Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

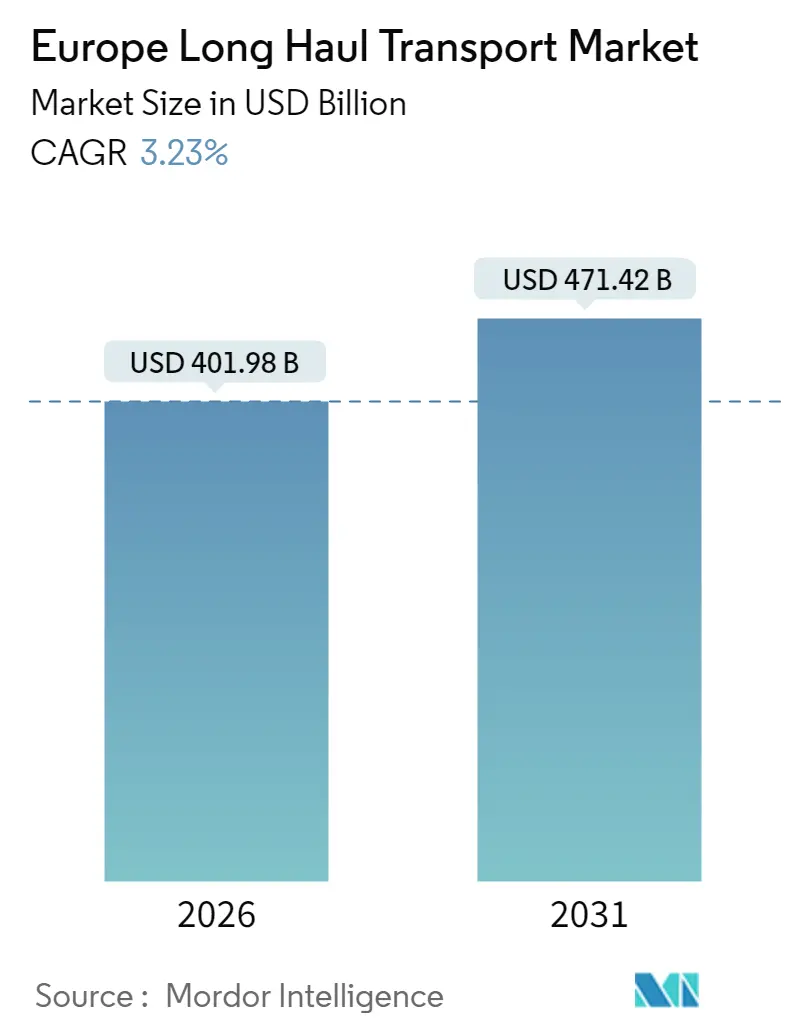

| Market Size (2026) | USD 401.98 Billion |

| Market Size (2031) | USD 471.42 Billion |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Long Haul Transport Market Analysis by Mordor Intelligence

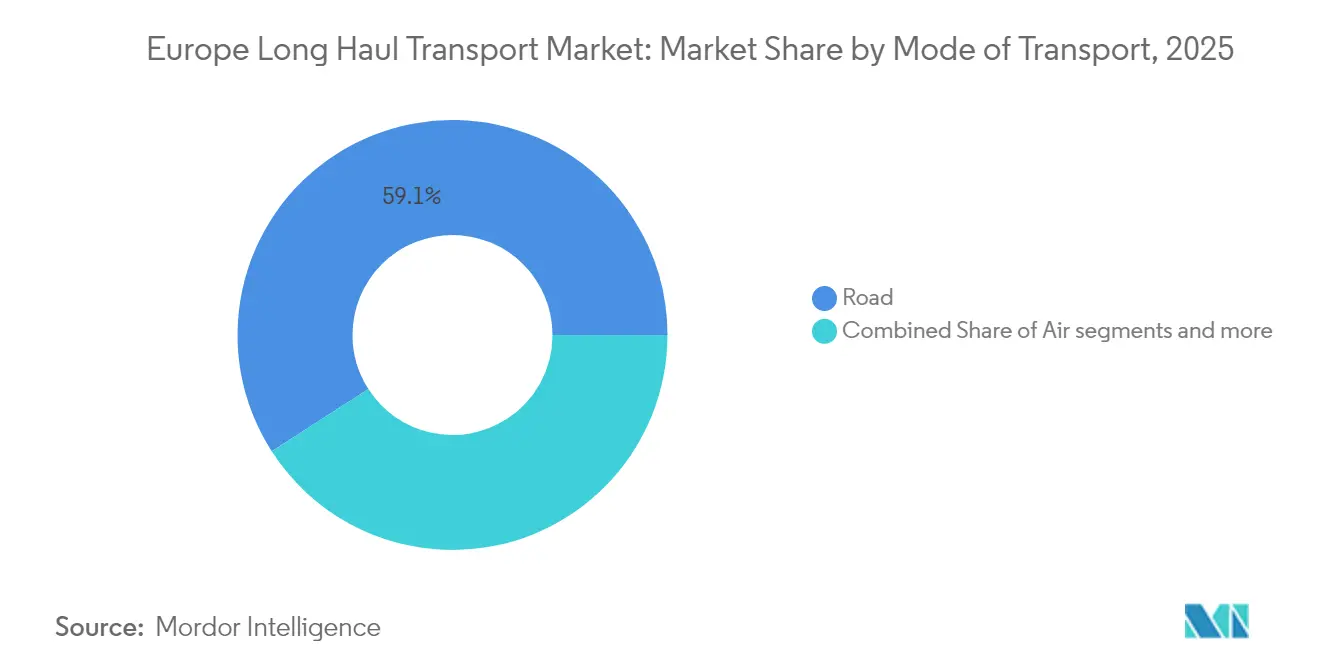

The Europe Long Haul Transport Market was valued at USD 389.44 billion in 2025 and estimated to grow from USD 401.98 billion in 2026 to reach USD 471.42 billion by 2031, at a CAGR of 3.23% during the forecast period (2026-2031). This growth trajectory rests on manufacturing’s entrenched freight needs, the rapid rise of e-commerce, and an active M&A pipeline that concentrates volume with a shrinking set of multimodal providers. At the same time, decarbonization deadlines and infrastructure gaps impose capital and operational stresses that pull margins in opposite directions. Road transport preserved a 59.60% Europe Long Haul Transport market share in 2024 as just-in-time production and high-frequency retail replenishment still require door-to-door flexibility. Air freight is emerging as the fastest mode with a 4.80% CAGR forecast through 2030, a direct offshoot of cross-border parcel flows and high-value pharmaceutical consignments that must move within tight thermal tolerances.

Key Report Takeaways

- By mode of transport, road commanded 59.10% of the Europe Long Haul Transport market share in 2025 and continues to expand, though air freight is forecast to post the highest 4.75% CAGR to 2031.

- By end-user industry, manufacturing accounted for 32.55% of the Europe Long Haul Transport market size in 2025 while wholesale and retail trade is advancing at a 3.72% CAGR through 2031.

- By geography, Germany captured 23.40% revenue in 2025; Poland records the strongest 3.83% CAGR to 2031 as near-shoring accelerates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Long Haul Transport Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal & Fit-for-55 modal-shift targets | 0.9% | EU-wide, strongest in Germany, Netherlands, France | Medium term (2-4 years) |

| Expansion of TEN-T megaprojects (Rail Baltica, Fehmarn Belt, etc.) | 0.6% | Baltic States, Germany, Denmark, Poland | Long term (≥4 years) |

| Explosive e-commerce boosting parcel & air-cargo lane demand | 1.1% | Global, concentrated in UK, Germany, France, Netherlands | Short term (≤2 years) |

| Consolidation & 4PL integration across modes | 0.5% | EU-wide, led by Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Roll-out of zero-carbon fuel & shore-power infrastructure | 0.4% | Major ports: Rotterdam, Hamburg, Antwerp, Barcelona | Long term (≥4 years) |

| Post-pandemic resilience & near-shoring strategies | 0.7% | Poland, Czech Republic, Hungary, with spillover to Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Green Deal & Fit-for-55 Modal-Shift Targets

The Fit-for-55 package fixes legally binding CO₂ cuts that push shippers to reroute long-haul volume from road toward rail or inland waterways, yet terminal backlogs and last-mile constraints still tilt day-to-day demand toward trucks. Rail’s 80% lower emissions per tonne-kilometer give it a clear environmental edge, but capacity on core corridors hovers above 85%, leaving little surge headroom. The carbon-border adjustment mechanism extends the pressure by inserting logistics emissions into import compliance audits, so procurement teams now assess freight carbon data with the same rigor once reserved for cost. Certification schemes such as ISO 14083 have become de facto tender prerequisites, compelling smaller carriers to buy telematics and data-reporting tools they had long deferred. Consequently, fleet renewal and digital visibility projects are pacing quicker than anticipated, even if modal shifts lag policy intent.

Expansion of TEN-T Megaprojects

Rail Baltica’s 870 km of standard-gauge track, supported by EUR 1.4 billion in EU co-financing, promises a seamless Tallinn-Warsaw route, yet permitting delays push commissioning beyond 2030. The Fehmarn Belt rail tunnel slashes Copenhagen–Hamburg transit to under three hours when operational in 2029, unlocking freight flows that today navigate ferry bottlenecks[1]Femern A/S, “Fehmarn Belt Fixed Link Project,” femern.com . Parallel German network upgrades receive EUR 2.5 billion of annual funding, but localized land-acquisition disputes slow diggers on the ground. Each delay holds back the rail share of Europe Long Haul Transport market growth, leaving road hauliers to soak up volume despite carbon targets. Secondary investments in intermodal yards and electrification hinge on main-line completion, amplifying the knock-on effect of every missed milestone. Long-term, these links still reshape continental freight geometry by embedding a high-speed, low-carbon spine into the network.

Explosive E-commerce

Air cargo tonnage at Frankfurt, Leipzig, and Paris climbed 8%, fueled by small parcels and temperature-controlled pharma consignments requiring sub-48-hour delivery windows. Cross-border parcels jumped 15% as marketplace platforms integrate EU inventories, yet customs digitalization still lags at non-Schengen borders, extending lead times on southeast routes. To stay competitive, integrators are retrofitting freighters with IoT-driven temperature controls and AI routing that predicts congestion down to neighborhood level.

Consolidation & 4PL Integration

DSV’s USD 14.3 billion purchase of DB Schenker creates a forwarding titan topping USD 39 billion in revenue, yielding purchasing clout with ocean carriers and airlines that mid-tier forwarders cannot match. Scale also allows end-to-end contract bundling across air, sea, rail, and road, simplifying procurement for large shippers and nudging share toward integrated providers. Digital freight platforms such as sennder, armed with EUR 160 million in fresh capital, use algorithms to force down empty running and broker margins, compelling legacy 3PLs to either invest in proprietary tech or cede spot loads. Automotive and retail verticals lead the shift to 4PL models where a single coordinator orchestrates multiple carriers in real time. This trend indirectly elevates data-governance and cybersecurity requirements in contracts, creating a new barrier to entry for smaller players..

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail-line, port & intermodal terminal capacity bottlenecks | -0.70% | Germany, Netherlands, Belgium, Italy | Short term (≤2 years) |

| Heavier-truck Directive risk of reverse modal shift | -0.30% | Germany, France, Poland, Spain | Medium term (2-4 years) |

| Driver & skills shortages across road, rail & maritime | -0.60% | EU-wide, acute in Germany, UK, France | Medium term (2-4 years) |

| Energy & bunker-fuel price volatility | -0.40% | Global, impacting sea and air freight | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rail-Line, Port & Intermodal Capacity Bottlenecks

Rail freight utilization on Rhine-Alpine and North Sea–Mediterranean corridors exceeded 85% in 2024, leaving minimal headroom for extra trains and increasing schedule unreliability. Rotterdam, Antwerp, and Hamburg terminals ran near saturation during peak weeks, extending container dwell times beyond 48 hours and eroding rail’s theoretical door-to-door speed advantage. Terminal automation projects are underway, yet land acquisition and permitting often span three to five years, so meaningful relief is not expected before 2027. Diesel motive power still covers 46% of European track, limiting the emissions benefit of modal shift and exposing operators to fuel-price volatility. These bottlenecks collectively cap the rail share of the Europe Long Haul Transport market until new capacity comes online.

Driver & Skills Shortages

Road freight lacked 400,000 drivers in 2024, equal to about 7% of its workforce, due to aging demographics and limited appeal of long-haul jobs among younger workers. Cabotage restrictions compound the issue by limiting how many domestic hauls a foreign truck may perform, fragmenting capacity during seasonal peaks. Rail operators also face two-year training cycles for locomotive engineers, a lag that slows service additions despite available wagons. Short-sea shipping reports officer shortfalls that forced 10% to 15% wage hikes in 2024, costs ultimately passed through freight rates. Persistent talent gaps therefore tighten spot capacity and inflate logistics budgets for shippers across the board.

Segment Analysis

By Mode of Transport: Road Dominance Meets Air’s Ascent

Road transport maintained a 59.10% Europe Long Haul Transport market share in 2025 as the continent’s dense highway network underpins time-critical deliveries, yet escalating diesel costs and driver scarcity compress operator margins. Air freight carries the fastest growth outlook at a 4.75% CAGR through 2031, fueled by e-commerce parcel volume and GDP-compliant cold-chain pharmaceuticals that command premium rates. Rail’s lower emissions per tonne-kilometer align with Fit-for-55 policy, but capacity bottlenecks and first-mile/last-mile transfers temper its immediate share gains. Inland waterways, moving 300 million t of Rhine traffic annually, face climate-linked low-water disruptions that shift cargo onto rail and road, highlighting the climate resilience imperative.

Digital freight platforms reduced empty running on primary road corridors from 25% to under 18%, boosting small-fleet competitiveness and lowering emissions intensity. Rail intermodal operators deploy IoT sensors that track location and shock to mimic road-level transparency, narrowing a historic information gap. Meanwhile, EU funds of EUR 500 million target lock modernization on Rhine and Danube stretches, a step meant to safeguard waterway competitiveness against drought risk. The Europe Long Haul Transport market size attached to air freight is forecast to climb steadily as parcel density rises, underscoring modal diversification in corporate shipping strategies.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Manufacturing Leads, Retail Accelerates

Manufacturing retained 32.55% of the Europe Long Haul Transport market size in 2025, propelled by automotive and machinery supply chains that run lean inventories and rely on synchronized inbound flows. Wholesale and retail trade will grow at a 3.72% CAGR through 2031 as omnichannel models multiply fulfillment nodes and spike demand for cross-dock and parcel services. Agriculture, fishing, and forestry sustain steady refrigerated-freight demand, with reefer truck fleets expanding 8% in 2024 to move Mediterranean produce northward. Oil, gas, and extractive segments confront decarbonization headwinds but still require heavy-haul capacity and specialized tank equipment for fossil fuels and bulk mineral movements.

Construction freight pivots with public-works cycles; EU recovery funds spurred a 2024 surge that pulled cement and steel volumes back to pre-pandemic highs. The “Others” bucket, spanning pharma, chemicals, and electronics, carries stringent chain-of-custody protocols; GDP-certified carriers command premium pricing thanks to validated cold-chain processes. Retail’s fragmentation into micro-fulfillment adds shipment frequency yet shrinks average consignment size, lifting express-mode share and monetizing last-mile logistics—key contributors to Europe Long Haul Transport industry profitability. Near-shoring tilts manufacturing freight eastward but also intensifies shipment cadence, benefiting less-than-truckload specialists positioned on central European corridors.

Geography Analysis

Germany commanded 23.40% of the Europe Long Haul Transport market in 2025, leveraging its automotive export corridors and multimodal hubs in Duisburg and Hamburg, although rail congestion on the Rhine-Alpine axis and a 7% driver shortfall curb growth potential. Poland is the pace-setter with a 3.83% CAGR forecast to 2031, powered by EUR 8 billion in near-shoring FDI and a pipeline of 4 million m² in new logistics real estate that clusters along east-west highways. The United Kingdom’s post-Brexit freight now stabilizes; yet new border-entry systems expected in late 2025 will layer compliance time and cost onto cross-Channel routes, prompting some shippers to reroute via Benelux ports.

France exploits Atlantic and Mediterranean dual-sea access, with the Seine-Nord Europe canal linking Paris to northern waterways by 2030, a move set to recalibrate barge competitiveness on north–south trades. Spain positions the Port of Barcelona as a southern gateway; EUR 400 million in automation cuts vessel dwell times and anchors catalytic rail-barge links inland. Italy confronts Alpine road congestion; the Brenner Base Tunnel, targeted for 2032, will push a meaningful slice of north–south flows to rail, trimming transit times between Verona and Munich.

The Netherlands, through Rotterdam’s 440 million t throughput, remains a continental pivot, integrating deep-sea, barge, and rail in a high-density hinterland network. Nordic states invest in electric-truck corridors, while Balkan members upgrade roads with cohesion funds, collectively lifting capacity in the “Rest of Europe” segment. Germany’s EUR 2.5 billion rail-digitalization plan aims to raise freight capacity 20% by 2030, but permitting drag risks schedule slippage beyond 2028. Poland’s warehouse rents climb as e-commerce and auto suppliers chase scarce labor, nudging logistics budgets and fueling automation spending. Finally, UK freeport zones, announced in 2024, attract measured interest as operators balance customs incentives against dual-regime complexity.

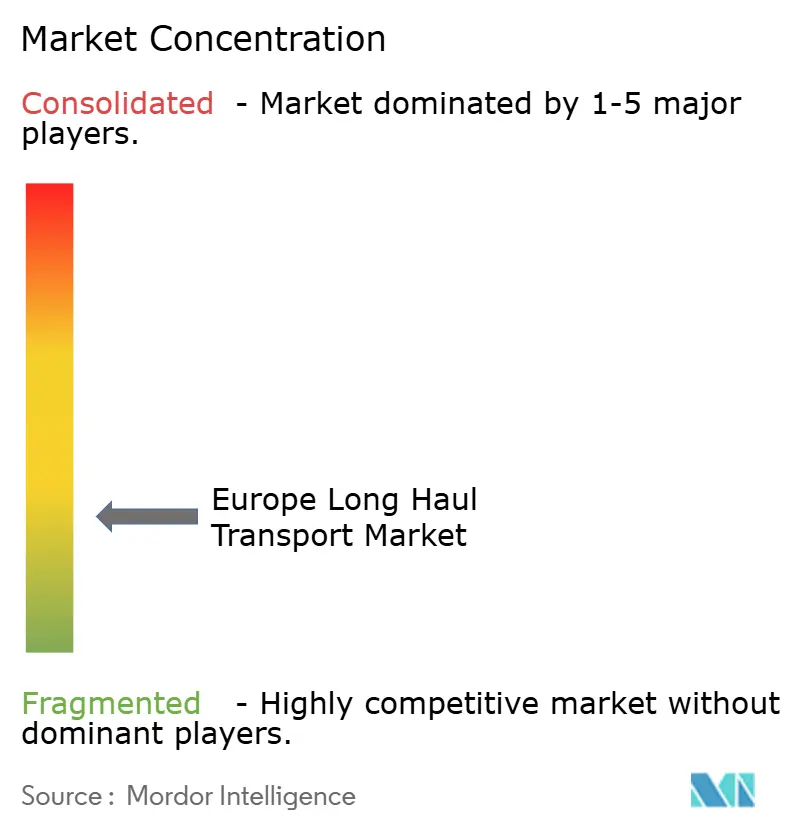

Competitive Landscape

The Europe Long Haul Transport market remains fragmented. DSV’s pending merger with DB Schenker will vault the combined entity into a revenue league with DHL and Kuehne+Nagel, creating 150,000-plus headcount and unmatched bargaining heft across modal contracts. Scale advantages now extend beyond volume discounts to technology spend; multi-billion-dollar players amortize visibility platforms and data-science teams across thousands of lanes, a hurdle that asset-light forwarders fend off through partnerships or divestitures.

Specialists defend turf with expertise in hazardous goods, pharma cold-chain, or urban micro-fulfillment, where regulatory compliance and asset specificity deter generalists. Digital challengers such as sennder and Transporeon compress broker margins by 20% in some lanes via algorithmic matching, pushing incumbents to invest or acquire to stay relevant. Sustainability differentiation grows in importance; operators sign renewable-energy PPAs, deploy battery-electric trucks, and pilot hydrogen rigs to appeal to shipper decarbonization scorecards embedded in 2025 RFQs..

Rail Cargo Group filed patents for automated coupling that cuts yard dwell, illustrating technology’s role in unlocking capacity without new track. Autonomous-truck pilots run platoons on German autobahns, yet commercial rollout awaits harmonized liability rules, still fragmented across member states. Private-equity roll-ups thrive in fragmented sub-segments, stitching together regional hauliers to gain density and negotiate fuel or toll rebates—a model active in Benelux and the UK.

Europe Long Haul Transport Industry Leaders

Girteka Logistics

DHL Group

DSV A/S

Dachser

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2024: Kuehne+Nagel won a 5-year inbound logistics mandate across 12 European auto plants.

- July 2024: CMA CGM pledged EUR 300 million to expand Marseille container handling by 500,000 TEU.

- June 2024: Girteka grew its fleet by 1,200 trucks and opened a Poland maintenance hub.

- April 2024: DFDS started an Immingham–Gothenburg freight ferry adding 6,000 lane-meters weekly.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European long-haul road freight transport market as revenue generated when heavy-duty tractors haul full-truck-load or less-than-truck-load cargo over distances typically beyond 300 km across or within EU, EFTA, and U.K. borders, using articulated trucks operating on public highways. Our lens keeps the unit of analysis at the service level, not vehicle sales or in-house captive fleets.

Scope exclusion: Passenger coach services and unitized rail, sea, or air legs that do not involve a road haul exceeding 300 km are left outside the baseline.

Segmentation Overview

- By Mode of Transport

- Road

- Rail

- Sea and Inlandwaterways

- Air

- By End-user Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- By Country

- Germany

- United Kingdom

- Spain

- Italy

- Netherlands

- France

- Poland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed European road carriers, 3PL route planners, large exporters, and driver unions across Germany, Poland, Spain, and the Benelux to validate rate evolution, dead-head ratios, and upcoming regulatory costs. Short web surveys with shippers in retail and automotive supplied corridor-level load-factor assumptions that desk data could not reveal.

Desk Research

We began by scraping public datasets such as Eurostat's distance-band tonne-kilometer tables, the IRU driver-shortage barometer, and monthly Upply-Ti freight-rate indices, which together give volume, capacity, and pricing fingerprints. Trade association white papers from CLECAT and UIC, customs flow records on UN Comtrade, and national statistics portals (Destatis, INE, ISTAT) rounded out the traffic and commodity mix. Paid stores available to Mordor analysts, including D&B Hoovers for carrier revenues and Dow Jones Factiva for deal flow, helped us benchmark operator yields. The sources noted are illustrative; many additional public and commercial references fed our evidence file.

Market-Sizing & Forecasting

We anchored the top-down model on Eurostat long-haul tonne-kilometers, multiplied by corridor-specific average revenue per tkm derived from contract and spot benchmarks, then reconciled totals against sampled carrier financials and tender databases to catch outliers. Key variables like industrial production, e-commerce parcel volume, diesel and HVO prices, driver wage inflation, and new toll surcharges feed a multivariate regression that drives the 2025-2030 forecast. Bottom-up tests (selected fleet counts × average kilometers × yield) acted as sense checks, with gaps in smaller countries bridged by calibrated penetration ratios.

Data Validation & Update Cycle

Models pass two-stage peer review; variance beyond ±5 % versus historical series triggers reruns, and any mid-year shocks (fuel tax, ETS-2 rollout) cue a rapid refresh. Reports are rebuilt annually; before release, an analyst re-pulls the latest macro and rate prints so clients receive a current view.

Why Mordor's Europe Long Haul Transport Baseline Commands Reliability

Published figures often differ because firms stretch scope, freeze exchange rates, or roll forward older surveys. Our disciplined corridor filter, live FX feeds, and yearly refresh keep the base year crisp, while selective bottom-up audits stop over-aggregation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 389.44 B (2025) | Mordor Intelligence | - |

| USD 474.2 B (2024) | Global Consultancy A | Combines short-haul and first/last-mile legs; keeps 2023 EUR/USD fixed; update cadence biennial |

| USD 235.4 B (2023) | Industry Analytics B | Uses narrower sample of carrier filings only; excludes cross-trade lanes; baseline year older |

Taken together, the comparison shows that when scope is tightened to true over-the-road hauls and variables are refreshed annually, Mordor's balanced midpoint offers decision-makers a dependable, easy-to-replicate starting point.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2026 value of Europe Long Haul Transport?

The Europe Long Haul Transport market stands at USD 401.98 billion in 2026.

Which mode is forecast to grow fastest through 2031?

Air freight is projected to expand at a 4.75% CAGR, driven by cross-border e-commerce and pharma cold-chain demand.

How large is the German share of continental long-haul freight?

Germany held 23.40% of the market in 2025, anchored by automotive and machinery export corridors.

What CAGR is expected for Poland’s long-haul sector?

Poland is forecast to post a 3.83% CAGR between 2026 and 2031 as near-shoring attracts new manufacturing.

Which end-user segment is gaining share fastest?

Wholesale and retail trade leads segment growth at a 3.72% CAGR as omnichannel fulfillment multiplies shipment frequency.

How does consolidation impact freight pricing power?

Scale from deals like DSV-DB Schenker gives large 4PLs negotiating leverage with carriers, compressing broker margins and pushing smaller firms toward technology partnerships.