| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 5.50 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe In Vitro Diagnostics (IVD) Market Analysis

The Europe In-Vitro Diagnostics Market is expected to register a CAGR of 5.5% during the forecast period.

The European in vitro diagnostics landscape is experiencing significant transformation driven by the increasing prevalence of chronic diseases and technological advancements in diagnostic testing solutions. According to the International Diabetes Federation, the prevalence of diabetes among adults in Europe is expected to rise from 9.2% to 9.8% by 2030, highlighting the growing need for advanced clinical diagnostics capabilities. The healthcare infrastructure supporting these diagnostic needs continues to expand, with Europe hosting approximately 19,464 hospitals and 4,997 laboratory testing facilities as of 2022. This robust healthcare network facilitates the widespread adoption of innovative diagnostic testing solutions and supports the increasing demand for precise testing methodologies.

The industry is witnessing a notable shift towards automation and integration of advanced technologies in molecular diagnostics procedures. Major industry players are actively developing and launching sophisticated diagnostic platforms that offer improved accuracy and efficiency. For instance, in April 2023, ELITech Group unveiled plans to launch a new high-throughput sample-to-result instrument for molecular diagnostics, demonstrating the industry's commitment to technological advancement. These developments are particularly significant in addressing the growing demand for rapid and accurate diagnostic solutions across various medical conditions.

Strategic collaborations and partnerships are reshaping the competitive landscape of the European in vitro diagnostics market. In June 2023, Seegene Inc. established a strategic partnership with Werfen in Spain to develop syndromic quantitative PCR assays, including those for sexually transmitted infections and drug resistance. Such collaborations are instrumental in expanding product portfolios and enhancing market reach. Additionally, companies are increasingly focusing on developing specialized diagnostic kit solutions for emerging health challenges, as evidenced by Virax Biolabs' March 2023 agreement for distributing Avian Influenza A Virus PCR test kits across the European Union.

The market is characterized by increasing regulatory scrutiny and standardization efforts, particularly in response to the evolving healthcare landscape. The implementation of the In Vitro Diagnostic Regulation (IVDR) in Europe has established more stringent requirements for diagnostic products, ensuring higher safety and performance standards. This regulatory framework has prompted manufacturers to invest in research and development to meet these enhanced requirements while also driving innovation in diagnostic technologies. The industry's response to these regulatory changes has resulted in the development of more sophisticated and reliable diagnostic solutions, ultimately benefiting healthcare providers and patients across Europe.

Europe In Vitro Diagnostics (IVD) Market Trends

Increasing Demand for Point-of-Care Diagnostics

Point-of-care diagnostics offers rapid detection of diseases compared to conventional methods, enabling better diagnosis, monitoring, and management while helping healthcare professionals make quick medical decisions regarding patient care. The rising importance of POC testing in making surgical decisions and improving clinical practice is driving significant market growth, particularly in resource-limited settings. For instance, studies conducted in Germany have demonstrated that point-of-care diagnostics provides various potential benefits, including improved clinical practice through easily applicable tests that provide instant results and allow immediate clinical decisions, enhancing effectiveness, especially in ambulant settings. The National Health Service (NHS) in England has committed substantial investments, planning to launch 40 community diagnostic centers with an investment of GBP 350 million to provide around 2.8 million scans, including POC diagnostic scans.

The advantages offered by point-of-care molecular diagnostics are driving their increased adoption across European healthcare systems. POC tests are currently available for several pathogens, including influenza, tuberculosis, respiratory viruses, chlamydia, and group A streptococcus, utilizing both antigen tests and nucleic acid tests. Studies conducted in Central and Eastern European countries have shown that POC testing leads to faster decision-making, especially in acute cases like sepsis, where rapid diagnosis is crucial for patient safety. Additionally, POC tools such as CRP tests have proven most useful in determining the viral or bacterial origin of diseases, enabling more targeted treatment approaches. The continuous development of new POC technologies and their integration into clinical practice is expected to further drive market growth as healthcare providers increasingly recognize their value in improving patient outcomes.

Understand The Key Trends Shaping This Market

Download PDF

Advancements in Pharmacogenomics and Other Technologies

The field of pharmacogenomics has witnessed significant technological advancement, with the development of high-throughput technologies enabling more comprehensive and extensive approaches to genetic analysis. Advanced Cell Diagnostics (ACD) has developed over 40,000 different RNAscope in situ Hybridization (ISH) probes across more than 400 species, demonstrating the rapid evolution of molecular diagnostic capabilities. These technological developments have led to more accurate and efficient diagnostic tools, particularly in the areas of drug development and molecular diagnosis. The integration of modern techniques such as multigene analysis and whole-genome single nucleotide polymorphism (SNP) profiles is increasing in clinical use, providing more precise and personalized treatment approaches.

The advancement in molecular diagnostic technologies has particularly benefited areas such as cancer research and infectious disease detection. For instance, oligonucleotide fluorescence in situ hybridization (Oligo-FISH) has emerged as a crucial technology in biopharmaceutical research, showing significant success in chromosomal variation detection, allopolyploid identification, and understanding three-dimensional genomic architecture. The development of high-throughput sample-to-result systems and automated platforms has further enhanced the efficiency and accuracy of diagnostic procedures. These technological improvements have led to reduced processing times, increased accuracy in disease detection, and better patient outcomes through more targeted therapeutic approaches.

Possibility of Outbreaks of Bacterial and Viral Epidemics

The increasing frequency and severity of bacterial and viral epidemics across Europe have highlighted the critical need for advanced molecular diagnostic capabilities. Recent surveillance data has shown significant disease outbreaks, with 24,999 RSV cases reported from 261,187 specimens in 2022-2023 in Europe, demonstrating the ongoing challenge of respiratory infections. The emergence of various strains of infectious diseases has created a sustained demand for diagnostic testing, particularly in identifying and characterizing new variants and monitoring disease spread. Healthcare systems across Europe have responded by strengthening their diagnostic capabilities and implementing more comprehensive testing protocols.

The threat of emerging infectious diseases has led to increased investment in diagnostic infrastructure and technology development. For instance, in Denmark, the cumulative number of RSV-related hospital admissions reached 3,323 by December 2022, while the Netherlands reported a sharp increase in laboratory-confirmed RSV cases. The ability to rapidly detect and respond to these outbreaks has become crucial for public health management. This has driven the development and adoption of more sophisticated molecular diagnostic tools capable of detecting multiple pathogens simultaneously, as well as identifying drug-resistant strains. The continuous evolution of pathogens and the emergence of new infectious diseases maintain a constant demand for innovative diagnostic solutions, supporting sustained market growth in the molecular diagnostics sector.

Segment Analysis: By Technology

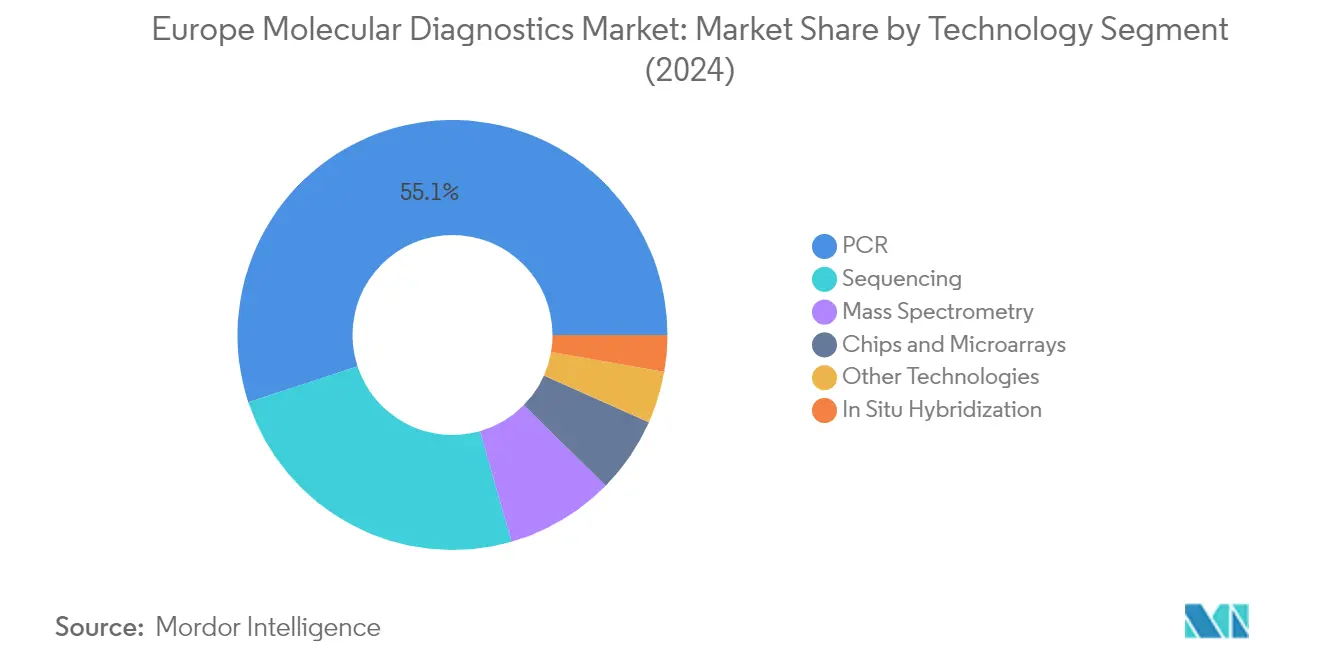

PCR Segment in Europe Molecular Diagnostics Market

The Polymerase Chain Reaction (PCR) segment maintains its dominant position in the European molecular diagnostics market, commanding approximately 55% market share in 2024. PCR technology's widespread adoption is driven by its high sensitivity and specificity in detecting various pathogens, particularly in infectious disease diagnostic testing. The segment's strength is reinforced by continuous technological advancements in PCR platforms, including the development of multiplex PCR assays that can simultaneously detect multiple targets. Major market players are actively expanding their PCR product portfolios through new launches and regulatory approvals, particularly for respiratory pathogen testing panels and other infectious disease applications. The segment's robust performance is also supported by the increasing integration of automation and digital capabilities in PCR systems, making them more efficient and user-friendly for clinical laboratories.

Chips and Microarrays Segment in Europe Molecular Diagnostics Market

The Chips and Microarrays segment is emerging as the fastest-growing technology segment, projected to grow at approximately 10% annually from 2024 to 2029. This impressive growth is driven by the increasing adoption of microarray technology in genetic testing, cancer diagnostics, and pharmacogenomics applications. The segment's expansion is fueled by technological innovations in chip design and analysis capabilities, enabling more comprehensive and accurate genetic analysis. Recent developments in high-throughput screening capabilities and the integration of artificial intelligence in data analysis have significantly enhanced the utility of microarray platforms. The segment is particularly benefiting from the growing demand for personalized medicine and the need for simultaneous analysis of multiple genetic markers in clinical diagnostics.

Remaining Segments in Technology Segmentation

The other significant segments in the molecular diagnostics market include Sequencing, Mass Spectrometry, In Situ Hybridization, and Other Technologies. Sequencing technology continues to play a crucial role in genetic analysis and disease diagnosis, particularly in oncology and rare disease applications. Mass Spectrometry is gaining importance in clinical diagnostics due to its high precision and ability to analyze complex biological samples. In Situ Hybridization maintains its significance in cytogenetic analysis and cancer diagnostics. These segments collectively contribute to the market's technological diversity, offering healthcare providers a comprehensive range of diagnostic solutions for various clinical applications. The continuous innovation and development in these technologies are essential in addressing the evolving needs of molecular diagnostics.

Segment Analysis: By Application

Respiratory Disease Segment in Europe Molecular Diagnostics Market

The respiratory disease segment dominates the European molecular diagnostics market, commanding approximately 52% market share in 2024. This significant market position is driven by the increasing prevalence of various respiratory infections and diseases across Europe. The segment's growth is particularly supported by the rising adoption of molecular diagnostic tests for detecting respiratory pathogens, including influenza, respiratory syncytial virus (RSV), and other respiratory infections. Healthcare facilities across Europe are increasingly implementing advanced molecular diagnostic platforms for rapid and accurate detection of respiratory diseases, enabling faster treatment decisions and better patient outcomes. The segment's dominance is further reinforced by the expanding availability of multiplex PCR tests that can simultaneously detect multiple respiratory pathogens, improving diagnostic testing efficiency and patient care management.

Cancer Segment in Europe Molecular Diagnostics Market

The cancer segment is emerging as one of the fastest-growing segments in the European molecular diagnostics market, with a projected growth rate of approximately 10% during 2024-2029. This robust growth is primarily attributed to the increasing adoption of precision medicine approaches in cancer treatment, which rely heavily on molecular diagnostic testing. The segment is witnessing significant technological advancements in areas such as liquid biopsy, next-generation sequencing, and PCR-based diagnostics for cancer detection and monitoring. Healthcare providers across Europe are increasingly incorporating molecular diagnostic tests for early cancer detection, treatment selection, and monitoring treatment effectiveness. The segment's growth is further supported by the rising focus on personalized cancer treatment approaches and the development of companion diagnostics for targeted cancer therapies.

Remaining Segments in Application Market Segmentation

The European molecular diagnostics market encompasses several other significant segments including gastrointestinal tract infections, genetic disorders, pharmacogenomics, meningitis, bacterial resistance, human papillomavirus (HPV), sepsis, and other applications. Each of these segments plays a crucial role in different aspects of clinical diagnostics and patient care. The gastrointestinal tract infections segment is particularly notable for its comprehensive testing capabilities, while the genetic disorders segment is gaining prominence due to increasing awareness about genetic testing. The pharmacogenomics segment is emerging as a key area in personalized medicine, while segments like meningitis and bacterial resistance are critical for infectious disease management. The HPV segment continues to be important in women's health diagnostics, while the sepsis segment remains crucial for critical care management.

Segment Analysis: By Product

Reagents Segment in Europe Molecular Diagnostics Market

The reagents segment has established itself as the dominant force in the European molecular diagnostics market, commanding approximately 61% of the total market share in 2024. This substantial market presence can be attributed to the increasing demand for molecular diagnostic tests across various applications including respiratory diseases, gastrointestinal tract infections, and cancer diagnostics. The segment's growth is further bolstered by the continuous development and introduction of innovative reagent solutions by key market players, particularly in areas such as PCR testing, sequencing, and other molecular diagnostic techniques. The widespread adoption of these reagents in both clinical and research settings, coupled with their essential role in ensuring accurate and reliable diagnostic testing results, has solidified their position as the cornerstone of molecular diagnostic testing. Additionally, the rising prevalence of infectious diseases and the growing emphasis on early disease detection have significantly contributed to the increased utilization of molecular diagnostic reagents across European healthcare facilities.

Reagents Segment Growth Trajectory in Europe Molecular Diagnostics Market

The reagents segment is projected to maintain its growth momentum, demonstrating the highest growth rate among all product segments during the forecast period 2024-2029, with an expected growth rate of approximately 9% annually. This accelerated growth is driven by several factors, including the increasing adoption of molecular diagnostic testing in personalized medicine, the expansion of testing capabilities in clinical laboratories, and the growing demand for advanced diagnostic testing solutions. The segment's growth is further supported by ongoing technological advancements in reagent formulations, which are enhancing the sensitivity and specificity of molecular diagnostic tests. The rising investment in research and development activities by major market players to develop novel reagent solutions, particularly for emerging applications in oncology and infectious disease diagnostics, is expected to fuel this growth. Moreover, the increasing focus on developing cost-effective and efficient reagent solutions is anticipated to drive market expansion in both established and emerging molecular diagnostic applications.

Remaining Segments in Product Market Segmentation

The instruments and other products segments play crucial complementary roles in the European molecular diagnostics market. The instruments segment encompasses a wide range of diagnostic platforms and equipment essential for performing molecular diagnostic tests, including PCR systems, sequencing platforms, and automated sample preparation systems. These instruments serve as the backbone of molecular diagnostic laboratories, enabling high-throughput testing and accurate results. The other products segment includes various supporting products such as software solutions, calibrators, controls, and other consumables that are integral to the molecular diagnostic workflow. Both segments continue to evolve with technological advancements, with manufacturers focusing on developing more automated, efficient, and user-friendly solutions to meet the growing demands of clinical laboratories and healthcare facilities across Europe.

Segment Analysis: By End User

Hospitals Segment in Europe Molecular Diagnostics Market

The hospitals segment continues to dominate the European molecular diagnostics market, holding approximately 46% market share in 2024. This significant market position is attributed to hospitals' comprehensive diagnostic testing infrastructure, ability to handle high testing volumes, and increasing adoption of advanced molecular diagnostic technologies. The segment's growth is driven by the rising prevalence of infectious diseases, cancer, and genetic disorders requiring molecular testing in hospital settings. Additionally, hospitals are increasingly investing in state-of-the-art molecular diagnostic equipment and expanding their in-house testing capabilities to provide faster results and better patient care. The presence of skilled healthcare professionals and the ability to provide integrated healthcare services further strengthens hospitals' position as the primary end-users in the molecular diagnostics market.

Laboratories Segment in Europe Molecular Diagnostics Market

The laboratories segment is emerging as the fastest-growing end-user segment in the European molecular diagnostics market, with a projected growth rate of approximately 9% from 2024 to 2029. This rapid growth is fueled by the increasing trend of outsourcing diagnostic testing to specialized laboratories, which offer cost-effective and efficient testing services. The segment's expansion is further supported by laboratories' focus on automation, standardization of testing procedures, and investment in advanced molecular diagnostic platforms. Independent laboratories are also strengthening their position by offering comprehensive test menus, maintaining high-quality standards, and providing specialized molecular testing services that many hospitals may not offer in-house. The growing demand for precision medicine and personalized healthcare is expected to further drive the growth of laboratory-based molecular diagnostic services.

Remaining Segments in End User Market Segmentation

The other end-users segment in the European molecular diagnostics market encompasses various healthcare settings such as academic and research institutions, blood banks, and point-of-care testing facilities. These settings play a crucial role in advancing molecular diagnostic technologies through research and development activities. Academic institutions contribute significantly to the validation of new molecular diagnostic methods and techniques, while point-of-care facilities are increasingly adopting molecular diagnostic tests to provide rapid results in community settings. The segment also includes specialized testing centers that focus on specific areas such as genetic testing or cancer diagnostics, contributing to the overall growth and diversification of molecular diagnostic services in Europe.

Segment Analysis: By Test Type

Centralized Laboratory-Based Testing Segment in Europe Molecular Diagnostics Market

The centralized laboratory-based testing segment dominates the European molecular diagnostics market, holding approximately 68% of the market share in 2024. This significant market position is attributed to the segment's ability to efficiently process a high number of samples while maintaining quality and result integrity through automated high-throughput laboratory instruments. The segment's prominence is further strengthened by its comprehensive testing capabilities, advanced automation features, and the ability to handle multiple patient samples and types of tests simultaneously. Centralized laboratories are particularly valued for their role in conducting complex molecular diagnostic procedures, offering economies of scale, and providing standardized testing protocols. The segment's dominance is also supported by the presence of well-established laboratory infrastructure across Europe and the increasing adoption of automated laboratory systems that enhance testing efficiency and accuracy.

Point of Care Testing Segment in Europe Molecular Diagnostics Market

The point of care testing segment is emerging as the fastest-growing segment in the European molecular diagnostics market, projected to grow at approximately 10% CAGR from 2024 to 2029. This rapid growth is driven by the increasing demand for rapid diagnostic testing solutions that enable quick decision-making in clinical settings. The segment's expansion is supported by technological advancements in portable diagnostic devices, improved accuracy of point-of-care tests, and the growing need for immediate test results in emergency and primary care settings. Healthcare facilities are increasingly adopting point-of-care molecular diagnostic solutions to improve patient care outcomes through faster diagnosis and treatment initiation. The segment's growth is further accelerated by the development of more sophisticated, user-friendly devices that can perform complex molecular tests at the point of care, reducing the time between testing and treatment decisions.

Europe In-Vitro Diagnostics Market Geography Segment Analysis

Molecular Diagnostics Market in Germany

Germany stands as the powerhouse of Europe's molecular diagnostics landscape, commanding approximately 17% of the regional market share. The country's dominant position is underpinned by its advanced healthcare infrastructure and robust research capabilities. German healthcare facilities have demonstrated particular strength in adopting innovative molecular diagnostic technologies, especially in areas such as infectious disease testing and cancer diagnostics. The country's healthcare system's emphasis on preventive care and early disease detection has created a strong foundation for molecular diagnostic applications. Furthermore, Germany's position as a hub for biotechnology research and development has attracted significant investments from major molecular diagnostic companies, fostering innovation and market growth. The presence of leading research institutions and medical centers has facilitated the rapid adoption of cutting-edge molecular diagnostic technologies. Additionally, the country's well-established reimbursement policies and healthcare coverage systems have ensured widespread accessibility to molecular diagnostic tests, contributing to market expansion. The market is expected to grow at nearly 11% annually from 2024 to 2029, driven by increasing applications in personalized medicine and genetic testing.

Molecular Diagnostics Market in Italy

Italy's molecular diagnostics market has emerged as a crucial player in Europe's diagnostic landscape, characterized by its comprehensive healthcare system and growing emphasis on preventive medicine. The country's molecular diagnostics sector has shown remarkable resilience and adaptation, particularly in response to emerging healthcare challenges. Italian healthcare providers have increasingly integrated molecular diagnostic technologies into their standard clinical practices, especially in oncology and infectious disease management. The country's strong tradition in medical research and development has fostered innovations in molecular diagnostic techniques and applications. Italian healthcare institutions have demonstrated particular expertise in developing and implementing novel diagnostic approaches for various genetic disorders and infectious diseases. The market has benefited from strong collaboration between academic institutions and industry players, leading to the development of more efficient and accurate diagnostic testing solutions. Furthermore, Italy's aging population has created sustained demand for advanced diagnostic testing solutions, particularly in the areas of chronic disease management and early disease detection.

Molecular Diagnostics Market in France

France has established itself as a significant force in the European molecular diagnostics landscape, supported by its sophisticated healthcare infrastructure and strong emphasis on medical innovation. The French market is characterized by its comprehensive approach to healthcare delivery and strong focus on preventive medicine. The country's molecular diagnostics sector has benefited from substantial government support and investment in healthcare technology. French laboratories and healthcare facilities have shown particular strength in adopting advanced molecular diagnostic techniques for cancer detection and monitoring. The market has also seen significant developments in the field of infectious disease diagnostics, with French institutions playing a crucial role in developing new testing methodologies. The country's well-structured healthcare system, combined with favorable reimbursement policies, has facilitated broad access to molecular diagnostic services. Additionally, France's strong research and development ecosystem has fostered continuous innovation in diagnostic testing technologies and applications.

Molecular Diagnostics Market in Other Countries

The molecular diagnostics market across other European countries, including Spain, the Netherlands, Sweden, Switzerland, and Norway, demonstrates diverse growth patterns and unique market characteristics. These countries have shown varying levels of adoption and implementation of molecular diagnostic technologies, influenced by their respective healthcare systems and regulatory frameworks. Each country brings its unique strengths to the European molecular diagnostics landscape, with Spain showing particular progress in infectious disease diagnostics, Switzerland excelling in precision medicine applications, and the Nordic countries demonstrating leadership in healthcare technology adoption. These markets are characterized by strong healthcare infrastructure, increasing investment in research and development, and growing awareness of personalized medicine benefits. The presence of innovative start-ups and research institutions in these countries continues to drive technological advancements in molecular diagnostics. Furthermore, these nations have demonstrated commitment to advancing their clinical diagnostics capabilities through strategic partnerships and investments in healthcare infrastructure.

Get Analysis on Important Geographic Markets

Download PDF

Europe In Vitro Diagnostics (IVD) Industry Overview

Top Companies in Europe In-Vitro Diagnostics Market

The European in vitro diagnostics market features prominent players like Roche Diagnostics, Danaher Corporation (Cepheid), Abbott Laboratories, and Thermo Fisher Scientific leading the competitive landscape. Companies are increasingly focusing on developing advanced molecular diagnostic instrument platforms incorporating artificial intelligence and automation capabilities to enhance testing efficiency and accuracy. Strategic collaborations with healthcare providers and research institutions have become crucial for expanding market presence and driving innovation. Operational agility is demonstrated through rapid product development cycles and flexible manufacturing capabilities, particularly evident during the COVID-19 pandemic response. Companies are investing heavily in research and development to expand their test menu offerings while simultaneously strengthening their distribution networks across European countries. The market is characterized by continuous product launches, particularly in areas like infectious diseases, oncology, and genetic testing, alongside strategic acquisitions to enhance technological capabilities and market reach.

Consolidated Market with Strong Regional Players

The European in-vitro diagnostics market exhibits a relatively consolidated structure, dominated by large multinational corporations with extensive product portfolios and strong research capabilities. These major players leverage their global presence and financial resources to maintain market leadership through continuous innovation and strategic acquisitions. Regional players maintain a significant presence in specific geographic markets or specialized diagnostic segments, often competing through localized service offerings and established healthcare provider relationships. The market has witnessed increased merger and acquisition activity, particularly targeting companies with innovative molecular diagnostic technologies or strong regional market positions.

The competitive dynamics are shaped by a mix of global conglomerates and specialized diagnostic companies, each bringing unique strengths to the market. Global players benefit from economies of scale and extensive distribution networks, while specialized companies often lead in specific diagnostic technologies or disease areas. Market consolidation continues as larger companies acquire innovative startups and medium-sized players to expand their technological capabilities and geographic reach. The presence of strong local players in key European markets creates a complex competitive landscape requiring nuanced market entry and expansion strategies.

Innovation and Adaptability Drive Market Success

Success in the European IVD market increasingly depends on companies' ability to innovate while maintaining operational efficiency and regulatory compliance. Incumbent companies must focus on continuous product innovation, particularly in emerging areas like molecular diagnostics and point-of-care testing, while maintaining strong relationships with healthcare providers and laboratory customers. Building comprehensive service offerings, including data management solutions and technical support, has become crucial for maintaining market position. Companies must also demonstrate agility in responding to changing healthcare needs and regulatory requirements while maintaining cost competitiveness.

For contenders seeking to gain market share, focusing on specialized diagnostic segments or underserved geographic markets offers promising opportunities. Success requires developing differentiated product offerings, establishing strong local partnerships, and building efficient distribution networks. The relatively high concentration of end-users in hospital and laboratory segments necessitates strong key account management capabilities and customized service offerings. While substitution risk remains moderate due to established diagnostic protocols and regulatory requirements, companies must continuously innovate to maintain competitiveness. Regulatory compliance, particularly with the EU's In Vitro Diagnostic Regulation (IVDR), represents both a challenge and an opportunity for market participants to differentiate themselves through quality and compliance excellence. The integration of diagnostic reagent and clinical diagnostics solutions further enhances the market's adaptability.

Europe In Vitro Diagnostics (IVD) Market Leaders

-

Sysmex Corporation

-

QIAGEN

-

BioMérieux SA

-

F. Hoffmann-La Roche Ltd

-

Illumina, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe In Vitro Diagnostics (IVD) Market News

- In March 2023, MGI Tech Co., Ltd. received the CE mark for the DNBSeq-G99 sequencer with an aim to precise sequencing of genetic substances.

- In December 2022, BioMérieux SA received the CE mark for Vidas Kube automated immunoassay system to diagnose immunochemistry, infectious diseases, and food industry pathogens.

- In September 2022, Noul Co., Ltd. received the CE-IVD mark for two next-generation diagnostic testing products, miLab Cartridge CER and miLab Cartridge BCM to expand its product line in in-vitro diagnostics systems.

Europe In Vitro Diagnostics (IVD) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 High Prevalence of Chronic Diseases

- 4.2.2 Increasing Demand for Point-of-care Diagnostics

- 4.2.3 Technological Advancements in In-Vitro Diagnostics Devices

-

4.3 Market Restraints

- 4.3.1 Stringent Regulations

- 4.3.2 Cumbersome Reimbursement Procedures

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Molecular Diagnostics

- 5.1.3 Hematology

- 5.1.4 Immuno Diagnostics

- 5.1.5 Other Test Types

-

5.2 By Product

- 5.2.1 Instrument

- 5.2.2 Reagents

- 5.2.3 Other Products

-

5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Reusable IVD Devices

-

5.4 By Application

- 5.4.1 Infectious Disease

- 5.4.2 Diabetes

- 5.4.3 Cancer/Oncology

- 5.4.4 Cardiology

- 5.4.5 Autoimmune Disease

- 5.4.6 Nephrology

- 5.4.7 Other Applications

-

5.5 By End User

- 5.5.1 Diagnostic Laboratories

- 5.5.2 Hospitals and Clinics

- 5.5.3 Other End Users

-

5.6 Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Bio-Rad Laboratories Inc.

- 6.1.4 Danaher Corporation (Beckman Coulter, Inc)

- 6.1.5 Hologic, Inc.

- 6.1.6 Roche Diagnostics

- 6.1.7 Siemens Healthcare

- 6.1.8 Thermo Fisher Scientific Inc.

- 6.1.9 Sysmex Corporation

- 6.1.10 QIAGEN

- 6.1.11 BioMerieux SA

- 6.1.12 Tesa SE

- 6.1.13 Diasorin S.p.A

- 6.1.14 Illumina, Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe In Vitro Diagnostics (IVD) Industry Segmentation

As per the scope of this report, in-vitro diagnostics are the tests performed in laboratories or by consumers at home to diagnose, monitor, screen, and assess various diseases, conditions, or infections. IVD products are reagents, instruments, and systems intended for use in diagnosing diseases or other conditions. IVDs form an essential part of the current healthcare system. They reduce hospital stays and the need to recuperate. The Europe In-Vitro Diagnostics Market is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Immuno Diagnostics, Hematology, and Other Test Types), Product (Instruments, Reagents, and Other Products), Usability (Disposable IVD Devices and Reusable IVD Devices), Application (Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disease, Nephrology, and Other Applications), End User (Diagnostic Laboratories, Hospitals and Clinics, and Other End Users) and Geography (Germany, United Kingdom, France, Italy, Spain, and the Rest of Europe). The report offers the value (in USD million) for the above segments.

| By Test Type | Clinical Chemistry |

| Molecular Diagnostics | |

| Hematology | |

| Immuno Diagnostics | |

| Other Test Types | |

| By Product | Instrument |

| Reagents | |

| Other Products | |

| By Usability | Disposable IVD Devices |

| Reusable IVD Devices | |

| By Application | Infectious Disease |

| Diabetes | |

| Cancer/Oncology | |

| Cardiology | |

| Autoimmune Disease | |

| Nephrology | |

| Other Applications | |

| By End User | Diagnostic Laboratories |

| Hospitals and Clinics | |

| Other End Users | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe In Vitro Diagnostics (IVD) Market Research FAQs

What is the current Europe In-Vitro Diagnostics Market size?

The Europe In-Vitro Diagnostics Market is projected to register a CAGR of 5.5% during the forecast period (2025-2030)

Who are the key players in Europe In-Vitro Diagnostics Market?

Sysmex Corporation, QIAGEN, BioMérieux SA, F. Hoffmann-La Roche Ltd and Illumina, Inc. are the major companies operating in the Europe In-Vitro Diagnostics Market.

What years does this Europe In-Vitro Diagnostics Market cover?

The report covers the Europe In-Vitro Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe In-Vitro Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe In-Vitro Diagnostics Market Research

Mordor Intelligence provides a comprehensive analysis of the in vitro diagnostics industry. This analysis combines expertise in laboratory testing and clinical diagnostics research. Our detailed report, available as an easy-to-download PDF, covers crucial segments such as blood testing, genetic testing, and molecular diagnostics. The analysis includes clinical chemistry, immunodiagnostics, and laboratory diagnostics. It offers stakeholders essential insights into diagnostic testing methodologies and technological advancements in clinical immunology.

The report benefits industry participants by offering a detailed analysis of POCT solutions and developments in rapid diagnostics. It also examines the evolution of companion diagnostics and point of care diagnostics. Stakeholders gain valuable insights into diagnostic kit manufacturing, diagnostic reagent formulation, and innovations in diagnostic instrument technologies. The coverage extends to emerging fields such as microbiology diagnostics, applications of diagnostic biomarkers, and hematology diagnostics. It includes an analysis of diagnostic analyzer technologies and their implementation across European healthcare systems.