Market Size of Europe Intravenous Solutions Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

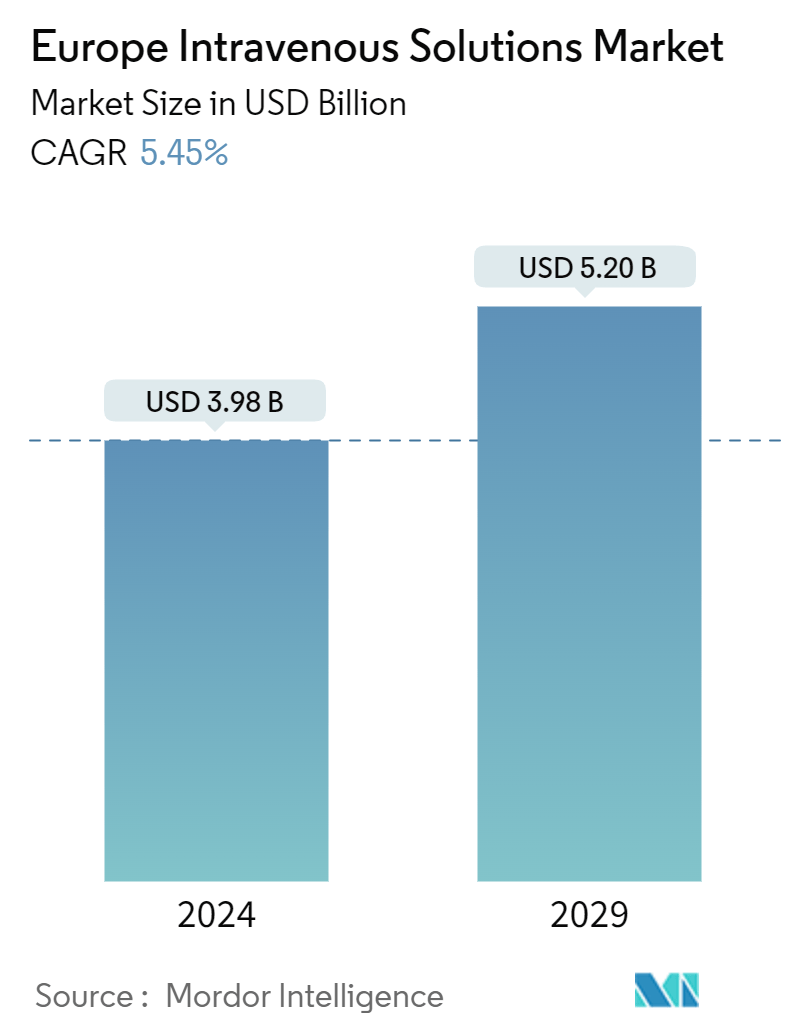

| Market Size (2024) | USD 3.98 Billion |

| Market Size (2029) | USD 5.20 Billion |

| CAGR (2024 - 2029) | 5.45 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe Intravenous Solutions Market Analysis

The Europe Intravenous Solutions Market size is estimated at USD 3.98 billion in 2024, and is expected to reach USD 5.20 billion by 2029, growing at a CAGR of 5.45% during the forecast period (2024-2029).

Factors such as the increasing prevalence of chronic diseases, such as gastrointestinal disorders, neurological diseases, and cancer, as well as advancements and innovations in products for patient convenience, are expected to drive market growth during the forecast period. For instance, according to the data updated by the Spanish Network of Cancer Registries (REDECAN) in January 2023, approximately 279,260 new cases of cancer occurred in Spain by the end of 2023, out of which 42,721 were new cases of colorectal cancer, 31,282 were cases of lung cancer, and 21,694 were cases of urinary bladder cancer. Therefore, the high incidence of cancer is predicted to increase the demand for intravenous solutions and is expected to further contribute to the market’s growth.

Additionally, the profound impact on the quality of life of patients afflicted with neurological disorders, alongside the escalating societal burden attributed to the aging demographic of the Western population. For instance, according to data published by University College London in October 2023, by 2040, England and Wales are projected to experience a significant increase in the prevalence of dementia, with 1.7 million individuals affected in England alone, exceeding previous estimates. NHS data released in November 2023 revealed a surge in dementia diagnoses, with 475,573 people identified in September 2023, representing a rise of over 52,000 from the previous year. This surge marked the highest dementia diagnosis rate in the past three years, highlighting an alarming trend. Thus, the increasing number of brain disorders is increasing the demand for intravenous solutions in the United Kindom, thereby contributing to the growth of the market studied.

Moreover, various initiatives taken by key players, such as product launches, investments, and partnerships to increase the footprint, are expected to boost the market's growth during the forecast period. For instance, in July 2023, Recce Pharmaceuticals Ltd reported positive results from a Phase I (R327-001) study of RECCE 327 (R327) as an intravenous (IV) infusion formulation in 80 healthy male subjects in Austria. When administered at doses much higher than the expected therapeutic window, R327 IV does not lead to safety or toxicity issues in healthy subjects.

Thus, the abovementioned factors, such as the high burden of chronic diseases and strategic initiatives, are expected to drive the market's growth during the forecast period. However, regulatory and quality requirements are expected to restrain the market's growth.

Europe Intravenous Solutions Industry Segmentation

As per the scope of the report, intravenous solutions are chemically prepared fluids administered in the body through the venous circulation to maintain or replace the level of lost body fluid. The European intravenous solutions market is segmented by type, solution composition, and geography. By type, the market is segmented into total parenteral nutrition and peripheral parenteral nutrition. By solution composition, the market is segmented into saline, carbohydrates, vitamins and minerals, and other solution compositions. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and Rest of Europe. The report offers the value (USD) for the above segments.

| By Type | |

| Total Parenteral Nutrition | |

| Peripheral Parenteral Nutrition |

| By Solution Composition | |

| Saline | |

| Carbohydrates | |

| Vitamins and Minerals | |

| Other Solution Compositions |

| By Geography | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Europe Intravenous Solutions Market Size Summary

The European intravenous solutions market is poised for significant growth, driven by the increasing prevalence of chronic diseases such as cancer, gastrointestinal disorders, and neurological conditions. The demand for intravenous solutions is further bolstered by advancements in product innovations aimed at enhancing patient convenience. The aging population in Western Europe, particularly in countries like the United Kingdom and Germany, is contributing to the rising incidence of conditions such as dementia, which in turn is fueling the need for intravenous solutions. Strategic initiatives by key market players, including product launches and partnerships, are expected to enhance market penetration and drive growth during the forecast period.

The total parenteral nutrition (TPN) segment is experiencing growth due to the rising number of patients with chronic illnesses who are unable to consume food normally. This segment's expansion is supported by collaborations and strategic agreements among major players to broaden their product offerings and reach. Germany is anticipated to be a significant contributor to market growth, driven by its increasing geriatric population and the high burden of chronic diseases. The competitive landscape of the European intravenous solutions market is characterized by the presence of major players who are focusing on manufacturing expansion and innovation to maintain their market position.

Europe Intravenous Solutions Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Prevalence of Diseases, such as Gastrointestinal Disorder, Neurological Diseases, and Cancer

-

1.2.2 Advancements and New Innovations in the Products for Patient Convenience

-

-

1.3 Market Restraints

-

1.3.1 Regulatory and Quality Requirements

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Type

-

2.1.1 Total Parenteral Nutrition

-

2.1.2 Peripheral Parenteral Nutrition

-

-

2.2 By Solution Composition

-

2.2.1 Saline

-

2.2.2 Carbohydrates

-

2.2.3 Vitamins and Minerals

-

2.2.4 Other Solution Compositions

-

-

2.3 By Geography

-

2.3.1 Germany

-

2.3.2 United Kingdom

-

2.3.3 France

-

2.3.4 Italy

-

2.3.5 Spain

-

2.3.6 Rest of Europe

-

-

Europe Intravenous Solutions Market Size FAQs

How big is the Europe Intravenous Solutions Market?

The Europe Intravenous Solutions Market size is expected to reach USD 3.98 billion in 2024 and grow at a CAGR of 5.45% to reach USD 5.20 billion by 2029.

What is the current Europe Intravenous Solutions Market size?

In 2024, the Europe Intravenous Solutions Market size is expected to reach USD 3.98 billion.