Market Trends of Europe Insurance Telematics Industry

Adoption of Usage-based Insurance by Insurance Companies will Drive The Market

- Usage-based insurance (or UBI) uses a unique tracking device (usually placed within a client's vehicle) to track driving behavior. By examining how a driver accelerates, brakes, and corners, the idea is that an insurance company can determine a more appropriate premium for that client. Insurance companies who have adopted these programs also examine when clients drive and how much time they spend behind the wheel.

- In the coming years, the expansion of the vehicle industry is likely to move the usage-based insurance market forward. The automotive industry comprises many firms and organizations involved in automobile design, production, marketing, and sale. Telematics-driven usage-based insurance appeals to car owners since it offers low premiums for low-risk driving and high premiums for high-risk driving. As a result, individuals can significantly reduce their insurance prices by changing their driving behaviors.

- Light-duty vehicles (LDV) and heavy-duty vehicles (HDV) are the two most common vehicle classes for usage-based insurance (UBI). Passenger automobiles with a maximum gross vehicle weight of fewer than 8500 lbs are classified as light-duty vehicles, whereas heavy-duty vehicles have a higher gross vehicle weight. OBD-II-based UBI programs, smartphone-based UBI programs, hybrid-based UBI programs, and black-box-based UBI programs are among the several technologies that are utilized in various sorts of packages such as pay-as-you-drive (PAYD), pay-how-you-drive (PHYD), and manage-how-you-drive (MWYD).

- One point of contention is privacy. It's one thing for private individuals to choose usage-based insurance, but it's quite another for business fleets to demand that their drivers be regularly watched. However, with telematics, the usual norm is that measurable benefits eventually surpass privacy concerns, primarily handled by anonymizing data collection and processing. In reality, tracking and reporting on driving behavior might be a positive experience for drivers, allowing them to improve their performance against various benchmarks, thereby gamifying the practice of safe driving.

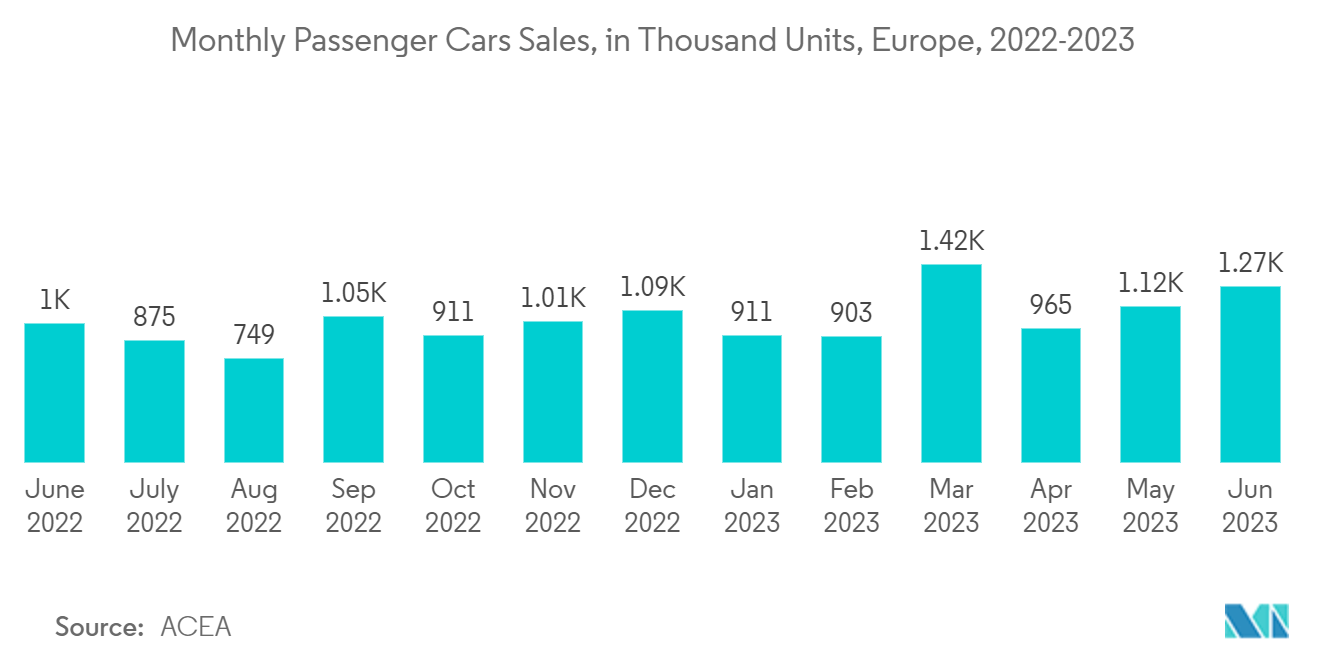

- According to the European Automobile Manufacturers Association (ACEA), the count of passenger car registrations in the European Union reduced by -20.5% in March 2022, with 844,187 units sold. Car production has been harmed by persistent supply chain disruptions, worsened by Russia's invasion of Ukraine. As a result, most nations in the region saw double-digit sales declines, including Spain (-30.2%), Italy (-29.7%), France (-19.5 %), and Germany (-17.5%). This could harm the telematics insurance sector.

Understand The Key Trends Shaping This Market

Download PDF

Italy to Account for the Fastest Growth

- The insurance telematics market in Italy is driven by the rising adoption of telematics-based insurance policies, which offer drivers the opportunity to save money on their premiums by demonstrating safe driving habits.

- The Italian government is constantly supporting the developments of the telematics market with legislation requiring all new cars to be equipped with telematics devices from 2022. This legislation is further expected to drive the growth of the studied market.

- Italian insurtech companies collaborate to bring new options and insurance schemes to Italian customers. This would encourage a smoother transition of the clients from traditional methods of buying vehicle insurance to detailed telematics alternatives.

- According to Istat, as per the initial estimates, the number of road accidents resulting in death or injury has increased by 24.7%, the number of injured by 25.7%, and the number of casualties within 30 days by 15.3% increased from January to June 2022 compared to the same period in 2021. Such increased number of road fatalities is further expected to boost the demand for insurance telematics market.

Get Analysis on Important Geographic Markets

Download PDF