Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

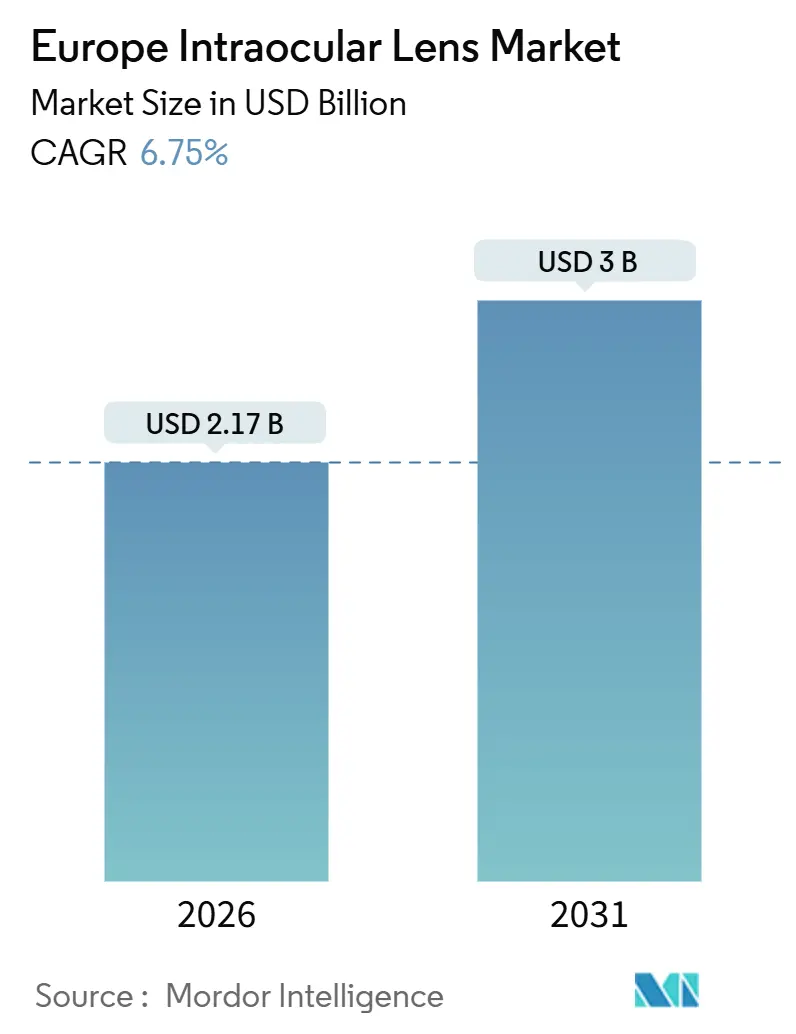

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 3 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

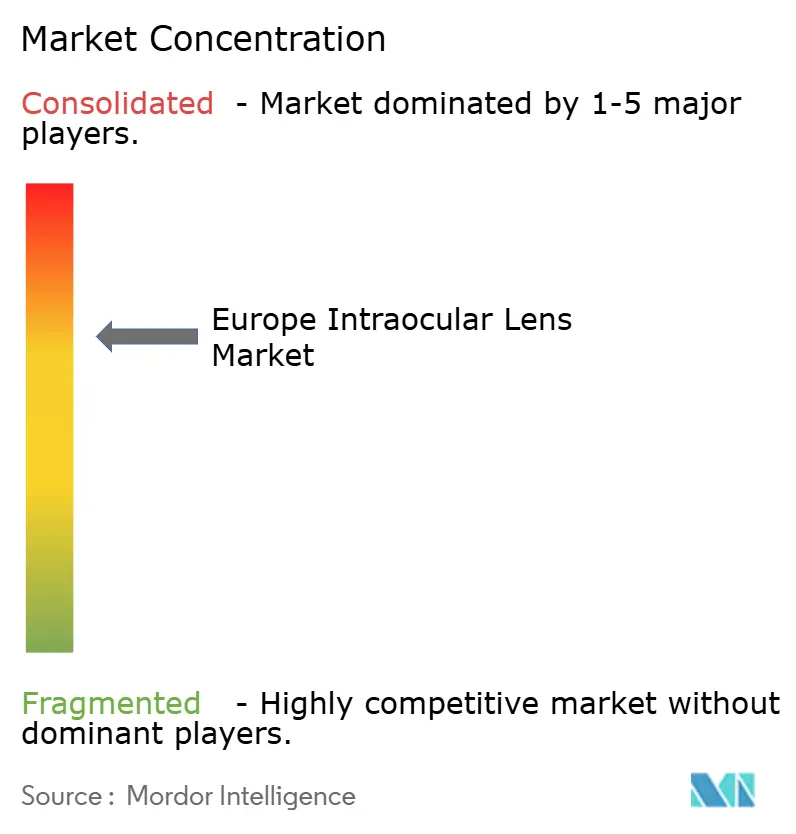

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Intraocular Lens Market Analysis by Mordor Intelligence

The Europe Intraocular Lens Market size is estimated at USD 2.17 billion in 2026, and is expected to reach USD 3 billion by 2031, at a CAGR of 6.75% during the forecast period (2026-2031).

The aging population continues to drive structural growth; however, demand is increasingly shifting toward premium toric, multifocal, and extended-depth-of-focus designs. These products command higher average selling prices and deliver more substantial profit margins. While hospitals remain the primary setting for implants, ambulatory clinics are rapidly expanding as governments adopt day-case cataract pathways, reducing procedure costs by up to 40%. In Europe, Germany leads in revenue generation, Spain records the fastest growth, and France achieves the highest per-capita procedure rate. The competitive landscape remains highly concentrated, with Alcon, Johnson & Johnson Vision, and Bausch + Lomb collectively controlling approximately two-thirds of the market volume. Despite this, regional specialists are thriving by focusing on delivery-system innovations and niche optical designs.

Key Report Takeaways

- By product, monofocal lenses commanded 58.65% of the Europe intraocular lens market share in 2025, while toric variants are advancing at an 8.53% CAGR through 2031.

- By indication, age-related cataract accounted for 56.54% of the Europe intraocular lens market size in 2025; refractive lens exchange is projected to expand at an 8.76% CAGR over the same period.

- By end user, hospitals held 61.45% revenue share in 2025, whereas ambulatory clinics are forecast to post a 9.12% CAGR to 2031.

- By geography, Germany captured 26.54% regional revenue in 2025; Spain is set to log a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Intraocular Lens Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising cataract burden | +1.8% | Pan-European | Long term (≥ 4 years) |

| Growing adoption of premium multifocal and toric IOLs | +1.5% | Core Western Europe | Medium term (2-4 years) |

| Technological advances in aspheric and blue-light filtering materials | +1.0% | Germany, Switzerland, Nordics | Medium term (2-4 years) |

| Surge in refractive lens exchange among high-myopia patients | +1.2% | Urban Germany, Spain, UK | Short term (≤ 2 years) |

| Expansion of day-case cataract surgery | +0.9% | France, Spain, Netherlands | Medium term (2-4 years) |

| Uptake of AI-driven biometry | +0.7% | Germany, UK, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Premium Multifocal and Toric IOLs

Toric volumes outpace the overall Europe intraocular lens market by nearly two percentage points, and multifocal uptake accelerates as optics improve and patient expectations climb. A premium lens costs EUR 1,500-3,000 per eye, compared to EUR 300-500 for a monofocal lens; yet, the unit manufacturing cost rises only modestly, lifting gross margins beyond 70%. Germany’s supplemental insurance and Spain’s price-competitive medical tourism hubs create early-adopter pockets, while Johnson & Johnson’s TECNIS Odyssey, launched in 2025, aims to mitigate halo and glare complaints that once limited multifocal lens penetration. Reimbursement ceilings remain the binding gatekeeper, restricting adoption largely to affluent urban cohorts.

Technological Advances in Aspheric and Blue-Light Filtering Materials

Aspheric optics flatten lens curvature to reduce spherical aberration, thereby sharpening contrast sensitivity for night driving. Meanwhile, embedded chromophores absorb sub-450 nm wavelengths that could potentially harm the retina. Alcon’s Clareon platform, CE-marked in 2025, combines UV-blocking monomers with a hydrophobic surface that resists posterior capsule opacification. This complication otherwise affects up to 30% of patients within five years. Carl Zeiss Meditec’s CT ASPHINA 409M reports a gleaming incidence of less than 1% at two years. The EU Medical Device Regulation heightens post-market evidence requirements, favoring incumbents that maintain robust quality management systems.

Surge in Refractive Lens Exchange Among High-Myopia Patients

Refractive lens exchange (RLE) is growing at an annual rate of 8.76% and now attracts presbyopic professionals in their 40s and 50s who want spectacle independence sooner than the onset of cataracts. Spain’s private clinics bundle premium IOL implantation, biometry, and follow-up for EUR 3,000-5,000 per eye, undercutting Northern Europe by up to 30% and attracting cross-border patients. Bausch + Lomb’s LuxLife toric lens, CE-marked in 2025, targets explicitly high-astigmatism RLE cases with a preloaded injector that enhances rotational stability. Public insurers still deem RLE cosmetic, placing the segment firmly in the self-pay arena.

Aging Population and Rising Cataract Burden

The share of Europeans aged 65 and above climbed to 21.6% in 2024 and is projected to reach 29% by 2050, marking a demographic shift that mechanically expands the pool of cataract candidates. EU member states performed 4.73 million cataract surgeries in 2022, rebounding from pandemic-related backlogs and shortening waitlists. France already executes 1,493 procedures per 100,000 population, while Romania remains below 500, revealing a capacity gap that device makers can target through distribution partnerships in underserved regions. Untreated cataracts account for 51% of global blindness, so basic monofocal reimbursement persists even within fiscally constrained health systems, according to the. Still, surgical throughput could plateau if rural workforce shortages are not addressed, capping revenue translation of latent demand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium intraocular lenses | -1.3% | Germany, UK, France | Medium term (2-4 years) |

| Reimbursement limitations | -1.1% | Pan-European | Long term (≥ 4 years) |

| Supply-chain fragility | -0.6% | UK, Eastern Europe | Short term (≤ 2 years) |

| Limited surgical capacity in rural regions | -0.8% | Romania, Bulgaria, Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Intraocular Lenses

Out-of-pocket charges range from EUR 1,500-3,000 in Germany to GBP 2,000-3,500 in the United Kingdom, effectively excluding lower-income cohorts from premium options[1]German Ophthalmological Society, “Cataract Surgery Pricing Study,” dog.org. VAT disparities—0% in the UK versus 23% in Portugal—further skew access and invite gray-market arbitrage. Manufacturers face a balancing act: they can either widen access by lowering prices or protect R&D funding and margins; neither route resolves the equity gap in the near term.

Reimbursement Limitations for Advanced Technology IOLs

French, German, and UK payers reimburse only basic monofocals, labeling toric and multifocal lenses discretionary upgrades. Patients must sign private-pay agreements, a friction that limits premium uptake to roughly 10-25% of total implants even in affluent markets[2]NHS England, “Clinical Commissioning Policy for Cataract Surgery,” nhs.uk. Health-technology assessment agencies demand real-world effectiveness data that remains scarce, perpetuating a circular stalemate between evidence and adoption.

Segment Analysis

By Product: Toric Lenses Capture the Refractive-Correction Wave

Toric lenses are expanding 8.53% a year, pulling Europe intraocular lens market revenue ahead of the broader average as surgeons increasingly prefer to eliminate pre-existing astigmatism in a single event. In contrast, monofocal implants still represent 58.65% of the Europe intraocular lens market share because public insurance covers only basic spherical models. Multifocals and extended-depth-of-focus platforms now chip away at monofocal dominance as designs like Alcon’s Clareon Vivity and Johnson & Johnson’s TECNIS Odyssey gain traction. Manufacturers exploit favorable economics: a toric SKU costs roughly five times a monofocal at retail yet carries only a fractional increase in production cost, sustaining premium gross margins. Post-market evidence showing stable rotational alignment within ±5° at one year further reassures surgeons who once feared axis drift. The EU MDR's post-market surveillance adds compliance overhead, but dominant suppliers leverage their established quality systems to stay ahead of emerging low-cost entrants.

Second-generation diffractive optics resolve earlier halo and glare complaints, improving satisfaction rates and widening the candidate pool to exacting younger RLE patients. Rotationally stable injector systems, such as Bausch + Lomb’s enVista Aspire, reduce operating time and minimize the risk of endophthalmitis, two essential differentiators for high-throughput ambulatory centers. As clinical outcomes converge, marketing shifts toward lifestyle messaging—such as night-driving clarity and digital-screen comfort—and bundled service contracts that lock ambulatory clinics into multi-year purchase agreements. Nonetheless, premium adoption remains gated by the self-pay model, meaning toric acceleration keeps contingent on income demographics and private insurance uptake.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Indication: Refractive Lens Exchange Redefines Patient Demographics

Age-related cataract still accounts for 56.54% of procedures, yet refractive lens exchange is the fastest-growing segment, increasing 8.76% annually and driving average selling prices upward. Spain exemplifies the trend: RLE packages priced EUR 3,000-5,000 per eye lure Northern Europeans seeking lower costs and warmer climates. RLE patients skew younger, exhibit a higher willingness to self-fund, and present with lower comorbidity profiles, allowing clinics to streamline perioperative pathways and schedule bilateral same-day procedures, thereby doubling operating-room productivity. The Europe intraocular lens market size attached to RLE is projected to compound faster than cataract volumes, ultimately reshaping surgeon case-mix economics.

Stringent refractive accuracy demands—mean absolute error below 0.50 diopters—are driving rapid uptake of AI-enhanced biometry tools as standard of care in urban centers. High myopia RLE carries a modestly elevated risk of retinal detachment, yet clearer counseling tools and improved capsular bag management techniques are reducing complication perception. Regulatory positioning remains complex: insurers classify RLE as elective, but lobbying efforts citing lifetime spectacle independence savings are mounting, especially as the workforce ages and near-vision tasks proliferate in digital economies.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Ambulatory Clinics Scale on Cost Efficiency

Hospitals accounted for 61.45% of Europe intraocular lens market revenue in 2025, though ambulatory surgery centers are projected to record a brisk 9.12% CAGR as health ministries push cost-per-case optimization. Day-case models shave EUR 300-500 from each German cataract procedure and free inpatient beds for higher-acuity cases. Ambulatory setups feature shorter turnover times and often bundle premium IOL upgrades with ancillary services, such as femtosecond laser capsulotomy, which lifts average revenue per case 15-25% above hospital levels. EU structural funds earmarked for outpatient infrastructure in Poland, Romania, and Bulgaria promise fresh greenfield opportunities for distributors able to supply turnkey ophthalmic suites.

Nevertheless, public-hospital networks maintain a grip on complex cases requiring extended postoperative monitoring or general anesthesia, domains where economies of scale and critical-care backup remain indispensable. Academic medical centers also preserve influence by piloting novel optics and surgical robotics that later disseminate into community settings. As ambulatories proliferate, leading IOL suppliers secure loyalty through service-based contracts that include biometer leasing, staff training, and guaranteed consumable deliveries, embedding switching costs and safeguarding share.

Geography Analysis

Germany generated 26.54% of Europe intraocular lens market revenue in 2025, underpinned by roughly 800,000 annual surgeries and a 10% population segment holding supplemental insurance that reimburses premium lenses. The ecosystem benefits from high diagnostic uptake, with more than 1,200 practices running optical biometers, and femtosecond laser penetration reaching over 15%. Reimbursement, however, caps basic lens payments, so surgeons rely on patient top-ups for toric or multifocal upgrades. Logistics remain efficient despite Brexit-induced compliance duality because Germany functions as a continental distribution hub for many global manufacturers.

Spain is the fastest-growing market, clocking a 7.54% CAGR to 2031. Private-clinic build-out, competitive package pricing, and a growing medical-tourism reputation draw patients from France, the UK, and Scandinavia. Domestic demand also rises as younger cohorts view RLE as a lifestyle investment analogous to orthodontic work.

France logs Europe’s highest per-capita surgery rate thanks to universal coverage for monofocal implants and a mature outpatient infrastructure that handles more than 80% of cases. Premium uptake remains muted because Social Security covers only basic optics, yet supplemental insurance adoption is inching upward, hinting at latent potential for toric and EDOF conversion.

The United Kingdom faces constrained National Health Service budgets and friction from dual CE-Mark/UKCA certification post-Brexit, both of which are slowing premium adoption and complicating supply chains. Eastern European member states still post sub-500 procedures per 100,000 population but receive EU cohesion funds for ambulatory build-outs; success will hinge on workforce retention and tariff-free supply corridors.

Competitive Landscape

Alcon, Johnson & Johnson Vision, and Bausch + Lomb collectively controlled 60-65% of Europe intraocular lens market volume in 2025. Alcon’s USD 300 million Singapore plant expansion boosts Clareon output and hedges geographic risk[3]Alcon, “Singapore Manufacturing Expansion Press Release,” alcon.com. Johnson & Johnson’s TECNIS Odyssey focuses on dysphotopsia-free, continuous-vision optics, positioning the firm for share gains in the RLE sub-segment. Bausch + Lomb counters with enVista Aspire and LuxLife, emphasizing materials that are glistening-free and preloaded injectors that reduce operating time.

Regional challengers differentiate through specialization. Rayner’s RayOne preloaded system wins traction in high-volume ambulatory centers seeking workflow simplification. Carl Zeiss Meditec leverages its dominance in diagnostic equipment to cross-sell CT ASPHINA lenses, while HumanOptics courts boutique practices with accommodative designs and surgeon education programs.

Strategic partnerships between device and software players tighten ecosystems: Carl Zeiss Meditec now integrates Microsoft Azure AI into its IOLMaster 700 platform. At the same time, Alcon’s digital-planning suite embeds its own cloud calculator. EU MDR compliance costs and AI transparency rules under the EU AI Act raise entry barriers, favoring entrenched firms that can amortize regulatory overhead across global revenues.

Europe Intraocular Lens Industry Leaders

Bausch Health Companies Inc. (Bausch + Lomb)

Carl Zeiss Meditec AG

EyeKon Medical Inc.

Alcon

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Johnson & Johnson Vision introduced the TECNIS Odyssey IOL across Europe, touting continuous-range-of-vision optics without halo or glare trade-offs

- May 2025: Bausch + Lomb received CE-Mark for LuxLife toric IOL featuring a preloaded injector that improves rotational stability in high-astigmatism cases

- April 2025: Alcon unveiled PanOptix Pro in the United States and announced European rollout for late 2025, extending its trifocal portfolio

- March 2025: Clareon Vivity won CE-Mark clearance, expanding Alcon’s extended-depth-of-focus family with UV-absorbing hydrophobic acrylic

- January 2025: Bausch + Lomb launched enVista Aspire, a glistening-free toric platform targeting ambulatory clinics

- November 2024: Ophtec obtained CE-Mark for Artisan Toric phakic IOL, expanding options for high-myopia patients unsuitable for corneal laser surgery

- August 2024: LENSAR secured EU MDR certification for its ALLY adaptive cataract laser integrating real-time OCT and AI-driven planning

Europe Intraocular Lens Market Report Scope

According to the report's scope, intraocular lenses are implanted in the eyes of individuals with cataracts or myopia who undergo surgery for these conditions. Several types of intraocular lenses are available on the market, primarily designed to improve vision.

The Europe Intraocular Lens Market is Segmented by Product (Monofocal, Accommodative, Multifocal, and Toric), Indication (Age-Related Cataract, Congenital/Traumatic Cataract, and Refractive Lens Exchange), End User (Hospitals, Ambulatory Clinics, and Other End Users), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The report offers the value (in USD million) for the above segments.

By Product

| Monofocal Intraocular Lens |

| Accommodative Intraocular Lens |

| Multifocal Intraocular Lens |

| Toric Intraocular Lens |

By Indication

| Age-Related Cataract |

| Congenital/Traumatic Cataract |

| Refractive Lens Exchange (RLE) |

By End User

| Hospitals |

| Ambulatory Clinics |

| Other End Users |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest Of Europe |

| By Product | Monofocal Intraocular Lens |

| Accommodative Intraocular Lens | |

| Multifocal Intraocular Lens | |

| Toric Intraocular Lens | |

| By Indication | Age-Related Cataract |

| Congenital/Traumatic Cataract | |

| Refractive Lens Exchange (RLE) | |

| By End User | Hospitals |

| Ambulatory Clinics | |

| Other End Users | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe intraocular lens market in 2026?

It reached USD 2.17 billion in 2026 and is projected to rise to USD 3.00 billion by 2031.

What is driving the fastest growth within product segments?

Toric lenses lead the acceleration with an 8.53% CAGR because they correct astigmatism during cataract surgery.

Which procedure type is expanding quickest in Europe?

Refractive lens exchange is growing 8.76% a year as younger, self-pay patients seek premium spectacle-independent vision.

Why are ambulatory clinics gaining implant share?

Day-case pathways cut payer costs by up to 40% and boost premium-lens attachment rates by 15-25%.

What role does AI play in lens-power calculation?

AI-driven biometry platforms reduce mean absolute error to below 0.30 diopters, broadening candidacy for premium optics.

Which country is currently the fastest-growing IOL market in Europe?

Spain is leading with a 7.54% CAGR, fueled by medical tourism and private-clinic expansion.