Europe Hybrid Electric Vehicle Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

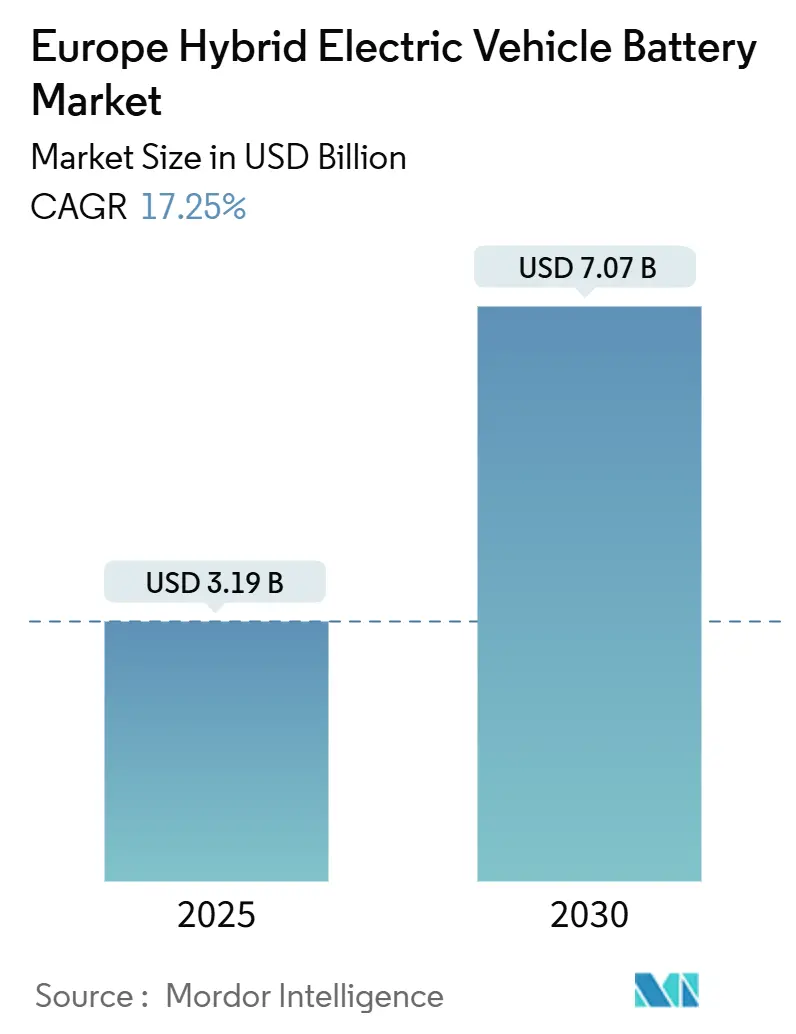

| Market Size (2025) | USD 3.19 Billion |

| Market Size (2030) | USD 7.07 Billion |

| Growth Rate (2025 - 2030) | 17.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hybrid Electric Vehicle Battery Market Analysis by Mordor Intelligence

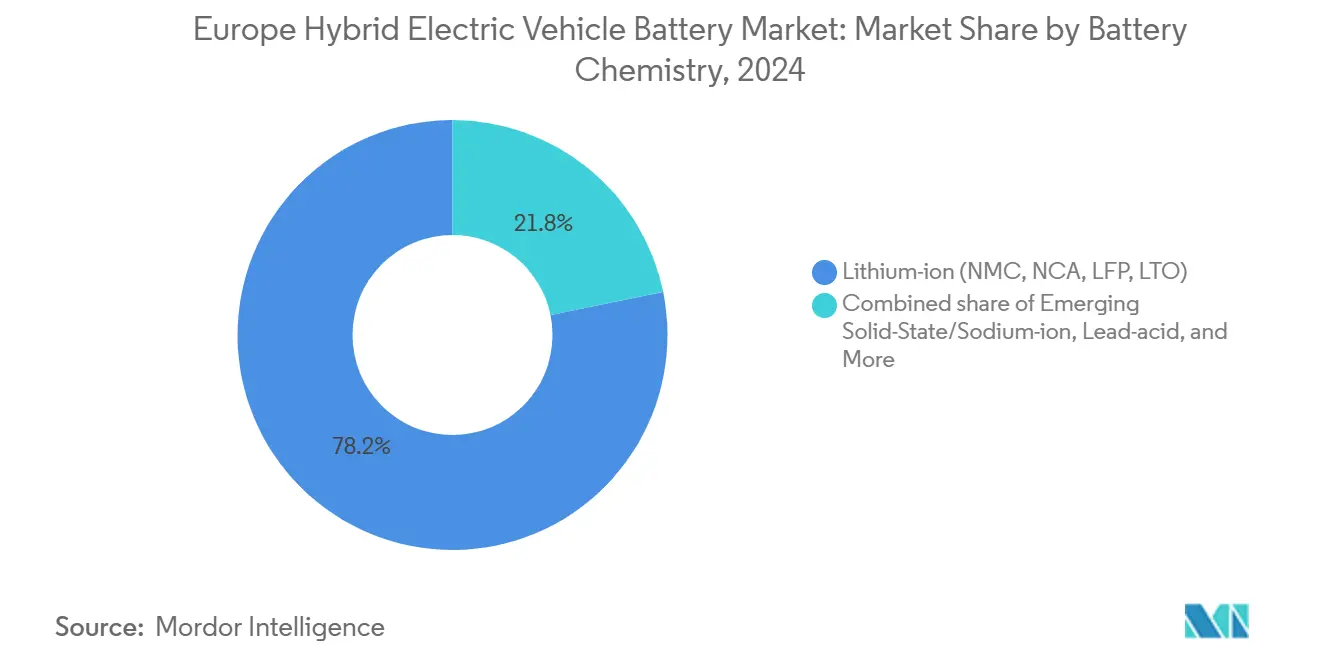

The Europe hybrid electric vehicle battery market size reached USD 2.79 billion in 2024 and is projected to advance at a 17.25% CAGR to USD 7.07 billion by 2030, underscoring the region’s rapid pivot toward electrified propulsion and reflecting robust demand for 48-volt mild-hybrid packs that help automakers satisfy EU fleet-average CO₂ rules.[1]European Commission, “Proposal for CO₂ Emission Performance Standards,” ec.europa.eu Mild-hybrid penetration is climbing ahead of full and plug-in variants because the technology delivers 10-15% fuel-economy gains at roughly one-third the system cost of a full hybrid, preserving margin while avoiding expensive charging infrastructure build-outs.[2]Stellantis, “2024 Electrification Strategy,” stellantis.com Li-ion chemistries dominated in 2024 with 78.2% volume, as cell makers chase lower material cost and supply-chain resilience. Asian suppliers still account for about 60% of the installed European capacity, but fresh gigafactory investments in Spain, Hungary, and Poland are cutting logistics lead times and positioning domestic entrants for future share gains.

Key Report Takeaways

- By degree of hybridization, mild hybrids led with 47.5% revenue share of the European hybrid electric vehicle battery market in 2024; plug-in hybrids are anticipated to post the highest CAGR at 19.6% through 2030.

- By battery chemistry, lithium-ion commanded 78.2% share of the European hybrid electric vehicle battery market size in 2024 and is forecast to register a 16.0% CAGR during 2025-2030.

- By vehicle class, passenger cars captured 61.8% of the European hybrid electric vehicle battery market share in 2024, while commercial vehicles are projected to expand at a 23.1% CAGR to 2030.

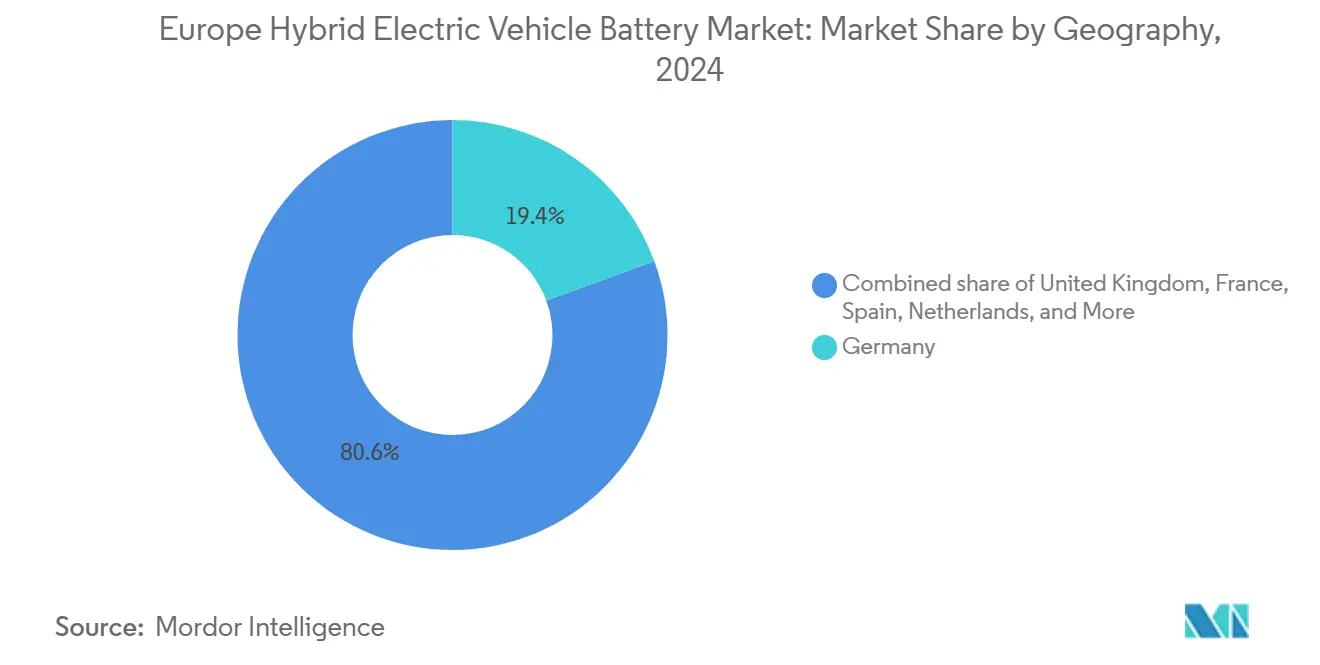

- By geography, Germany accounted for 19.4% revenue share of the European hybrid electric vehicle battery market in 2024; Spain is on track to log the fastest CAGR at 22.9% over the forecast period.

- LG Energy Solution, Samsung SDI, CATL, Panasonic, and SK On collectively held about 60% of 2024 cell manufacturing capacity in the region.

Europe Hybrid Electric Vehicle Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HEV production volumes aligned with EU CO₂ fleet targets | 4.20% | EU-wide, strongest in Germany, France, Italy | Short term (≤ 2 years) |

| Gigafactory investments in CEE region localizing supply chains | 3.80% | Poland, Hungary, Czech Republic, Slovakia | Medium term (2-4 years) |

| Declining lithium-ion pack prices in Europe | 2.10% | EU-wide, especially Spain, Germany | Short term (≤ 2 years) |

| EU sustainable-battery regulation incentives | 2.90% | EU-wide, early compliance in Nordics | Medium term (2-4 years) |

| Surge in 48-V mild-hybrid architectures | 3.50% | Germany, UK, France, Italy | Short term (≤ 2 years) |

| Emergence of sodium-ion batteries for low-cost hybrids | 1.00% | Spain, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HEV Production Volumes Aligned With EU CO₂ Fleet Targets

Automakers must meet the 2025 fleet-average ceiling of 93.6 g/km, reduced from 115.1 g/km in 2021, or pay EUR 95 for every excess gram per vehicle sold, pushing brands to standardize hybrid powertrains across high-volume B- and C-segment models. Stellantis, Renault, and Volkswagen expanded 48-volt offerings in 2024, each leveraging belt-starter-generator systems that shave roughly 12 g/km from type-approval emissions for less than a EUR 1,000 cost premium. Because super-credits for zero and low-emission vehicles can still be applied through 2025, building hybrids today generates compliance headroom while BEV infrastructure scales. This rule architecture therefore locks in baseline demand for lithium-ion cells through at least 2027, after which the stricter 2030 targets will intensify electrification pressure.

Gigafactory Investments in CEE Region Localizing Supply Chains

Over EUR 15 billion was committed to new cell plants in Hungary, Poland, and Slovakia during 2024, led by CATL’s 100 GWh Debrecen facility and LG Energy Solution’s Wrocław expansion to 70 GWh. The labor arbitrage of 15-20% versus Western Europe, plus just-in-time proximity to German assembly hubs, trims pack lead times to under 24 hours. European Battery Alliance co-financing is accelerating upstream cathode precursor and separator projects that substitute Asia-origin inputs, simultaneously lowering embedded CO₂ per kWh. As carbon-footprint declarations become mandatory, local supply chains gain a strategic advantage.

Surge in 48-V Mild-Hybrid Architectures

Mild-hybrid packs of 0.5-1.5 kWh captured 47.5% revenue in 2024 and are on pace for a 19.6% CAGR through 2030. Peugeot 308, Opel Astra, and multiple Mercedes-Benz models now integrate 48-volt systems, enabling engine-off coasting and torque fill.[3]Mercedes-Benz Group, “48-V Powertrain Technical Brief,” group.mercedes-benz.com Typical incremental cost remains below EUR 1,000, a fraction of full-hybrid outlays, making the format the default compliance lever for mass-market platforms until charging networks are universal.

EU Sustainable-Battery Regulation Incentives

Regulation (EU) 2023/1542 enforces minimum recycled-content levels and lifecycle CO₂ disclosure from 2025 onward, fundamentally shifting sourcing logic toward low-carbon production and closed-loop recycling.[4]CATL, “Debrecen Gigafactory Announcement,” catl.com Northvolt’s Skellefteå plant and Volkswagen’s forthcoming Sagunto site both rely on >90% renewable energy, pushing lifecycle emissions below 50 kg CO₂/kWh. Automakers embed the compliance premium, estimated at EUR 50-80/kWh, directly in supply contracts, creating a quasi-subsidy for domestic cell fabrication and encouraging cobalt-free sodium-ion for entry-level hybrids.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical mineral cost volatility | −2.7% | EU-wide, affects NMC users | Short term (≤ 2 years) |

| OEM cap-ex shift toward full-BEV platforms | −3.1% | Germany, France, UK, Sweden | Medium term (2-4 years) |

| Cross-border battery-transport regulatory complexity | −0.8% | EU corridors | Short term (≤ 2 years) |

| Rise of hydrogen ICE hybrids diverting investment | −0.4% | Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical Mineral Cost Volatility

Lithium carbonate prices collapsed from USD 80,000/t in late 2022 to near USD 10,000/t by December 2024, while nickel sulfate swung USD 7,000/t inside a single year. Such turbulence compresses margins on fixed-price supply deals, particularly for smaller European entrants lacking vertical integration. Investors now demand price-adjustment clauses or equity stakes in upstream mines before funding capacity expansions, delaying several gigafactory timelines.

OEM Cap-ex Shift Toward Full-BEV Platforms

Volkswagen has earmarked EUR 180 billion for electrification through 2028, dedicating 60% to BEV-native architectures that de-prioritize hybrid R&D. Stellantis plans only BEV-derived platforms after 2027, and Mercedes-Benz trimmed its PHEV lineup by 30% in 2024. This reallocation constrains long-term hybrid battery demand and signals that future procurement will pivot toward cylindrical 4680 and prismatic LFP cells optimized for BEVs, raising stranded-asset risk at plants tuned to pouch-cell hybrid volumes.

Segment Analysis

By Battery Chemistry: LFP Broadens Reach While Solid-State Targets Premium PHEVs

Lithium-ion held 78.2% of 2024 demand, with high-nickel NMC variants powering plug-in hybrids that require 250-280 Wh/kg energy density. LFP gained share in mild-hybrids owing to 3,000-cycle durability and cobalt-free supply chains, a feat demonstrated by BYD’s Blade pack that cut system cost 30% for Stellantis models. Emerging sodium-ion and solid-state formats should grow 32.2% annually yet remain sub-scale until after 2026, when Northvolt’s pilot line in Sweden starts series output for entry-level hybrids. Nickel-metal-hydride slipped to 8% share as Toyota transitioned to new European releases to lithium-ion. The European hybrid electric vehicle battery market sees chemistry bifurcation: cost-sensitive mild hybrids gravitate to LFP and sodium-ion, performance-oriented PHEVs keep high-nickel NMC, and ultra-premium variants pilot solid-state cells.

Advanced chemistries introduce recycling complexity. Solid-state packs using sulfide electrolytes demand novel dismantling and recovery steps that few European recyclers are ready to scale. Simultaneously, cobalt-free formats lighten obligations under Regulation 2023/1542, saving OEMs the EUR 50-80/kWh compliance premium attached to high cobalt content cells. These shifts require gigafactories to design flexible lines capable of chemistry switching without extended downtime, a capability that entrenched Asian incumbents already demonstrate, and new European players must replicate quickly.

Note: Segment shares of all individual segments available upon report purchase

By Degree of Hybridization: Mild Gains Persist, PHEVs Test Policy Headwinds

The European hybrid electric vehicle battery market recorded 47.5% revenue from mild hybrids in 2024, and this cohort will compound 19.6% annually to 2030. System costs as low as EUR 800 make 48-volt the dominant compliance lever for models such as the Volkswagen Golf and Renault Clio. Full hybrids, typified by Toyota’s e-CVT system, held a 28% share yet face a slower 11% CAGR as European brands redirect engineering budgets. Plug-in hybrids claimed 21% revenue but are vulnerable after Germany and the UK scrapped purchase incentives, eroding total-cost-of-ownership parity with BEVs.

Real-world usage data compounds the pressure. A 2024 Transport & Environment study found fleet PHEVs drive less than half their kilometers in electric mode, prompting policymakers to consider tougher utility-factor testing. Absent tax breaks, buyers gravitate either to lower-cost mild hybrids or to BEVs as charging networks improve. Range-extender designs remain below 3% share due to packaging complexity and are unlikely to scale before 2030.

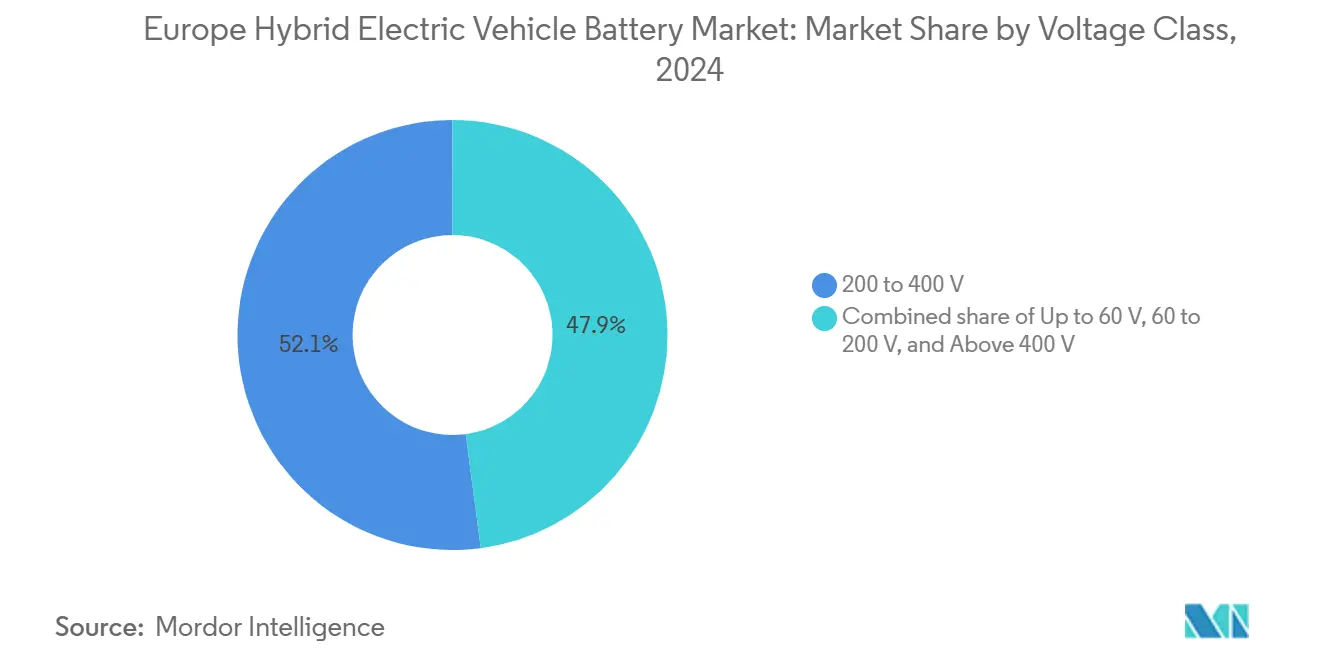

By Voltage Class: 800-Volt Platforms Move From BEVs to Premium PHEVs

Voltage architecture delineates clear performance tiers inside the European hybrid electric vehicle battery market. Systems in the 200-400 V range still owned 52.1% share during 2024, powering mainstream mild and full hybrids. Yet adoption of 800-V platforms in plug-in models such as Porsche’s Cayenne E-Hybrid is pushing the above-400 V band to a 21.8% CAGR. Charging from 10-80% in about 11 minutes aligns user expectations with premium BEVs, and the reduced copper mass lowers vehicle weight.

The up-to-60 V class, essentially 48-V, accounted for a 35% share and will grow 18% annually as cost-focused OEMs deploy belt-starter-generators across entry-level segments. Voltage harmonization across hybrid and BEV lines allows platform reuse of inverters and motors, feeding economies of scale. Infrastructure remains a limiting factor: just 12% of European public chargers supplied 350 kW output in 2024. Still, future-proofing arguments compel OEMs to embed 800-V readiness even if public charging lags, setting the stage for rapid capability unlock once the grid catches up.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Class: Logistics Electrification Accelerates Commercial Segment

Passenger cars generated 61.8% of 2024 revenue inside the European hybrid electric vehicle battery market, driven by compliance-focused mild-hybrid adoption in high-volume C-segment hatchbacks. Commercial vehicles, however, will be the fastest grower at 23.1% CAGR to 2030, lifted by zero-emission zones in more than 300 cities and fleet managers seeking diesel cost hedges. Volvo Trucks delivered 1,200 hybrid distribution trucks in 2024, and Daimler’s eCitaro hybrid captured 18% of electric-bus orders, showing municipalities value the range security a back-up combustion unit provides. Yet payload penalties remain. Hybrid drivetrains add up to 500 kg, cutting capacity, and affecting the total cost. Parity depends on diesel staying above EUR 1.50/L and annual mileage topping 50,000 km, conditions found mostly in urban parcel delivery. Off-highway equipment, a 3% share niche, nevertheless benefits from hybrid cycles that slash idle fuel consumption by 30%, making excavators and loaders early adopters in Scandinavia’s construction sector.

Geography Analysis

Germany delivered 19.4% of the 2024 European hybrid electric vehicle battery market revenue due to concentrated Volkswagen, BMW, and Mercedes-Benz production footprints. CATL’s Erfurt and LG Energy Solution’s Wrocław plants feed German lines within 24 hours, enabling chemistry swaps on short notice. Although subsidy withdrawals pose headwinds, the market still projects a 14.8% CAGR through 2030 as commercial-vehicle hybrids expand in urban freight corridors such as Berlin and Hamburg.

Spain is set to be the region’s growth engine at 22.9% CAGR, buoyed by EUR 3 billion of government co-financing under the PERTE program and Volkswagen’s 40 GWh Sagunto plant that will leverage low-cost solar power to hit sub-50 kg CO₂/kWh footprints. Basquevolt’s solid-state pilot line promises local premium-segment supply from 2027, reinforcing Spain’s ambition to anchor a full value chain from raw materials to packs.

France, the UK, and Italy collectively held a 28% share in 2024. France’s Automotive Cells Company delayed its Douvrin ramp-up, reflecting a softer PHEV outlook, yet long-term demand remains underpinned by Stellantis models. The UK is luring investments via the Advanced Propulsion Centre’s GBP 350 million grant scheme, enticing Tata and Envision AESC to scale beyond 70 GWh combined. Italy’s Italvolt project targets 45 GWh by 2027 despite financing hurdles, eyeing supply contracts with both Stellantis and incoming Chinese OEMs.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

Market concentration is moderate. The five largest suppliers command about 60% of capacity, led by LG Energy Solution’s Poland and Hungary footprints, Samsung SDI’s expanded Göd campus, and CATL’s new Debrecen super-plant. Each is pursuing upstream acquisitions to buffer mineral volatility; LG’s 20% stake in Liontown Resources locks 150,000 t/y spodumene supply.

European challengers encounter scale and capital gaps. Northvolt’s September 2024 bankruptcy filing illustrated execution risk when ramp delays meet surging interest rates and cautious automaker offtake. Automotive Cells Company, Verkor, and FREYR continue to seek blended financing from the European Investment Bank, strategic OEMs, and sovereign funds.

Technology differentiation is intensifying. BYD’s Blade and CATL’s Qilin cell-to-pack structures lower mass 10-15% and shave USD 10-15/kWh from cost, forcing rivals toward similar structural designs. Solid-state patent filings rose 40% YoY in 2024, yet manufacturing readiness lags by at least four years, suggesting incumbents will commercialize step-change improvements before disruptors scale.

Europe Hybrid Electric Vehicle Battery Industry Leaders

-

Panasonic Holdings Corporation

-

LG Energy Solution

-

Samsung SDI Co., Ltd.

-

CATL Europe (subs. of CATL)

-

Northvolt AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Northvolt AB filed for Chapter 11 protection after cost overruns and contract cancellations left USD 5.8 billion in debt, triggering restructuring talks with Volkswagen and BMW.

- August 2024: CATL began trial output at its 100 GWh Debrecen plant, Europe’s largest battery facility, with commercial deliveries scheduled for Q1 2025.

- July 2024: Volkswagen’s PowerCo broke ground on the 40 GWh Sagunto gigafactory in Spain with EUR 3 billion in public co-financing.

- June 2024: LG Energy Solution inked a 10-year, 200 GWh supply pact with Volkswagen covering cylindrical 4680 and prismatic cells sourced from Poland and Hungary lines.

Europe Hybrid Electric Vehicle Battery Market Report Scope

A Hybrid Electric Vehicle (HEV) battery is a rechargeable energy storage system that powers the electric motor of a hybrid vehicle. HEVs combine a conventional internal combustion engine (ICE) with an electric propulsion system. The battery in an HEV is crucial for capturing and storing energy, particularly during regenerative braking, and for providing additional power during acceleration.

Europe's hybrid electric vehicle battery market is Segmented By Battery Chemistry (Lithium-ion (NMC, NCA, LFP, LTO), Nickel-Metal Hydride (NiMH), Lead-acid, Emerging Solid-State/Sodium-ion), By Degree of Hybridization (Mild Hybrid (48 V MHEV), Full Hybrid (HEV), Plug-in Hybrid (PHEV), Range-Extender Hybrid), By Voltage Class (Up to 60 V, 60 to 200 V, 200 to 400 V, Above 400 V), By Vehicle Class (Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, Off-Highway and Specialty), By Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Norway, Russia, Rest of Europe). The report also covers the market size and forecasts for Europe's hybrid electric vehicle battery market across major countries. The Report Offers the Market Size and Forecasts in Revenue (USD) for all the Above.

| Lithium-ion (NMC, NCA, LFP, LTO) |

| Nickel-Metal Hydride (NiMH) |

| Lead-acid |

| Emerging Solid-State/Sodium-ion |

| Mild Hybrid (48 V MHEV) |

| Full Hybrid (HEV) |

| Plug-in Hybrid (PHEV) |

| Range-Extender Hybrid |

| Up to 60 V |

| 60 to 200 V |

| 200 to 400 V |

| Above 400 V |

| Passenger Cars |

| Commercial Vehicles |

| Two-/Three-Wheelers |

| Off-Highway and Specialty |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Norway |

| Russia |

| Rest of Europe |

| By Battery Chemistry | Lithium-ion (NMC, NCA, LFP, LTO) |

| Nickel-Metal Hydride (NiMH) | |

| Lead-acid | |

| Emerging Solid-State/Sodium-ion | |

| By Degree of Hybridization | Mild Hybrid (48 V MHEV) |

| Full Hybrid (HEV) | |

| Plug-in Hybrid (PHEV) | |

| Range-Extender Hybrid | |

| By Voltage Class | Up to 60 V |

| 60 to 200 V | |

| 200 to 400 V | |

| Above 400 V | |

| By Vehicle Class | Passenger Cars |

| Commercial Vehicles | |

| Two-/Three-Wheelers | |

| Off-Highway and Specialty | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe hybrid electric vehicle battery market in 2025?

It is estimated at USD 3.19 billion, progressing toward USD 7.07 billion by 2030 under a 17.25% CAGR.

Which battery chemistry is growing fastest in European hybrids?

Emerging sodium-ion and solid-state chemistries are set to expand at roughly 32% CAGR, although they remain pre-commercial until after 2026.

Why are 48-volt mild hybrids so popular in Europe?

They cut fuel use 10-15% at under EUR 1,000 incremental cost, making them the cheapest route to meet EU CO₂ targets without charging infrastructure.

Which country will be the fastest-growing European market for hybrid batteries?

Spain is forecast to deliver a 22.9% CAGR through 2030 thanks to strong public funding and multiple new gigafactories.

What share of capacity do Asian suppliers hold in Europe?

LG Energy Solution, Samsung SDI, CATL, Panasonic, and SK On together control roughly 60% of installed European cell manufacturing capacity.

What new EU rules affect battery suppliers after 2024?

Regulation (EU) 2023/1542 mandates lifecycle CO₂ disclosure from 2025 and minimum recycled-content thresholds starting 2026, reshaping sourcing and recycling strategies.

Page last updated on: