Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

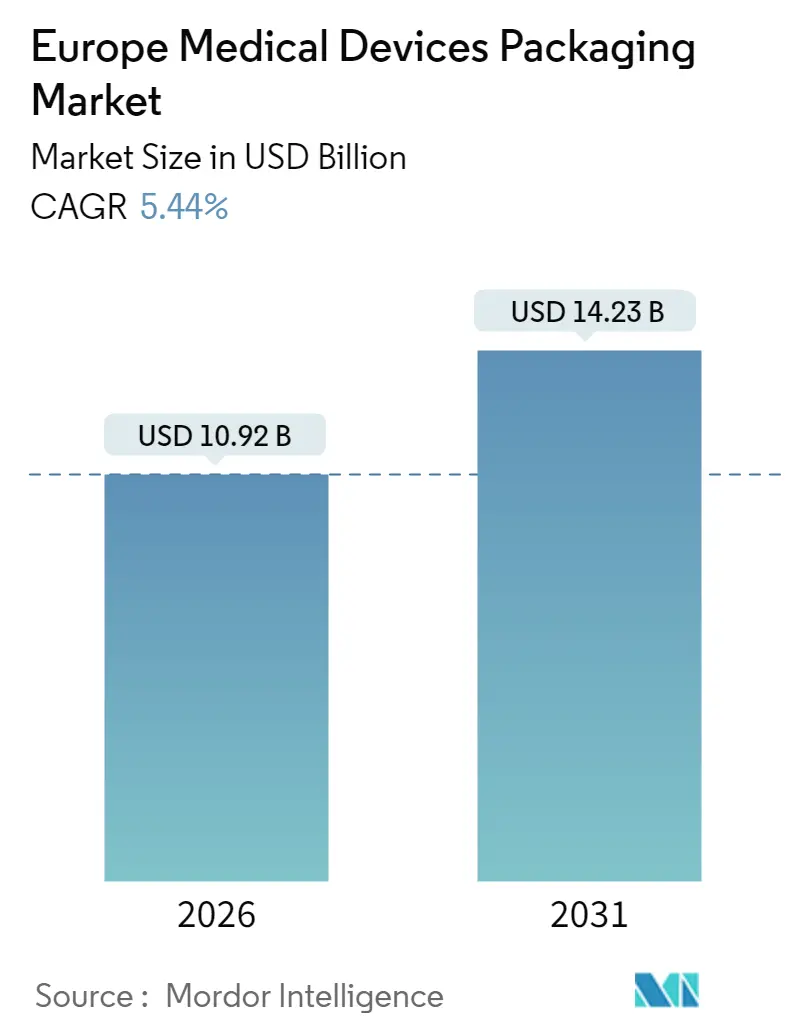

| Market Size (2026) | USD 10.92 Billion |

| Market Size (2031) | USD 14.23 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

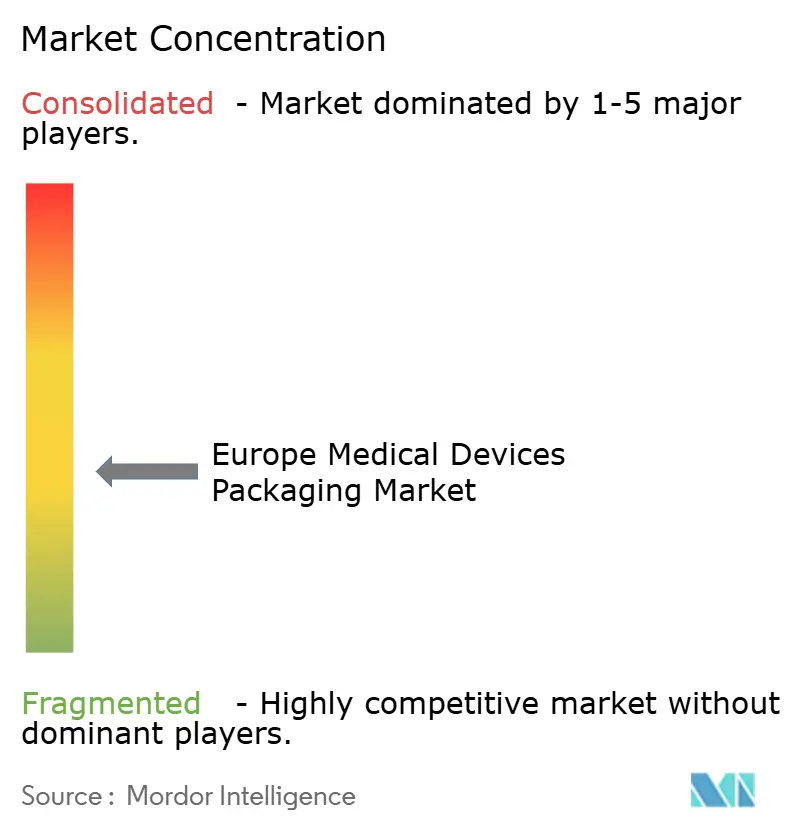

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medical Devices Packaging Market Analysis by Mordor Intelligence

Europe Medical Devices Packaging market size in 2026 is estimated at USD 10.92 billion, growing from 2025 value of USD 10.36 billion with 2031 projections showing USD 14.23 billion, growing at 5.44% CAGR over 2026-2031. Demand is underpinned by strict EU Medical Device Regulation (MDR) requirements that push for unique device identification, higher traceability, and serialized labeling. Investments in smart labeling, sterile-barrier innovations, and bio-based materials continue to rise as manufacturers align with the EU Packaging and Packaging Waste Regulation. Germany keeps its lead through deep manufacturing capabilities, while Spain’s rapid healthcare digitalization fuels expansion. Sustainability programs, growing home-healthcare adoption, and device miniaturization collectively amplify opportunities for the Europe Medical Devices Packaging market, even as polymer price volatility and recycling infrastructure gaps temper gains.

Key Report Takeaways

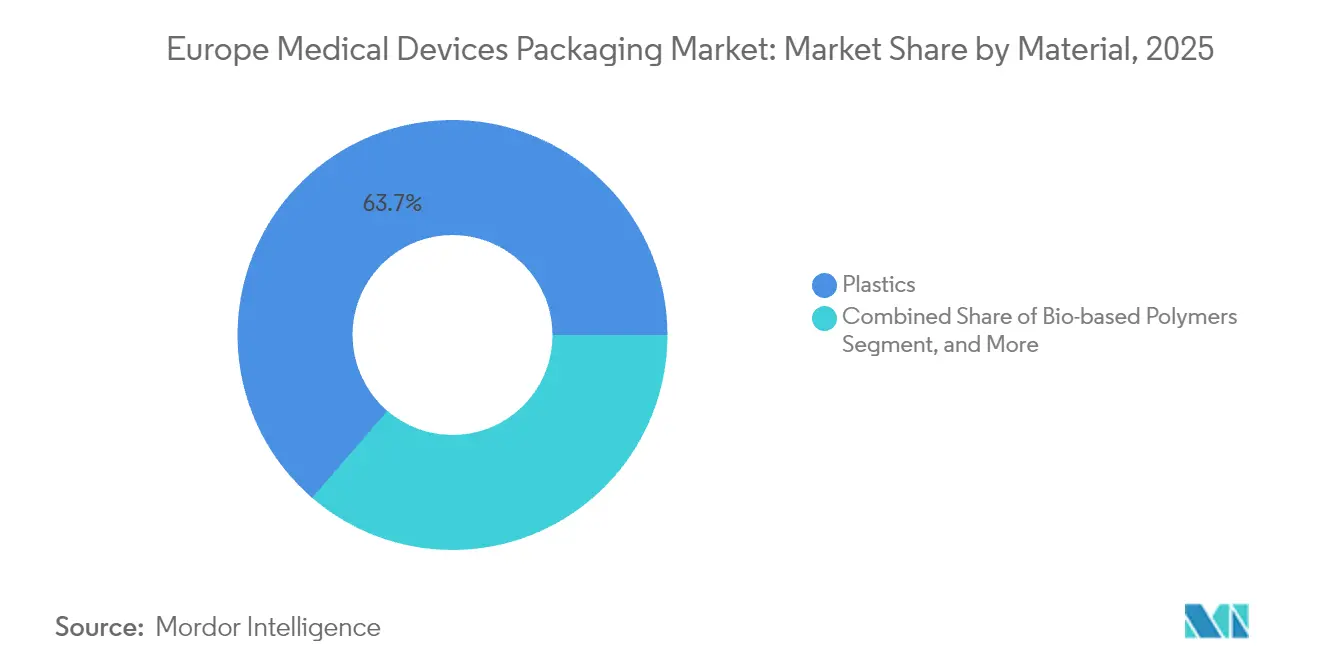

- By material, plastics led with 63.68% of Europe Medical Devices Packaging market share in 2025; bio-based polymers are forecast to expand at an 8.28% CAGR through 2031.

- By packaging format, pouches and bags captured 35.10% of Europe Medical Devices Packaging market size in 2025, while trays and clamshells are set to climb at a 7.29% CAGR to 2031.

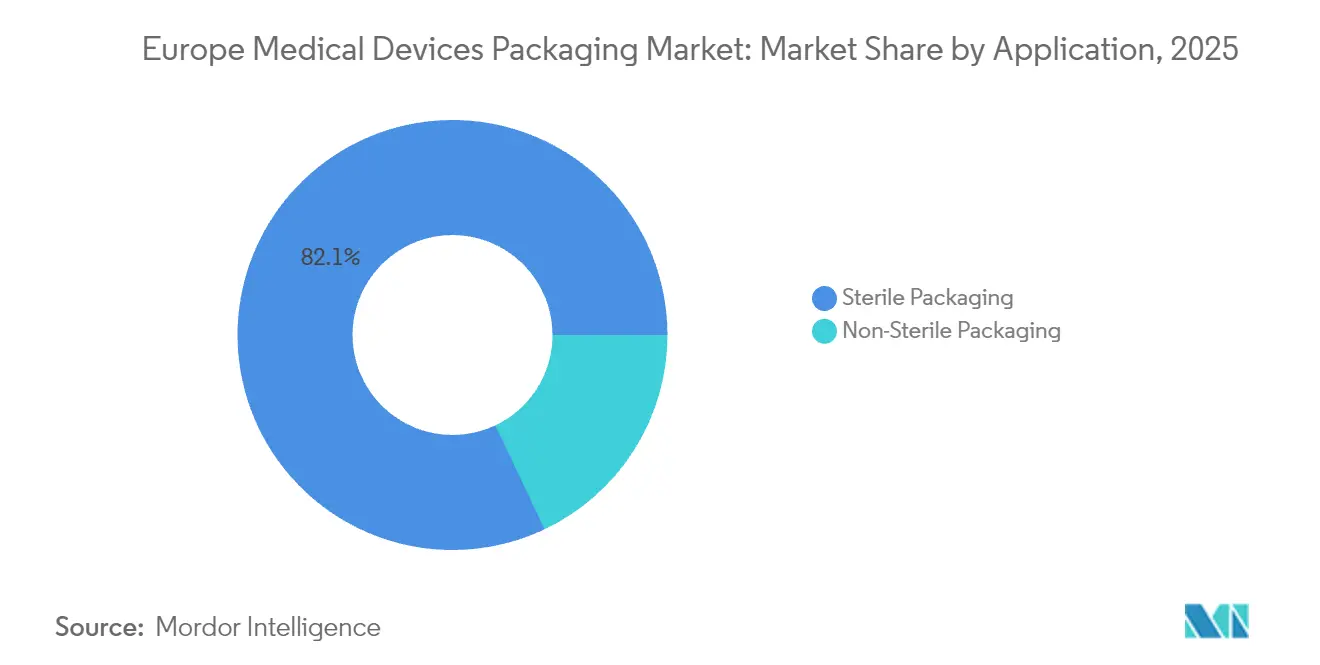

- By application, sterile packaging accounted for 82.05% of the Europe Medical Devices Packaging market size in 2025 and is advancing at a 6.12% CAGR through 2031.

- By end user, hospitals and clinics held 46.42% revenue share in 2025; home-health settings exhibit the highest projected CAGR at 7.73% through 2031.

- By country, Germany led with 22.30% market share in 2025, whereas Spain posted the fastest growth at an 8.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer shelf-life demands | +0.8% | Germany, France | Medium term (2-4 years) |

| Device miniaturization | +1.2% | EU manufacturing hubs | Short term (≤2 years) |

| MDR traceability and UDI | +1.5% | EU-wide | Long term (≥4 years) |

| Home-based monitoring growth | +1.1% | Urban EU centers | Medium term (2-4 years) |

| Sustainability mandates | +0.9% | Nordic countries lead | Long term (≥4 years) |

| AI-enabled inline inspection | +0.6% | Germany, Switzerland | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

MDR Traceability and UDI Labeling Requirements

EU MDR enforcement drives investment in serialization, smart labels, and digital identifiers that secure full supply-chain visibility. The Commission’s phased UDI rollout through 2028 guarantees steady spending on high-resolution on-pack codes and human-readable data. German converters now embed oxygen-barrier labels that integrate UDI data and maintain drug stability, illustrating how regulatory needs and performance targets converge. Large device OEMs demand suppliers with ISO 13485-aligned quality systems, propelling specialized printers and sensor-label innovators. European plants also leverage cloud-based tracking to cut recall risk. As compliance costs climb, vendors offering turnkey MDR-ready packaging gain a competitive edge across the Europe Medical Devices Packaging market.

Accelerating Device Miniaturization Driving Innovative Pack Formats

Ultra-compact catheter assemblies and implantables require thin-wall thermoformed trays able to tolerate gamma, steam, or nitrogen-oxide sterilization without collapse. Microsystems tooling developed for wearables transfers effectively to packaging, giving converters flexibility in geometry control. Research on BioMEMS shows demand for biocompatible substrates that deliver moisture protection while supporting wireless telemetry. [1]Vibhor Kumar, “Advancements in Wearable and Implantable BioMEMS Devices,” MDPI, mdpi.com OEMs lean on quick-change forming lines that swap pocket depths mid-run to handle mixed kit SKUs. Regulatory bodies now draft size-specific vibration and drop-test protocols, guiding material selection. These pressures collectively push the trays and clamshells segment of the Europe Medical Devices Packaging market toward high-value engineering solutions.

Growth of Home-based and Remote Patient Monitoring Devices

Home-health monitoring expands packaging needs that prioritize self-administration, tamper evidence, and intuitive opening cues. Smart glucose and cardiac patches shipped in rigid-flex carriers guard delicate antennas and batteries yet let seniors peel film without tools. Manufacturers such as Gerresheimer offer large-volume wearable injectors requiring protective but breathable over-wraps that prevent condensation over multi-day use. Bluetooth modules inside on-body devices demand electromagnetic shielding during transit, creating hybrid pack designs of metallized plastics and molded pulp inserts. As reimbursement rules encourage at-home treatment, user-centric packs increase volumes within the Europe Medical Devices Packaging market.

Sustainability Mandates Boosting Recyclable and Bio-based Packs

EU circular-economy law compels converters to demonstrate recyclability or renewable content by 2030. Bio-PVC certified under ISCC PLUS now matches legacy sterilization performance while cutting life-cycle emissions by up to 90%. [2]TekniPlex Healthcare, “ISCC PLUS Bio-PVC Launch,” tekniplex.com Suppliers scale mono-material high-barrier films that replace complex laminates and feed directly into RIC 1 streams once used. Chemical-recycling pilots in Belgium target sterilization wrap, aspiring to closed-loop feeds for medical-grade resin. Nordic hospitals already tender contracts factoring carbon intensity, prompting rapid switchovers inside the Europe Medical Devices Packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-layer EU compliance costs | -1.8% | SMEs EU-wide | Long term (≥4 years) |

| Polymer price volatility | -1.3% | Import-dependent EU | Short term (≤2 years) |

| Limited recycling for multi-material packs | -0.9% | Eastern Europe | Medium term (2-4 years) |

| Carbon-reduction targets shrinking blister use | -0.7% | Germany, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-layer EU Regulations and Compliance Costs

Small converters face overlapping MDR, Packaging Waste, and language-label directives that demand capital-intensive validation and multilingual artwork. Notified-body backlogs slow certificate renewals, stretching lead times and tying up working capital. Firms allocate engineers to maintain EUDAMED submissions, diverting resources from R&D. High upfront documentation burdens encourage outsourcing, yet partnership vetting adds further complexity. These hurdles disproportionately affect SMEs, restraining supply expansion in the Europe Medical Devices Packaging market.

Polymer Raw-material Price Volatility

Polypropylene and PVC track crude oil swings, and 2024 spot hikes exceeded prior contracts by double-digit percentages, straining margins. [3]British Plastics Federation, “Polymer Price Report March 2024,” bpf.co.uk European pack converters also wrestled with energy-cost spikes that triggered temporary shutdowns. OEMs countered volatility via multi-year supply pacts, trading flexibility for predictability. Elevated resin prices accelerate the search for bio-attributed and mechanically recycled alternatives, yet stringent traceability screens slow swift substitution.

Segment Analysis

By Material: Bio-based Innovation Challenges Plastic Dominance

Plastics retained 63.68% of Europe Medical Devices Packaging market share in 2025, as established sterilization compatibility and cost efficiency kept demand high. Over the forecast horizon, bio-based polymers will deliver 8.28% CAGR, reflecting EU sustainability goals and advancements such as MedEco renewable-content resins. Paperboard remains entrenched for secondary packs, while metals fill niche barrier roles in implantables needing ultra-low permeability.

Manufacturers now run twin-screw extruders that co-process bio-attributed feedstocks without requalifying entire lines, easing transition risks. Investments in chemical recycling scale pilot volumes capable of producing virgin-grade styrene for medical apps. These advances position bio-materials to capture incremental volumes, reshaping long-term material mix inside the Europe Medical Devices Packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Miniaturization Drives Tray Innovation

Pouches and bags led with 35.10% Europe Medical Devices Packaging market size in 2025 due to versatility across catheter sets and surgical kits. Tray and clamshell formats will outpace others at 7.29% CAGR as micro-electronics push for precise cavity protection. Thin-wall thermoforming lines now achieve 60% resin savings without compromising stack strength, shrinking logistics costs.

High-clarity PETG trays that integrate molded lid channels enhance sterile integrity under ethylene-oxide cycles and eliminate lidding delamination. Smart sensors embedded in tray corners log temperature excursions, aligning with MDR post-market surveillance rules. These traits propel tray uptake among cardiovascular and neuro device OEMs, sustaining growth across the Europe Medical Devices Packaging market.

By Application: Sterile Dominance Reflects Safety Imperatives

Sterile packaging commanded 82.05% share in 2025 and heads toward 6.12% CAGR as home therapy volume rises. ISO 11607 revisions demand quantitative seal-strength evidence, driving adoption of vacuum-based rigid containers that outperform porous wraps. Non-sterile packs persist for diagnostic disposables, but hybrid solutions emerge for partially invasive wearables.

Nitric-oxide sterilization offers lower temperature alternatives for electronics-laden devices, widening material choices beyond high-heat polymers. Monitoring kits now ship in dual-chamber pouches separating reagents until activation, extending shelf life in uncontrolled environments. These innovations reinforce sterile packaging’s centrality to the Europe Medical Devices Packaging market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home Healthcare Reshapes Usage Patterns

Hospitals and clinics still account for 46.42% demand, yet home-health settings will record the highest 7.73% CAGR. Large-volume patch pumps require tamper-evident carriers that elderly users can access without scissors, driving ergonomic redesign. Refill cartridges for on-body injectors now feature smart RFID seals enabling automatic inventory checks within pharmacy cabinets.

Contract manufacturing organizations expand clean-room capacity to serve OEMs outsourcing packaging to manage MDR overhead. Diagnostic labs specify pre-barcoded tubes that streamline track-and-trace, intersecting with UDI mandates. Together these shifts diversify consumption across the Europe Medical Devices Packaging market.

Geography Analysis

Germany’s dominance arises from its integrated machinery cluster, ensuring vertical control from resin extrusion to automated cartoning. Plants operate predictive-maintenance programs that reduce downtime and bolster dependable supply. Regulatory authorities collaborate closely with industry on MDR interpretations, accelerating approval cycles and keeping domestic converters at the forefront.

Spain’s rapid expansion rides on state-backed digital health pilots that include remote monitoring kits for chronic care. These programs need intuitive, lightweight packs suited to courier networks reaching rural patients. Domestic converters invest in ISCC-certified bio-PVC to comply with EU circularity mandates, enhancing their attractiveness to export-oriented OEMs.

Mature markets in the United Kingdom, France, Italy, and the Netherlands each exhibit specialty strengths. Post-Brexit, UK firms offer dual-regime labeling expertise. France, housing large biologics producers, prioritizes high-barrier cyclic-olefin polymers that endure cold-chain transport. Italian flexible-film suppliers drive cost efficiencies, while Dutch sterilization hubs expedite pan-EU distribution within tight time windows. Collectively, these nations sustain incremental gains that stabilize overall revenues of the European Medical Devices Packaging market.

Competitive Landscape

The Europe Medical Devices Packaging market remains moderately fragmented, with global players Amcor, Constantia Flexibles, and Klöckner Pentaplast competing through material science innovations and pan-EU regulatory services. DuPont’s 2024 acquisition of Donatelle Plastics expanded its precision-medical portfolio, signaling consolidation that favors scale and specialized know-how. Klöckner Pentaplast’s launch of fully recyclable kpNext films aligns with customers’ sustainability KPIs, differentiating its offer.

Mid-tier converters focus on niche segments such as ultra-small trays for neurostimulation implants or RFID-ready labels for infusion pumps. AI-driven inspection and cleanroom robotics emerge as key investment areas that raise quality while limiting labor dependency. Suppliers with in-house recycling lines capture OEMs seeking closed-loop solutions.

Start-ups explore printed-electronics labels measuring shock, humidity, and temperature, adding post-market surveillance value. Partnerships between material innovators and machinery providers shorten scale-up times, fostering quick response to regulatory tweaks. The net result is vigorous competition centered on compliance agility, digital features, and carbon-footprint metrics within the Europe Medical Devices Packaging market.

Europe Medical Devices Packaging Industry Leaders

Amcor PLC

Constantia Flexibles

Smurfit WestRock

DuPont de Nemours Inc.

Mondi Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SCHOTT Pharma launched its next-generation TOPPAC infuse polymer syringe system with RFID-ready functional labels for automated hospital inventory.

- January 2025: Harpak-ULMA introduced the ARTIC SS Chevron flow-wrap machine that forms aseptic seals from a single film, reducing material use and processing steps.

- December 2024: Körber Business Area Pharma acquired Wilhelm Bähren to integrate labels and leaflets into its secondary-pack offering.

- November 2024: DuPont unveiled Tyvek with Renewable Attribution, replacing fossil feedstock with certified bio-circular inputs while retaining sterile-barrier performance.

Europe Medical Devices Packaging Market Report Scope

The medical devices packaging market is growing as the healthcare industry has witnessed rapid changes over time with the outbreak of new diseases, growth in regulatory norms, and growth in advanced healthcare systems. This has resulted in the implementation of a standardized packaging process where flexible packaging demand is growing in sterile and non-sterile packaging applications.

By Material

| Plastics |

| Paper and Paperboard |

| Metal |

| Bio-based Polymers |

By Packaging Type

| Pouches and Bags |

| Trays and Clamshells |

| Boxes and Cartons |

| Other Packaging Type |

By Application

| Sterile Packaging |

| Non-Sterile Packaging |

By End-User

| Hospitals and Clinics |

| Home-Health Settings |

| Diagnostic Centres and Laboratories |

| Contract Manufacturing Organisations (CMOs and CDMOs) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Material | Plastics |

| Paper and Paperboard | |

| Metal | |

| Bio-based Polymers | |

| By Packaging Type | Pouches and Bags |

| Trays and Clamshells | |

| Boxes and Cartons | |

| Other Packaging Type | |

| By Application | Sterile Packaging |

| Non-Sterile Packaging | |

| By End-User | Hospitals and Clinics |

| Home-Health Settings | |

| Diagnostic Centres and Laboratories | |

| Contract Manufacturing Organisations (CMOs and CDMOs) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe Medical Devices Packaging market in 2026?

It is valued at USD 10.92 billion, with a projected 5.44% CAGR to 2031.

Which material dominates device packaging across Europe?

Plastics lead with 63.68% market share due to reliable sterile-barrier performance.

What drives the shift toward trays and clamshells?

Device miniaturization and the need for precise protection push trays to a 7.29% CAGR.

Why are home-health settings important for packaging providers?

Rapid adoption of remote monitoring and wearable injectors boosts demand for user-friendly, tamper-evident packs growing at 7.73% CAGR.

How do EU regulations impact packaging specifications?

MDR mandates serialization, UDI labeling, and strict quality validation, prompting heavy investment in smart labels and compliant materials.

What role does sustainability play in material choice?

EU circular-economy rules favor recyclable mono-materials and bio-based polymers, ca

Page last updated on: