| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.48 Billion |

| Market Size (2030) | USD 4.55 Billion |

| CAGR (2025 - 2030) | 5.50 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Liquid Fertilizer Market Analysis

The Europe Liquid Fertilizers Market size is estimated at USD 3.48 billion in 2025, and is expected to reach USD 4.55 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The European liquid fertilizers industry is experiencing significant transformation driven by pressing food security challenges and evolving agricultural landscapes. According to UNICEF's 2022 survey, severe food insecurity in Northern America and Europe increased from 0.9% to 1.5% between 2019 and 2021, highlighting the urgent need for enhanced agricultural nutrients productivity. This situation is further complicated by the European Commission's projections indicating that EU agricultural land, which currently covers 42% of all EU land area, is expected to shrink by 1.1% between 2015 and 2030, with specific declines in arable land and livestock grazing areas by 4.0% and 2.6%, respectively.

The industry is witnessing substantial consolidation and technological advancement as companies seek to strengthen their market positions and enhance product offerings. A notable development in January 2023 was Tessenderlo Group's strategic acquisition of Ammonium Thiosulfate fertilizer marketing and sales activities from Esseco Srl, demonstrating the industry's movement toward consolidation and expanded product portfolios. This trend is particularly evident in Northern Europe, where companies like NordFert are establishing new production facilities to strengthen their regional presence and supply capabilities, focusing on crop nutrition solutions.

Environmental sustainability has become a cornerstone of industry development, with manufacturers increasingly focusing on developing products that align with the EU's agricultural policy objectives. The industry has witnessed a notable shift toward liquid organic fertilizers and liquid biofertilizers, particularly in countries like Italy, where the use of natural and organic potassium liquid fertilizers is rising while synthetic variants are declining. This transformation is supported by new EU regulations that facilitate the marketing of more organic and waste-based fertilizers across the European Union.

The market is experiencing significant developments in production and distribution infrastructure, with companies investing in advanced manufacturing facilities and logistics networks. Major industry players are establishing dedicated manufacturing units equipped with sophisticated technology for liquid fertilizers production, complemented by extensive distribution networks spanning multiple European countries. These investments are particularly focused on regions with high agricultural activity and areas requiring specialized nutrient management solutions, enabling more efficient and targeted delivery of liquid fertilizers products to end-users.

Europe Liquid Fertilizer Market Trends

Easy Usage and Application Procedures Suitable for European Land

The declining arable land in Europe has necessitated the adoption of highly efficient and easy-to-use fertilization methods. According to a report published by the European Commission in November 2018, the EU agricultural land is expected to shrink by 1.1% during 2015-2030, with arable land area declining by 4.0% and land for livestock grazing reducing by 2.6%. This trend has driven the demand for liquid fertilizers as they are technically fast-acting and uniform, making them particularly suitable for smaller land patches. The ease of application through irrigation systems without requiring heavy machinery makes liquid fertilizers an optimal choice for European farmers dealing with diminishing agricultural spaces.

Several European countries are experiencing not just declining arable land areas but also deteriorating soil quality due to extensive farming, overgrazing, and excessive chemical use. Studies conducted across Western Europe have highlighted extensive degradation in physical, chemical, and biological soil health aspects. Liquid fertilizers present a solution to these challenges as they disperse easily in distorted soil structures and are readily absorbed. Unlike granular fertilizers, liquid formulations also protect workers from dust inhalation during application. The versatility of liquid fertilizers is further demonstrated in their ability to be applied using conventional sprayers and their decreased nutrient loss properties, making them particularly effective under varied agro-climatic conditions prevalent across Europe.

Understand The Key Trends Shaping This Market

Download PDF

Rising Importance of Precision Farming in Europe

The adoption of precision farming in European agriculture has witnessed significant growth, driven by the demand for improved productivity, efficiency, and sustainable agricultural practices. According to scientists from the Clean Energy Research Laboratory in 2021, approximately 50% of agricultural production in various European countries utilizes inorganic nitrogen fertilizers, highlighting the scope for precision application methods. Liquid fertilizers are particularly well-suited for precision agriculture practices as they enable targeted and efficient nutrient delivery, making them an integral component of modern farming techniques that emphasize precise input application for optimal yields.

The European Union has demonstrated strong support for precision agriculture through various initiatives, including the implementation of the Common Agricultural Policy. Under this policy, substantial funds have been allocated to research and development for precision agriculture techniques, including the development of innovative liquid plant nutrients solutions. This commitment is further evidenced by successful field trials, such as the 2022 UK farming trial where a controlled-release liquid fertilizer application not only reduced costly ammonium nitrate rates but also significantly decreased blackgrass pressure. Additionally, in 2020, a Lincolnshire arable farmer achieved a remarkable increase in winter wheat yields by 3.6 metric tons per hectare through precise timing of liquid fertilizer application, demonstrating the tangible benefits of combining precision farming techniques with liquid fertilizer usage.

Increase in the Demand for High-Efficiency Fertilizers in Europe

The demand for high-efficiency fertilizers in Europe has grown substantially, driven by the need for sustainable and cost-effective agricultural practices. Liquid fertilizers have emerged as a superior choice due to their ability to provide accurate, cost-effective yields under varied agro-climatic conditions. These technically advanced products can supply nutrients to crops even under adverse ecological conditions, making them particularly valuable in regions with limited land and challenging weather patterns, such as the Netherlands, where innovative agricultural practices are essential for maximizing yields in controlled environments like greenhouses and hydroponic systems.

The future demand for liquid fertilizers is increasingly influenced by environmental considerations and the need to reduce nutrient losses. This trend is particularly evident in the growing organic farming sector, with the Research Institute of Organic Agriculture reporting an increase in organic farming area from 17.09 million hectares in 2020 to 17.84 million hectares in 2021. The high absorption rates of liquid fertilizers result in reduced chemical leaching and less soil accumulation compared to solid fertilizers, making them an environmentally responsible choice. The quick seepage of liquid fertilizers into the soil enables immediate nutrient absorption by crops, which is particularly beneficial for early-season applications when rapid root growth is crucial for plant establishment. This efficiency in nutrient delivery and environmental sustainability continues to drive the adoption of liquid fertilizers across European agricultural operations.

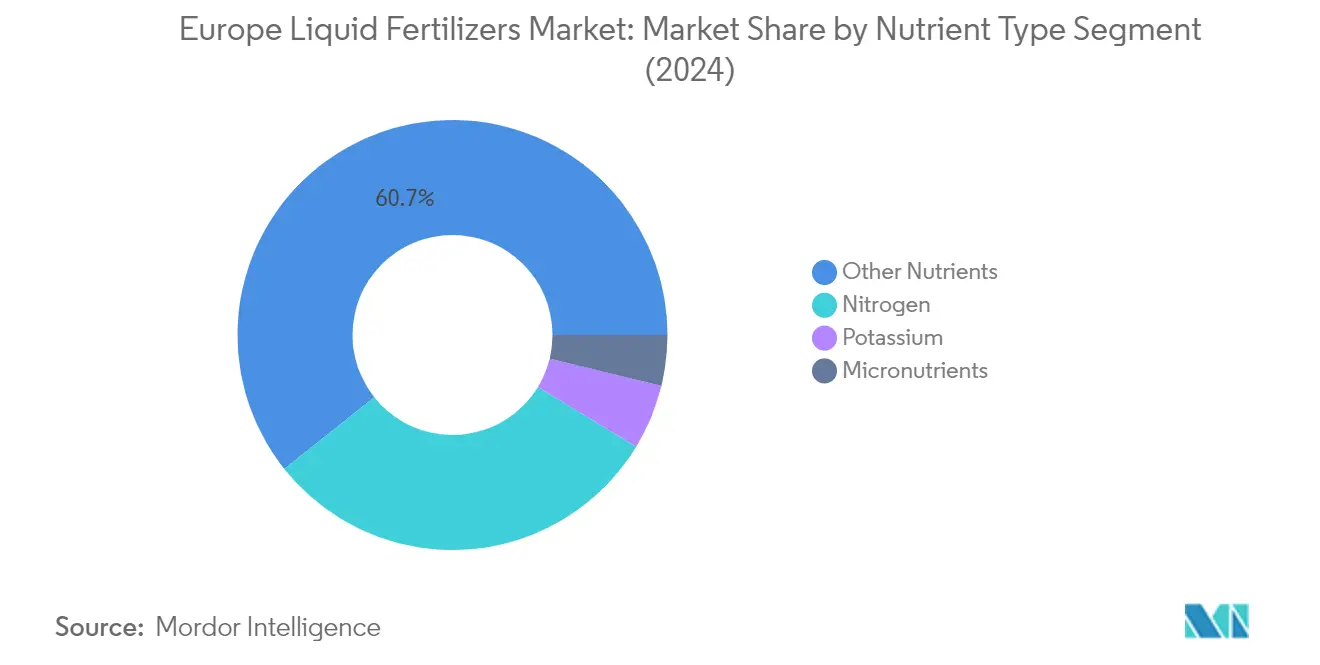

Segment Analysis: Nutrient Type

Nitrogen Segment in Europe Liquid Fertilizers Market

The nitrogen segment holds a dominant position in the Europe liquid fertilizers market, accounting for approximately 31% market share in 2024. The segment's prominence is primarily driven by the extensive usage of liquid nitrogen fertilizers like urea ammonium nitrate (UAN) solutions across major agricultural regions in Europe. According to industry experts, liquid solutions represent nearly 13% of nitrogen consumption in Europe, with UAN being the most prominent liquid nitrogen fertilizer containing 28-32% nitrogen content. The segment's growth is further supported by the active involvement of market players in expanding their production capabilities to meet both domestic and global demand. For instance, several manufacturers have been focusing on developing innovative nitrogen-based liquid fertilizers formulations that offer improved nutrient absorption and environmental sustainability.

Micronutrients Segment in Europe Liquid Fertilizers Market

The micronutrients segment is experiencing the fastest growth in the Europe liquid fertilizers market, with a projected growth rate of approximately 7% during 2024-2029. This remarkable growth is attributed to the increasing recognition of micronutrient deficiencies in European soils and their critical role in crop development. The segment's expansion is particularly driven by the rising adoption of zinc ammonium sulfate and other micronutrient-based liquid fertilizers among urban farmers and home gardeners, owing to their ease of handling and storing. The segment has witnessed significant product diversification with several players offering varied liquid micronutrient solutions specifically designed for different crop types and growing conditions. The trend is particularly strong in the greenhouse and protected cultivation sectors, where precise micronutrient management is crucial for optimal crop yields.

Remaining Segments in Nutrient Type

The potassium and other nutrients segments continue to play vital roles in the European liquid fertilizers market landscape. The potassium segment is particularly significant in regions with intensive agriculture, where it helps improve crop stress tolerance and water management. The other nutrients segment, which includes phosphatic fertilizers and secondary macronutrients like calcium, sulfur, and magnesium, serves diverse agricultural needs across different European regions. These segments are seeing increased adoption in precision farming practices and fertigation systems, particularly in countries with advanced agricultural practices. The demand for these segments is also being driven by the growing trend of sustainable agriculture and the need for balanced crop nutrition programs.

Segment Analysis: Ingredient Type

Synthetic Segment in Europe Liquid Fertilizers Market

The synthetic segment dominates the European liquid fertilizers market, holding approximately 81% of the market share in 2024. The synthetic liquid fertilizer industry is primarily driven by the abundance of raw materials and sophisticated technology and machinery for their manufacturing in the region. To maintain market competition, players have adopted various strategies, including partnerships within the sector. The segment's strong position is supported by the region's well-developed manufacturing infrastructure, with several countries possessing advanced production capabilities. For instance, Russia has emerged as one of the largest producers of liquid nitrogen fertilizer due to easy availability of raw materials and robust production infrastructure. The segment's growth is further bolstered by the increasing adoption of precision farming techniques and the need for high-efficiency fertilizers in European agriculture.

Organic Segment in Europe Liquid Fertilizers Market

The organic segment is projected to experience the fastest growth in the European liquid fertilizers market during 2024-2029, with an expected growth rate of approximately 5%. This accelerated growth is primarily driven by the increasing environmental awareness and the European Union's agricultural policies that promote the use of organic liquid fertilizers over synthetic alternatives. The segment's expansion is further supported by new regulations from the European Union, as part of the European Green Deal, which have made it possible to market more organic and waste-based fertilizers. The growing trend of organic farming in the region has also significantly contributed to the segment's growth, with the area under organic farming showing consistent expansion. Additionally, the unexplored scope of developing organic liquid fertilizers from various sources presents high-end growth potential for emerging players in this segment.

Segment Analysis: Mode of Application

Foliar Application Segment in Europe Liquid Fertilizers Market

The foliar application segment dominates the Europe liquid fertilizers market, commanding approximately 44% market share in 2024. For foliar fertilizers to be most effective, they should remain on leaves or other targeted plant tissue in liquid form as long as possible, which has favored the choice of liquid fertilizers for foliar application. This segment is also experiencing the fastest growth rate of around 5% during 2024-2029, driven by comprehensive studies showing that spraying chelated liquid fertilizer on leaves can reduce the total amounts of fertilizer applied while achieving high fertilizer efficiency. Research studies from prominent institutions like the University of Parma in Italy have demonstrated the advantageous effects of foliar application, particularly in winter wheat cultivation, where trials showed that foliar nitrogen fertilization with reduced doses maintains high yield and quality standards. Additionally, the laws regulating fertilizer production and commercialization in the European Union (EU) and its Member States predominantly focus on liquid products for foliar sprays, highlighting the significance of liquid fertilizers in foliar fertilization.

Remaining Segments in Mode of Application

The remaining segments in the mode of application include fertigation, starter solutions, aerial application, and injection into soil. Fertigation represents a significant portion of the market as it allows better control of nutrient application rates through irrigation systems, particularly beneficial in regions with water scarcity. Starter solutions are primarily adopted for transplanted vegetables and have gained popularity in indoor vegetable production through sustainable hydroponic nutrients techniques. Aerial application, though less common, is particularly valuable for production forests in remote locations and large-scale farms, especially with the evolution of agricultural drones and UAVs. The injection into soil segment, while smaller, plays a crucial role in preventing nutrient loss and is particularly effective for organic liquid fertilizers and manures as it reduces ammonia volatilization.

Segment Analysis: Application

Grains and Cereals Segment in Europe Liquid Fertilizers Market

The grains and cereals segment continues to dominate the Europe liquid fertilizers market, holding approximately 46% of the market share in 2024. Cereals account for a significant share of consumption in Europe, with major crops including wheat, barley, maize, and sorghum. Several studies have demonstrated substantial crop yield improvements through the application of liquid fertilizers in cereal production. The segment's dominance is particularly evident in countries like France, where the area under cereal crop cultivation has shown consistent growth. Trials carried out by farmers in the region have illustrated several advantages of liquid fertilizers in cereal production, including improved nutrient absorption and enhanced crop yields. The effectiveness of liquid fertilizers in cereals is particularly notable during critical growth phases, where uniform nutrient distribution is essential for optimal yield development.

Fruits and Vegetables Segment in Europe Liquid Fertilizers Market

The fruits and vegetables segment is projected to experience the highest growth rate of approximately 5% during the forecast period 2024-2029. This growth is primarily driven by the increasing adoption of precision farming techniques and the rising demand for high-quality produce in the European market. Liquid fertilizers play a crucial role in fruits and vegetables production, particularly in addressing specific nutrient requirements during various growth stages. The segment's growth is further supported by the expanding greenhouse production technology and the increasing trend of organic farming in countries like France. Calcium deficiency, a significant problem in leafy vegetables and salad leaves, has necessitated the use of liquid calcium fertilizers, especially in indoor and protected cultivation. The segment's expansion is also influenced by the growing adoption of fertigation systems in vegetable production, where liquid fertilizers prove highly efficient in delivering precise nutrient applications.

Remaining Segments in Application Market Segmentation

The remaining segments in the market include pulses and oilseeds, commercial crops, and other applications, each serving distinct agricultural needs. The pulses and oilseeds segment is particularly significant in regions focusing on protein crop production, with liquid fertilizers playing a vital role in improving yield and quality. Commercial crops, including sugarcane, cotton, and tobacco, benefit from liquid fertilizers' ability to address specific nutrient deficiencies and enhance crop quality. The other applications segment encompasses various uses including turf management, ornamental plants, and specialized crop applications. These segments collectively contribute to the market's diversity, offering specialized solutions for different crop types and growing conditions across Europe.

Europe Liquid Fertilizers Market Geography Segment Analysis

Europe Liquid Fertilizers Market in France

France dominates the European liquid fertilizers landscape, commanding approximately 11% of the regional market share. The country's leadership position is driven by its extensive agricultural base and progressive farming practices. France has adopted an ambitious plan to promote vegetable proteins, with a significant focus on precision agriculture techniques, including variable rate application and site-specific nutrient management. The country's farmers are increasingly embracing liquid fertilizers due to their compatibility with modern precision farming equipment such as sprayers and injection systems. Additionally, France has implemented a comprehensive Nitrate Action Program aimed at protecting water resources from agricultural pollution, which has encouraged farmers to switch to liquid fertilizers over solid variants due to better control of nutrient application rates and minimal risk of nitrate leaching. The country's agricultural sector benefits from sophisticated infrastructure and distribution networks, enabling efficient delivery of liquid fertilizers to farming communities across different regions.

Europe Liquid Fertilizers Market in Spain

Spain's liquid fertilizers market is projected to grow at approximately 5% CAGR from 2024 to 2029, emerging as the fastest-growing market in Europe. The country's unique agricultural landscape, characterized by arid and semi-arid regions, has necessitated efficient water management practices, making fertigation with liquid fertilizers an ideal solution. Spain's position as the world's largest olive producer has created substantial demand for liquid potassium fertilizers, which are particularly crucial for olive orchards. The regions of Castile-Leon, Andalusia, and Castile-La Mancha have emerged as the largest consumers of liquid fertilizers, primarily due to their extensive cereal production. The country's agricultural sector is witnessing a notable shift toward crops with higher biomass production, which has increased the adoption of liquid fertilizers. Furthermore, Spain's commitment to water-conserving practices and the growing implementation of advanced irrigation systems has created a favorable environment for liquid fertilizer applications.

Europe Liquid Fertilizers Market in Russia

Russia has established itself as a major force in the European liquid fertilizers market, leveraging its robust manufacturing capabilities and abundant raw material resources. The country has demonstrated significant advancement in liquid fertilizer technology, particularly in the development and application of urea-ammonium nitrate (UAN) solutions. Russian agricultural practices have evolved to embrace innovative fertilizer applications, especially in field crops, which constitute the major share of liquid fertilizer consumption. The country's research institutions actively conduct studies on fertilizer efficiency, particularly focusing on potato cultivation and other strategic crops. Russia's extensive agricultural land and diverse climatic conditions have necessitated the development of specialized liquid fertilizer formulations suitable for different regions and crop types. The country's self-sufficiency in fertilizer production, coupled with its strong distribution infrastructure, has created a sustainable ecosystem for the liquid fertilizers market.

Europe Liquid Fertilizers Market in Germany

Germany's liquid fertilizers market is characterized by its high-tech approach to agriculture and strong focus on environmental sustainability. The country's North German Plain, known for its fertile soils and intensive agricultural production, has become a key consumption center for liquid fertilizers, particularly in large-scale arable farming systems cultivating wheat, barley, rapeseed, and sugar beets. The Lower Rhine region, with its concentrated horticultural and greenhouse cultivation, represents another significant market for liquid fertilizers. Germany's well-established biogas industry has created unique opportunities for liquid fertilizer applications, with digestate being increasingly used as a nutrient-rich fertilizer. The country's strong emphasis on research and development has led to continuous innovations in liquid fertilizer formulations and application technologies. German farmers' increasing adoption of precision farming techniques has further boosted the demand for liquid fertilizers, which offer superior compatibility with modern agricultural equipment.

Europe Liquid Fertilizers Market in Other Countries

The remaining European countries, including the United Kingdom, Italy, Netherlands, Belgium, and other nations, collectively represent a significant portion of the liquid fertilizers market. These markets are characterized by diverse agricultural practices and varying levels of technological adoption. The United Kingdom's focus on addressing micronutrient solution deficiencies, Italy's growing organic farming sector, and the Netherlands' advanced greenhouse cultivation systems all contribute to the regional market dynamics. Eastern European countries are showing increasing interest in liquid fertilizers as they modernize their agricultural practices. The Nordic countries, with their specific climatic challenges, have developed specialized applications for liquid fertilizers. These markets benefit from the European Union's common agricultural policies and environmental regulations, which increasingly favor precise nutrient application methods. The varying soil conditions, crop patterns, and farming practices across these countries continue to drive innovation in liquid fertilizer formulations and application technologies.

Get Analysis on Important Geographic Markets

Download PDF

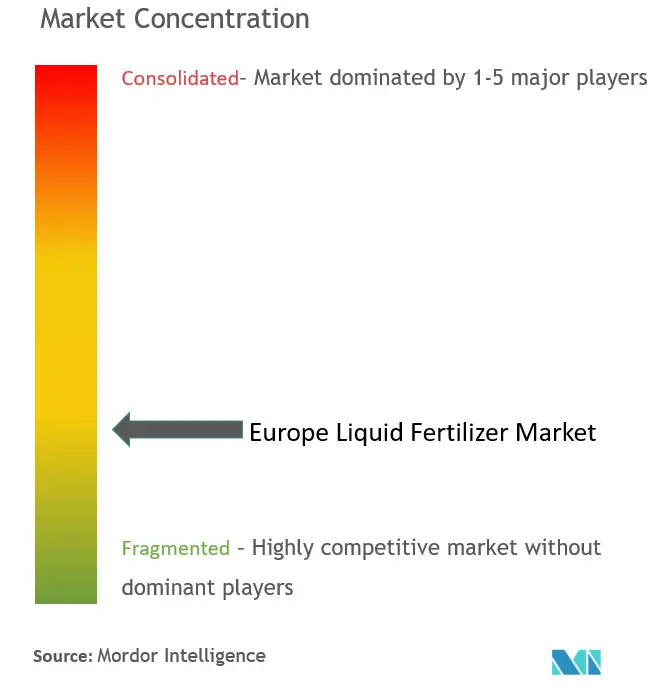

Europe Liquid Fertilizer Industry Overview

Top Companies in Europe Liquid Fertilizers Market

The European liquid fertilizers market is led by established players like Yara International ASA, Tessenderlo Group, ICL Fertilizers, and Compo Expert, who have built a strong regional presence through extensive distribution networks and manufacturing facilities. The market has seen limited product innovations in recent years, with companies focusing more on operational expansion and strategic acquisitions to strengthen their positions. Key strategic moves have centered around acquiring logistics and storage facilities to improve distribution capabilities, particularly evident in companies like Tessenderlo Group and Compo Expert's recent expansions. Manufacturing capacity enhancement has been another prominent trend, with companies like BTU Center and NordFert establishing new production lines and facilities to meet growing regional demand. The emphasis has been on developing comprehensive solutions for precision agriculture and liquid organic fertilizers applications, reflecting the evolving needs of European farmers.

Fragmented Market with Strong Regional Players

The European liquid fertilizers market exhibits a fragmented structure with a mix of global conglomerates and regional specialists operating across different geographical segments. Major global players like Yara International maintain dominant positions through their extensive manufacturing capabilities and well-established distribution networks, while regional specialists such as BMS Micro-Nutrients and Ledra Group have carved out niches through specialized product offerings and local market expertise. The market shows moderate consolidation levels, with the top players collectively holding a significant but not overwhelming market share, leaving room for smaller players to operate in specialized segments.

The market has witnessed strategic mergers and acquisitions aimed at strengthening distribution capabilities and expanding geographical presence. Companies have focused on acquiring complementary businesses, particularly in logistics and storage infrastructure, to enhance their supply chain efficiency. The trend of vertical integration is evident, with larger players acquiring smaller companies to gain access to new markets or specialized product portfolios. This M&A activity has been particularly pronounced in key markets like Germany, France, and the Benelux region, where companies seek to consolidate their positions and achieve operational synergies.

Innovation and Distribution Drive Market Success

For incumbent companies to maintain and increase their market share, the focus needs to be on developing innovative product formulations that address specific crop needs and align with the growing trend toward sustainable agriculture. Success factors include investing in research and development to create more efficient nutrient delivery systems, expanding distribution networks to improve market access, and developing integrated solutions that combine products with digital farming technologies. Companies must also strengthen their positions in key agricultural regions while simultaneously exploring opportunities in emerging markets within Eastern Europe.

New entrants and smaller players can gain ground by focusing on specialized market segments, particularly in organic farming and precision agriculture applications. The development of niche products for specific crop types or regional growing conditions presents opportunities for differentiation. Building strong relationships with local distributors and agricultural service providers is crucial for market penetration. However, companies must navigate challenges such as high customer loyalty to established brands, significant capital requirements for manufacturing facilities, and increasingly stringent environmental regulations. The ability to offer comprehensive technical support and demonstrate clear value propositions to farmers will be crucial for success in this competitive landscape. The role of agricultural nutrients in enhancing crop yield and the strategic use of fluid fertilizers in precision agriculture are pivotal for future growth.

Europe Liquid Fertilizer Market Leaders

-

Yara International ASA

-

ICL Group Ltd.

-

Grupa Azoty S.A.

-

CF Industries Holdings, Inc.

-

Sociedad Quimica y Minera de Chile SA (SQM)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Liquid Fertilizer Market News

- September 2024: Grupa Azoty S.A. launched an improved version of its RSM (urea-ammonium nitrate solution), a widely used urea-ammonium nitrate solution. This new formulation, called RSM OPTIMA, is enriched with copper, boron, and molybdenum.

- April 2024: Yara International ASA launched YaraVita B-Phos, a novel foliar liquid fertilizer for legumes, in Germany. This product contains phosphorus and boron nutrients along with bioactive compounds, including alkanolamine salts and algae extracts rich in phytohormones.

- April 2024: Grupa Azoty S.A. has finalized contracts in the Agro segment for the 2024/2025 season. The company has signed 66 agreements with its authorized distribution network for the domestic fertilizer market. Through this partnership, the company aims to increase the supply of liquid fertilizers in the European and global markets.

Europe Liquid Fertilizers Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Importance of Precision Farming

- 4.2.2 Decreasing Arable Land

- 4.2.3 Growing Government Support and Initiative

-

4.3 Market Restraints

- 4.3.1 Increase in Adoption of Oragnic Farming

- 4.3.2 Comparative High Cost

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

- 5.1 Complex

-

5.2 Straight

- 5.2.1 Micronutrients

- 5.2.2 Nitrogenous

- 5.2.3 Phosphatic

- 5.2.4 Potassic

- 5.2.5 Secondary Macronutrients

-

5.3 Mode of Application

- 5.3.1 Fertigation

- 5.3.2 Foliar Application

-

5.4 Cop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental Crops

-

5.5 Geography

- 5.5.1 France

- 5.5.2 Germany

- 5.5.3 Italy

- 5.5.4 Netherlands

- 5.5.5 Russia

- 5.5.6 Spain

- 5.5.7 United Kingdom

- 5.5.8 Ukraine

- 5.5.9 Rest of Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Yara International ASA

- 6.3.2 ICL Group Ltd

- 6.3.3 Grupa Azoty S.A.

- 6.3.4 BMS Micro-nutrients NV

- 6.3.5 CF Industries Holdings, Inc.

- 6.3.6 Nordfert

- 6.3.7 YILDIRIM Group

- 6.3.8 Sociedad Quimica y Minera de Chile SA (SQM)

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Liquid Fertilizer Industry Segmentation

Liquid fertilizers are concentrates or water-soluble powders of synthetic chemicals of nitrogen, phosphorus, potassium, secondary macronutrients, and other micronutrient. The European liquid fertilizer market is segmented by Complex, Straight (Micronutrients, Nitrogenous, Phosphatic, Potassic, and Secondary Macronutrients), Mode of Application (Fertigation and Foliar application, Crop Type (Field crops, Horticultural crops, and Turf and Ornamental crops), and Geography (France, Italy, Germany, Netherlands, Russia, Spain, Ukraine, United Kingdom, and Rest of Europe). For each segment, the market sizing and forecasts have been done based on value (USD).

| Straight | Micronutrients |

| Nitrogenous | |

| Phosphatic | |

| Potassic | |

| Secondary Macronutrients | |

| Mode of Application | Fertigation |

| Foliar Application | |

| Cop Type | Field Crops |

| Horticultural Crops | |

| Turf and Ornamental Crops | |

| Geography | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| United Kingdom | |

| Ukraine | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe Liquid Fertilizers Market Research Faqs

How big is the Europe Liquid Fertilizers Market?

The Europe Liquid Fertilizers Market size is expected to reach USD 3.48 billion in 2025 and grow at a CAGR of 5.5% to reach USD 4.55 billion by 2030.

What is the current Europe Liquid Fertilizers Market size?

In 2025, the Europe Liquid Fertilizers Market size is expected to reach USD 3.48 billion.

Who are the key players in Europe Liquid Fertilizers Market?

Yara International ASA, ICL Group Ltd., Grupa Azoty S.A., CF Industries Holdings, Inc. and Sociedad Quimica y Minera de Chile SA (SQM) are the major companies operating in the Europe Liquid Fertilizers Market.

What years does this Europe Liquid Fertilizers Market cover, and what was the market size in 2024?

In 2024, the Europe Liquid Fertilizers Market size was estimated at USD 3.29 billion. The report covers the Europe Liquid Fertilizers Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Liquid Fertilizers Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Liquid Fertilizers Market Research

Mordor Intelligence offers a comprehensive analysis of the liquid fertilizers industry. We leverage decades of expertise in agricultural nutrients research. Our latest report examines the complete spectrum of products, including NPK liquid fertilizers, liquid organic fertilizers, and liquid biofertilizers. The analysis covers various application methods such as foliar fertilizers, spray fertilizers, and drip fertilizers. It also explores emerging technologies in fertigation solutions and suspension fertilizers.

Stakeholders gain valuable insights into the evolving landscape of liquid plant nutrients and fluid fertilizers. The report provides a detailed examination of hydroponic nutrients and water soluble fertilizers applications. Available as an easy-to-download PDF, it offers an in-depth analysis of liquid plant food trends, micronutrient solution developments, and the impacts of liquid soil amendments. Special attention is given to sustainable practices, including crop nutrition solutions and advanced fertigation solutions. This enables businesses to make informed decisions in this dynamic market segment.