Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

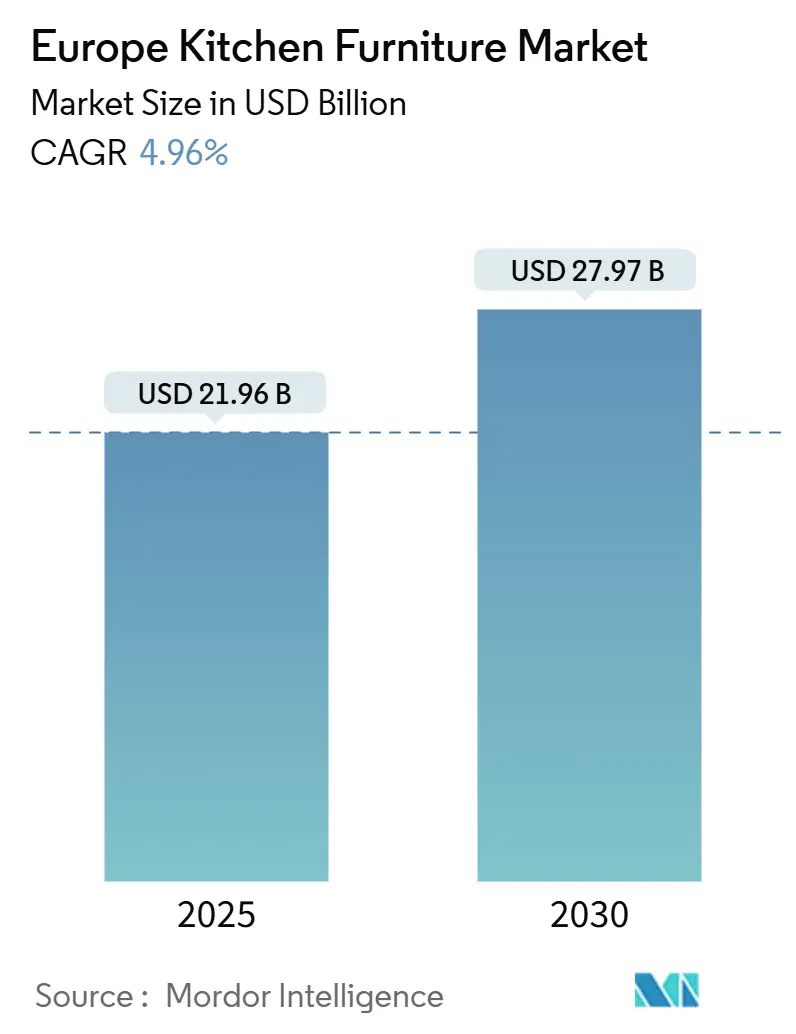

| Market Size (2025) | USD 21.96 Billion |

| Market Size (2030) | USD 27.97 Billion |

| Growth Rate (2025 - 2030) | 4.96% CAGR |

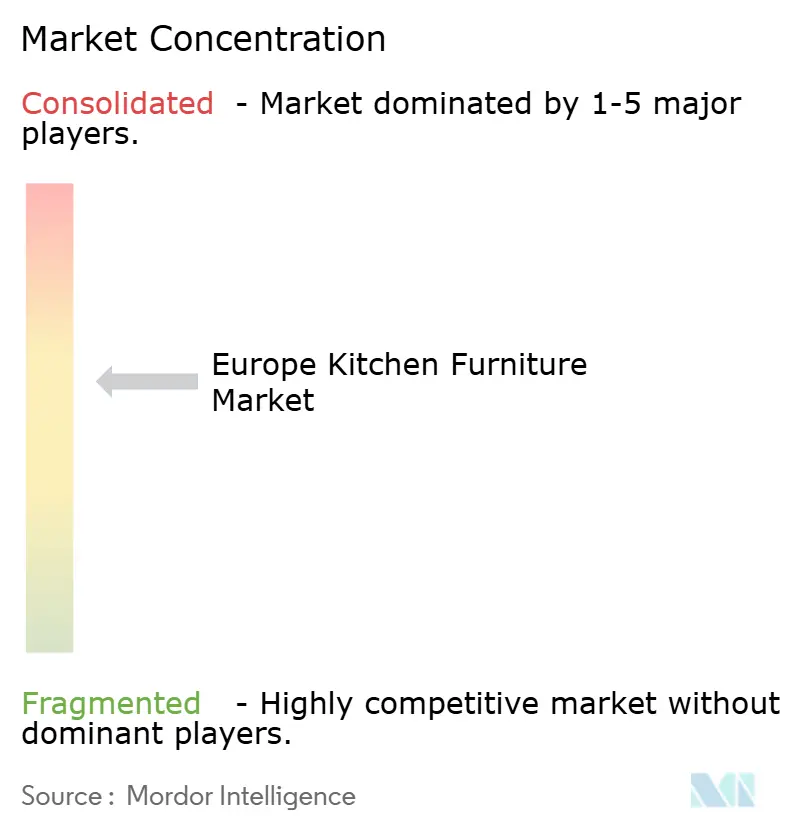

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Kitchen Furniture Market Analysis by Mordor Intelligence

The Europe kitchen furniture market size stands at USD 21.96 billion in 2025 and is forecast to reach USD 27.97 billion by 2030, expanding at a 4.96% CAGR. Modular remodeling, sustainability mandates, and digital buying journeys underpin this steady trajectory even as residential construction weakens across several member states[1]FIEC, “European Union Construction Activity,” fiec.eu. Demand tilts toward space-saving formats that merge cooking, dining, and storage zones; meanwhile, retailers strengthen omnichannel pipes to shorten design-to-delivery times and lift conversion. Manufacturers race to secure certified wood and recyclable metals, buffering regulatory risk while using eco-labels as price-premium levers. Competitive intensity remains moderate: established German, Italian, and Nordic brands wield vertical integration, whereas Asian importers play the low-price card. Long-run opportunities concentrate around smart-kitchen dock integration, circular take-back programs, and project-based commercial renovations that value turnkey performance over unit cost.

Key Report Takeaways

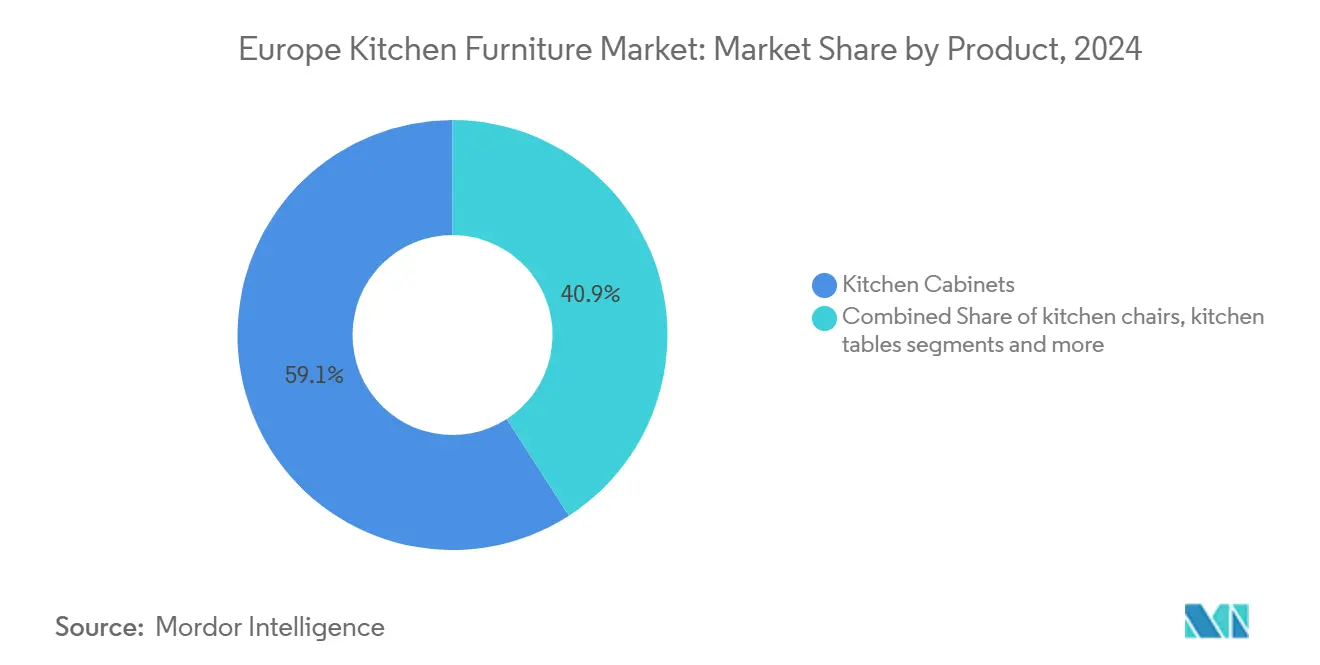

- By product category, kitchen cabinets led with 59.11% of the Europe kitchen furniture market share in 2024; kitchen chairs are advancing at a 5.26% CAGR through 2030.

- By material, wood commanded 66.42% of the Europe kitchen furniture market size in 2024, while metal components recorded the highest projected CAGR at 6.17% between 2025 and 2030.

- By end-user, the residential segment held 73.82% revenue share in 2024; commercial applications are projected to expand at a 6.76% CAGR to 2030.

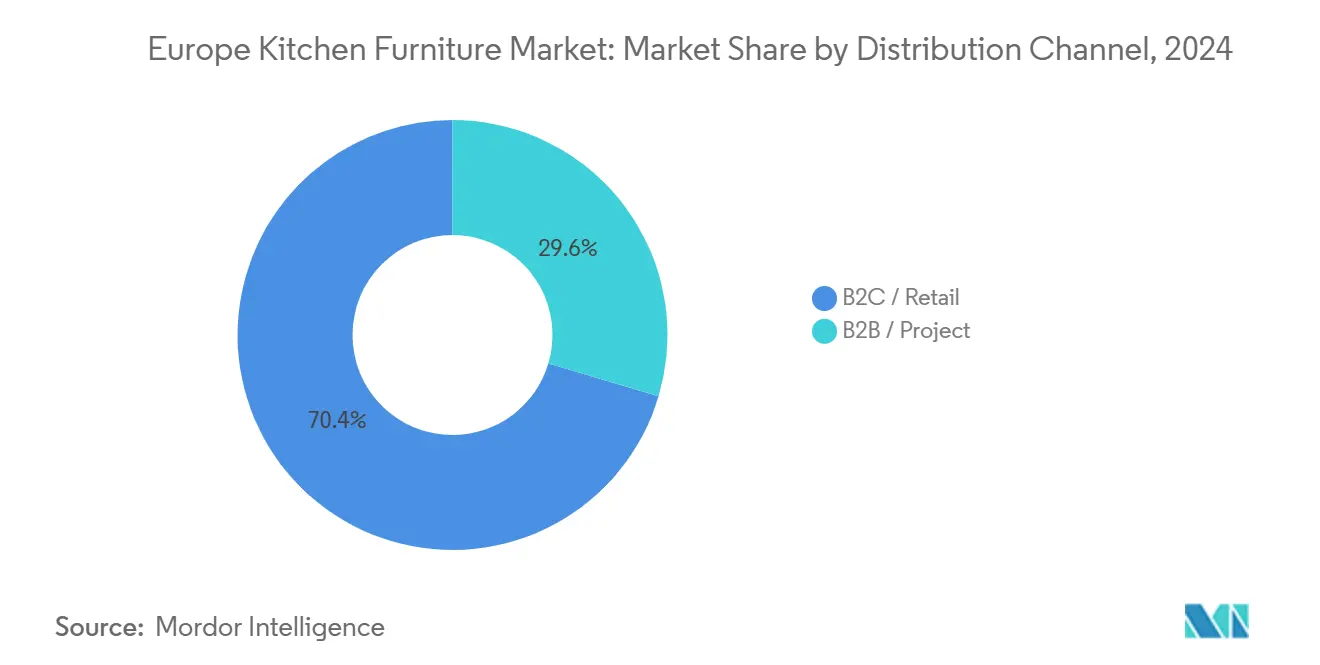

- By distribution channel, B2C retail accounted for 70.41% of the Europe kitchen furniture market size in 2024, whereas B2B project sales show the fastest CAGR of 6.28% through 2030.

- By geography, Germany dominated with a 16.56% share in 2024; France is forecast to achieve the highest CAGR at 5.83% to 2030.

Europe Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modular kitchen demand & remodeling activity | +1.8% | Germany, UK, France | Medium term (2-4 years) |

| Urban, smaller households fuel compact designs | +1.2% | Major EU metros | Long term (≥4 years) |

| E-commerce & omnichannel retail growth | +0.9% | Pan-European, Nordic lead | Short term (≤2 years) |

| Eco-friendly certified wood adoption | +0.7% | Germany, Netherlands, EU-wide | Long term (≥4 years) |

| Circulars refurbish & take-back modules | +0.4% | IKEA's core markets | Medium term (2-4 years) |

| Inventory build-ups before deforestation rules | +0.3% | Import-reliant Eastern Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Modular Kitchens & Remodeling Activity

Renovation now buffers the Europe kitchen furniture market against sluggish new housing. Remodeling captured 30.3% of all construction outlays in 2023, enabling cabinet producers to balance factory loads and stabilize margins. Mid-market brands exploit modularity to mass-customize without high scrap, while kitchen islands evolve into multifunction hubs that hold induction panels, downdraft vents, and charging docks. German suppliers note higher order conversion when installers can finish a 12-unit apartment block in two workdays, highlighting the time-saving halo around factory-finished modules. The practice also expands aftermarket potential because damaged door fronts or drawer boxes can be swapped without dismantling the full layout, creating annuity-style revenue streams.

Urban Smaller Households Driving Compact & Space-Saving Designs

Average EU household size slipped below 2.2 persons in 2024, a demographic twist magnifying the quest for collapsing tables, pocket doors, and pull-out pantries. Milan and Paris apartments under 55 m² often specify full-height monolithic fronts that hide appliances, turning the kitchen into a seamless continuation of the living zone. Hardware innovators such as Hawa report double-digit sales growth for pivot-sliding tracks that let doors disappear into cabinetry walls, freeing critical circulation space [2]Hawa AG, “News from Milan—Space-Saving Hardware Trends,” hawa.com. The space challenge also spurs growth in integrated downdraft ventilation and combination steam ovens, both of which eliminate overhead hoods and separate cooking appliances. Manufacturers that bundle these solutions with compact cabinets capture incremental margin while solving a tangible floor-plan pain point.

Growth of E-Commerce & Omnichannel Retail for Furniture

Online configuration portals compress the path from inspiration to purchase. Augmented-reality tools now visualize cabinet finishes at scale and feed data to factory CAM lines, trimming lead times by almost two weeks for some German export models. Nordic retailers pioneered click-and-collect locker networks that solved the last-mile puzzle for flat-pack furniture, a model cascading into Central Europe. As web traffic rises, retailers integrate finance calculators and installer-booking widgets to secure higher basket values. Brands that share lead-time transparency and delivery slot selection during checkout report lower cart abandonment, helping them offset higher digital advertising costs.

Consumer Shift to Eco-Friendly Certified Wood Under EU Green Deal

PEFC and FSC labels are no longer niche badges; they are baseline specifications for public tenders. Producers shift to traceable spruce, oak, and beech from sustainably managed forests, often securing multi-year supply pacts to lock in availability. French and Dutch consumers ask explicitly for formaldehyde-free MDF, rewarding brands that reformulate glues. The sustainability pull extends beyond raw panels to packaging—flat-pack shipments increasingly rely on recycled-fiber cardboard, and ink usage shifts to water-based formulations. Such end-to-end compliance stories justify 8–10% price premiums in style-conscious markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wood & panel prices | -1.1% | EU manufacturing hubs | Short term (≤2 years) |

| Rising low-cost imports from Asia | -0.8% | Import-dependent states | Medium term (2-4 years) |

| Weak housing starts & discretionary spend | -0.6% | Germany, Sweden, Finland | Medium term (2-4 years) |

| Compliance costs for recyclability rules | -0.3% | EU-wide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Wood & Panel Prices Amid Supply Constraints

Producer price indices in Germany show cumulative 50% jumps for particleboard since late 2020, crimping gross margins and making six-month fixed quotes risky. Smaller Italian studios now schedule quarterly price reviews with dealers to dodge currency and commodity mismatches. Some firms hedge by substituting plywood back panels with honeycomb aluminum, but face learning curves on adhesive selection and screw pull-out strength. Exporters to the United Kingdom also juggle new phytosanitary checks that add port dwell costs, further inflating landed prices. Wider adoption of long-term wood futures contracts is under discussion but limited by liquidity concerns.

Increasing Low-Cost Imports from Asia Intensifying Price Pressure

Chinese exporters accelerated shipments of ready-to-assemble cabinets, exploiting container-rate easing and a 13%-yuan depreciation versus the euro. Preferential tariffs under the EU-Vietnam Free Trade Agreement give Vietnamese solid-wood door producers cost advantages that ripple down mid-tier price ladders. Domestic brands counter by pushing faster deliverables and warranty-bundled installation. Eurostat data show import unit values often undercut German FOB quotations by 25%, compelling local manufacturers to promote design provenance and after-sales networks rather than base price. The ongoing dynamics spur industry consolidation as sub-scale firms struggle to finance automation upgrades.

Segment Analysis

By Product: Cabinets Anchor Market Leadership

In 2024, cabinets accounted for 59.11% of the European kitchen furniture market, primarily due to their high ticket values and frequent replacement cycles. The segment benefits from modular grid systems, which support 'batch-size-1' production. This approach minimizes inventory excess and enables factories to fulfill custom orders within days rather than weeks. Smart-ready cabinets equipped with concealed power rails are sold at double-digit premiums, reflecting their growing demand. Additionally, luxury product lines have introduced biometric drawers, further enhancing the appeal of high-end cabinets. Chairs, although a smaller segment, are experiencing the fastest growth, with a compound annual growth rate (CAGR) of 5.26%. This growth is attributed to the increasing popularity of open-plan layouts, which blur the boundaries between dining and preparation areas.

The persistence of remote work has also influenced market trends. Dining tables are now frequently doubling as workstations, driving steady sales of multifunctional table designs. These tables cater to the evolving needs of consumers who require versatile furniture for both professional and personal use. The shift in consumer preferences highlights the importance of adaptability in kitchen furniture design. Overall, the European kitchen furniture market is witnessing significant innovation and growth. Manufacturers are leveraging advanced production techniques and integrating smart features to meet changing consumer demands. The focus on customization, functionality, and premium offerings is shaping the competitive landscape of the market in 2024.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Wood Dominance Faces Metal Innovation

Wood holds 66.42% of the value attributed to tactile warmth and certified sourcing. Oak, ash, and walnut veneers dominate the market, often finished with water-borne lacquers to comply with VOC regulations. Composite plywood substrates are increasingly favored due to their cost-effectiveness and stability, supporting the transition to recyclable furniture frameworks. These materials align with sustainability goals while maintaining functionality and aesthetic appeal, making them a preferred choice for manufacturers and consumers alike.

Metal components are experiencing robust growth, with a 6.17% CAGR driven by brushed-aluminum frames and stainless-steel worktops, valued for their industrial design and hygienic properties. Manufacturers are diversifying offerings by introducing powder-coated steel legs and anodized trims, which provide color variety without compromising durability. Mixed-material designs, such as walnut fronts framed in aluminum, are gaining traction as they help brands mitigate risks from commodity price fluctuations while expanding style options. This combination of materials allows manufacturers to cater to evolving consumer preferences and maintain a competitive edge in the market.

By End-User: Residential Stability Meets Commercial Growth

In 2024, residential buyers contributed 73.82% of the total turnover, with renovation spending helping to mitigate the impact of weaker housing starts. Homeowners are prioritizing kitchen upgrades, channeling their discretionary budgets into spaces that integrate cooking and socializing. This shift has driven demand for high-function kitchen islands, handle-less cabinetry, and connected appliances that enhance convenience and aesthetics. The trend reflects a growing preference for multifunctional and modern kitchen designs that cater to both utility and lifestyle needs.

Conversely, commercial revenue is growing at a faster rate, with a 6.76% CAGR. Hotels are upgrading back-of-house kitchens to improve operational efficiency and meet stricter food safety standards. At the same time, corporate offices are redesigning pantry areas to create inviting spaces that encourage employees to return to on-site work. Suppliers securing these contracts are leveraging opportunities to offer bundled services, including installation, maintenance, and lifecycle management, which allow them to command premium margins. This approach not only ensures long-term client relationships but also enhances profitability in the competitive commercial segment.

By Distribution Channel: B2C Retail Leads Digital Transformation

In 2024, B2C outlets, including big-box chains and boutique studios, captured 70.41% of the European kitchen furniture market. The adoption of online configurators and AR visualizers has significantly compressed consideration cycles, enabling customers to make quicker decisions. Hybrid showrooms have gained popularity by offering tactile reassurance, allowing customers to physically experience products before completing their purchases. Additionally, the "buy-online-pick-up-in-store" model has seen a sharp rise as consumers aim to reduce delivery wait times and streamline the purchasing process. These trends highlight the evolving preferences of B2C customers, who increasingly value convenience, speed, and a blend of digital and physical shopping experiences.

B2B project channels are growing at a 6.28% CAGR, fueled by developers specifying turnkey kitchens for build-to-rent and senior-living complexes. Manufacturers are responding to this demand by integrating BIM-ready catalogues, which enable architects to easily incorporate cabinets into digital floor plans. This innovation not only shortens specification timelines but also helps manufacturers secure brand preference early in the project lifecycle. The B2B segment's growth reflects the increasing importance of efficiency and customization in large-scale projects, as developers and architects seek solutions that simplify workflows while meeting specific design requirements. Together, these factors are driving significant changes in the European kitchen furniture market, with both B2C and B2B channels adapting to meet evolving customer needs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany anchors the Europe kitchen furniture market with 16.56% value share in 2024, sustained by manufacturing clusters in North Rhine-Westphalia and export-friendly logistics corridors. Domestic giants reinvest in robotic drilling and edge banding lines to counter wage inflation, yet consumer sales slid 3.6% to EUR 22.6 billion during 2024 amid construction softness. Renovation grants and energy-efficiency subsidies partly offset the slump; plus, sustainability leadership and smart-integration credentials position German producers for long-term gain. France is the fastest-growing market, booking a 5.83% CAGR through 2030 as urban densification and eco-renovation credits fuel compact, design-centric kitchen makeovers. Parisian apartments favor matte lacquered fronts and fluted-glass cabinets, pushing average selling prices upward. Retailers employ appointment-only consults and AI-driven configurators to elevate the buying experience and convert style-savvy consumers.

The United Kingdom faces macro headwinds but shows resilience in trade-focused channels. Howdens scales depot networks and offers rapid fulfillment to installers, offsetting flagging DIY demand. Currency swings elevate costs of mostly imported wooden components—the UK brought in USD 87.1 million of wooden kitchenware in 2023, 68% from China[3]World Bank, “United Kingdom Wooden Kitchenware Imports 2023,” wits.worldbank.org. Domestic producers tout “made in Britain” lines to reduce import risk.

Italy leverages its design heritage, marrying artisanal veneers with industrial robotics to serve premium buyers. Spain benefits from 2.1% construction growth in 2023, especially in tourist regions, investing in rental-property refurbishments. BENELUX markets emphasize cradle-to-grave certifications, while Nordic consumers lead in circular take-back schemes, pulling forward demand for easily disassembled modules.

Competitive Landscape

Market concentration is moderate: the top five players hold the majority of sales, granting them negotiating clout but leaving whitespace for regional specialists. German heavyweights Nobilia, Häcker, and Nolte operate vertically integrated plants covering chipboard production to last-mile delivery, reinforcing cost leadership. Scandinavian group Nobia relies on AI-based configurators to streamline consultative selling and shrink design-approval cycles. IKEA’s circular buy-back programs set up new sustainability bars, forcing rivals to draft similar initiatives.

Tech adoption defines winners. Schmidt Groupe embeds AI into sales scripts, lifting conversion rates, while Scavolini rolls out IoT-enabled drawers that flag maintenance alerts—features resonating with multi-family property managers. XXXLutz’s 2025 purchase of 140 Central European stores widens its retail grid, enabling private-label penetration and scale purchasing of certified wood. Private-equity funds target fragmented cabinet makers, bundling them into pan-EU supply platforms that promise procurement synergies and shared digital tools.

Europe Kitchen Furniture Industry Leaders

-

Nobilia

-

Howdens Joinery Group

-

Schmidt Groupe

-

Häcker Küchen

-

Nobia AB

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Ultima Kitchens surpassed GBP 100 million in sales after upgrading its Leeds plant with automated nesting routers and launching a “48-hour door swap” service that underpins its premium quick-refresh offering. Management indicated plans to double export revenue to Ireland by 2027.

- April 2025: XXXLutz acquired 140 stores across Germany, the Czech Republic, and Slovakia, adding more than 400,000 m² of selling space. The rollout brings its private-label kitchen lines closer to Central European consumers and enhances bargaining leverage with raw-material suppliers.

- February 2025: Nobia closed a sale-leaseback on its Tidaholm factory, freeing SEK 750 million for digital showroom investments. The company will continue production in the facility under a 15-year lease, demonstrating faith in Swedish manufacturing while optimizing its balance sheet.

- January 2025: Porta Group purchased Möbel Letz GmbH, inheriting an online catalogue of 30,000 SKUs. Integration includes migrating Letz’s logistics algorithms into Porta’s ERP, expected to shave last-mile costs by 8% within one year.

Europe Kitchen Furniture Market Report Scope

Europe Kitchen Furniture is one of the most widely demanded Kitchen Furniture as people are more preferring urban and modern kitchen furniture. European countries like Italy, France, Spain, and Sweden are profoundly known for their well-designed, luxurious, and newly innovative furniture. A complete background analysis of the European Kitchen Furniture Market, which includes the market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report.

The European kitchen Furniture Market is Segmented by Product Type (Kitchen Cabinets, Kitchen Chairs, Kitchen Tables, and Other Product Types), by Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online, and Other Distribution Channels), by End User (Residential, and Commercial), and by Geography (Italy, Germany, France, Poland, United Kingdom and Rest of Europe). The report offers market size and forecasts for the Europe Kitchen Furniture Market in value (USD) for all the above segments.

By Product

| Kitchen Cabinets |

| Kitchen Chairs |

| Kitchen Tables |

| Other Products (trolley, cart, pantry shelves) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product | Kitchen Cabinets | |

| Kitchen Chairs | ||

| Kitchen Tables | ||

| Other Products (trolley, cart, pantry shelves) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the European kitchen furniture market in 2025?

It stands at USD 21.96 billion and is projected to reach USD 27.97 billion by 2030 at a 4.96% CAGR.

Which product category holds the top revenue share?

Cabinets lead with 59.11% of the Europe kitchen furniture market share in 2024, reflecting high ticket values and frequent replacements.

What drives the fastest growth in materials?

Metal components, especially brushed aluminum and stainless steel, post the highest CAGR at 6.17% due to durability and industrial aesthetics.

Why is France the fastest-growing geography?

Urban densification, eco-renovation credits, and strong design preferences push France toward a 5.83% CAGR through 2030.

How are EU sustainability rules shaping the industry?

They accelerate the adoption of certified wood, recyclability-ready connectors, and circular take-back programs, adding cost but creating differentiation opportunities.

What is the outlook for commercial kitchen projects?

Commercial applications, particularly hospitality and workplace refurbishments, are set to grow at a 6.76% CAGR as businesses prioritize experiential dining spaces.

Page last updated on: