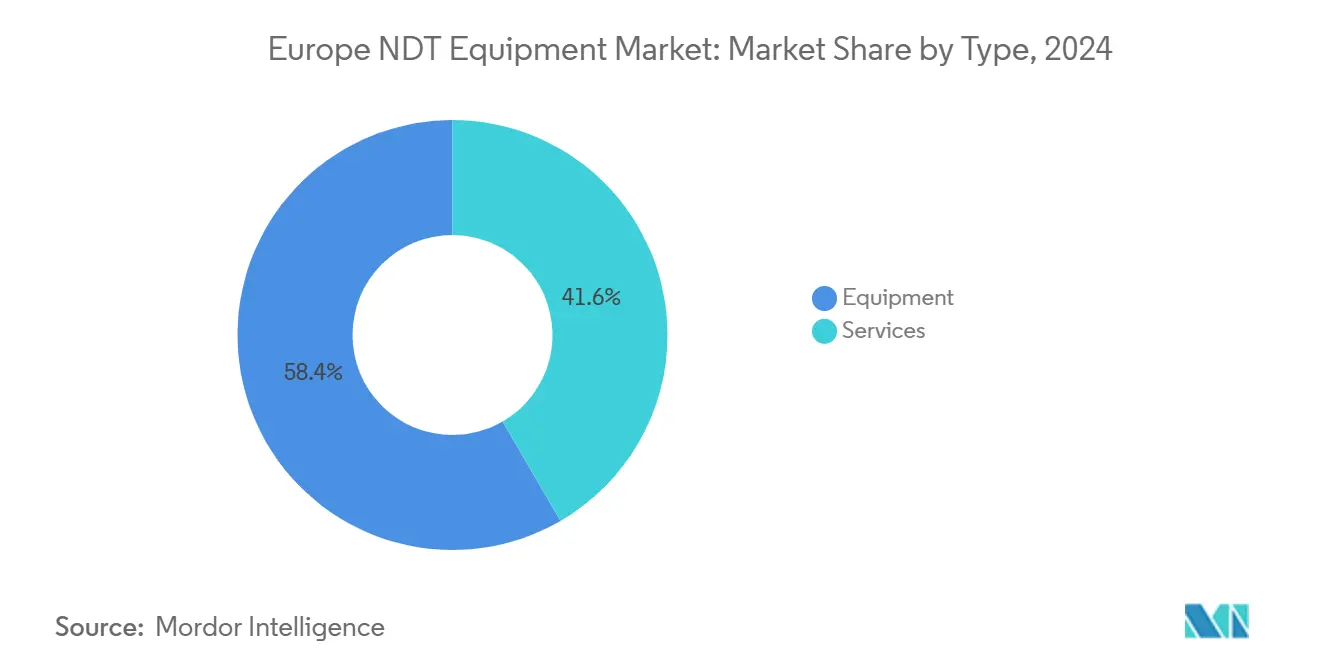

- By type, equipment accounted for 58.38% of 2024 revenue, while services are expanding at a 9.24% CAGR through 2030, underscoring an outsourcing pivot that is reshaping the Europe NDT Equipment market.

- By testing technology, ultrasonic testing accounted for 32.57% of 2024 deployments, whereas thermography showed the quickest trajectory, with an 8.23% CAGR, driven by wind-blade and solar-thermal monitoring needs.

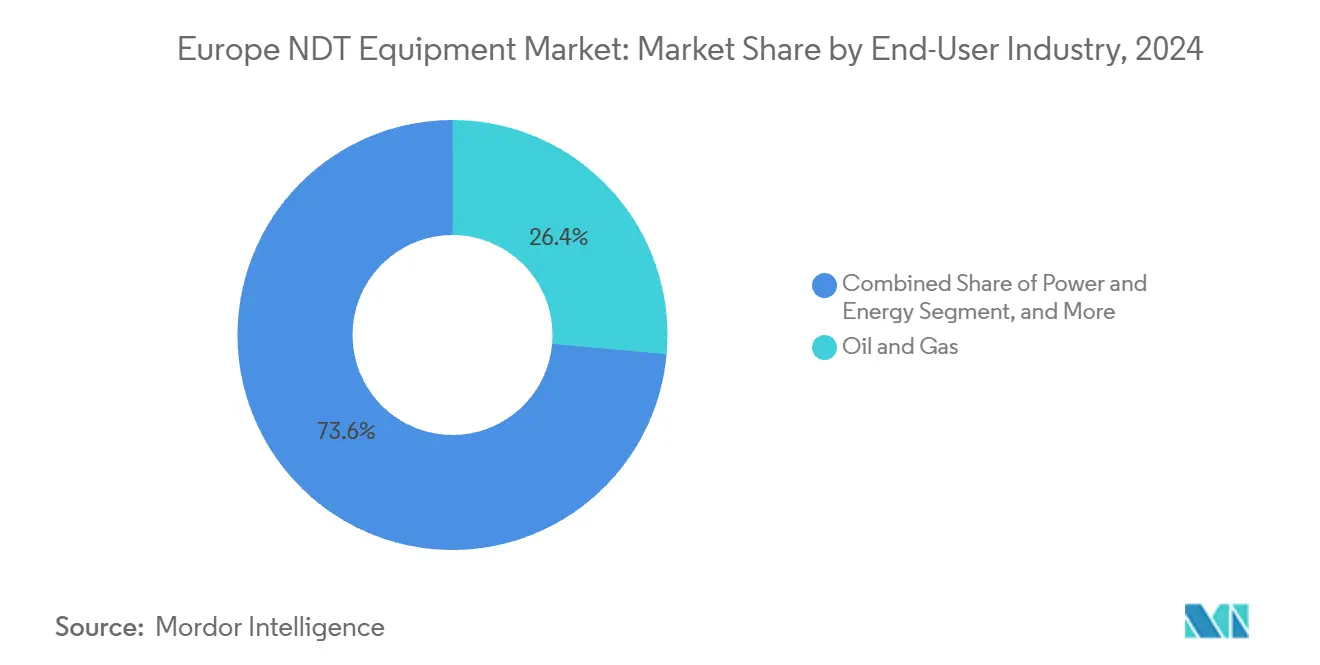

- By end-user, the oil and gas sector generated 26.43% of 2024 demand, whereas additive manufacturing is projected to accelerate at an 8.45% CAGR, as aviation primes insist on sub-10-micron porosity detection.

- By service type, inspection services accounted for 42.17% of 2024 revenue, while training services are projected to grow at an 8.48% CAGR, reflecting the shortage of ISO 9712-certified personnel.

- By Country, Germany led with a 24.73% revenue share in 2024; Spain is forecast to rise at an 8.32% CAGR as renewables build-out drives recurrent inspection cycles.

Europe NDT Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Standards Mandating Safety Compliance | +1.8% | Pan-European, strongest in Germany, France, UK | Medium term (2-4 years) |

| Growing Adoption in Oil and Gas for Pipeline Integrity | +1.5% | North Sea operators (UK, Netherlands, Norway), Eastern Europe transit routes | Long term (≥ 4 years) |

| Increasing Aerospace and Defense Manufacturing Investments | +1.3% | France, Germany, UK, Italy | Medium term (2-4 years) |

| Integration of Digital Twin Models with NDT Systems | +1.1% | Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Shift Toward Micro-Focus X-Ray for Additive Manufacturing Parts | +0.9% | Germany, France, UK aerospace clusters | Short term (≤ 2 years) |

| EU Funding to Modernize Nuclear Reactor Inspection Infrastructure | +0.7% | France, Spain, Finland, Czech Republic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Standards Mandating Safety Compliance

Across the Europe NDT Equipment market, operators must align with the EU Pressure Equipment Directive and the updated IAEA Safety Standards that came into force in 2024. National bodies, such as Germany’s TÜV, have already shortened the allowable inspection intervals for high-pressure vessels, driving the immediate procurement of phased-array ultrasonic instruments that generate full-wall coverage in a single scan.[2]International Atomic Energy Agency, “Safety Standards Series: In-Service Inspection of Nuclear Power Plants,” iaea.org Harmonized ISO 9712 personnel rules now demand dual certification for cross-border work, but implementation still varies across Eastern Europe, creating a price gap that incentivizes multinationals to centralize high-end inspections in Germany or the Netherlands. Insurance underwriters are increasingly refusing policies for critical assets that are inspected only with manual methods, pushing even cost-sensitive SMEs toward advanced, traceable solutions. Compliance spend is therefore rising faster than overall capital expenditure, anchoring a resilient demand stream for both equipment and managed services.

Growing Adoption in Oil and Gas for Pipeline Integrity

North Sea and Baltic operators are replacing calendar-based inspection with condition-based pipelines assessment supported by inline ultrasonic and electromagnetic acoustic tools that map wall thinning without halting throughput. The North Sea Transition Authority’s 2024 mandate added more than 12,000 km of legacy steel pipelines to the biennial inspection schedule, lifting service backlogs and sparking a wave of multiyear contracts. Hydrogen blending pilots across Germany and the Netherlands are amplifying the need for more frequent weld inspections to monitor embrittlement. Service providers with robotic crawlers capable of 1,500-meter subsea depth and phased-array coverage enjoy pricing power, while equipment vendors are designing modular scanners that can be leased per campaign, a model favored by operators looking to contain upfront outlays.

Increasing Aerospace and Defense Manufacturing Investments

Airbus, Dassault Aviation, and other primes are embedding real-time computed tomography (CT) stations at every additive manufacturing cell to guarantee volumetric integrity before downstream machining. Airbus alone installed 23 new CT systems in 2024, trimming scrap by 19% and proving the ROI of early-stage defect detection. NATO-aligned defense agencies now require cloud-traceable inspection data for every critical part, extending demand for digital radiography with secured on-premise storage. Public funding via the European Defence Fund has earmarked EUR 565 million (USD 658.82 million) for fuselage composite inspection projects that lean heavily on automated phased-array ultrasonic robots. As a result, the Europe NDT Equipment market is experiencing a sharper replacement cycle in aerospace than any other vertical.

Integration of Digital Twin Models with NDT Systems

Wind-farm operators and power-plant owners are fusing inspection data with digital twins to defer costly shutdowns. Siemens’ Xcelerator roll-out across 14 European gas-turbine plants extended major-overhaul windows by an average 18 months after ultrasonic data fed directly into virtual replicas of hot sections. However, proprietary data formats still hinder seamless connectivity, forcing users to purchase middleware that normalizes NDT outputs. Germany’s BAM has issued voluntary data schema guidelines, but low adoption in Southern Europe underscores the need for regulatory nudges. Vendors that enable open-architecture exports are beginning to command premiums, signaling that software compatibility is now a buying criterion on par with detector resolution.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled NDT Technicians | -1.2% | Pan-European, acute in Germany, UK, Netherlands | Long term (≥ 4 years) |

| High Initial Capital Investment for Advanced Equipment | -0.9% | Southern and Eastern Europe, SME-heavy markets | Medium term (2-4 years) |

| Fragmented Calibration Standards Across EU Member States | -0.6% | Cross-border operators, particularly in Central and Eastern Europe | Medium term (2-4 years) |

| Data Security Concerns in Cloud-based NDT Platforms | -0.4% | Defense, nuclear, critical infrastructure sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled NDT Technicians

Nearly 38% of ISO 9712 Level 3 inspectors will reach retirement age by 2028, yet current training pipelines graduate fewer than 2,500 Level 2 candidates per year. Average hourly rates for certified ultrasonic specialists surged 14% in 2024, twice the pace of general manufacturing wages, squeezing service-provider margins under fixed-price frame agreements. VR-based simulators help compress learning curves, but certification bodies still cap virtual hours that count toward qualification, delaying workforce replenishment. The talent gap also limits how quickly the Europe NDT Equipment market can adopt complex modalities such as time-of-flight diffraction, which require extensive interpretive expertise.

High Initial Capital Investment for Advanced Equipment

Computed tomography scanners, high-power micro-focus X-ray systems, and phased-array ultrasonic units cost between EUR 250,000 (USD 291513.75) and EUR 2 million (USD 2.33 million), sums that deter SMEs in Spain, Italy, and Romania from upgrading film-based assets. Leasing helps, but lenders add 3–5 percentage-point risk premiums to cover concerns about technology obsolescence, and useful life is shrinking to under 9 years as detector innovations accelerate. Although Italy introduced a EUR 45 million (USD 52.47 million) grant pool for SME NDT upgrades, the average approval time of 9 months blunts the impact. The result is a patchwork of capability depth across Europe, with highly automated labs in Germany alongside film-based lines in Southern Europe.

Segment Analysis

By Type: Services Gain Ground as Outsourcing Accelerates

Equipment continued to dominate the Europe NDT Equipment market size with a 58.38% value share in 2024, yet services are forecast to outpace at 9.24% CAGR through 2030 as clients pivot to variable operating costs over lump-sum capital spending. The Europe NDT Equipment market share, currently dominated by equipment vendors, is shifting toward bundled leasing options that include software updates and on-site calibration, aligning cash flows with project milestones. For oil and gas supermajors, the equipment-ownership model remains relevant because frequent inspections justify high utilization rates; however, even these players outsource CT or acoustics when usage is sporadic over a platform’s life. The trend is particularly vivid among construction firms that prefer to book inspections on a per-project basis rather than maintain idle detectors between building cycles. Service specialists, meanwhile, expand regional labs, reducing mobilization costs and leveraging volume discounts on consumables, which translates into competitive day rates.

Momentum in services also stems from insurance stipulations that require third-party sign-off on critical welds, pressure vessels, and composite joints. Bureau Veritas expanded its network by 17% in 2024, promoting trade-in credits that encourage customers to retire aging radiography sets and transition to fee-for-service contracts. Equipment makers are responding by forming joint ventures with regional labs, ensuring market access while sharing risk on asset utilization. These alliances further blur the vendor-service boundary and reinforce a hybrid competitive landscape where revenue diversification is key.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Testing Technology: Thermography Emerges as Renewable Energy Catalyst

Ultrasonic testing retained 32.57% of 2024 technology revenue, underpinned by its adaptability to weld inspection, thickness gauging, and composite delamination detection within the Europe NDT Equipment market. However, thermography is projected to advance at an 8.23% CAGR through 2030, reflecting declines in infrared sensor prices and the growing need for contactless surveys of wind blades and solar collectors. In offshore wind parks, drone-mounted infrared cameras scan 80-meter blades in under an hour, cutting downtime that would otherwise require rope access. Infrared also supports early fault detection in solar fields, pinpointing hot-spots that signal string failures without halting generation. Radiography maintains a foothold in aerospace because it delivers permanent records, yet expansion is limited in urban settings where licensing hurdles and exclusion-zone costs erode ROI.

Eddy current testing is rewriting additive-manufacturing protocols by detecting subsurface porosity in conductive alloys without the radiation baggage associated with X-ray testing. The new EN 17640 standard harmonized eddy current acceptance criteria, smoothing qualification for flight parts. Acoustic emission systems occupy a niche but growing spot for real-time leak detection in petrochemical spheres, while visual inspection remains the volume workhorse though low-margin because of its labor intensity. Magnetic particle and dye penetrant hold a role in automotive crankshafts and forged hardware, but their combined share is edging down as eddy current and thermography substitute faster, cleaner workflows.

By End-User Industry: Additive Manufacturing Reshapes Inspection Protocols

Oil and gas preserved a 26.43% share of Europe NDT Equipment market demand in 2024, yet additive manufacturing is on track for the fastest lift at an 8.45% CAGR, moving 3D printing from prototype phases into serial flight hardware. Aerospace primes mandate 100% volumetric inspection of printable parts, which accelerates the uptake of CT scanners and stimulates innovation in automated defect classification. Defence programs add a further pull by requiring traceable data archives for fatigue-life prediction, making digital radiography and ultrasonic array capture indispensable. EV battery-pack inspection and bond-line verification offset declining calls for crankshaft magnetic particle checks.

Manufacturing, a broad category that encompasses general industrials, relies on customer specifications rather than statutory law, so adoption rates hinge on OEM quality clauses embedded in purchase contracts. Construction demand is closely tied to EU infrastructure funding; here, intermittent inspection needs prompt contractors to opt for service rental instead of owning detectors. In power generation, thermal and nuclear sites require continuous monitoring, whereas wind and solar facilities necessitate non-contact techniques, such as thermography, that can be mounted on aerial vehicles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Type: Training Demand Reflects Skills Crisis

Inspection services occupied 42.17% of service revenue in 2024 and will remain the anchor, yet training is poised for the sharpest climb at an 8.48% CAGR as companies grapple with technician deficits. ISO 9712 harmonization drives firms to certify existing staff and court new entrants, propelling demand for virtual labs and intensive boot camps. Calibration services track the expanding installed base of high-spec instruments, albeit with margin pressure because OEMs bundle first-year calibrations for free. Consultancy, though smaller, attracts high fees to unlock value from digital twins and multivariate defect data.

Intertek’s EUR 15 million (USD 17.49 million) VR-equipped academy in Düsseldorf demonstrates how providers monetize training by supplying both curricula and simulation suites that mimic field conditions. Equipment makers like Sonatest, now ISO 17025-accredited, leverage calibration certificates as a wedge to sell extended warranties, safeguarding recurring revenue streams. As labor scarcity persists, managed-service contracts increasingly bundle annual certification refreshers, embedding training costs into multiyear inspection packages and further weaving services into the Europe NDT Equipment market fabric.

Geography Analysis

Germany commanded 24.73% of the 2024 regional revenue, driven by stringent automotive quality controls, life-extension programs for its nuclear fleet, and the localized presence of major aerospace assemblies, which gave it the single-largest Europe NDT Equipment market share. Strong domestic R&D underpins early adoption of micro-focus X-ray and AI-assisted defect recognition, and federal apprenticeship pathways produce a comparatively deeper technician bench. However, labor costs and environmental permitting slow the proliferation of new radiography bays, nudging operators toward portable ultrasonic and thermographic solutions that avoid the need for radiation licensing.

Spain is forecast to advance at an 8.32% CAGR through 2030, fueled by wind-blade production and installation cycles that require frequent infrared and ultrasonic scans of composite joints. EU green-energy funding lowers project cost of capital, so developers can allocate larger budgets for condition monitoring. Iberdrola’s mandate for quarterly thermographic surveys on new turbines creates recurring service revenue, and local providers are adding drone fleets to keep pace. Southern regions also modernize rail and highway bridges, injecting intermittent but high-margin phased-array ultrasonic demand to spot fatigue cracks in steel girders.

France, the United Kingdom, and the Netherlands form a second-tier growth cluster characterized by diversified industrial bases. France’s 56-reactor nuclear fleet forces continuous eddy current and ultrasonic checks of steam-generator tubing, committing EDF to ongoing high-resolution equipment purchases. The UK’s North Sea assets sustain steady inspection spending, yet Brexit-driven regulatory divergence adds compliance administration costs that advantage multinational inspection majors. The Netherlands is fast becoming an offshore wind inspection hub, with SGS’s Rotterdam launch of subsea crawler capabilities that scan monopiles at 50-meter depths. Eastern Europe, notably Poland and Romania, benefits from EU cohesion funds, but equipment adoption skews toward mid-range ultrasonic and magnetic particle units given budget sensitivities.

Competitive Landscape

Competitive concentration in the Europe NDT Equipment market remains moderate, with the top 10 vendors controlling roughly 45% of revenue. Waygate Technologies, YXLON, and Evident Europe defend share via proprietary detector stacks and advanced signal-processing patents, enabling them to price at a premium in aerospace, defense, and nuclear verticals. On the service side, Bureau Veritas, Intertek, and SGS accumulate dense laboratory footprints, improving fleet utilization and turnaround times that small local labs struggle to match. A hybrid model has emerged, whereby equipment OEMs lease systems under usage-based contracts, bundling analytics platforms that lock customers in for several years.

M&A activity is brisk as incumbents seek to acquire adjacent capabilities. Bureau Veritas has acquired Advanced Inspection Technologies for GBP 78 million, adding 12 labs and 145 certified technicians specializing in aerospace phased-array procedures. Eddyfi Technologies acquired French eddy current specialist M2M, leveraging its expertise in the high-barrier nuclear steam-generator tube segment. Patent filings at the European Patent Office reveal a 34% year-on-year rise in NDT submissions, mostly covering machine-learning-driven signal interpretation and portable CT with miniaturized X-ray sources.[3]European Patent Office, “Patent Statistics 2024,” epo.org Niche firms push AI-enabled mobile platforms that promise to ease the technician shortage, yet adoption is gradual because certification requires empirical validation in field conditions.

Regional fragmentation persists; language, certification reciprocity, and legacy relationships grant local service firms a defensive moat in Southern Italy, Greece, and the Baltics. Nonetheless, medium-size players risk displacement as pan-European contracts bundle multi-country scopes, and large primes favor suppliers that can deliver harmonized procedures across borders. The competitive direction therefore favors scaled networks paired with proprietary tech or, conversely, hyper-specialized boutiques dominating a narrow modality such as acoustic emission.

Europe NDT Equipment Industry Leaders

-

Waygate Technologies GmbH

-

YXLON International GmbH

-

Evident Europe GmbH (Olympus Corporation)

-

Nikon Metrology NV

-

Eddyfi Europe SAS

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Waygate Technologies launched the Phoenix Microme|x CT system with 0.5-micron resolution and AI defect classification for additive manufacturing quality control.

- November 2024: Bureau Veritas acquired UK-based Advanced Inspection Technologies for GBP 78 million (USD 99 million), strengthening its aerospace inspection network.

- October 2024: Evident Europe introduced the OmniScan X4 phased-array ultrasonic detector featuring encrypted cloud connectivity options aimed at defense customers.

- September 2024: Intertek opened a EUR 15 million (USD 17.49 million) NDT training center in Düsseldorf equipped with VR simulators for accelerated ISO 9712 Level 2 certification.

Europe NDT Equipment Market Report Scope

Non-destructive testing (NDT) instruments are used to scan, inspect, and quantify flaws, corrosion, and other material conditions without permanently damaging or altering the examined product or part. NDT equipment encompasses a broad set of equipment, such as flaw detectors, thickness gages, material condition testers, visual inspection devices, acoustic emission testers, eddy current instruments, and devices that measure resistivity, conductivity, and corrosion. The market study is focused on the trends affecting the market in the Europe region.

The Europe NDT Equipment Market Report is Segmented by Type (Equipment, Services), Testing Technology (Radiography, Ultrasonic, Magnetic Particle, Liquid Penetrant, Visual Inspection, Eddy Current, Acoustic Emission, Thermography), End-User Industry (Oil and Gas, Power and Energy, Aerospace and Defense, Automotive and Transportation, Construction, Manufacturing, Others), Service Type (Inspection Services, Calibration Services, Training Services, Consultancy, Others), and Geography (United Kingdom, Germany, France, Italy, Spain, Netherlands, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Equipment |

| Services |

By Testing Technology

| Radiography |

| Ultrasonic |

| Magnetic Particle |

| Liquid Penetrant |

| Visual Inspection |

| Eddy Current |

| Acoustic Emission |

| Thermography |

By End-User Industry

| Oil and Gas |

| Power and Energy |

| Aerospace and Defense |

| Automotive and Transportation |

| Construction |

| Manufacturing |

| Other End-User Industry |

By Service Type

| Inspection Services |

| Calibration Services |

| Training Services |

| Consultancy |

| Other Service Type |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Russia |

| Rest of Europe |

| By Type | Equipment |

| Services | |

| By Testing Technology | Radiography |

| Ultrasonic | |

| Magnetic Particle | |

| Liquid Penetrant | |

| Visual Inspection | |

| Eddy Current | |

| Acoustic Emission | |

| Thermography | |

| By End-User Industry | Oil and Gas |

| Power and Energy | |

| Aerospace and Defense | |

| Automotive and Transportation | |

| Construction | |

| Manufacturing | |

| Other End-User Industry | |

| By Service Type | Inspection Services |

| Calibration Services | |

| Training Services | |

| Consultancy | |

| Other Service Type | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Europe NDT Equipment market by 2030?

The Europe NDT Equipment market is expected to reach USD 8.76 billion by 2030 based on a 7.97% CAGR projection.

Which testing technology is growing the fastest in Europe?

Thermography is projected to rise at an 8.23% CAGR through 2030 thanks to widespread renewable-energy blade and panel monitoring.

Why are services expanding faster than equipment sales?

Asset owners prefer outcome-based contracts and flexible costs, pushing services to grow at a 9.24% CAGR versus slower equipment expansion.

Which country will record the quickest growth through 2030?

Spain leads with an 8.32% CAGR driven by wind and solar installations that require frequent non-contact inspections.

How is additive manufacturing influencing inspection demand?

Aerospace and medical sectors mandate 100% volumetric checks on printed parts, propelling CT and eddy current uptake and making additive manufacturing the fastest-growing end-user segment at an 8.45% CAGR.

What is the main restraint facing the Europe NDT Equipment market?

A shortage of certified technicians is curbing capacity, shaving an estimated 1.2% from the underlying CAGR outlook.

Page last updated on: