Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 13.29 Billion |

| Market Size (2030) | USD 13.79 Billion |

| Growth Rate (2025 - 2030) | 0.74% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Military Aviation Market Analysis by Mordor Intelligence

The Europe Military Aviation Market size is estimated at 13.29 billion USD in 2025, and is expected to reach 13.79 billion USD by 2030, growing at a CAGR of 0.74% during the forecast period (2025-2030).

The European military aviation landscape has undergone significant transformation, driven by escalating geopolitical tensions and increased defense commitments. Europe's defense expenditure witnessed a substantial surge of 23% from 2021 to 2022, reaching USD 512 billion, with military research and development and weaponry purchases accounting for the majority of this growth. The commitment to defense spending is further evidenced by the fact that 26 out of 27 European NATO nations secured financing for their armed forces in 2022, with eight member states achieving NATO's target of allocating at least 2% of their GDP to military spending. This unprecedented increase in defense budgets reflects the region's growing focus on military modernization and strategic capabilities enhancement.

Fleet modernization initiatives have become a cornerstone of European military aviation strategy, with countries actively pursuing the replacement of aging military aircraft with next-generation platforms. The fixed-wing aircraft segment has witnessed substantial procurement activities, particularly in combat aircraft acquisition. Major European powers are investing heavily in advanced fighter jets, transport aircraft, and special-mission platforms to enhance their operational capabilities and maintain technological superiority. These modernization efforts are complemented by increased investments in military research and development, fostering innovation in aircraft design, avionics, and combat systems.

The rotorcraft segment is experiencing a parallel transformation, with European nations placing significant emphasis on multi-mission military helicopter capabilities. The region's commitment to helicopter fleet modernization is reflected in the comprehensive procurement plans spanning from 2023 to 2029, with multiple countries including Germany, France, the United Kingdom, and Italy leading major acquisition programs. These initiatives focus on enhancing combat capabilities, improving operational effectiveness, and ensuring interoperability with NATO and allied forces through the integration of state-of-the-art military helicopter platforms.

The European military aerospace industry is characterized by strong international collaboration and strategic partnerships. Major defense contractors are actively engaged in joint development programs, technology transfers, and industrial cooperation agreements. This collaborative approach has fostered innovation in aircraft design, propulsion systems, and advanced avionics. The industry's focus on developing indigenous capabilities while maintaining strategic partnerships has resulted in the emergence of sophisticated defense aircraft platforms that meet the evolving requirements of modern warfare and address the complex security challenges facing the region.

Europe Military Aviation Market Trends and Insights

NATO alliances are contributing to the region's defense spending

- In 2022, Europe spent USD 480 billion on its military, a 13% increase over 2021 and a 38% increase over 2013. In 2022, Europe accounted for 21% of the total defense expenditure in the world. In 2021, Central and Western Europe's combined military expenditure totaled USD 345 billion (USD 305 billion for Western Europe and USD 45 billion for Central Europe), including most NATO allies and all of the EU member states.

- Increased expenditures on military R&D and arms purchases were the main drivers of the surge in military spending in Central and Western Europe. In 2022, defense expenditures in Eastern Europe increased to USD 76.3 billion. In 2022, 19 European NATO member nations, up from five in 2014 and 13 in 2020, dedicated a minimum of 20% of their defense spending to arms purchases and military R&D.

- In 2022, these member states' average proportion of defense spending on weapons and R&D increased to 24% from 22% in 2020 and 14% in 2014. Only two of the 26 NATO members in Europe with a military budget, Albania and Estonia, did not increase the portion of their budgets devoted to arms purchases and R&D from 2014 to 2021. By the end of March 2022, numerous European NATO member nations announced plans to increase military expenditure in response to the Russian invasion of Ukraine in February 2022, aiming to meet or exceed the NATO spending target of 2% of the GDP or higher. Belgium, Denmark, Germany, Lithuania, the Netherlands, Norway, Poland, and Romania were members of this group. These budgets were expected to be centered on the purchase of new armaments.

Understand The Key Trends Shaping This Market

Download PDF

Fixed-wing aircraft accounted for 54% of the total fleet in the European military aviation market

- As of 2022, there were 8,326 active aircraft in Europe, of which fixed-wing aircraft accounted for 58% and rotorcraft for 42%. The total active aircraft fleet increased by 4% compared to 2016 in the region. Russia, the United Kingdom, the Netherlands, Germany, Italy, Spain, and France accounted for 95% of the total active fleet in the region.

- The fixed-wing aircraft and multi-role aircraft segments accounted for 54%, while transport aircraft, training aircraft, and others accounted for 16%, 23%, and 7%, respectively. In 2021, the active fleet of fixed-wing aircraft decreased by 3% compared to 2016. In rotorcraft, multi-mission helicopters accounted for 38%, while transport helicopters and other helicopters accounted for 30% and 32%, respectively. In 2021, the active fleet of rotorcraft increased by 1% compared to 2016.

- As of 2022, the average age of the Russian aircraft fleet was 10.5 years. The Yakovlev Yak-42 jets had the highest average age of any type of aircraft, at nearly 28 years. During the forecast period, the United Kingdom, Germany, France, Italy, and Spain may continue to build and buy next-generation aircraft to meet the demands of modern warfare. The regional armed forces are also upgrading the capabilities of helicopters with cutting-edge technology to achieve military superiority over possible invaders. The UK Ministry of Defence plans to retire several aging aircraft; however, it needs to actively continue the procurement of replacement aircraft to avoid any gaps within the fleet. The country's continued support for Ukraine in its war with Russia may add pressure on its defense budget. This factor may threaten the country's usual place as Europe’s largest defense spender.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The Ukraine-Russia War is expected to improve defense contribution, even with economic growth uncertainty

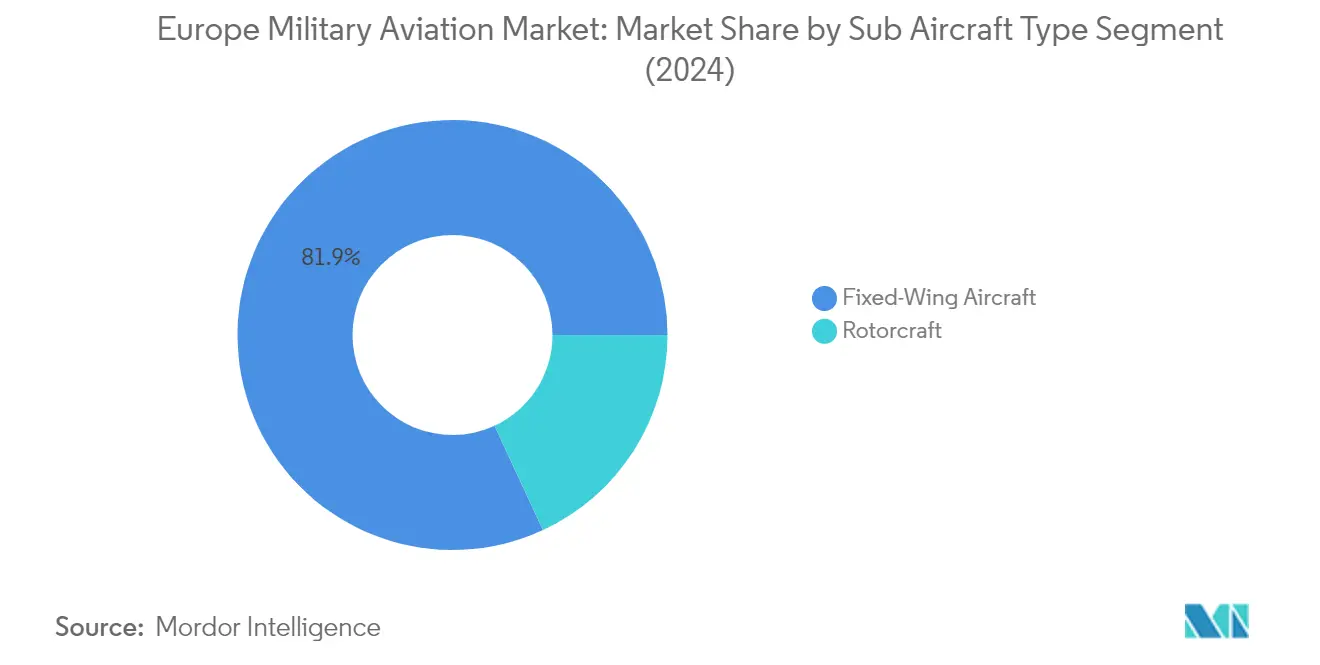

Segment Analysis: Sub Aircraft Type

Fixed-Wing Aircraft Segment in Europe Military Aviation Market

The fixed-wing aircraft segment dominates the European military aviation market, accounting for approximately 82% of the total market value in 2024. This significant market share is primarily driven by the extensive procurement of fighter aircraft and multi-role combat aircraft by major European nations to strengthen their air defense capabilities. Countries like France, Germany, and the UK are actively modernizing their fixed-wing fleets through various procurement programs, including next-generation fighter aircraft and advanced training platforms. The segment's dominance is further reinforced by the increasing focus on territorial defense and air superiority requirements among NATO member states, particularly in response to evolving regional security dynamics.

Rotorcraft Segment in Europe Military Aviation Market

The rotorcraft segment is experiencing robust growth in the European military aviation market, with a projected growth rate of approximately 4% from 2024 to 2029. This growth is primarily driven by increasing investments in military helicopter fleets across European nations, particularly for multi-mission and transport applications. The segment's expansion is supported by several major procurement programs, including Germany's heavy-lift helicopter acquisition plans and France's military helicopter modernization initiatives. The growing emphasis on tactical mobility, search and rescue capabilities, and maritime operations is further accelerating the demand for military rotorcraft across the region.

Europe Military Aviation Market Geography Segment Analysis

Europe Military Aviation Market in Russia

Russia maintains its dominant position in the European military aircraft landscape, commanding approximately 17% of the market share in 2024. The country's military aviation capabilities are undergoing significant transformation with a focus on modernizing its aircraft fleet and enhancing operational effectiveness. Russia's strategic emphasis on developing indigenous aircraft manufacturing capabilities has strengthened its position in both fixed-wing and rotorcraft segments. The country's commitment to military modernization is evident in its procurement strategies, particularly in the development and acquisition of next-generation combat aircraft. Russia's military aviation sector benefits from a robust domestic manufacturing base, with several key production facilities dedicated to both combat and transport aircraft. The country's focus on developing advanced avionics systems and military technologies has further reinforced its position in the European military aviation market. Additionally, Russia's continued investment in research and development has led to innovations in aircraft design and capabilities, particularly in the areas of stealth technology and advanced propulsion systems.

Europe Military Aviation Market in Germany

Germany's military aviation market is experiencing remarkable growth, with a projected CAGR of approximately 37% from 2024 to 2029. The country's strategic shift towards modernizing its air force has catalyzed significant investments in new aircraft acquisitions and upgrades. Germany's focus on enhancing its military aviation capabilities is driven by its commitment to NATO obligations and the need to address evolving security challenges in the region. The country has implemented comprehensive fleet modernization programs, encompassing both fixed-wing aircraft and military helicopters. Germany's military aviation sector is characterized by strong partnerships with leading European aircraft manufacturers and a focus on acquiring advanced multi-role aircraft. The country's emphasis on developing maintenance, repair, and overhaul (MRO) capabilities has created a robust support infrastructure for its military aviation fleet. Furthermore, Germany's investment in training facilities and simulation technologies has strengthened its position as a key player in military aviation training within Europe.

Europe Military Aviation Market in France

France continues to be a pivotal player in the European military aviation sector, with a strong focus on maintaining technological sovereignty in aerospace capabilities. The country's military aviation strategy emphasizes the development and acquisition of advanced combat aircraft and support systems. France's commitment to maintaining a diverse fleet of military aircraft reflects its global military responsibilities and strategic interests. The country's robust aerospace industry, supported by leading manufacturers and research institutions, enables continuous innovation in military aviation technologies. France's military aviation capabilities are enhanced by its strong focus on pilot training programs and operational readiness. The nation's strategic emphasis on developing both manned and unmanned aerial systems demonstrates its forward-looking approach to military aviation. Additionally, France's collaborative approach to military aviation programs with other European nations has strengthened its position in the regional aerospace sector.

Europe Military Aviation Market in Spain

Spain has established itself as a significant force in the European military aviation market, with a comprehensive approach to modernizing its air capabilities. The country's military aviation strategy focuses on maintaining a balanced fleet of combat, transport, and training aircraft. Spain's participation in multinational military aviation programs has strengthened its aerospace capabilities and industrial base. The nation's investment in military aviation infrastructure, including maintenance facilities and training centers, supports its growing fleet requirements. Spain's focus on developing specialized capabilities in areas such as aerial refueling and maritime patrol has enhanced its strategic importance in European defense operations. The country's commitment to modernizing its helicopter fleet demonstrates its recognition of the importance of rotary-wing capabilities in modern military operations. Furthermore, Spain's emphasis on developing domestic aerospace capabilities has created opportunities for technology transfer and industrial growth.

Europe Military Aviation Market in Other Countries

The military aviation market in other European countries, including Italy, the United Kingdom, the Netherlands, and Turkey, demonstrates diverse approaches to air force modernization and capability development. These nations are actively pursuing fleet renewal programs and capability enhancements aligned with their specific defense requirements and NATO commitments. Many of these countries are focusing on specialized capabilities, such as maritime patrol aircraft and advanced training systems. The emphasis on interoperability with NATO standards has driven procurement decisions and modernization efforts across these nations. Regional cooperation in military aviation programs has fostered technology sharing and industrial collaboration among these countries. Their collective approach to military aviation modernization contributes to the overall strength of European air defense capabilities. These nations are also investing in support infrastructure and training facilities to maintain their military aviation capabilities effectively.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Europe Military Aviation Market

The European military aviation market is characterized by continuous innovation and strategic developments among major players like Airbus SE, Lockheed Martin, Dassault Aviation, and Boeing. Companies are focusing on developing next-generation defense aircraft with advanced capabilities, including stealth technology, enhanced avionics, and improved fuel efficiency. The industry witnesses frequent collaborations and partnerships to strengthen technological capabilities and expand market presence, particularly in emerging defense segments. Manufacturers are increasingly investing in sustainable aviation technologies and digital transformation initiatives to maintain a competitive advantage. Operational agility is demonstrated through flexible production systems and robust supply chain networks spanning multiple countries. Strategic expansion moves include establishing regional manufacturing facilities, service centers, and training academies to better serve local defense requirements and ensure long-term market presence.

Market Dominated by European Defense Giants

The European military aviation market exhibits a highly consolidated structure dominated by established aerospace and defense conglomerates with deep historical roots in the region. These companies leverage their extensive experience, technological expertise, and strong relationships with defense ministries to maintain market leadership. Local players hold significant advantages due to their understanding of regional defense requirements and established infrastructure networks. The market is characterized by high entry barriers due to substantial capital requirements, complex regulatory frameworks, and the need for specialized technological capabilities.

The industry landscape is shaped by strategic alliances and joint ventures between major players to share development costs and technological expertise. Cross-border collaborations are common, particularly for large-scale military aircraft programs, enabling companies to combine their strengths and serve multiple markets efficiently. The market sees limited pure-play specialists, as most successful players are diversified across multiple aerospace and defense segments, allowing them to better manage market cyclicality and defense budget fluctuations.

Innovation and Collaboration Drive Future Success

Success in the European military aerospace market increasingly depends on companies' ability to innovate while maintaining cost efficiency. Incumbent players must focus on developing cutting-edge technologies while strengthening their existing relationships with defense agencies and supply chain partners. Companies need to invest in emerging technologies like artificial intelligence, autonomous systems, and advanced materials to maintain their competitive edge. Building flexible manufacturing capabilities and establishing strong aftermarket service networks are crucial for long-term success.

For contenders looking to gain market share, focusing on specialized niches and developing unique technological capabilities offers the most promising path forward. Building strategic partnerships with established players and local suppliers can help overcome entry barriers and gain market access. Companies must also consider potential regulatory changes, particularly regarding defense exports and technology transfers, while developing their market strategies. The increasing focus on standardization across European defense forces presents opportunities for players who can offer interoperable solutions while meeting specific national requirements.

Europe Military Aviation Industry Leaders

-

Airbus SE

-

Dassault Aviation

-

Lockheed Martin Corporation

-

The Boeing Company

-

United Aircraft Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2023: Airbus Flight Academy Europe, a subsidiary of Airbus that supplies training services for the pilots and civilian cadets of the French Armed Forces, signed a memorandum of understanding (MoU) with AURA AERO.

- May 2023: The US State Department approved a potential sale of CH-47 Chinook helicopters, engines, and equipment worth USD 8.5 billion to Germany.

- March 2023: Boeing has been awarded a contract by the US government to manufacture 184 AH-64E Apache attack helicopters for the US military and international customers. The US government announced USD 1.95 million, indicating that the helicopter will be delivered to the US military and overseas buyers - specifically Australia and Egypt - as a part of the paramilitary process to the Foreign Service (FMS) from the US government. Contract completion is expected by the end of 2027.

Europe Military Aviation Market Report Scope

Fixed-Wing Aircraft, Rotorcraft are covered as segments by Sub Aircraft Type. France, Germany, Italy, Netherlands, Russia, Spain, Turkey, UK are covered as segments by Country.

Sub Aircraft Type

| Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | |

| Transport Aircraft | |

| Others | |

| Rotorcraft | Multi-Mission Helicopter |

| Transport Helicopter | |

| Others |

Country

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Turkey |

| UK |

| Rest of Europe |

| Sub Aircraft Type | Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Others | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Others | ||

| Country | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| UK | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - All the military aircraft and rotorcraft which are used for various applications are included in this study.

- Sub-Aircraft Type - For this study, sub-aircraft types such as fixed-wing aircraft and rotorcraft based on their application are considered.

- Body Type - Multi-Role Aircraft, Transport, Training Aircraft, Bombers, Reconnaissance Aircraft, Multi-Mission Helicopters, Transport Helicopters and various other aircraft and rotorcraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF