| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2029 |

| Market Size (2025) | USD 2.36 Billion |

| Market Size (2029) | USD 4.39 Billion |

| CAGR (2025 - 2029) | 16.80 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe LFP Battery Pack Market Analysis

The Europe LFP Battery Pack Market size is estimated at 2.36 billion USD in 2025, and is expected to reach 4.39 billion USD by 2029, growing at a CAGR of 16.80% during the forecast period (2025-2029).

The European LFP battery pack industry is experiencing transformative growth driven by technological advancements and shifting market dynamics. Major automotive manufacturers are increasingly adopting lithium iron phosphate battery technology due to its enhanced safety features, longer lifespan, and improved cost-effectiveness compared to other battery chemistries. This shift is evidenced by Toyota Group's dominant position, accounting for 14.84% of the European electric car market in 2023. The industry is witnessing significant improvements in battery performance, with manufacturers focusing on increasing energy density and reducing charging times while maintaining the inherent safety advantages of LFP chemistry.

The supply chain landscape for LFP battery packs in Europe is undergoing substantial restructuring as the region aims to reduce dependency on external markets. Currently, Europe accounts for only 3% of global battery production, but ambitious initiatives are underway to capture 25% of the world battery market by 2030. This strategic push has attracted significant investments in domestic battery manufacturing capabilities, with major players like CATL establishing production facilities with capacities exceeding 70 GWh per year. The localization of production is expected to strengthen supply chain resilience and reduce logistics costs for European automotive manufacturers.

Battery technology innovation continues to drive market evolution, with manufacturers achieving breakthrough improvements in energy density and thermal management systems. LFP batteries have gained significant traction, capturing more than 8% of the battery chemistry market share in 2022, driven by their superior safety profile and competitive cost structure. The industry is witnessing increased collaboration between battery manufacturers and automotive OEMs to develop customized solutions that optimize performance while maintaining cost competitiveness. The integration of advanced battery management systems is further enhancing the efficiency and reliability of these solutions.

The economic landscape of the LFP battery pack market is characterized by declining production costs and improving economies of scale. Battery pack prices have shown a consistent downward trend, with costs decreasing by 14.11% year-over-year, making electric vehicles more accessible to mainstream consumers. This cost reduction is driven by technological improvements in manufacturing processes, increased automation, and optimization of material usage. The industry is also benefiting from standardization initiatives that are helping to streamline production processes and reduce manufacturing complexity, leading to further cost efficiencies. As the market evolves, the focus on sustainable battery solutions is becoming increasingly prominent, aligning with global environmental goals.

Europe LFP Battery Pack Market Trends

TOYOTA GROUP LEADS THE EUROPEAN EV MARKET, FOLLOWED BY RENAULT, TESLA, KIA, AND BMW

- The market for electric vehicles in various European countries is growing significantly, with numerous players operating, but it is largely driven by five major companies, which held more than 50% of the market in 2022. These companies include Toyota Group, Kia, Renault, Tesla, Kia, and Volkswagen. Toyota Group is the largest seller of electric vehicles in Europe, accounting for around 14.84% share of the electric car market. The company has a strong supply and distribution network catering to the demand and supply of customers in various European countries. The company has a wide product portfolio offering in the EV market.

- Renault holds a market share of around 7.47%, making it the second-largest seller of electric vehicles across Europe. The company has a good brand image and a strong financial position. The company has alliances and strategic partnerships with good brands such as Nissan. The 3rd highest market share, 6.71%, for electric vehicle sales was recorded by Tesla. The business focuses on cutting-edge innovations and has solid strategic alliances with producers of several EV parts, including batteries.

- The 4th largest place in European EV sales is Kia, accounting for around 6.26% of the market share. The company has wide product offerings for various types of customers with various budget-friendly options compared to other brands. The 5th largest player operating in the European EV market is BMW, maintaining its market share at around 6.14%. Some of the other players selling EVs in various European countries include Hyundai, Mercedes-Benz, BMW, Audi, and Ford.

Understand The Key Trends Shaping This Market

Download PDF

Tesla and Renault are the largest contributors to the demand for battery packs, as a result of the widespread sale of EVs in Europe in 2022

- The demand for electric vehicles has dramatically increased during the past several years in every part of Europe. Electric vehicles are now more prevalent on European roadways. Although consumer interest in buying electric vehicles varies by area and by country, SUVs are the most popular type of electric vehicle in Germany and the United Kingdom, the region's two biggest markets for electric vehicles. The demand for electric SUVs is outpacing that for sedans in various European countries due to the increased interest in comfortable transportation and the fact that SUVs are roomier than sedans.

- The number of compact SUVs purchased by consumers has increased dramatically across Europe. The Tesla Model Y offers a fully electric motor, a 5-star NCAP safety certification, spacious seating for up to 7 passengers, a long-range, and other features. It became one of the most popular models in several major European markets, including the United Kingdom and Germany, in 2022. The Renault Arkana provides a full hybrid engine, which has received a strong sales reaction from customers in several European nations like France due to its fuel efficiency and competitive pricing.

- Captur was one of the best sellers from Renault in the European countries in 2022, owing to its offering of a hybrid and a plug-in hybrid powertrain, and is packed with lots of features attracting buyers. The European EV market also features a variety of electric SUVs and sedans from various international brands. One of the common cars is the Toyota Yaris and Ford Kuga, which recorded good sales in 2022. Other cars in the European EV market that are in the competition include the Fiat 500 and Toyota Yaris Cross.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Environmental Concerns, Government Support, and Decarbonization Goals Fuel European Electric Vehicle Demand and Sales

- Declining Battery Prices and Government Initiatives Drive Demand for Electric Vehicles in Europe

- Technological innovations, production efficiency, and competition are expected to continue exerting downward pressure on lithium-ion battery prices in Europe

- Rising Sales and Government Initiatives Signal Robust Growth in the European Electric Vehicle Sector

- Growth in Demand for Various Battery Chemistries Across European Countries

- Demand for Battery Materials and Evolving Battery Chemistries Increases as Europe’s Electric Vehicle Market Grows

- Sales of Electric Vehicles in Europe Rise Due to Developments in Battery Technology

Segment Analysis: Body Type

Passenger Car Segment in Europe LFP Battery Pack Market

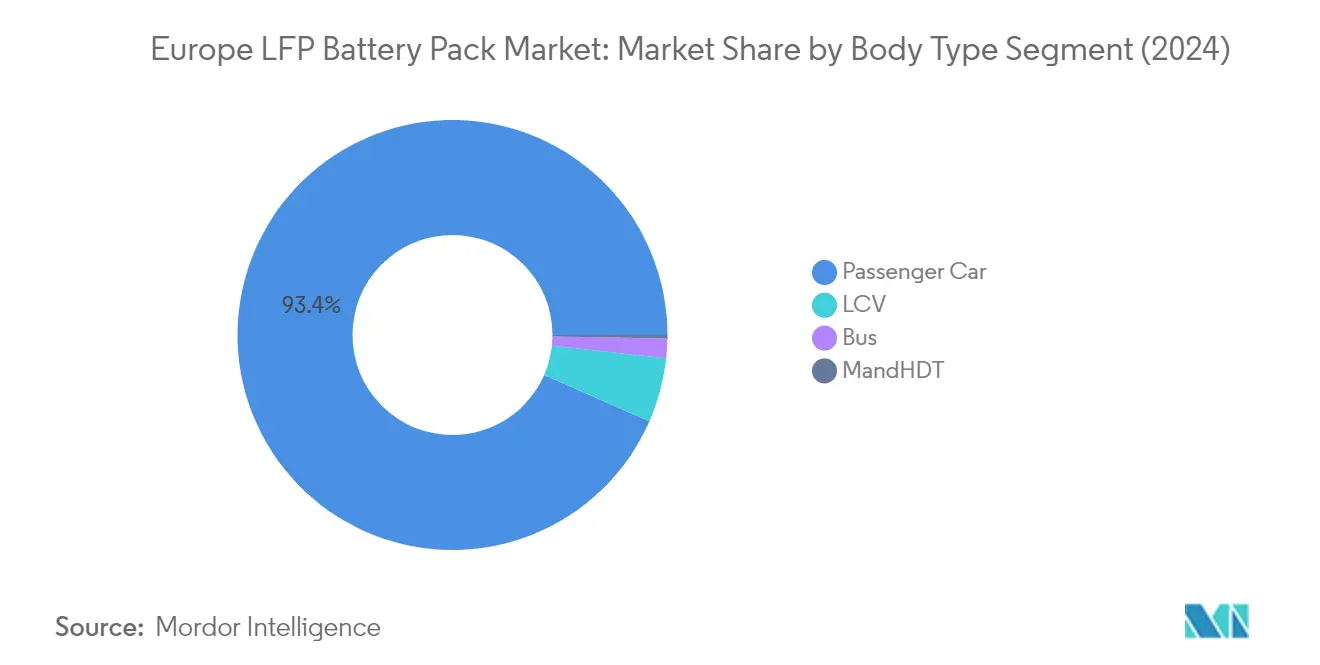

The passenger car segment dominates the European LFP battery pack market, commanding approximately 93% market share in 2024. This substantial market position is driven by the increasing adoption of electric passenger vehicles across major European markets. The segment's growth is supported by favorable government policies promoting electric vehicle adoption, including purchase subsidies and tax incentives in key markets like Germany, France, and the UK. Additionally, the expanding charging infrastructure network across Europe and technological advancements in LFP battery cell technology, particularly in terms of energy density and charging capabilities, have made electric passenger vehicles more attractive to consumers. Major automotive manufacturers are also expanding their electric vehicle portfolios with LFP battery module options, recognizing the chemistry's advantages in terms of cost-effectiveness, safety, and longevity.

M&HDT Segment in Europe LFP Battery Pack Market

The Medium and Heavy-Duty Truck (M&HDT) segment is emerging as the fastest-growing segment in the European LFP battery pack market, with a projected growth rate of approximately 64% during the forecast period 2024-2029. This remarkable growth is driven by increasing regulations on commercial vehicle emissions across European cities and the growing focus on sustainable logistics solutions. Fleet operators are increasingly recognizing the total cost of ownership benefits of electric trucks, particularly in urban delivery and regional haul applications. The segment's growth is further supported by the development of high-capacity charging infrastructure specifically designed for commercial vehicles and the introduction of new electric truck models from major manufacturers. Additionally, government initiatives targeting the decarbonization of commercial transport and the availability of subsidies for electric truck purchases are accelerating the adoption of electric M&HDT vehicles.

Remaining Segments in Body Type

The Light Commercial Vehicle (LCV) and Bus segments complete the European LFP battery pack market landscape, each playing distinct roles in the market's development. The LCV segment is particularly significant in urban delivery and last-mile logistics applications, where the operational benefits of electric vehicles are most pronounced. The bus segment, while smaller in volume, represents a strategic sector for public transportation electrification initiatives across European cities. Both segments benefit from specific government support programs and municipal clean air initiatives. The adoption of LFP batteries in these segments is driven by the chemistry's inherent advantages, including improved safety characteristics, longer cycle life, and lower total cost of ownership, making them particularly suitable for commercial applications where reliability and cost-effectiveness are paramount considerations.

Segment Analysis: Propulsion Type

BEV Segment in Europe LFP Battery Pack Market

Battery Electric Vehicles (BEV) have emerged as the dominant force in the European LFP battery pack market, commanding approximately 87% of the market share in 2024. This substantial market presence can be attributed to several factors, including the increasing adoption of pure electric vehicles across European countries, particularly in regions like Germany, France, and the Nordic countries. The segment's growth is being driven by favorable government policies, expanding charging infrastructure, and increasing consumer awareness about environmental sustainability. Major automotive manufacturers are increasingly focusing on BEV production, with companies like Tesla, Volkswagen, and Renault leading the charge. The segment is also benefiting from technological advancements in LFP battery cell technology, which has improved energy density and reduced costs. Additionally, the segment is experiencing the highest growth rate in the market, projected to expand at approximately 28% from 2024 to 2029, driven by stringent emission regulations, government incentives, and increasing consumer preference for zero-emission vehicles.

PHEV Segment in Europe LFP Battery Pack Market

The Plug-in Hybrid Electric Vehicle (PHEV) segment represents a significant portion of the European LFP battery pack market, serving as a transitional technology between conventional vehicles and pure electric vehicles. This segment is experiencing steady growth, driven by consumers who seek the flexibility of both electric and conventional powertrains. The PHEV segment benefits from various government incentives and subsidies across European countries, making these vehicles an attractive option for consumers who want to reduce their environmental impact while maintaining the convenience of traditional fuel options. Automotive manufacturers are continuing to invest in PHEV technology, introducing new models with improved electric range and performance capabilities. The segment is particularly popular in urban areas where short-distance electric-only operation is feasible, while the conventional engine provides peace of mind for longer journeys. Market dynamics indicate that PHEVs will continue to play a crucial role in the transition towards full electrification, especially in regions where charging infrastructure is still developing.

Segment Analysis: Capacity

Above 80 kWh Segment in Europe LFP Battery Pack Market

The Above 80 kWh segment has emerged as the dominant force in the European LFP battery pack market, commanding approximately 35% of the total market share in 2024. This significant market position can be attributed to the increasing demand for high-capacity battery packs in premium electric vehicles and commercial applications. The segment's growth is being driven by automotive manufacturers' focus on developing long-range electric vehicles to address consumer range anxiety concerns. Additionally, the Above 80 kWh segment benefits from technological advancements in battery chemistry and manufacturing processes, which have helped improve energy density while maintaining the inherent safety advantages of LFP technology. The segment's strong performance is further supported by the growing adoption of electric buses and heavy-duty vehicles that require high-capacity battery packs for extended operational range.

40 kWh to 80 kWh Segment in Europe LFP Battery Pack Market

The 40 kWh to 80 kWh segment is demonstrating remarkable growth potential in the European LFP battery pack market, with an expected growth rate of approximately 20% during the forecast period 2024-2029. This impressive growth trajectory is driven by the segment's sweet spot positioning in the market, offering an optimal balance between range capability and cost-effectiveness for mainstream electric vehicles. The segment is benefiting from increasing investments in manufacturing capabilities across Europe, with several major battery manufacturers expanding their production facilities. Technological innovations in cell design and pack assembly are further enhancing the segment's appeal, while improvements in energy density and charging capabilities are making these battery packs increasingly attractive to both automotive manufacturers and consumers. The segment's growth is also supported by favorable government policies promoting the adoption of electric vehicles in the mid-range category.

Remaining Segments in Capacity

The Less than 15 kWh and 15 kWh to 40 kWh segments play crucial roles in serving specific market niches within the European LFP battery pack ecosystem. The Less than 15 kWh segment primarily caters to urban mobility solutions, including small city cars and plug-in hybrid vehicles, offering cost-effective electrification solutions for short-range applications. Meanwhile, the 15 kWh to 40 kWh segment serves the compact electric vehicle market, providing an attractive option for urban and suburban commuting needs. Both segments benefit from the ongoing trend toward vehicle electrification and are particularly important in markets where space constraints and cost considerations are primary factors in vehicle selection. These segments continue to evolve with improvements in battery technology and manufacturing efficiency, maintaining their relevance in the broader market landscape.

Segment Analysis: Battery Form

Segment Analysis: Method

Laser Segment in Europe LFP Battery Pack Market

The laser bonding method has emerged as the dominant segment in the European LFP battery pack market, commanding approximately 61% of the market share in 2024. This significant market position can be attributed to laser bonding's superior precision, minimal adhesive usage, and cost-effectiveness in battery pack manufacturing. The segment is also experiencing the fastest growth trajectory, expected to grow at around 36% annually from 2024 to 2029. This remarkable growth is driven by several factors, including the increasing adoption of laser technology by major battery manufacturers, its ability to enhance battery pack durability and lifespan, and the growing focus on high-quality, reliable bonding methods for electric vehicle batteries. The laser bonding method's popularity is further reinforced by its environmental benefits, as it minimizes waste and improves overall production efficiency. Additionally, advancements in laser technology, such as improved weld quality and reduced cycle times, are making it an increasingly attractive choice for manufacturers looking to scale up their production capabilities.

Remaining Segments in Method

The wire bonding method represents the alternative approach in the European LFP battery pack market, offering its own set of advantages and applications. Wire bonding has traditionally been valued for its reliability and established track record in battery pack assembly. This method continues to find applications in specific battery configurations where its particular characteristics are advantageous. The wire bonding technique is particularly favored in scenarios requiring flexible production setups and when dealing with certain battery cell configurations. While the market is shifting towards laser bonding, wire bonding maintains its relevance through continuous technological improvements and optimization of production processes. The method's established infrastructure and expertise base in many manufacturing facilities ensure its continued presence in the market, particularly in specialized applications and specific battery pack designs where its characteristics provide unique advantages.

Segment Analysis: Component

Cathode Segment in Europe LFP Battery Pack Market

The cathode segment has emerged as the dominant component in the European LFP battery pack market, commanding approximately 69% of the total market value in 2024. This substantial market share can be attributed to the critical role cathodes play in determining battery performance, energy density, and overall efficiency. The segment's dominance is further strengthened by continuous technological advancements in cathode materials, particularly in improving energy density and thermal stability. Major manufacturers are investing heavily in research and development to enhance cathode performance while reducing production costs. The segment's growth is also supported by increasing partnerships between battery manufacturers and material suppliers to secure stable cathode material supply chains across Europe.

Separator Segment in Europe LFP Battery Pack Market

The separator segment is projected to exhibit the strongest growth trajectory in the European LFP battery pack market from 2024 to 2029, with an expected growth rate of approximately 18%. This remarkable growth is driven by increasing emphasis on battery safety and performance optimization. Manufacturers are focusing on developing advanced separator technologies that offer enhanced thermal stability and improved ionic conductivity. The segment's growth is further supported by innovations in separator materials, including the introduction of ceramic-coated separators and composite materials that significantly enhance battery safety and longevity. European battery manufacturers are increasingly investing in high-performance separator technologies to meet the stringent safety requirements of electric vehicle applications.

Remaining Segments in Component

The anode and electrolyte segments continue to play vital roles in shaping the European LFP battery pack market landscape. The anode segment is witnessing significant developments in material technology, with manufacturers exploring various carbon-based materials to improve battery performance and charging capabilities. The electrolyte segment, while smaller in market share, remains crucial for battery functionality and performance optimization. Both segments are experiencing continuous innovation, with manufacturers focusing on developing new materials and compositions to enhance battery efficiency and safety. The ongoing research and development in these segments are contributing to the overall advancement of LFP battery technology in Europe.

Segment Analysis: Material Type

Nickel Segment in Europe LFP Battery Pack Market

The nickel segment has emerged as a dominant force in the European LFP battery pack market, commanding approximately 35% market share in 2024. This significant market position can be attributed to nickel's crucial role in enhancing battery performance and energy density. The segment's growth is being driven by increasing demand from electric vehicle manufacturers who are focusing on developing high-performance batteries with extended range capabilities. European battery manufacturers are increasingly incorporating nickel in their battery chemistry to achieve better energy density and overall performance. The segment has also benefited from strategic partnerships between major automotive OEMs and battery manufacturers, leading to increased adoption of nickel-based LFP batteries across various applications.

Natural Graphite Segment in Europe LFP Battery Pack Market

The natural graphite segment is demonstrating remarkable growth potential in the European LFP battery pack market, with projections indicating strong expansion from 2024 to 2029. This growth is being fueled by the increasing focus on sustainable and cost-effective battery materials. Natural graphite's superior conductivity properties and its role as a crucial anode material are driving its adoption in LFP battery manufacturing. European battery manufacturers are investing heavily in securing sustainable sources of natural graphite to meet the growing demand from the electric vehicle sector. The segment is also benefiting from technological advancements in graphite processing and purification techniques, which are improving the material's performance characteristics in battery applications.

Remaining Segments in Material Type

The other significant materials in the European LFP battery pack market include cobalt, lithium, and manganese, each playing vital roles in battery performance and functionality. Cobalt continues to be essential for thermal stability and overall battery safety, while lithium remains fundamental to the battery's core chemistry and energy storage capabilities. Manganese serves as a crucial component in optimizing battery performance and cost-effectiveness. These materials are experiencing varying levels of demand based on evolving battery technologies and manufacturer preferences. The market dynamics for these materials are influenced by factors such as supply chain sustainability, environmental considerations, and ongoing research and development efforts to optimize battery chemistry formulations.

Europe LFP Battery Pack Market Geography Segment Analysis

Europe LFP Battery Pack Market in Germany

Germany stands as the powerhouse of Europe's LFP battery pack market, commanding approximately 30% of the total market volume in 2024. The country's dominance is underpinned by its robust automotive manufacturing infrastructure and substantial investments in electric vehicle technology. The German government's commitment to sustainable transportation has created a favorable environment for lithium iron phosphate battery manufacturers, with numerous incentives and support mechanisms in place. The presence of major automotive OEMs and their increasing focus on electric vehicle production has attracted significant investments in battery manufacturing facilities across the country. The country's strategic location and well-developed logistics infrastructure have made it an ideal hub for LFP battery pack production and distribution across Europe. Furthermore, Germany's strong research and development capabilities have fostered innovation in battery technology, leading to improvements in energy density and performance. The collaboration between industry players, research institutions, and government bodies has created a robust ecosystem that continues to drive market growth.

Europe LFP Battery Pack Market in Sweden

Sweden has emerged as a significant player in Europe's LFP battery pack market, driven by its comprehensive approach to electric mobility and sustainable energy solutions. The country's strong focus on environmental sustainability has created a robust market for electric vehicles and associated technologies. Swedish manufacturers have been particularly successful in developing innovative battery solutions that cater to the specific requirements of the Nordic climate. The country's rich mineral resources, particularly in terms of raw materials needed for battery production, have attracted substantial investments from both domestic and international players. The Swedish government's supportive policies and regulations have created a favorable environment for battery manufacturers and suppliers. The presence of well-established research institutions and technology centers has facilitated continuous innovation in battery technology. Additionally, the country's strong focus on circular economy principles has led to the development of efficient battery recycling programs, making the Swedish market more sustainable and environmentally friendly.

Europe LFP Battery Pack Market in France

France has established itself as a crucial market for lithium iron phosphate battery packs, supported by its strong automotive industry and commitment to clean energy transition. The country's strategic approach to developing its battery industry has attracted significant investments from both domestic and international players. French authorities have implemented comprehensive support mechanisms for the electric vehicle industry, including research grants and manufacturing incentives. The country's focus on developing a complete battery value chain, from raw material processing to recycling, has created numerous opportunities for market growth. France's strong technological capabilities and research infrastructure have contributed to advancements in battery technology and manufacturing processes. The collaboration between automotive manufacturers, battery producers, and research institutions has created a dynamic ecosystem for innovation. Furthermore, the country's emphasis on developing charging infrastructure has helped boost confidence in electric vehicle adoption, directly impacting the demand for LFP battery packs.

Europe LFP Battery Pack Market in Other Countries

The LFP battery pack market in other European countries, including the United Kingdom, Italy, Hungary, and Poland, demonstrates varying degrees of development and potential. These markets are characterized by their unique approaches to electric mobility and energy storage solutions. Each country has implemented specific policies and incentives to promote the adoption of electric vehicles and the development of battery manufacturing capabilities. The United Kingdom has focused on developing its domestic battery manufacturing capacity, while Italy has leveraged its strong automotive manufacturing heritage to attract investments in battery technology. Hungary has positioned itself as an emerging hub for battery production, attracting significant foreign investment, while Poland has focused on developing its battery supply chain infrastructure. These markets benefit from the broader European Union's support for battery technology development and electric vehicle adoption. The varying levels of market maturity and different regulatory approaches in these countries create a diverse landscape of opportunities for market participants. Additionally, the integration of renewable energy storage solutions and battery management system advancements are pivotal in enhancing the efficiency and sustainability of these markets.

Get Analysis on Important Geographic Markets

Download PDF

Europe LFP Battery Pack Industry Overview

Top Companies in Europe LFP Battery Pack Market

The European LFP battery pack market is characterized by intense competition and continuous innovation among key players. Companies are focusing on developing advanced battery technologies with improved energy density, faster charging capabilities, and enhanced safety features. Strategic partnerships and collaborations with automotive manufacturers have become crucial for market expansion, with many players establishing joint ventures to strengthen their position. Manufacturers are investing heavily in research and development to optimize battery performance and reduce production costs. The industry is witnessing significant capacity expansion through new manufacturing facilities across Europe, particularly in countries like Germany, France, and Sweden. Companies are also emphasizing sustainable production methods and circular economy principles, including battery recycling programs and environmentally friendly manufacturing processes.

Market Dominated by Global Battery Specialists

The European LFP battery pack market exhibits a consolidated structure dominated by established global players, particularly from Asia, who have brought their expertise and technology to the European market. These major players leverage their extensive experience in battery technology, established supply chains, and strong relationships with automotive manufacturers to maintain their market positions. The market is characterized by high entry barriers due to significant capital requirements, technical expertise needs, and stringent quality standards, which favor large, well-established companies.

The industry is experiencing active merger and acquisition activity as companies seek to expand their technological capabilities and market presence. Traditional automotive suppliers and energy companies are entering the market through strategic acquisitions and partnerships with battery technology specialists. Local European players are emerging through government support and regional initiatives aimed at establishing domestic battery production capabilities. The market structure is evolving with increasing vertical integration as manufacturers seek to control critical aspects of the supply chain and reduce dependence on external suppliers.

Innovation and Localization Drive Future Success

Success in the European lithium iron phosphate battery market increasingly depends on companies' ability to innovate while maintaining cost competitiveness. Manufacturers need to focus on developing next-generation battery technologies that offer improved performance, longer lifespan, and enhanced safety features. Building strong relationships with automotive OEMs through customized solutions and reliable supply chains is becoming crucial. Companies must also invest in local production facilities to benefit from government incentives and reduce logistics costs while meeting growing demand for regional supply chains.

The market's future will be shaped by companies' ability to adapt to evolving regulatory requirements, particularly regarding sustainability and recycling. Success factors include developing efficient recycling processes, implementing sustainable production methods, and ensuring compliance with European battery regulations. Companies need to maintain flexibility in their production systems to accommodate rapid technological changes and varying customer requirements. Building strong research and development capabilities, either internally or through partnerships with research institutions, will be essential for long-term success. Additionally, manufacturers must focus on developing comprehensive service offerings, including battery management systems and after-sales support, to differentiate themselves in an increasingly competitive market.

Europe LFP Battery Pack Market Leaders

-

BYD Company Ltd.

-

Contemporary Amperex Technology Co. Ltd. (CATL)

-

Prime Planet Energy & Solutions Inc.

-

SK Innovation Co. Ltd.

-

Vehicle Energy Japan Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Free With This Report

Our comprehensive data set offers over 120 free charts, providing detailed regional and country-level insights into the EV battery pack industry. This includes analyses of distribution and production centers, variations in average selling prices (ASPs) across different regions, and a deep dive into industry trends like demand shifts and technological innovations. We also offer a thorough market segmentation, examining different battery chemistries, capacities, and form factors, alongside an in-depth understanding of market trends such as the adoption of advanced technologies and the impact of environmental regulations. Additionally, we provide an overview of major industry players, a look at the regulatory landscape, and market size analysis in terms of revenue and volume, all culminating in projections and forecasts that consider emerging trends and potential industry shifts.

Europe LFP Battery Pack Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

-

4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 France

- 4.11.3 Germany

- 4.11.4 Hungary

- 4.11.5 Poland

- 4.11.6 UK

- 4.12 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

-

5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

-

5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

-

5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

-

5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

-

5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

-

5.7 Material Type

- 5.7.1 Cobalt

- 5.7.2 Lithium

- 5.7.3 Manganese

- 5.7.4 Natural Graphite

- 5.7.5 Nickel

- 5.7.6 Other Materials

-

5.8 Country

- 5.8.1 France

- 5.8.2 Germany

- 5.8.3 Hungary

- 5.8.4 Italy

- 5.8.5 Poland

- 5.8.6 Sweden

- 5.8.7 UK

- 5.8.8 Rest-of-Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 BMZ Batterien-Montage-Zentrum GmbH

- 6.4.2 BYD Company Ltd.

- 6.4.3 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.4 LG Energy Solution Ltd.

- 6.4.5 NorthVolt AB

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Prime Planet Energy & Solutions Inc.

- 6.4.8 SAIC Volkswagen Power Battery Co. Ltd.

- 6.4.9 Samsung SDI Co. Ltd.

- 6.4.10 SK Innovation Co. Ltd.

- 6.4.11 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.12 TOSHIBA Corp.

- 6.4.13 Vehicle Energy Japan Inc.

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- ELECTRIC VEHICLE SALES, BY BODY TYPE, UNITS, EUROPE, 2017 - 2029

- Figure 2:

- ELECTRIC VEHICLE SALES, BY MAJOR OEMS, UNITS, EUROPE, 2023

- Figure 3:

- ELECTRIC VEHICLE SALES, BY MAJOR OEMS, UNITS, EUROPE, 2023

- Figure 4:

- BEST-SELLING EV MODELS, UNITS, EUROPE, 2023

- Figure 5:

- OEMS MARKET SHARE BY ELECTRIC VEHICLE BATTERY CHEMISTRY, VOLUME %, EUROPE, 2023

- Figure 6:

- ELECTRIC VEHICLE BATTERY CELL AND PACK PRICE, USD, EUROPE, 2017 - 2029

- Figure 7:

- ELECTRIC VEHICLE KEY BATTERY MATERIAL PRICE, BY MATERIAL, USD, EUROPE, 2017 - 2029

- Figure 8:

- ELECTRIC VEHICLE BATTERY PRICE, BY BATTERY CHEMISTRY, USD, EUROPE, 2017 - 2029

- Figure 9:

- EV BATTERY PACK CAPACITY AND EFFICIENCY, KM/KWH, EUROPE, 2023

- Figure 10:

- UPCOMING EV MODELS, BY BODY TYPE, UNITS, EUROPE, 2023

- Figure 11:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, KWH, EUROPE, 2017 - 2029

- Figure 12:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, USD, EUROPE, 2017 - 2029

- Figure 13:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BODY TYPE, KWH, EUROPE, 2017 - 2029

- Figure 14:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BODY TYPE, USD, EUROPE, 2017 - 2029

- Figure 15:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 16:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 17:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BUS, KWH, EUROPE, 2017 - 2029

- Figure 18:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BUS, USD, EUROPE, 2017 - 2029

- Figure 19:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 20:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LCV, KWH, EUROPE, 2017 - 2029

- Figure 21:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LCV, USD, EUROPE, 2017 - 2029

- Figure 22:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 23:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY M&HDT, KWH, EUROPE, 2017 - 2029

- Figure 24:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY M&HDT, USD, EUROPE, 2017 - 2029

- Figure 25:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 26:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PASSENGER CAR, KWH, EUROPE, 2017 - 2029

- Figure 27:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PASSENGER CAR, USD, EUROPE, 2017 - 2029

- Figure 28:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 29:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PROPULSION TYPE, KWH, EUROPE, 2017 - 2029

- Figure 30:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PROPULSION TYPE, USD, EUROPE, 2017 - 2029

- Figure 31:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 32:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, PROPULSION TYPE, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 33:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BEV, KWH, EUROPE, 2017 - 2029

- Figure 34:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BEV, USD, EUROPE, 2017 - 2029

- Figure 35:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 36:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PHEV, KWH, EUROPE, 2017 - 2029

- Figure 37:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PHEV, USD, EUROPE, 2017 - 2029

- Figure 38:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 39:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CAPACITY, KWH, EUROPE, 2017 - 2029

- Figure 40:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CAPACITY, USD, EUROPE, 2017 - 2029

- Figure 41:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, CAPACITY, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 42:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, CAPACITY, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 43:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY 15 KWH TO 40 KWH, KWH, EUROPE, 2017 - 2029

- Figure 44:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY 15 KWH TO 40 KWH, USD, EUROPE, 2017 - 2029

- Figure 45:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 46:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY 40 KWH TO 80 KWH, KWH, EUROPE, 2017 - 2029

- Figure 47:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY 40 KWH TO 80 KWH, USD, EUROPE, 2017 - 2029

- Figure 48:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 49:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ABOVE 80 KWH, KWH, EUROPE, 2017 - 2029

- Figure 50:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ABOVE 80 KWH, USD, EUROPE, 2017 - 2029

- Figure 51:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 52:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LESS THAN 15 KWH, KWH, EUROPE, 2017 - 2029

- Figure 53:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LESS THAN 15 KWH, USD, EUROPE, 2017 - 2029

- Figure 54:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 55:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BATTERY FORM, KWH, EUROPE, 2017 - 2029

- Figure 56:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY BATTERY FORM, USD, EUROPE, 2017 - 2029

- Figure 57:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BATTERY FORM, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 58:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BATTERY FORM, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 59:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CYLINDRICAL, KWH, EUROPE, 2017 - 2029

- Figure 60:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CYLINDRICAL, USD, EUROPE, 2017 - 2029

- Figure 61:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 62:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY POUCH, KWH, EUROPE, 2017 - 2029

- Figure 63:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY POUCH, USD, EUROPE, 2017 - 2029

- Figure 64:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 65:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PRISMATIC, KWH, EUROPE, 2017 - 2029

- Figure 66:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY PRISMATIC, USD, EUROPE, 2017 - 2029

- Figure 67:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 68:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY METHOD, KWH, EUROPE, 2017 - 2029

- Figure 69:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY METHOD, USD, EUROPE, 2017 - 2029

- Figure 70:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, METHOD, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 71:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, METHOD, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 72:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LASER, KWH, EUROPE, 2017 - 2029

- Figure 73:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LASER, USD, EUROPE, 2017 - 2029

- Figure 74:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 75:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY WIRE, KWH, EUROPE, 2017 - 2029

- Figure 76:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY WIRE, USD, EUROPE, 2017 - 2029

- Figure 77:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 78:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COMPONENT, UNITS, EUROPE, 2017 - 2029

- Figure 79:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COMPONENT, USD, EUROPE, 2017 - 2029

- Figure 80:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, COMPONENT, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 81:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, COMPONENT, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 82:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ANODE, UNITS, EUROPE, 2017 - 2029

- Figure 83:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ANODE, USD, EUROPE, 2017 - 2029

- Figure 84:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 85:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CATHODE, UNITS, EUROPE, 2017 - 2029

- Figure 86:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY CATHODE, USD, EUROPE, 2017 - 2029

- Figure 87:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 88:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ELECTROLYTE, UNITS, EUROPE, 2017 - 2029

- Figure 89:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ELECTROLYTE, USD, EUROPE, 2017 - 2029

- Figure 90:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 91:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY SEPARATOR, UNITS, EUROPE, 2017 - 2029

- Figure 92:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY SEPARATOR, USD, EUROPE, 2017 - 2029

- Figure 93:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 94:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY MATERIAL TYPE, KG, EUROPE, 2017 - 2029

- Figure 95:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY MATERIAL TYPE, USD, EUROPE, 2017 - 2029

- Figure 96:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, MATERIAL TYPE, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 97:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, MATERIAL TYPE, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 98:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COBALT, KG, EUROPE, 2017 - 2029

- Figure 99:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COBALT, USD, EUROPE, 2017 - 2029

- Figure 100:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 101:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LITHIUM, KG, EUROPE, 2017 - 2029

- Figure 102:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY LITHIUM, USD, EUROPE, 2017 - 2029

- Figure 103:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 104:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY MANGANESE, KG, EUROPE, 2017 - 2029

- Figure 105:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY MANGANESE, USD, EUROPE, 2017 - 2029

- Figure 106:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 107:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY NATURAL GRAPHITE, KG, EUROPE, 2017 - 2029

- Figure 108:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY NATURAL GRAPHITE, USD, EUROPE, 2017 - 2029

- Figure 109:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 110:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY NICKEL, KG, EUROPE, 2017 - 2029

- Figure 111:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY NICKEL, USD, EUROPE, 2017 - 2029

- Figure 112:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 113:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY OTHER MATERIALS, KG, EUROPE, 2017 - 2029

- Figure 114:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY OTHER MATERIALS, USD, EUROPE, 2017 - 2029

- Figure 115:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 116:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COUNTRY, KWH, EUROPE, 2017 - 2029

- Figure 117:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY COUNTRY, USD, EUROPE, 2017 - 2029

- Figure 118:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, COUNTRY, VOLUME SHARE (%), EUROPE, 2022 & 2029

- Figure 119:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, COUNTRY, VALUE SHARE (%), EUROPE, 2022 & 2029

- Figure 120:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY FRANCE, KWH, EUROPE, 2017 - 2029

- Figure 121:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY FRANCE, USD, EUROPE, 2017 - 2029

- Figure 122:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 123:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY GERMANY, KWH, EUROPE, 2017 - 2029

- Figure 124:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY GERMANY, USD, EUROPE, 2017 - 2029

- Figure 125:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 126:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY HUNGARY, KWH, EUROPE, 2017 - 2029

- Figure 127:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY HUNGARY, USD, EUROPE, 2017 - 2029

- Figure 128:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 129:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ITALY, KWH, EUROPE, 2017 - 2029

- Figure 130:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY ITALY, USD, EUROPE, 2017 - 2029

- Figure 131:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 132:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY POLAND, KWH, EUROPE, 2017 - 2029

- Figure 133:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY POLAND, USD, EUROPE, 2017 - 2029

- Figure 134:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 135:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY SWEDEN, KWH, EUROPE, 2017 - 2029

- Figure 136:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY SWEDEN, USD, EUROPE, 2017 - 2029

- Figure 137:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 138:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY UK, KWH, EUROPE, 2018 - 2029

- Figure 139:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY UK, USD, EUROPE, 2018 - 2029

- Figure 140:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 141:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY REST-OF-EUROPE, KWH, EUROPE, 2017 - 2029

- Figure 142:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BY REST-OF-EUROPE, USD, EUROPE, 2017 - 2029

- Figure 143:

- BREAKDOWN OF EUROPE LFP BATTERY PACK MARKET, BODY TYPE, VALUE SHARE (%), EUROPE, 2017-2029

- Figure 144:

- EUROPE LFP BATTERY PACK MARKET, MOST ACTIVE COMPANIES, BY NUMBER OF STRATEGIC MOVES, 2020 - 2022

- Figure 145:

- EUROPE LFP BATTERY PACK MARKET, MOST ADOPTED STRATEGIES, 2020 - 2022

- Figure 146:

- EUROPE LFP BATTERY PACK MARKET SHARE(%), BY MAJOR PLAYER REVENUE, 2022

Europe LFP Battery Pack Industry Segmentation

Bus, LCV, M&HDT, Passenger Car are covered as segments by Body Type. BEV, PHEV are covered as segments by Propulsion Type. 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh, Less than 15 kWh are covered as segments by Capacity. Cylindrical, Pouch, Prismatic are covered as segments by Battery Form. Laser, Wire are covered as segments by Method. Anode, Cathode, Electrolyte, Separator are covered as segments by Component. Cobalt, Lithium, Manganese, Natural Graphite, Nickel are covered as segments by Material Type. France, Germany, Hungary, Italy, Poland, Sweden, UK, Rest-of-Europe are covered as segments by Country.| Body Type | Bus |

| LCV | |

| M&HDT | |

| Passenger Car | |

| Propulsion Type | BEV |

| PHEV | |

| Capacity | 15 kWh to 40 kWh |

| 40 kWh to 80 kWh | |

| Above 80 kWh | |

| Less than 15 kWh | |

| Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| Method | Laser |

| Wire | |

| Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator | |

| Material Type | Cobalt |

| Lithium | |

| Manganese | |

| Natural Graphite | |

| Nickel | |

| Other Materials | |

| Country | France |

| Germany | |

| Hungary | |

| Italy | |

| Poland | |

| Sweden | |

| UK | |

| Rest-of-Europe |

Need A Different Region or Segment?

Customize Now

Market Definition

- Battery Chemistry - LFP battery type is considred under the scope of battery chemistry.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 4

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF