Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

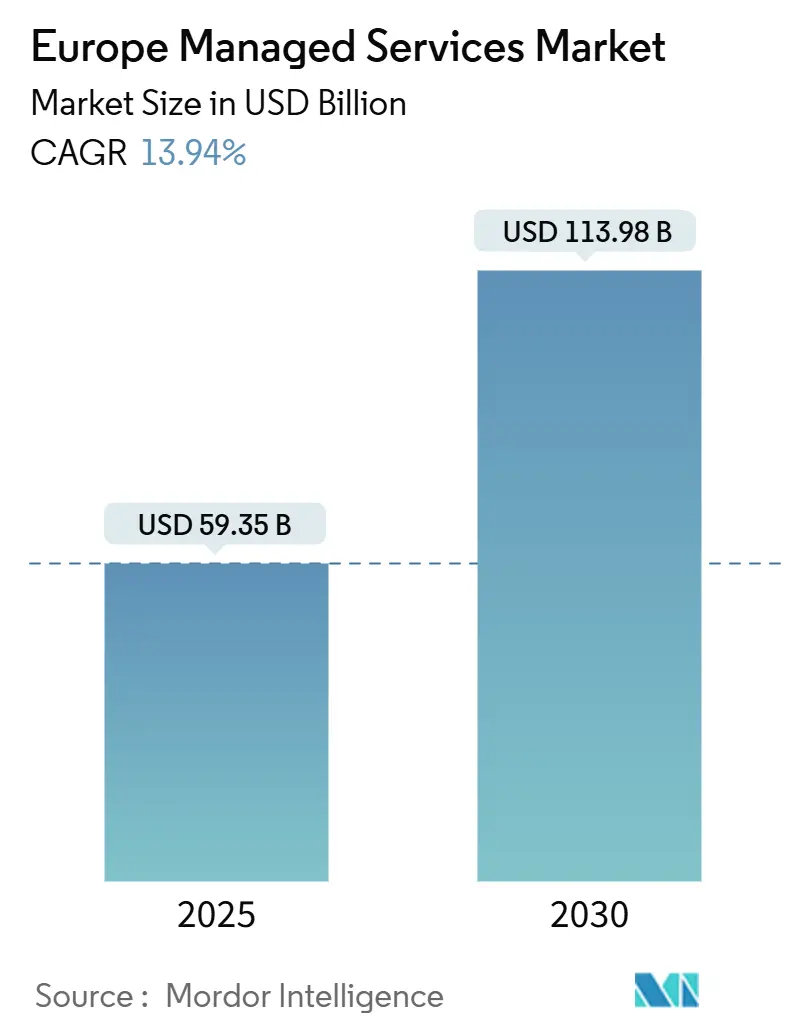

| Market Size (2025) | USD 59.35 Billion |

| Market Size (2030) | USD 113.98 Billion |

| Growth Rate (2025 - 2030) | 13.94% CAGR |

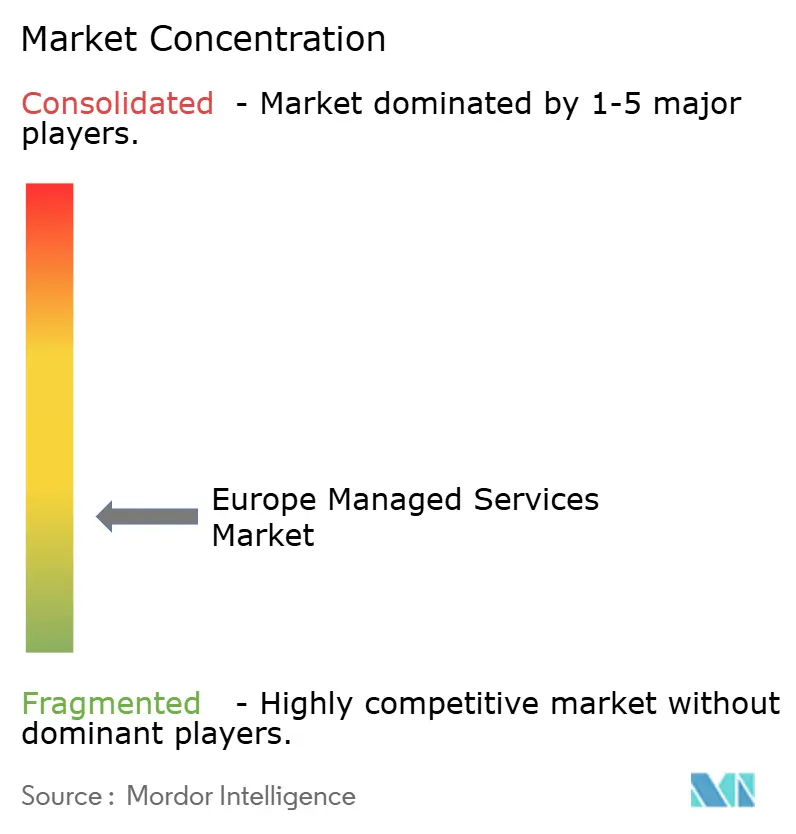

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Managed Services Market Analysis by Mordor Intelligence

Europe managed services market size stands at USD 59.35 billion in 2025 and is forecast to climb to USD 113.98 billion by 2030, reflecting a 13.94% CAGR through the period. Accelerated cloud migration, mounting cybersecurity pressure, and widening skills gaps underpin the rise in demand, while recent regulations such as the EU Digital Operational Resilience Act (DORA) amplify the need for compliant, round-the-clock support.[1]SAI360 Editorial Team, “EU DORA,” SAI360, sai360.com Sovereign-cloud initiatives, including AWS’s long-term European Sovereign Cloud investment program, reinforce regional data-residency expectations that favor providers with local infrastructure footprints. Heightened hacktivist activity, 96% of recorded attacks since early 2022 have targeted European infrastructure, continues to steer budgets toward managed security offerings. Finally, persistent energy-price swings push enterprises to favor service partners that can blend workload flexibility with transparent power-efficiency reporting, helping stabilize operating expenses.

Key Report Takeaways

- By deployment model, cloud captured 58.62% revenue share in 2024 in the Europe managed services; hybrid/hosted is advancing at a 14.87% CAGR to 2030.

- By service type, managed security held 29.61% of Europe managed services market share in 2024, while managed cloud and application services are projected to expand at 14.62% CAGR through 2030.

- By enterprise size, large enterprises accounted for 62.76% of the Europe managed services market size in 2024; small and medium enterprises are progressing at 15.03% CAGR to 2030.

- By end-user vertical, BFSI led with 24.53% share in 2024 in the Europe managed services; healthcare and life sciences are tracking a 14.21% CAGR to 2030.

- By country, the United Kingdom retained 26.82% share in 2024 in the Europe managed services, whereas Germany is expected to post the quickest 14.43% CAGR through 2030

Europe Managed Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of hybrid and multi-cloud architectures | +3.2% | Global, with Nordic leadership in cloud-first strategies | Medium term (2-4 years) |

| Rising demand for cost optimisation and predictable OPEX | +2.8% | EU-wide, particularly SME-focused markets | Short term (≤ 2 years) |

| Increasing cybersecurity threats pushing managed security uptake | +3.5% | Europe-wide, concentrated in BFSI and critical infrastructure | Short term (≤ 2 years) |

| Shortage of in-house IT talent across Europe | +2.1% | UK, Germany, Netherlands with spillover to Eastern Europe | Long term (≥ 4 years) |

| EU Digital Operational Resilience Act (DORA) compliance burden | +1.8% | EU financial sector with extension to ICT third-party providers | Medium term (2-4 years) |

| Sovereign-cloud initiatives prompting specialised MSP deals | +1.4% | Germany, France, Netherlands with broader EU adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Hybrid and Multi-Cloud Architectures

Nordic enterprises continue to champion multi-cloud strategies, with regional leaders such as Tietoevry Tech Services being recognized for multi-public-cloud mastery for five consecutive years.[2]Tietoevry Communications, “Cloud Services: Leader in ISG 2024 Multi Cloud Nordic Report,” tietoevry.com Complex workload orchestration, vendor lock-in avoidance, and real-time processing needs spur reliance on managed providers that can unify governance across public, private, and edge nodes. The Europe managed services market increasingly rewards partners able to deliver automated cost controls and AIOps that translate platform spend into measurable business outcomes. Industrial use cases, autonomous driving, smart robotics, and edge analytics, further strengthen demand for distributed management capabilities. Providers possessing sovereign-cloud options gain preference from customers eager to satisfy diverging data-localization mandates.

Rising Demand for Cost Optimization and Predictable OPEX

SMEs across the bloc adopt FinOps disciplines to tame cloud bills and protect cash flow amid economic volatility. TIMETOACT reports that license-optimization projects helped mid-market clients counter rising Microsoft 365 and Azure fees, underscoring the importance of granular spend visibility. The same mindset drives uptake of subscription bundles that merge labor, tooling, and advisory into all-inclusive monthly charges. Market participants increasingly emphasize energy-efficiency credentials as fluctuating electricity prices heighten focus on total cost of ownership]. Strategic users now view managed services as a lever for faster product launches and innovation throughput rather than mere expense reduction, a shift that elevates the provider’s role in value creation.

Increasing Cybersecurity Threats Pushing Managed Security Uptake

Hacktivist groups have targeted European infrastructure with 6,600 attacks since 2022, and 96% of these incidents stem from pro-Russian actors. Continuous monitoring and rapid incident response have thus become non-negotiable for regulated sectors such as BFSI and critical infrastructure. Small businesses face disproportionate risk, representing two-thirds of extortion cases, yet many lack internal defenses. Managed security services fill the gap by offering 24/7 detection, double-extortion mitigation, and threat-intelligence fusion. Providers layering AI-assisted analysis over telemetry streams gain competitive edge through faster triage and reduced false positives.

Shortage of In-House IT Talent Across Europe

Most of UK organizations report difficulty recruiting core IT roles, while cite technology complexity as a compounding factor. Similar shortages appear in Germany and the Netherlands, intensifying reliance on managed partners for cloud, cybersecurity, and AI skill sets. Survey data show three-quarters of IT teams already outsource at least some network tasks, freeing capacity for innovation. The Europe managed services market benefits as providers embed continuous up-skilling programs and knowledge-transfer sessions that help clients stay abreast of rapid technology change. Even data-center operators signal workforce anxiety: 71% list staffing as their top operational concern.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex EU data-sovereignty and privacy regulations | -1.9% | EU-wide with varying national implementations | Medium term (2-4 years) |

| Integration complexity with legacy systems | -1.4% | Established markets: UK, Germany, France, Italy | Long term (≥ 4 years) |

| Escalating carbon-accounting scrutiny on outsourced workloads | -0.8% | Northern Europe leading, broader EU adoption | Medium term (2-4 years) |

| Rising energy costs squeezing data-centre service margins | -1.1% | Europe-wide with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex EU Data-Sovereignty and Privacy Regulations

GDPR Article 28 mandates detailed processor agreements and transfer impact assessments, raising legal overhead for cross-border workloads. National deviations, such as France’s preference for EEA-hosted data, fragment compliance paths and inflate advisory costs for multi-nation deployments. Upcoming rules, including the Data Act (September 2025) and AI Act (August 2026)—layer fresh obligations onto service contracts, while the draft EU Cloud Scheme introduces a “high-plus” level requiring all-European operations. Managed providers must therefore fund repetitive audits and certification cycles, factors that elevate service prices and slightly temper Europe managed services market growth.

Integration Complexity with Legacy Systems

Mainframe estates and proprietary platforms still underpin critical operations in established industries. Transition projects routinely span six months or more, as demonstrated by SSE Services’ 32,000-endpoint migration program. High technical debt forces managed service providers to reconcile disparate security stacks and brittle interfaces, prolonging time-to-value. Premium pricing often offsets these risks, yet customers remain sensitive to incremental costs, causing occasional postponements. Providers that maintain specialized legacy know-how anchor sticky, multi-year relationships but must balance modernization roadmaps with ongoing regulatory compliance needs.

Segment Analysis

By Deployment Model: Cloud Leadership Spurs Hybrid Innovation

Cloud deployments contributed 58.62% to the Europe managed services market in 2024, mirroring widespread preference for consumption-based IT models that flex with business volume. The hybrid-hosted subset is set to grow at a 14.87% CAGR, propelled by data-sovereignty mandates and latency-sensitive workloads that cannot reside exclusively in hyperscale regions. Many banking and healthcare organizations keep Tier 1 records on sovereign instances while offloading analytics to public clouds. Providers offering unified visibility, policy enforcement, and automated cost controls across these mixed estates gain contract wins. The Europe managed services market size for hybrid solutions is forecast to expand notably as enterprises deploy edge nodes for real-time controls in manufacturing plants. Interoperability toolkits, zero-trust fabrics, and policy-as-code emerge as baseline capabilities for bidders in this segment.

Second-generation cloud adopters increasingly demand outcome-based SLAs and FinOps dashboards that show savings tied to automated rightsizing. This necessity pushes partners to invest in AIOps, observability, and infrastructure-as-code workflows. Federated architectures, such as Deutsche Telekom’s plan to connect 10,000 European edge nodes by 2030, exemplify the scale and distribution that managed providers must accommodate.[3]Deutsche Telekom Corporate Blog, “Together for a Sovereign Digital Future in Europe,” telekom.com As regulatory bodies tighten cross-border data-flow rules, architectures supporting dynamic workload placement within specific jurisdictions become critical. These factors collectively keep the Europe managed services market on a robust growth track and underpin hybrid’s role as the leading innovation vector.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Type: Security Overshadows While Cloud Accelerates

Managed security services delivered 29.61% of 2024 revenue, confirming that cyber risk sits at the top of executive agendas. Banking, energy, and public-sector buyers seek always-on monitoring wrapped with incident-response retainers that minimize downtime. Threat surfaces expand with distributed workforces and IoT deployments, further raising demand for vulnerability management and identity governance. The Europe managed services market size for security solutions is set to widen as double-extortion ransomware and hacktivist disinformation campaigns gain complexity. Providers combining managed detection and response with AI-based analytics shorten response times and therefore secure higher contract values.

Managed cloud and application services represent the fastest-expanding category, rising at a 14.62% CAGR through 2030. Customers expect DevOps pipelines, container orchestration, and automated scaling as standard inclusions, not premium add-ons. Bundled offers that merge cloud operations with application modernization appeal to resource-limited IT teams. The convergence of security and cloud drives cross-selling opportunities: a provider that governs multi-cloud estates naturally extends to securing them. Data-center, network, and collaboration services maintain steady, albeit slower, expansion as next-generation demands center on software-defined networking and edge connectivity. Yet even these traditional domains now integrate AI-enabled insights for capacity planning and quality assurance.

By Enterprise Size: SMEs Gain Momentum

Large enterprises delivered 62.76% of total sales in 2024, leveraging multi-year managed deals to streamline sprawling IT estates. Board-level mandates focus on reducing technical debt and accelerating new-product launch cycles, prompting long-term partnerships that guarantee predictable cost positions. Nonetheless, SMEs record the quickest 15.03% CAGR as standardized service bundles lower adoption barriers. The Europe managed services market now offers entry-level packages that wrap cloud hosting, endpoint management, and cybersecurity within one invoice, eliminating integration overhead for smaller firms.

SME buyers, often without dedicated CISOs, gravitate to managed detection and response, backup-as-a-service, and compliance-ready cloud platforms. The Europe managed services market share captured by this segment is set to creep upward as suppliers refine self-service portals and per-user pricing, making enterprise-grade features attainable for tight budgets. Providers that include onboarding toolkits and remote-support pools position themselves well in a landscape where speed to value outweighs bespoke customization. Market messaging that highlights business enablement rather than technology complexity resonates with this audience.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Vertical: BFSI Continues to Dominate

BFSI held 24.53% share in 2024, driven by stringent oversight such as DORA and EBA outsourcing guidelines. Institutions require zero-downtime operations, encrypted data exchanges, and certified service centers, all of which inflate the scope and duration of managed contracts. Regulatory change frequency encourages banks to retain strategic alliances with knowledgeable partners rather than cycle through new suppliers. The Europe managed services market size serving BFSI is poised to persist at a premium as open-banking interfaces and real-time payment rails advance.

Healthcare and life sciences will log a 14.21% CAGR to 2030. Telemedicine platforms, digital diagnostics, and genomics analytics create data-intensive workloads subject to GDPR and patient-participation rules. Providers that meet HDS or equivalent standards gain competitive standing. Manufacturing, meanwhile, invests in managed OT security for Industry 4.0 rollouts. Governments concentrate on sovereign-cloud capacity to safeguard citizen information, exemplified by national cloud programs in France and Germany. Retail companies integrate supply-chain visibility and omnichannel analytics, demanding low-latency edge nodes for real-time stock management.

Geography Analysis

The United Kingdom, as the largest single contributor to Europe managed services market revenue, benefits from advanced cloud penetration and a deep bench of providers with ServiceNow, AWS, and Microsoft specializations. System integrators secure multiyear framework agreements that cement recurring income streams, though some contracts now emphasize measurable carbon footprint reductions to align with national sustainability targets. Regional data-center capacity additions continue, yet power-availability constraints in London zones prompt interest in suburban campuses linked via high-capacity dark fiber.

Germany and France constitute the continental core, each combining sovereign-cloud ambitions with industrial resiliency objectives. German manufacturers channel resources into managed OT security and 5G-enabled production lines, spurring multi-disciplinary engagements that cover both factory floor and enterprise IT layers. France, meanwhile, leverages state-backed cloud-sovereignty programs to ensure sensitive public-sector workloads remain within national borders, raising the bar for providers on certification and domestic-ownership thresholds.

Central and Eastern Europe, headed by Poland, registers the fastest proportional growth as multinational corporations co-locate support hubs and invest in local hyperscale regions. Skilled labor availability, competitive wages, and improving connectivity position Warsaw and Kraków as attractive nearshore centers. Nordic markets focus on green-compute credentials and waste-heat recapture schemes, channeling managed budget toward partners able to validate lifecycle energy savings. Southern European countries close the digital-skills gap through EU recovery-fund projects, widening opportunities for mid-tier MSPs that bundle training and migration services.

Competitive Landscape

European managed services remain fragmented; more than 70% of active assets sit in private-equity portfolios, fueling multi-country roll-up strategies that pursue scale economies. Global consultancies and local specialists coexist, each carving niches through either breadth of service or domain depth. Transaction velocity stays high, exemplified by Agilitas Private Equity’s EUR 300 million purchase of Tietoevry Tech Services aimed at creating a Nordic heavyweight with 7,000 staff and regional data-center presence.

Strategic differentiators now extend beyond headcount and revenue. Providers win bids by showcasing sovereign-cloud alignment, AI-based automation, and sector-specific compliance toolkits. Partnerships with hyperscalers yield co-innovation sandboxes where clients trial advanced analytics and edge solutions without incurring heavy capex. Meanwhile, buyers scrutinize vendor energy strategies, prompting operators to integrate renewable PPAs and granular power-usage telemetry into service catalogs. Market consolidation has moderately improved bargaining power for larger players but still leaves ample greenfield for niche entrants orbiting emerging technologies such as quantum-secure networking.

Competitive dynamics further evolve as telecom operators re-enter the field through security and edge offerings. Proximus NXT’s EUR 100 million federal cybersecurity win illustrates the appetite of public entities for single-provider models that layer network and security operations under one roof. Similarly, Devoteam’s renewal of Google Cloud MSP status, along with its ServiceNow practice expansion, underscores the importance of certified expertise and ecosystem alliances. As managed workloads grow in complexity, selection criteria favor proof of resiliency, regulatory fluency, and demonstrated investment in continuous talent development.

Europe Managed Services Industry Leaders

-

AT&T Inc.

-

Fujitsu Limited

-

Cisco Systems, Inc.

-

International Business Machines Corporation

-

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Agilitas Private Equity agreed to acquire Tietoevry Tech Services for EUR 300 million, forming a Nordic-centric provider with over 7,000 employees and multiple regional data centers.

- February 2025: Proximus NXT won Belgium’s largest managed cybersecurity contract worth above EUR 100 million over seven years, supporting around 70,000 end-users across federal agencies.

- January 2025: 3i invested EUR 116 million in Constellation, signaling sustained private-equity interest in European managed services platforms.

- December 2024: SPIE acquired AnyLinQ B.V. in the Netherlands, adding EUR 21 million revenue and broadening its data-management, cloud, and cybersecurity portfolio.

Europe Managed Services Market Report Scope

The emergence of managed services is aiding in meeting the needs of a wide variety of businesses throughout Europe. In the region, the telecommunication providers are focusing on security services, owing to European regulations. Furthermore, the region has a strong automotive and manufacturing sector, and in addition, emerging applications, like cloud-based solutions, are expected to do significantly well during the forecast period.

The Europe managed services market is segmented by deployment (on-premise and cloud), by type (managed data center, managed security, managed communications, managed networks, managed infrastructure, and managed mobility), by enterprise size (small and medium enterprises and large enterprises), by end-user vertical (BFSI, manufacturing, healthcare, retail), and country (United Kingdom, Germany, France, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Deployment Model

| On-premises |

| Cloud |

| Hybrid/Hosted |

By Service Type

| Managed Data Centre |

| Managed Security |

| Managed Network |

| Managed Communication and Collaboration |

| Managed Infrastructure and Hosting |

| Managed Mobility |

| Managed Cloud and Application |

| Managed Workplace / Service Desk |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Vertical

| BFSI |

| Manufacturing |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Government and Public Sector |

| IT and Telecom |

| Energy and Utilities |

| Other End-user verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Russia |

| Poland |

| Rest of Europe |

| By Deployment Model | On-premises |

| Cloud | |

| Hybrid/Hosted | |

| By Service Type | Managed Data Centre |

| Managed Security | |

| Managed Network | |

| Managed Communication and Collaboration | |

| Managed Infrastructure and Hosting | |

| Managed Mobility | |

| Managed Cloud and Application | |

| Managed Workplace / Service Desk | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Healthcare and Life Sciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| IT and Telecom | |

| Energy and Utilities | |

| Other End-user verticals | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Russia | |

| Poland | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Europe managed services market by 2030?

The market is forecast to reach USD 113.98 billion by 2030 on a 13.94% CAGR.

Which service category currently dominates managed services revenue in Europe?

Managed security holds the largest share at 29.61% of 2024 revenue.

Why are hybrid and multi-cloud deployments important to European enterprises?

They blend public-cloud agility with data-sovereignty assurance, driving 14.87% CAGR for hybrid/hosted services.

Which European country is expanding fastest in managed services adoption?

Poland shows the quickest growth trajectory at a 14.43% CAGR through 2030.

How are energy-price swings influencing managed service provider strategies?

Providers secure renewable-energy contracts and invest in efficiency to protect margins and meet client ESG goals.

Page last updated on: